Middle East And Africa Leber Congenital Amaurosis Market

Market Size in USD Million

USD

45.00 Million

USD

55.68 Million

2025

2033

USD

45.00 Million

USD

55.68 Million

2025

2033

| 2026 - 2033 | |

| USD 45.00 Million | |

| USD 55.68 Million | |

| % | |

|

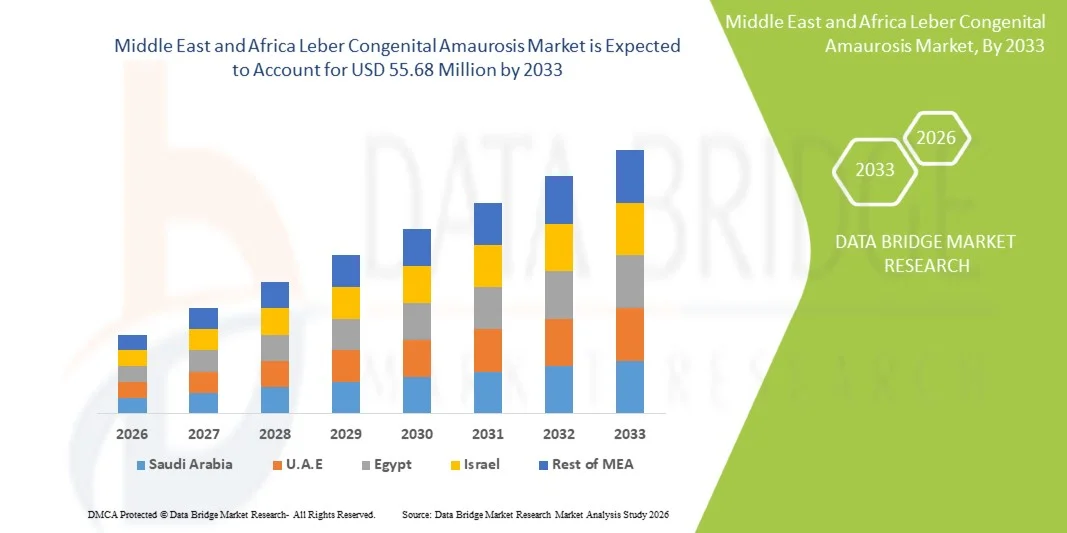

Middle East and Africa Leber Congenital Amaurosis Market Size

- The Middle East and Africa Leber Congenital Amaurosis market size was valued at USD 45.00 million in 2025 and is expected to reach USD 55.68 million by 2033, at a CAGR of 2.7% during the forecast period

- The market growth is primarily driven by increasing awareness of rare inherited retinal disorders, expanding access to genetic testing, and gradual improvements in ophthalmic healthcare infrastructure across key Middle Eastern and African countries

- Furthermore, rising focus on early diagnosis, supportive government healthcare initiatives, and emerging advancements in gene therapy and precision medicine are enhancing treatment prospects, thereby supporting steady market expansion across the region

Middle East and Africa Leber Congenital Amaurosis Market Analysis

- Leber Congenital Amaurosis is a rare inherited retinal disorder market characterized by severe vision impairment from birth or early infancy, and it is gradually gaining traction due to improving genetic diagnostic capabilities, rising awareness of rare eye diseases, and the slow expansion of specialized ophthalmology care across key countries in the region

- The escalating demand in the Middle East and Africa Leber Congenital Amaurosis market is primarily driven by increasing adoption of genetic testing for early diagnosis, growing clinical recognition of inherited retinal disorders, and improving access to advanced ophthalmic services, along with emerging research activity in gene-based treatment approaches

- Saudi Arabia dominated the Middle East and Africa Leber Congenital Amaurosis market with the largest share of 38.5% in 2025, supported by strong healthcare infrastructure, government-backed rare disease programs, and wider availability of genetic screening and specialized eye care services

- South Africa is expected to be the fastest growing country in the Middle East and Africa Leber Congenital Amaurosis market during the forecast period due to improving diagnostic facilities, increasing healthcare investments, and expanding awareness and identification of rare genetic eye disorders

- Therapy segment dominated the Middle East and Africa Leber Congenital Amaurosis market with the largest share of 46.2% in 2025, driven by growing clinical reliance on supportive and emerging gene-based therapies, increasing treatment-oriented care pathways, and rising focus on managing disease progression and preserving residual vision in affected patients

Report Scope and Middle East and Africa Leber Congenital Amaurosis Market Segmentation

|

Attributes |

Middle East and Africa Leber Congenital Amaurosis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Middle East and Africa Leber Congenital Amaurosis Market Trends

“Rising Adoption of Genetic Diagnosis and Precision Medicine in Rare Eye Disorders”

- A significant and emerging trend in the Middle East and Africa Leber Congenital Amaurosis market is the increasing integration of genetic testing and precision medicine approaches for early and accurate diagnosis of inherited retinal disorders, improving clinical identification rates across specialized healthcare centers

- For instance, hospitals in Saudi Arabia and the UAE are increasingly adopting next-generation sequencing panels for retinal dystrophies, enabling faster confirmation of Leber Congenital Amaurosis and improving patient referral to specialized ophthalmology and genetic counseling services

- Advances in gene therapy research and rare disease registries are supporting more structured disease management approaches, with some clinical centers beginning to participate in early-stage trials focused on RPE65 and related gene mutations associated with Leber Congenital Amaurosis

- The expansion of specialized ophthalmic centers and rare disease programs is enabling better integration of diagnostic, counseling, and supportive care services within a single treatment pathway for affected patients

- Increasing collaboration between international biotech firms and regional hospitals is accelerating access to experimental gene therapies and encouraging knowledge transfer in advanced retinal disease management approaches

- Growing digital health adoption, including tele-ophthalmology services, is improving patient screening and follow-up in remote areas, supporting earlier detection of Leber Congenital Amaurosis cases

Middle East and Africa Leber Congenital Amaurosis Market Dynamics

Driver

“Increasing Awareness and Expansion of Genetic and Ophthalmic Care Infrastructure”

- The increasing awareness of inherited retinal disorders among clinicians and patients, coupled with gradual improvements in genetic testing infrastructure, is a key driver for the Middle East and Africa Leber Congenital Amaurosis market growth

- For instance, in April 2025, major tertiary eye care hospitals in Saudi Arabia expanded rare disease screening programs to include routine genetic evaluation for pediatric patients with early-onset vision impairment

- Growing government focus on rare disease diagnosis and improved healthcare funding is enhancing access to advanced ophthalmology services in key countries such as Saudi Arabia and South Africa

- Rising availability of specialized ophthalmic clinics and genetic counseling services is improving early detection rates and supporting timely disease management strategies for affected patients

- Increasing collaboration between international research organizations and regional healthcare providers is further accelerating awareness and adoption of advanced diagnostic approaches in the market

- Expanding medical training programs for ophthalmologists in rare retinal disorders is improving diagnostic accuracy and strengthening clinical capacity across major healthcare institutions

Restraint/Challenge

“Limited Early Diagnosis Rates and High Cost of Advanced Genetic and Therapeutic Solutions”

- Limited early diagnosis rates due to low awareness in rural and underserved areas, combined with restricted access to advanced genetic testing facilities, poses a significant challenge to the Middle East and Africa Leber Congenital Amaurosis market expansion

- For instance, in several African countries, delayed diagnosis of pediatric vision disorders remains common due to limited availability of specialized ophthalmologists and genetic testing laboratories

- The high cost of gene therapy development and advanced diagnostic procedures limits widespread adoption, particularly in lower-income healthcare systems across parts of the region

- Regulatory and infrastructure gaps in rare disease management further slow the introduction of advanced treatment options and clinical trial participation in certain countries

- Shortage of skilled genetic counselors and retinal specialists restricts effective patient management and delays appropriate treatment referral in many healthcare systems

- Limited reimbursement frameworks for rare disease diagnostics and therapies reduces patient affordability and slows overall market penetration in several Middle East and Africa countries

Middle East and Africa Leber Congenital Amaurosis Market Scope

The market is segmented on the basis of disease type, type, end user, and distribution channel.

- By Disease Type

On the basis of disease type, the Middle East and Africa Leber Congenital Amaurosis market is segmented into infantile type, juvenile type, and other. The infantile type segment dominated the market with the largest revenue share of 52.4% in 2025, driven by its early onset manifestation within the first few months of life, leading to earlier clinical detection and higher diagnosis rates in pediatric ophthalmology settings. This subtype is more frequently identified in advanced healthcare centers due to severe visual impairment symptoms prompting early medical intervention. Increasing use of genetic testing in newborn screening programs, particularly in countries such as Saudi Arabia, further supports dominance. Hospitals and specialty clinics also prioritize infantile cases for early intervention and counseling services. Rising awareness among pediatricians regarding congenital vision disorders is contributing to higher reported cases. Additionally, improved access to retinal imaging technologies is strengthening diagnosis accuracy for this segment.

The juvenile type segment is expected to witness the fastest growth rate of 7.1% from 2026 to 2033, driven by improved diagnostic capabilities and delayed detection of milder or progressive cases. Many juvenile cases are diagnosed later due to subtle symptom progression, leading to increasing identification as genetic screening becomes more widespread. Expanding ophthalmology outreach programs in South Africa and UAE are improving detection rates among older pediatric populations. Rising availability of next-generation sequencing is enabling confirmation of late-onset genetic mutations linked to Leber Congenital Amaurosis. Growing awareness among general physicians and optometrists is also contributing to higher referrals. Furthermore, improved patient survival and follow-up systems are increasing recorded prevalence in this segment.

- By Type

On the basis of type, the market is segmented into therapy and diagnosis. The therapy segment dominated the market with the largest revenue share of 46.2% in 2025, driven by increasing reliance on supportive treatments, emerging gene therapy interventions, and long-term disease management strategies. Although curative options remain limited, growing clinical adoption of gene-based research therapies is strengthening this segment. Hospitals in Saudi Arabia and UAE are increasingly involved in early-stage clinical trials for retinal gene therapies. Supportive treatments such as visual rehabilitation and low-vision aids also contribute to therapy demand. Rising investment in rare disease treatment programs is improving access to advanced care pathways. Additionally, increasing patient enrollment in experimental therapy programs is boosting segment growth.

The diagnosis segment is expected to witness the fastest growth rate of 8.3% from 2026 to 2033, driven by expanding genetic testing infrastructure and rising awareness of inherited retinal diseases. Increased availability of next-generation sequencing panels is significantly improving early and accurate diagnosis rates. Governments and healthcare institutions are investing in rare disease screening programs, particularly in Saudi Arabia. Growing use of ophthalmic imaging technologies is supporting better disease confirmation. Rising collaboration between diagnostic labs and hospitals is improving test accessibility. Furthermore, increasing focus on newborn and pediatric genetic screening is accelerating demand for diagnostic services.

- By End User

On the basis of end user, the market is segmented into hospitals, specialty clinics, ambulatory surgical centers, home healthcare, and others. The hospitals segment dominated the market with the largest revenue share of 47.9% in 2025, driven by availability of advanced ophthalmic infrastructure, genetic testing facilities, and multidisciplinary rare disease care. Hospitals serve as primary centers for diagnosis and long-term management of Leber Congenital Amaurosis cases. Countries such as Saudi Arabia and South Africa have well-established tertiary care hospitals specializing in genetic eye disorders. Increasing patient inflow for complex diagnosis strengthens hospital dominance. Availability of trained ophthalmologists and genetic counselors further supports this segment. Additionally, hospitals play a key role in clinical trials and advanced therapy administration.

The specialty clinics segment is expected to witness the fastest growth rate of 6.9% from 2026 to 2033, driven by increasing establishment of dedicated eye care and genetic disorder clinics. These clinics offer focused and faster diagnostic services compared to general hospitals. Rising patient preference for specialized care centers is boosting demand. Expansion of private ophthalmology networks in UAE and South Africa is supporting growth. Specialty clinics are increasingly equipped with advanced retinal imaging and genetic testing tools. Furthermore, shorter waiting times and personalized care approaches are enhancing patient adoption.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender and retail sales. The direct tender segment dominated the market with the largest revenue share of 64.1% in 2025, driven by strong government procurement of genetic testing kits, ophthalmic diagnostic tools, and hospital-based treatment solutions. Public healthcare systems in Saudi Arabia and other Gulf countries rely heavily on direct tenders for rare disease diagnostics. Bulk procurement by hospitals ensures cost efficiency and wider accessibility. Increasing government-funded rare disease programs is further strengthening this channel. Direct collaboration between manufacturers and healthcare institutions improves supply chain efficiency. Additionally, clinical research procurement contributes significantly to this segment.

The retail sales segment is expected to witness the fastest growth rate of 7.8% from 2026 to 2033, driven by increasing availability of diagnostic kits, supplements, and supportive vision care products through private healthcare distributors and specialty pharmacies. Rising patient awareness is encouraging direct access to supportive care products. Expansion of private diagnostic laboratories in South Africa and UAE is supporting retail channel growth. Increasing digital health platforms and telemedicine services are improving product accessibility. Growing demand for at-home monitoring and supportive eye care solutions is further boosting this segment. Additionally, improving insurance coverage for outpatient diagnostics is enhancing retail penetration.

Middle East and Africa Leber Congenital Amaurosis Market Regional Analysis

- Saudi Arabia dominated the Middle East and Africa Leber Congenital Amaurosis market with the largest share of 38.5% in 2025, supported by strong healthcare infrastructure, government-backed rare disease programs, and wider availability of genetic screening and specialized eye care services

- Healthcare providers in the country increasingly prioritize early genetic screening and specialized ophthalmology services, supported by government-led initiatives focused on improving rare disease diagnosis and patient management outcomes

- The presence of well-established tertiary care hospitals and growing participation in gene therapy research programs further strengthens Saudi Arabia’s leadership position in the regional market. Increasing awareness among clinicians regarding inherited retinal diseases is improving diagnosis rates and driving demand for advanced diagnostic and therapeutic solutions

The Saudi Arabia Leber Congenital Amaurosis Market Insight

Saudi Arabia dominated the Middle East and Africa Leber Congenital Amaurosis market with the largest revenue share of 38.5% in 2025, driven by strong healthcare infrastructure, rising investment in rare disease programs, and increasing adoption of advanced genetic diagnostic technologies. Patients in the country benefit from expanding access to tertiary ophthalmology centers and specialized genetic testing facilities for early disease identification. The growing focus on precision medicine and gene-based therapies is further strengthening clinical management of inherited retinal disorders. Moreover, government initiatives supporting rare disease awareness and screening programs are significantly contributing to market expansion. Increasing participation in international clinical research and gene therapy trials is also boosting treatment prospects.

South Africa Leber Congenital Amaurosis Market Insight

The South Africa Leber Congenital Amaurosis market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by improving healthcare infrastructure and rising awareness of genetic eye disorders. The increasing availability of diagnostic services in urban hospitals is supporting earlier detection of Leber Congenital Amaurosis cases. Growing government and NGO involvement in rare disease screening programs is fostering improved patient identification. Additionally, expanding access to ophthalmology specialists is enhancing treatment pathways. Rising collaborations with international healthcare organizations are further supporting knowledge transfer and diagnostic advancements.

United Arab Emirates Leber Congenital Amaurosis Market Insight

The United Arab Emirates Leber Congenital Amaurosis market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by advanced healthcare infrastructure and strong adoption of genetic testing technologies. The country’s focus on becoming a regional medical hub is encouraging investments in rare disease diagnostics and specialized ophthalmology services. Patients benefit from access to state-of-the-art hospitals offering next-generation sequencing and retinal imaging. Increasing awareness among clinicians regarding inherited retinal diseases is improving diagnosis rates. Additionally, government support for precision medicine initiatives is contributing to steady market growth.

Egypt Leber Congenital Amaurosis Market Insight

The Egypt Leber Congenital Amaurosis market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing healthcare modernization and rising awareness of rare genetic disorders. Expanding access to ophthalmic care in urban hospitals is improving diagnostic capabilities for retinal diseases. Growing efforts to enhance pediatric eye screening programs are supporting earlier identification of cases. Additionally, gradual improvements in laboratory infrastructure are enabling wider availability of genetic testing services. Rising collaborations with international health organizations are further supporting clinical capacity building in the country.

Middle East and Africa Leber Congenital Amaurosis Market Share

The Middle East and Africa Leber Congenital Amaurosis industry is primarily led by well-established companies, including:

- Novartis AG (Switzerland)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Pfizer Inc. (U.S.)

- Bayer AG (Germany)

- AbbVie Inc. (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- Sanofi (France)

- Santen Pharmaceutical Co., Ltd. (Japan)

- Spark Therapeutics, Inc. (U.S.)

- MeiraGTx Holdings plc (U.K.)

- Regenxbio Inc. (U.S.)

- Editas Medicine, Inc. (U.S.)

- AGTC (U.S.)

- Nanoscope Therapeutics Inc. (U.S.)

- GenSight Biologics (France)

- Alnylam Pharmaceuticals, Inc. (U.S.)

- King Khaled Eye Specialist Hospital (Saudi Arabia)

- Moorfields Eye Hospital NHS Foundation Trust (U.K.)

What are the Recent Developments in Middle East and Africa Leber Congenital Amaurosis Market?

- In November 2025, Eli Lilly announced a major global licensing deal with MeiraGTx for the experimental gene therapy AAV-AIPL1 targeting severe Leber Congenital Amaurosis 4. The therapy focuses on restoring vision in children with AIPL1 gene mutations and strengthens the global development pipeline for LCA treatments, with potential future access for patients in Middle East referral centers such as Saudi Arabia and UAE

- In February 2025, doctors in London reported a breakthrough gene therapy using the AIPL1 gene that restored vision in children with severe Leber Congenital Amaurosis, including a patient from Tunisia. The therapy enabled previously blind children to recognize faces and objects, marking one of the most significant advances in inherited retinal disease treatment and demonstrating direct relevance for Middle East and Africa-linked patients

- In December 2024, researchers from King Fahd University of Petroleum and Minerals (Saudi Arabia) published advancements in non-viral gene therapy for Leber Congenital Amaurosis, focusing on nanoparticle and CRISPR-based delivery systems. The study highlighted Saudi Arabia’s growing contribution to rare retinal disease research and the development of safer gene delivery alternatives for clinical applications

- In November 2024, a peer-reviewed study reported continued clinical progress in gene therapy trials for inherited retinal disorders, including Leber Congenital Amaurosis, emphasizing the expansion of AAV-based and CRISPR-based treatment pipelines. The findings reinforce growing international clinical collaboration, including patient referrals from Middle Eastern ophthalmology centers

- In April 2024, researchers and clinicians at Moorfields Eye Hospital and UCL performed a pioneering gene therapy procedure for Leber Congenital Amaurosis-4 (AIPL1 mutation), one of the most severe forms of childhood blindness. The treatment, delivered via retinal gene injection, demonstrated early success in restoring light perception in previously blind children, reinforcing progress in curative therapies that are increasingly being referenced in Middle East ophthalmology centers for future adoption

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.