Middle East And Africa Lung Cancer Screening Software Market

Market Size in USD Million

USD

180.00 Million

USD

546.80 Million

2025

2033

USD

180.00 Million

USD

546.80 Million

2025

2033

| 2026 - 2033 | |

| USD 180.00 Million | |

| USD 546.80 Million | |

| % | |

|

Middle East and Africa Lung Cancer Screening Software Market Size

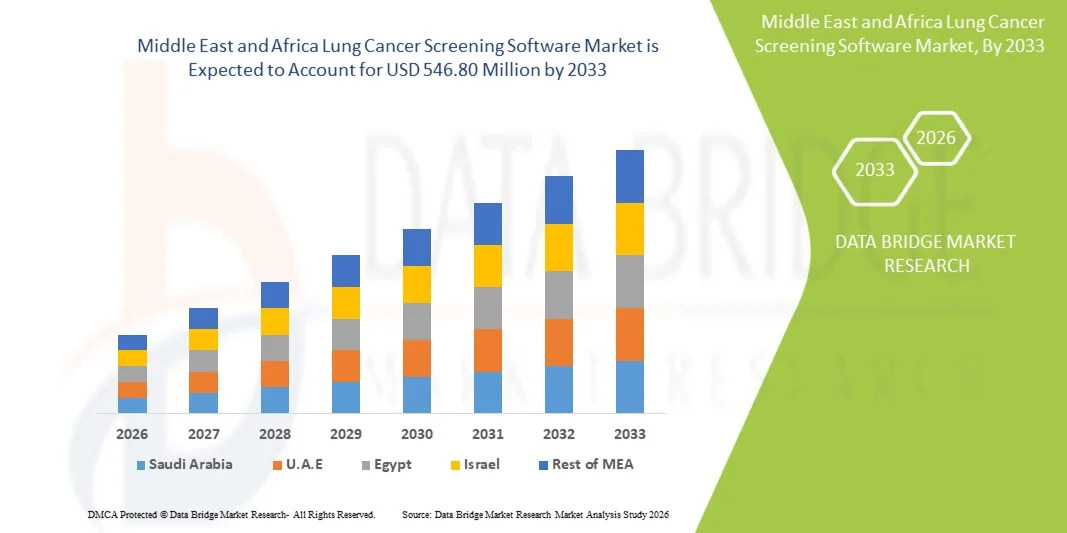

- The Middle East and Africa lung cancer screening software market size was valued at USD 180.00 million in 2025 and is expected to reach USD 546.80 million by 2033, at a CAGR of 14.9% during the forecast period

- The market growth is largely fueled by the increasing adoption of AI-enabled diagnostic tools, expanding implementation of low-dose CT screening programs, and rising healthcare digitization across emerging economies in the region

- Furthermore, growing awareness of early lung cancer detection, coupled with improving healthcare infrastructure and increasing investments in radiology software solutions, is establishing screening software as a critical component of modern oncology workflows, thereby significantly boosting industry growth

Middle East and Africa Lung Cancer Screening Software Market Analysis

- Lung cancer screening software, offering AI-powered imaging analysis, workflow automation, and clinical decision-support capabilities, is becoming an essential component of modern oncology diagnostics in both public and private healthcare settings in the Middle East and Africa region due to rising disease burden and increasing digital transformation in healthcare systems

- The escalating demand for lung cancer screening software is primarily fueled by increasing adoption of computer-assisted screening technologies, expanding use of integrated hospital imaging systems, and rising focus on early cancer detection supported by national health programs and international collaborations

- Saudi Arabia dominated the Middle East and Africa lung cancer screening software market with the largest revenue share of 38.6% in 2025, characterized by advanced healthcare infrastructure, strong adoption of AI-enabled radiology platforms, and government-backed cancer screening initiatives driving large-scale deployment in tertiary hospitals

- South Africa is expected to be the fastest growing country in the lung cancer screening software market during the forecast period due to improving diagnostic imaging accessibility, rising private healthcare investments, and increasing adoption of AI-based oncology screening tools across urban healthcare facilities

- The Lung Cancer Screening Radiology Solution segment dominated the market with the largest share of 41.2% in 2025, driven by its critical role in CT scan interpretation, early lung nodule detection, and seamless integration into radiology workflows for improving diagnostic efficiency and accuracy

Report Scope and Middle East and Africa Lung Cancer Screening Software Market Segmentation

|

Attributes |

Middle East and Africa Lung Cancer Screening Software Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Middle East and Africa Lung Cancer Screening Software Market Trends

“Rising Adoption of AI-Enabled Diagnostic Imaging Integration”

- A significant and accelerating trend in the Middle East and Africa lung cancer screening software market is the increasing integration of artificial intelligence (AI) with radiology imaging platforms and hospital information systems, improving early detection accuracy and workflow efficiency in oncology diagnostics

- For instance, AI-based lung nodule detection solutions such as screening software integrated into CT imaging workflows are being increasingly deployed in advanced hospitals across Saudi Arabia and the UAE to support faster clinical decision-making

- AI integration in lung cancer screening software enables features such as automated nodule detection, risk stratification, and image enhancement, helping radiologists identify early-stage abnormalities with higher precision and reduced diagnostic delay

- The seamless integration of screening software with PACS, RIS, and EMR systems is enabling centralized access to imaging data across hospitals and cancer centers, improving coordination between radiologists and oncologists in treatment planning

- The growing adoption of cloud-based deployment models is enabling remote access to screening platforms, allowing multi-site hospitals and diagnostic networks to share imaging data efficiently across geographies in real time

- This trend towards intelligent, interoperable, and AI-driven screening platforms is reshaping oncology workflows in the region, with companies focusing on cloud-based diagnostic ecosystems and automated reporting tools to support scalable cancer screening programs

- The demand for AI-enabled lung cancer screening software is growing rapidly across both public and private healthcare sectors, as governments and healthcare providers prioritize early detection and digital transformation in cancer care

Middle East and Africa Lung Cancer Screening Software Market Dynamics

Driver

“Rising Burden of Lung Cancer and Expansion of Digital Screening Programs”

- The increasing prevalence of lung cancer cases across the Middle East and Africa, coupled with growing adoption of national screening initiatives and digital health transformation programs, is a significant driver for the demand for screening software solutions

- For instance, national healthcare strategies in countries such as Saudi Arabia and South Africa are increasingly incorporating AI-based diagnostic imaging platforms to strengthen early cancer detection capabilities in public hospitals

- As healthcare systems become more focused on early diagnosis and precision oncology, lung cancer screening software offers advanced capabilities such as automated image analysis, patient tracking, and clinical decision support for improved outcomes

- Furthermore, the rising investment in hospital digitalization and expansion of radiology infrastructure is making screening software an essential component of oncology workflows across tertiary care centers

- The growing adoption of low-dose CT screening programs and increasing awareness of early lung cancer detection among physicians and patients are key factors propelling market adoption in the region

- Expanding partnerships between public health authorities and private diagnostic providers are improving access to structured lung cancer screening programs across urban healthcare systems

- Increasing penetration of cloud computing in healthcare IT infrastructure is further enabling scalable deployment of AI-based screening platforms across multiple hospital networks

Restraint/Challenge

“Limited Healthcare Infrastructure and High Deployment Costs in Emerging Economies”

- Concerns surrounding limited healthcare infrastructure and uneven availability of advanced imaging systems across several African countries pose a significant challenge to broader adoption of lung cancer screening software

- For instance, inconsistent access to high-resolution CT scanners and integrated hospital IT systems in certain regions limits the effective deployment of advanced AI-based screening platforms

- Addressing these challenges requires substantial investment in digital health infrastructure, interoperability standards, and training of radiology professionals to ensure effective use of screening technologies

- Additionally, the relatively high cost of advanced AI-enabled screening software and cloud integration solutions can be a barrier for smaller hospitals and public healthcare facilities in low-income regions

- While adoption is increasing in major urban healthcare centers, affordability and infrastructure gaps still hinder widespread implementation across the broader Middle East and Africa region

- Lack of standardized regulatory frameworks for AI-based medical imaging software across several countries further slows down large-scale commercialization and adoption

- Limited availability of skilled radiologists and trained healthcare IT professionals in rural and semi-urban areas also restricts optimal utilization of advanced screening technologies

Middle East and Africa Lung Cancer Screening Software Market Scope

The market is segmented on the basis of mode of delivery, product, type, application, platform, purchase mode, end user, and distribution channel.

- By Mode of Delivery

On the basis of mode of delivery, the market is segmented into cloud-based solutions, on-premise solutions, and web-based solutions. The cloud-based solutions segment dominated the market with the largest revenue share of 46.3% in 2025, driven by increasing adoption of scalable healthcare IT infrastructure and the need for centralized access to imaging and patient data across multiple healthcare facilities. Cloud deployment enables real-time data sharing between radiologists and oncologists, improves collaboration, and reduces dependency on on-site IT infrastructure. Additionally, rising digital transformation initiatives in countries such as Saudi Arabia and South Africa are accelerating cloud integration in diagnostic workflows. Hospitals and oncology centers also prefer cloud solutions due to lower maintenance costs and easier software updates. The segment further benefits from growing use of AI-enabled imaging platforms that require high computational scalability and cloud storage capabilities.

The on-premise solutions segment is expected to witness the fastest growth rate of 18.9% from 2026 to 2033, driven by increasing demand from hospitals and government healthcare institutions that prioritize data security and regulatory compliance. On-premise deployment is preferred in regions with strict data governance requirements where patient imaging data must remain within hospital-controlled IT environments. Large tertiary hospitals are increasingly investing in localized infrastructure to ensure uninterrupted access to screening systems even in low-connectivity regions. Moreover, concerns over cybersecurity risks in cloud systems are encouraging adoption of hybrid and on-premise models. The segment is also supported by long-term cost advantages for large institutions handling high patient volumes.

- By Product

On the basis of product, the market is segmented into lung cancer screening radiology solution, lung cancer screening patient management software, nodule management software, data collection and reporting, patient coordination and workflow, lung nodule computer-aided detection, pathology and cancer staging, statistical audit reporting, screening PACS, and practice management and audit log tracking. The lung cancer screening radiology solution segment dominated the market with the largest revenue share of 41.2% in 2025, driven by its essential role in CT scan interpretation, early lung nodule detection, and integration into radiology workflows. These solutions form the core diagnostic layer of lung cancer screening programs and are widely adopted across hospitals and oncology centers. Increasing prevalence of lung cancer and rising adoption of AI-based imaging tools further strengthen this segment. Radiology solutions also offer advanced visualization, automated reporting, and improved diagnostic accuracy. Strong integration with PACS and EMR systems enhances workflow efficiency.

The lung nodule computer-aided detection (CAD) segment is expected to witness the fastest growth rate of 22.4% from 2026 to 2033, driven by rising demand for AI-powered precision diagnostics and early-stage cancer detection. CAD systems significantly improve radiologists’ ability to identify small nodules that may be missed in conventional screening. Increasing integration of machine learning algorithms enhances detection accuracy and reduces false positives. Hospitals are rapidly adopting CAD tools as part of AI-assisted diagnostic workflows. Growing investments in AI healthcare startups and partnerships with global medtech companies are accelerating adoption in the region.

- By Type

On the basis of type, the market is segmented into computer-assisted screening and traditional screening. The computer-assisted screening segment dominated the market with the largest revenue share of 68.5% in 2025, driven by rapid adoption of AI-enabled diagnostic systems and the growing need for accurate and efficient lung cancer detection. These systems enhance radiologists’ decision-making by providing automated image analysis and risk assessment. Increased integration of digital health infrastructure in hospitals is further boosting adoption. Government-led screening programs in GCC countries are also prioritizing AI-based solutions. The segment benefits from improved diagnostic speed, reduced human error, and higher sensitivity in detecting early-stage lung cancer.

The computer-assisted screening segment is also expected to witness the fastest growth rate of 19.6% from 2026 to 2033, as healthcare providers increasingly shift away from manual interpretation methods toward AI-driven workflows. Expanding availability of cloud-based AI tools and improved computational capabilities are accelerating adoption. Rising awareness among clinicians about early detection benefits is also supporting growth. Continuous technological advancements in deep learning models are improving diagnostic precision. Increasing investment in digital oncology infrastructure across emerging African markets further strengthens growth prospects.

- By Application

On the basis of application, the market is segmented into non-small cell lung cancer (NSCLC) and small cell lung cancer (SCLC). The NSCLC segment dominated the market with the largest revenue share of 74.1% in 2025, driven by its significantly higher prevalence compared to SCLC in the Middle East and Africa region. NSCLC accounts for the majority of lung cancer cases, making it the primary focus of screening programs. Increasing use of CT-based early detection tools supports this segment’s dominance. Hospitals prioritize NSCLC screening due to better treatment outcomes when detected early. Strong integration of AI-based radiology tools further enhances detection accuracy for NSCLC cases.

The SCLC segment is expected to witness the fastest growth rate of 17.8% from 2026 to 2033, driven by increasing awareness and improved diagnostic capabilities for aggressive cancer types. Although less prevalent, SCLC requires rapid detection, which is increasingly supported by advanced screening software. Growing adoption of AI-assisted staging tools is improving early identification. Rising investment in oncology research and clinical trials is also supporting demand. Expansion of specialized cancer centers in urban regions is further accelerating segment growth.

- By Platform

On the basis of platform, the market is segmented into standalone and integrated systems. The integrated platform segment dominated the market with the largest revenue share of 61.7% in 2025, driven by strong demand for interoperability between hospital systems such as PACS, RIS, and EMR. Integrated platforms allow seamless data exchange, improving clinical workflow efficiency and reducing diagnostic delays. Hospitals prefer integrated systems for centralized patient data management and improved coordination between departments. Rising adoption of AI-based imaging tools further strengthens integration demand. Government healthcare digitization initiatives are also promoting unified diagnostic ecosystems.

The standalone platform segment is expected to witness the fastest growth rate of 16.9% from 2026 to 2033, driven by increasing adoption in small and mid-sized healthcare facilities with limited IT infrastructure. Standalone systems are easier to deploy and require lower initial investment. They are particularly suitable for emerging healthcare centers in Africa. Growing availability of cloud-based standalone AI tools is further supporting adoption. Flexibility and ease of installation make them attractive for rapid deployment scenarios.

- By Purchase Mode

On the basis of purchase mode, the market is segmented into institutional and individual. The institutional purchase mode dominated the market with the largest revenue share of 89.3% in 2025, driven by bulk procurement by hospitals, oncology centers, and government health programs. Institutions prefer centralized purchasing to ensure standardization of diagnostic tools across multiple facilities. Large-scale screening initiatives also rely heavily on institutional procurement. Government funding for cancer screening programs further supports dominance. The segment benefits from long-term contracts with software providers and integrated deployment models.

The individual purchase mode is expected to witness the fastest growth rate of 15.4% from 2026 to 2033, driven by increasing adoption in private diagnostic clinics and independent radiology practitioners. Rising affordability of AI-based screening tools is encouraging individual adoption. Growth of small diagnostic centers in urban areas is also supporting demand. Flexible subscription-based pricing models are making software more accessible. Increasing digitalization of private healthcare practices further accelerates growth.

- By End User

On the basis of end user, the market is segmented into oncology centers, hospitals, ambulatory surgical centers, and others. The hospitals segment dominated the market with the largest revenue share of 57.6% in 2025, driven by high patient inflow, advanced imaging infrastructure, and strong adoption of AI-based diagnostic tools. Hospitals serve as primary hubs for lung cancer screening programs in the region. Integration of screening software into radiology departments improves efficiency and accuracy. Government investments in hospital digitalization further support dominance. Hospitals also benefit from access to skilled radiologists and multidisciplinary oncology teams.

The oncology centers segment is expected to witness the fastest growth rate of 20.8% from 2026 to 2033, driven by increasing establishment of specialized cancer treatment facilities. These centers focus on early detection and personalized cancer care, driving demand for advanced screening software. Rising cancer awareness and referral rates are boosting patient volumes. Adoption of AI-enabled diagnostic systems is improving clinical outcomes. International collaborations and funding are further accelerating expansion of oncology centers.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender and third-party distributors. The direct tender segment dominated the market with the largest revenue share of 78.2% in 2025, driven by government procurement programs and large institutional contracts. Healthcare authorities prefer direct tenders for cost efficiency and standardized deployment across public hospitals. Bulk purchasing for national screening initiatives further strengthens dominance. Long-term agreements with software vendors ensure consistent system upgrades and support. This channel is widely used in GCC countries with centralized healthcare systems.

The third-party distributors segment is expected to witness the fastest growth rate of 18.1% from 2026 to 2033, driven by expanding private healthcare markets and increasing penetration in underserved regions. Distributors help smaller healthcare facilities access advanced screening solutions. They also provide localized support and implementation services. Growing demand from private diagnostic chains is accelerating this channel. Flexibility and wider market reach make distributors important for scaling adoption in Africa.

Middle East and Africa Lung Cancer Screening Software Market Regional Analysis

- Saudi Arabia dominated the Middle East and Africa lung cancer screening software market with the largest revenue share of 38.6% in 2025, characterized by advanced healthcare infrastructure, strong adoption of AI-enabled radiology platforms, and government-backed cancer screening initiatives driving large-scale deployment in tertiary hospitals

- Healthcare providers in the country highly value the improved diagnostic accuracy, early detection capabilities, and seamless integration of screening software with hospital systems such as PACS and EMR, enabling more efficient and standardized oncology workflows

- This widespread adoption is further supported by significant investments in advanced healthcare infrastructure, national cancer screening programs, and increasing awareness of early lung cancer detection, establishing Saudi Arabia as the key growth hub in the region

The Saudi Arabia Lung Cancer Screening Software Market Insight

The Saudi Arabia lung cancer screening software market captured the largest revenue share in the Middle East and Africa region in 2025, driven by strong government-led healthcare transformation programs and rapid adoption of AI-based diagnostic imaging solutions. Healthcare providers are increasingly prioritizing early lung cancer detection through advanced CT screening and AI-enabled radiology platforms. The growing integration of screening software with hospital systems such as PACS and EMR is further improving diagnostic efficiency and workflow standardization. Moreover, significant investments in oncology infrastructure and national cancer screening initiatives are strongly contributing to market expansion.

South Africa Lung Cancer Screening Software Market Insight

The South Africa lung cancer screening software market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing demand for early cancer detection and growing modernization of healthcare infrastructure. The rise in private healthcare investments and expansion of diagnostic imaging centers are fostering adoption of AI-based screening tools. South African healthcare providers are also focusing on improving radiology workflow efficiency through integrated digital platforms. Additionally, rising awareness of lung cancer screening among physicians and patients is supporting steady market growth across urban regions.

UAE Lung Cancer Screening Software Market Insight

The UAE lung cancer screening software market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by strong digital health adoption and advanced hospital infrastructure. The country’s emphasis on smart healthcare systems and AI integration is accelerating the deployment of lung cancer screening solutions in tertiary care hospitals. Increasing focus on precision medicine and early diagnosis is further encouraging adoption of advanced imaging software. Moreover, government initiatives promoting healthcare innovation and medical tourism are significantly supporting market development.

Egypt Lung Cancer Screening Software Market Insight

The Egypt lung cancer screening software market is expected to expand at a considerable CAGR during the forecast period, fueled by rising cancer burden and gradual improvements in healthcare infrastructure. Increasing investments in hospital modernization and diagnostic imaging capabilities are supporting adoption of screening software solutions. Egypt’s growing focus on expanding access to oncology care in public hospitals is further driving demand. Additionally, international collaborations and funding support are helping strengthen digital health transformation in the country.

Middle East and Africa Lung Cancer Screening Software Market Share

The Middle East and Africa Lung Cancer Screening Software industry is primarily led by well-established companies, including:

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V. (Netherlands)

- GE HealthCare (U.S.)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Fujifilm Holdings Corporation (Japan)

- Agfa-Gevaert N.V. (Belgium)

- Carestream Health, Inc. (U.S.)

- TeraRecon, Inc. (U.S.)

- Riverain Technologies LLC (U.S.)

- Median Technologies (France)

- Esaote S.p.A. (Italy)

- Visage Imaging GmbH (Germany)

- MeVis Medical Solutions AG (Germany)

- Riverain Technologies LLC (U.S.)

- Coreline Soft Co., Ltd. (South Korea)

- Lunit Inc. (South Korea)

- AZmed SAS (France)

- Thirona B.V. (Netherlands)

- Aidoc Medical Ltd. (Israel)

- Zebra Medical Vision Ltd. (Israel)

What are the Recent Developments in Middle East and Africa Lung Cancer Screening Software Market?

- In July 2025, Saudi Arabia initiated structured low-dose CT (LDCT) lung cancer screening programs supported by AI-enabled imaging systems to improve early detection rates among high-risk populations. The program integrates digital imaging workflows across hospitals and supports national early cancer detection strategy under healthcare transformation initiatives

- In June 2025, Saudi Arabia’s Ministry of Health and Seha Virtual Hospital used Lunit INSIGHT CXR AI software to screen hundreds of thousands of chest X-rays during the Hajj pilgrimage. The system enabled rapid detection of respiratory abnormalities and supported large-scale triage across millions of pilgrims. This deployment highlights real-world use of AI-based lung screening tools in mass public health programs in the Middle East

- In March 2025, Saudi Arabia expanded its deployment of AI-based chest X-ray screening software (Lunit INSIGHT CXR) through Dr. Sulaiman Al Habib Medical Group to analyze nearly 1 million chest X-rays over three years, supporting early detection of lung cancer, tuberculosis, and other thoracic diseases across its hospital network

- In February 2025, Coreline Soft presented its updated AVIEW AI-based lung cancer screening software at the European Congress of Radiology (ECR), highlighting ongoing deployments of AI diagnostic workflows in international screening programs that include Middle East hospital collaborations. The platform focuses on automated lung nodule detection and large-scale CT screening workflow optimization

- In January 2025, At Arab Health 2025 in Dubai, Philips introduced advanced AI-powered CT and cloud-based imaging software designed for oncology and lung screening workflows. These solutions aim to improve early diagnosis, automate reporting, and integrate imaging data across

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.