Middle East And Africa Lentiviral Vector Market

Market Size in USD Million

USD

85.50 Million

USD

282.24 Million

2025

2033

USD

85.50 Million

USD

282.24 Million

2025

2033

| 2026 - 2033 | |

| USD 85.50 Million | |

| USD 282.24 Million | |

| % | |

|

Middle East and Africa Lentiviral Vector Market Size

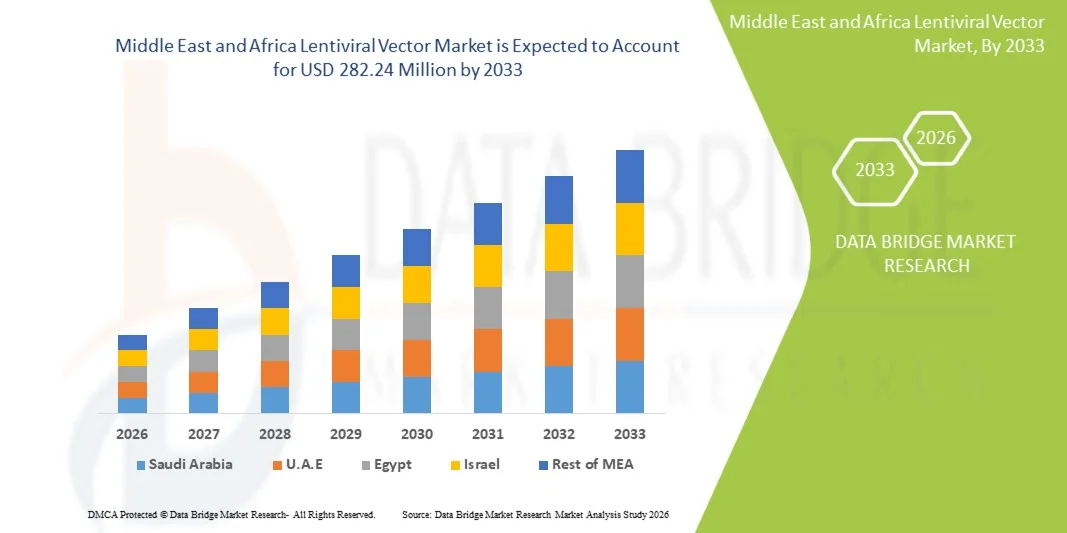

- The Middle East and Africa Lentiviral Vector Market size was valued at USD 85.50 Million in 2025 and is expected to reach USD 282.24 Million by 2033, at a CAGR of 16.10% during the forecast period

- The market growth is largely fueled by the increasing adoption of gene and cell therapies, rising prevalence of genetic disorders, and continuous technological advancements in viral vector engineering, leading to improved transduction efficiency and safety in therapeutic applications

- Furthermore, growing investment in research and development, expanding clinical trials, and rising demand for personalized medicine and advanced immunotherapies are establishing lentiviral vectors as critical tools in modern biotechnology and healthcare. These converging factors are accelerating the uptake of Lentiviral Vector solutions, thereby significantly boosting the industry’s growth

Middle East and Africa Lentiviral Vector Market Analysis

- Lentiviral vectors, widely used for efficient gene delivery in research, gene therapy, and cell therapy applications, are increasingly critical components of modern biotechnology due to their ability to enable stable gene expression and support advanced therapeutic development across preclinical and clinical settings

- The rising demand for lentiviral vectors is primarily driven by the rapid expansion of gene and cell therapy pipelines, increasing approvals of CAR-T and gene-modified therapies, and growing investments in personalized and precision medicine worldwide

- Saudi Arabia dominated the Middle East and Africa Lentiviral Vector Market with the largest revenue share of approximately 22.5% in 2025, supported by government funding for biotechnology, expansion of gene therapy clinical trials, local manufacturing capabilities, and growing CDMO presence. Strong focus on precision medicine, academic collaborations, and favorable regulatory initiatives further boost adoption. The country’s biotechnology ecosystem, coupled with rising demand for viral vector solutions, underpins its leading market position

- The United Arab Emirates (U.A.E.) is expected to be the fastest-growing country in the Middle East and Africa Lentiviral Vector Market during the forecast period, with an estimated CAGR of approximately 21.4% from 2025 to 2032, driven by national biotech initiatives, growing investment in viral vector production, increasing clinical research, and expansion of advanced biotech hubs. Supportive government policies, collaborations with international research institutions, and rising adoption of gene therapy solutions accelerate market growth

- The products segment dominated the market with a revenue share of 64.3% in 2025, driven by high demand for ready-to-use lentiviral vectors, plasmids, and transduction reagents

Report Scope and Middle East and Africa Lentiviral Vector Market Segmentation

|

Attributes |

Middle East and Africa Lentiviral Vector Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Middle East and Africa Lentiviral Vector Market Trends

“Expanding Utilization of Lentiviral Vectors in Advanced Gene and Cell Therapies”

- A significant and accelerating trend in the global Middle East and Africa Lentiviral Vector Market is the expanding utilization of lentiviral vectors in gene therapy, cell therapy, and regenerative medicine applications, owing to their ability to deliver genetic material into both dividing and non-dividing cells with high efficiency

- For instance, in June 2023, Thermo Fisher Scientific expanded its viral vector manufacturing capabilities in the U.S. and Europe to support increasing global demand for lentiviral vectors used in clinical-stage gene and cell therapy programs

- The rising number of clinical trials targeting rare genetic disorders, oncology indications, and autoimmune diseases is reinforcing the demand for lentiviral vectors across research institutions and biopharmaceutical companies worldwide

- In addition, advancements in vector engineering, including improved safety profiles and enhanced transduction efficiency, are supporting broader adoption in late-stage clinical development and commercial-scale manufacturing

- Growing collaborations between academic research centers, contract development and manufacturing organizations (CDMOs), and pharmaceutical companies are further shaping the global market landscape

Middle East and Africa Lentiviral Vector Market Dynamics

Driver

“Rising Global Demand for Gene Therapy, Cell Therapy, and Personalized Medicine”

- The increasing global focus on gene therapy and personalized medicine is a key driver of the Middle East and Africa Lentiviral Vector Market, as these vectors play a critical role in delivering therapeutic genes for long-term expression

- For instance, in September 2022, Oxford Biomedica entered into a long-term supply agreement with a global pharmaceutical company to manufacture lentiviral vectors for CAR-T cell therapies, reflecting strong commercial demand

- The growing prevalence of cancer, rare genetic disorders, and chronic diseases has intensified the need for innovative treatment approaches, thereby accelerating the adoption of lentiviral vectors in therapeutic development

- Favorable regulatory frameworks for cell and gene therapies in regions such as North America and Europe, combined with increasing healthcare investments in Asia-Pacific, are further driving market expansion

- Increased public and private funding for biotechnology research, along with government initiatives supporting advanced therapeutics, continues to strengthen global demand for lentiviral vector solutions

Restraint/Challenge

“High Manufacturing Complexity, Cost Constraints, and Stringent Regulatory Requirements”

- High manufacturing costs and complex production processes represent major challenges for the global Middle East and Africa Lentiviral Vector Market, as production requires specialized facilities, skilled personnel, and strict compliance with GMP standards

- For instance, in February 2023, several CDMOs highlighted delays in lentiviral vector production timelines due to increased regulatory scrutiny and capacity limitations, impacting the scalability of gene therapy programs

- Stringent regulatory requirements related to biosafety, quality control, and viral vector consistency increase development timelines and operational costs, particularly for small and mid-sized biotechnology companies

- Limited global manufacturing capacity and supply chain bottlenecks further constrain the availability of lentiviral vectors for large-scale clinical and commercial applications

- Addressing these challenges through process optimization, expansion of manufacturing infrastructure, workforce training, and regulatory harmonization will be critical for sustained global market growth

Middle East and Africa Lentiviral Vector Market Scope

The market is segmented on the basis of component, type, generation, workflow, delivery method, application, and end user.

• By Component

On the basis of component, the Middle East and Africa Lentiviral Vector Market is segmented into lentiviral promoters, lentiviral fusion tags, lentiviral packaging systems, and others. The lentiviral packaging systems segment dominated the largest market revenue share of 41.6% in 2025, driven by its essential role in the production of replication-deficient lentiviral vectors used in gene and cell therapies. Packaging systems are critical for assembling viral particles and ensuring high transduction efficiency, which is vital for clinical-grade vector manufacturing. Strong demand from CAR-T cell therapy developers significantly supports this segment. The growing number of gene therapy clinical trials globally increases consumption of packaging plasmids and reagents. Pharmaceutical and biotechnology companies prefer standardized packaging systems to ensure batch consistency and regulatory compliance. Advancements in packaging technology improving yield and safety further reinforce dominance. Increasing outsourcing of vector production to CDMOs also drives recurring demand. High usage frequency across upstream workflows boosts revenue generation. Regulatory familiarity with established packaging systems supports continued adoption. Expansion of GMP manufacturing facilities strengthens market penetration. Rising investments in gene therapy infrastructure further sustain dominance. Overall, the critical and non-substitutable nature of packaging systems secures their leading position in the market.

The lentiviral promoters segment is expected to witness the fastest growth, registering a CAGR of 18.9% from 2026 to 2033, driven by increasing demand for precise gene expression control in advanced gene therapies. Promoters play a key role in regulating transgene expression levels, which is crucial for improving therapeutic efficacy and safety. Growing research in cell-specific and inducible promoters accelerates adoption. Expansion of synthetic biology and precision medicine applications supports growth. Academic and research institutes increasingly utilize customized promoters for experimental flexibility. Rising focus on reducing off-target effects boosts promoter innovation. Increased funding for next-generation vector engineering contributes to market expansion. Pharmaceutical companies are investing in proprietary promoter designs to enhance product differentiation. The shift toward personalized therapies increases demand for specialized promoters. Advancements in promoter screening technologies improve development speed. Increasing patent activity reflects innovation momentum. These factors collectively drive the segment’s rapid CAGR growth.

• By Type

On the basis of type, the Middle East and Africa Lentiviral Vector Market is segmented into products and services. The products segment dominated the market with a revenue share of 64.3% in 2025, driven by high demand for ready-to-use lentiviral vectors, plasmids, and transduction reagents. Biotechnology and pharmaceutical companies rely heavily on standardized products to accelerate preclinical and clinical development timelines. Products offer reproducibility and quality consistency, which is essential for regulated environments. Strong usage in academic research and early-stage drug discovery supports revenue dominance. Increasing availability of GMP-grade products further strengthens adoption. Rising investment in gene and cell therapy pipelines boosts recurring product demand. Manufacturers continuously launch improved product variants, supporting replacement demand. Products reduce dependency on in-house vector production capabilities. Widespread distribution through established suppliers enhances accessibility. High consumption volume across workflows sustains revenue leadership. Increasing global clinical trial activity reinforces dominance. Overall, product reliability and scalability maintain the segment’s leading position.

The services segment is anticipated to witness the fastest growth, with a CAGR of 20.4% from 2026 to 2033, driven by increasing outsourcing trends across the gene therapy industry. Pharmaceutical and biotechnology companies increasingly rely on CDMOs for vector development, scale-up, and GMP manufacturing. Services reduce capital expenditure and operational complexity for therapy developers. Rising number of clinical trials significantly increases demand for contract services. Expertise in regulatory compliance makes service providers highly attractive. Expansion of personalized therapies drives demand for customized vector services. Increasing complexity of vector design necessitates specialized technical capabilities. Emerging biotech startups prefer service models for cost efficiency. Global shortage of in-house manufacturing capacity accelerates outsourcing. Strategic partnerships between sponsors and CDMOs support growth. Investments in service infrastructure expand capacity. These factors collectively drive strong CAGR growth for services.

• By Generation

On the basis of generation, the Middle East and Africa Lentiviral Vector Market is segmented into 4th-generation, 3rd-generation, 2nd-generation, and 1st-generation vectors. The 3rd-generation segment dominated the market with a revenue share of 38.7% in 2025, owing to its superior safety profile and widespread clinical acceptance. These vectors offer reduced risk of replication-competent virus formation, making them suitable for therapeutic use. High transduction efficiency supports use in oncology and rare disease applications. Regulatory authorities are more familiar with 3rd-generation vectors, easing approval pathways. Extensive clinical data supports physician and developer confidence. Strong adoption in CAR-T and stem cell therapies reinforces dominance. Compatibility with large-scale manufacturing further boosts demand. Established protocols simplify development processes. High availability across suppliers supports accessibility. Increasing approvals of gene therapies sustain usage. Longstanding market presence ensures trust. These factors secure the segment’s dominant position.

The 4th-generation segment is expected to grow at the fastest CAGR of 22.1% from 2026 to 2033, driven by enhanced biosafety and next-generation design improvements. These vectors further minimize insertional mutagenesis risks, improving patient safety. Growing focus on advanced gene therapies accelerates adoption. Increased R&D investment supports rapid innovation. Academic institutions are actively researching novel 4th-generation designs. Pharmaceutical companies adopt these vectors for next-phase clinical programs. Regulatory emphasis on safety favors advanced generations. Improved control over gene expression enhances therapeutic outcomes. Demand from high-risk disease indications increases uptake. Technological advancements reduce production complexity. Strategic collaborations support commercialization. These factors collectively drive rapid growth.

• By Workflow

On the basis of workflow, the Middle East and Africa Lentiviral Vector Market is segmented into upstream processing and downstream processing. The upstream processing segment dominated the market with a revenue share of 55.4% in 2025, driven by its critical role in vector production. Activities such as cell culture, transfection, and vector amplification generate high consumable demand. Increasing scale-up of gene therapy manufacturing supports dominance. High usage of media, reagents, and plasmids boosts revenue. Continuous production optimization investments strengthen adoption. Strong focus on improving vector yield supports spending. Expansion of GMP facilities increases upstream activity. Automation adoption enhances efficiency and repeatability. Frequent process iterations drive recurring purchases. High technical dependency ensures sustained demand. Increasing clinical trial volumes support usage. These factors maintain upstream dominance.

The downstream processing segment is projected to grow at the fastest CAGR of 19.2% from 2026 to 2033, driven by increasing emphasis on purification and quality control. Regulatory requirements demand highly purified vectors for clinical use. Rising adoption of chromatography and filtration technologies supports growth. Increasing complexity of vectors necessitates advanced downstream solutions. Demand for scalable purification processes accelerates adoption. Expansion of late-stage clinical trials increases downstream intensity. Investments in novel purification technologies enhance efficiency. CDMOs expand downstream capacity to meet demand. Stringent safety standards boost testing requirements. Improved analytical tools support growth. High value per process step increases revenue. These factors collectively drive rapid CAGR growth.

• By Delivery Method

On the basis of delivery method, the Middle East and Africa Lentiviral Vector Market is segmented into In Vivo and Ex Vivo. The Ex Vivo segment dominated the largest market revenue share of 58.3% in 2025, driven by its extensive use in CAR-T and other cell-based gene therapies where patient cells are modified outside the body. Ex vivo delivery ensures higher safety, precise control over transduction efficiency, and reduced systemic exposure, making it highly preferred in clinical applications. The segment benefits from increasing adoption of personalized cell therapies, rising number of clinical trials in oncology and immunology, and strong demand from biotechnology companies developing CAR-T, TCR-T, and stem cell therapies. Ex vivo methods are easier to monitor for regulatory compliance and quality control, which encourages pharmaceutical companies to adopt these approaches. Expansion of CDMO capacities and outsourcing of ex vivo processing further reinforces revenue growth. High adoption in hospital and research settings strengthens market dominance. Standardized ex vivo protocols facilitate reproducibility across batches. Additionally, the growing focus on next-generation cell therapies drives further market share for ex vivo delivery. Investment in GMP-compliant manufacturing facilities supports continued expansion of this segment. Overall, the precision, safety, and regulatory familiarity make Ex Vivo delivery the dominant method.

The In Vivo segment is expected to witness the fastest CAGR of 19.2% from 2026 to 2033, driven by rising interest in direct gene therapy applications where vectors are administered directly to patients. In vivo delivery enables treatment of diseases where ex vivo cell manipulation is impractical, such as certain genetic disorders and systemic conditions. Increasing research in tissue-specific targeting, development of advanced viral vectors with improved tropism, and growing adoption in preclinical and clinical studies contribute to rapid growth. Supportive regulatory frameworks and expanded government funding for gene therapy research accelerate adoption. Advances in delivery technologies, including safer viral capsids and promoter optimization, boost efficiency. Rising focus on rare genetic disorders fuels demand for in vivo approaches. Pharmaceutical companies are investing in proprietary vector platforms for targeted in vivo therapies. Collaborative research between biotech firms and academic institutions enhances innovation. In vivo delivery also benefits from streamlined administration procedures compared to ex vivo methods. Overall, the expanding pipeline of gene therapy candidates positions in vivo delivery for significant CAGR growth.

• By Disease Indication

On the basis of disease indication, the Middle East and Africa Lentiviral Vector Market is segmented into Cancer, Genetic Disorders, Infectious Diseases, Veterinary Diseases, and Others. The Cancer segment dominated the largest market revenue share of 46.5% in 2025, driven by the rapid adoption of CAR-T, TCR-T, and NK cell therapies targeting hematological and solid tumors. Oncology applications account for the majority of global lentiviral vector demand due to high clinical trial activity, regulatory approvals, and increasing commercial adoption. Rising prevalence of cancer, expanding gene therapy infrastructure, and growing investments by pharmaceutical and biotech companies further support the segment. CAR-T therapies targeting leukemia, lymphoma, and multiple myeloma are major revenue drivers. Collaboration between research institutes and CDMOs for oncology-focused vector production enhances supply capabilities. Advanced ex vivo cell modification and personalized treatment strategies reinforce dominance. The segment benefits from high reimbursement potential in developed markets. Increasing patient awareness and government support for cancer therapies also contribute to market share. Standardized lentiviral platforms for oncology improve consistency and scalability. Expanding access to global markets drives sustained adoption. Overall, cancer applications remain the most dominant disease indication in the market.

The Genetic Disorders segment is expected to witness the fastest CAGR of 18.7% from 2026 to 2033, fueled by increasing prevalence of inherited diseases such as sickle cell anemia, beta-thalassemia, and cystic fibrosis. Growth is supported by advances in precision medicine, gene editing, and ex vivo gene therapy approaches that correct genetic defects. Rising clinical trials, government funding initiatives, and growing adoption of personalized therapy platforms drive market expansion. Biotech and pharmaceutical companies are actively developing gene therapies targeting rare disorders, enhancing segment growth. Innovations in promoter design and vector engineering improve efficacy and reduce off-target effects. The segment benefits from increasing awareness and early diagnosis of rare genetic diseases. Academic and research institutes are exploring novel delivery mechanisms for these disorders. Regulatory approvals for genetic disorder therapies further stimulate adoption. Expansion of CDMOs offering specialized vector production strengthens supply chains. Rising demand in emerging markets contributes to segment growth. Overall, genetic disorders represent the fastest-growing disease indication segment globally.

• By Application

On the basis of application, the Middle East and Africa Lentiviral Vector Market is segmented into Gene Therapy and Vaccinology. The Gene Therapy segment dominated the largest market revenue share of 62.4% in 2025, driven by extensive use of lentiviral vectors in CAR-T, TCR-T, and stem cell therapies. Gene therapy applications are benefiting from robust clinical pipelines, growing regulatory approvals, and increasing commercialization of advanced therapeutics. High adoption in oncology, rare genetic disorders, and immunology applications supports dominance. Outsourcing of vector production to CDMOs, investment in GMP-compliant facilities, and standardization of manufacturing protocols contribute to growth. Pharmaceutical and biotechnology companies prioritize lentiviral vectors for ex vivo applications due to predictable transduction efficiency. Academic and research institutions also increasingly rely on gene therapy for preclinical studies. Expansion of personalized medicine and precision therapies further consolidates segment leadership. Regulatory familiarity with gene therapy workflows facilitates adoption. Government incentives and funding programs bolster research initiatives. Overall, gene therapy remains the dominant application segment in the Middle East and Africa Lentiviral Vector Market.

The Vaccinology segment is expected to witness the fastest CAGR of 20.1% from 2026 to 2033, driven by increasing global demand for viral vector-based vaccines, including for infectious diseases such as HIV, COVID-19, and emerging pathogens. Accelerated vaccine development, expanding public health initiatives, and government funding for pandemic preparedness drive growth. Advances in vector design, promoter optimization, and immunogenicity improvements increase vaccine efficacy. Strategic collaborations between biotech companies, CDMOs, and research institutes accelerate commercialization. Rising adoption in emerging markets due to government vaccination campaigns supports expansion. Vaccine-specific regulatory frameworks streamline approvals. Increased R&D investment in novel viral vector platforms fosters innovation. Growth in personalized immunotherapies also contributes to segment adoption. The scalability of vector production enhances manufacturing efficiency. Overall, vaccinology applications represent the fastest-growing segment globally.

• By End User

On the basis of end user, the Middle East and Africa Lentiviral Vector Market is segmented into Biotechnology Companies, Pharmaceutical Companies, Contract Research Organizations (CROs), Contract Development and Manufacturing Organizations (CDMOs), and Academic/Research Institutes. The CDMOs segment dominated the largest market revenue share of 48.2% in 2025, owing to their critical role in outsourced production of clinical- and commercial-grade lentiviral vectors. CDMOs provide specialized expertise, GMP-compliant facilities, and scalable manufacturing for CAR-T, TCR-T, and gene therapy products. Rising outsourcing by biotech and pharma companies, cost advantages, and the need for regulatory-compliant production reinforce dominance. Strong partnerships with global pharmaceutical companies increase recurring demand. High-volume ex vivo vector production supports revenue growth. Standardization of production protocols ensures quality and reproducibility. Expansion of CDMO facilities in North America, Europe, and Asia-Pacific strengthens market penetration. Investment in next-generation vector platforms enhances service offerings. Regulatory familiarity and experience with clinical supply chains boost adoption. Overall, CDMOs represent the dominant end-user segment in the Middle East and Africa Lentiviral Vector Market.

The Pharmaceutical Companies segment is expected to witness the fastest CAGR of 19.5% from 2026 to 2033, driven by increasing investments in proprietary gene therapy pipelines, novel lentiviral vector platforms, and global expansion of viral vector production capabilities. Pharmaceutical companies are integrating in-house development and outsourcing models to accelerate product commercialization. Growth is further fueled by demand for advanced CAR-T, TCR-T, and gene therapy products. Increasing collaboration with CDMOs and academic institutions enhances technological capabilities. Supportive regulatory policies and rising clinical trial activity in oncology and rare genetic diseases accelerate adoption. Strategic acquisitions and partnerships strengthen manufacturing capacities. Focus on innovation, precision medicine, and personalized therapies supports segment expansion. Rising demand for gene therapy solutions in emerging markets further propels growth. Technological advancements in vector engineering improve safety and efficacy. Overall, pharmaceutical companies represent the fastest-growing end-user segment

Middle East and Africa Lentiviral Vector Market Regional Analysis

- The Middle East and Africa Lentiviral Vector Market is poised to grow at the fastest CAGR of 24% during the forecast period of 2026 to 2033, driven by rapid expansion of biotechnology infrastructure, increasing investments in gene and cell therapy research, and rising clinical trial activity across countries such as Saudi Arabia, UAE, and Egypt

- Governments across the region are actively supporting advanced biologics, regenerative medicine, and gene therapy development through favorable funding policies and regulatory reform

- Furthermore, Middle East and Africa is emerging as a key manufacturing and outsourcing hub for lentiviral vector production, supported by cost advantages, expanding CDMO capacity, and growing demand from global biopharmaceutical companies

Saudi Arabia Middle East and Africa Lentiviral Vector Market Insight

Saudi Arabia Middle East and Africa Lentiviral Vector Market dominated the Middle East and Africa Lentiviral Vector Market with the largest revenue share of approximately 22.5% in 2025, supported by government funding for biotechnology, expansion of gene therapy clinical trials, local manufacturing capabilities, and growing CDMO presence. Strong focus on precision medicine, academic collaborations, and favorable regulatory initiatives further boost adoption. The country’s biotechnology ecosystem, coupled with rising demand for viral vector solutions, underpins its leading market position.

United Arab Emirates (U.A.E.) Middle East and Africa Lentiviral Vector Market Insight

The U.A.E. Middle East and Africa Lentiviral Vector Market is expected to be the fastest-growing country in the Middle East and Africa Lentiviral Vector Market during the forecast period, with an estimated CAGR of approximately 21.4% from 2025 to 2032, driven by national biotech initiatives, growing investment in viral vector production, increasing clinical research, and expansion of advanced biotech hubs. Supportive government policies, collaborations with international research institutions, and rising adoption of gene therapy solutions accelerate market growth.

Middle East and Africa Lentiviral Vector Market Share

The Lentiviral Vector industry is primarily led by well-established companies, including:

- Lonza Group (Switzerland)

- Takara Bio (Japan)

- Oxford Biomedica (U.K.)

- Sartorius AG (Germany)

- FUJIFILM Diosynth Biotechnologies (Japan)

- Catalent (U.S.)

- Charles River Laboratories (U.S.)

- AGC Biologics (Japan)

- Sirion Biotech (Germany)

- Vigene Biosciences (U.S.)

- GeneCopoeia (U.S.)

- VectorBuilder (U.S.)

- Creative Biogene (U.S.)

- Bio-Techne (U.S.)

- Aldevron (U.S.)

- WuXi Advanced Therapies (China)

- Bayer AG (Germany)

- Genscript Biotech (China)

Latest Developments in Middle East and Africa Lentiviral Vector Market

- In April 2023, Yposkesi, a CDMO specializing in viral vectors, announced the launch of LentiSure, a next-generation lentiviral vector production platform designed to boost production efficiency and robustness for CAR-T cell and other cell-based immuno-oncology therapies

- In December 2023, VIVEbiotech reported significant business growth with a 70% increase in sales and expanded lentiviral vector manufacturing capabilities, supporting both in vivo and ex vivo applications and supplying GMP-grade vectors to global partners

- In June 2024, Charles River Laboratories announced a strategic collaboration with the University of Colorado Anschutz Gates Institute to manufacture lentiviral vectors, aimed at accelerating CAR-T cell therapy development for hematological cancers and enhancing advanced gene therapy manufacturing capacity

- In September 2024, Rentschler Biopharma launched dedicated lentiviral vector manufacturing services at its Stevenage (UK) facility, introducing a new lentiviral vector toolbox to complement its AAV offerings and support cell and gene therapy development for rare diseases and cancer immunotherapy

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.