Middle East And Africa Lung Cancer Surgery Market

Market Size in USD Billion

USD

78.43 Billion

USD

106.51 Billion

2025

2033

USD

78.43 Billion

USD

106.51 Billion

2025

2033

| 2026 - 2033 | |

| USD 78.43 Billion | |

| USD 106.51 Billion | |

| % | |

|

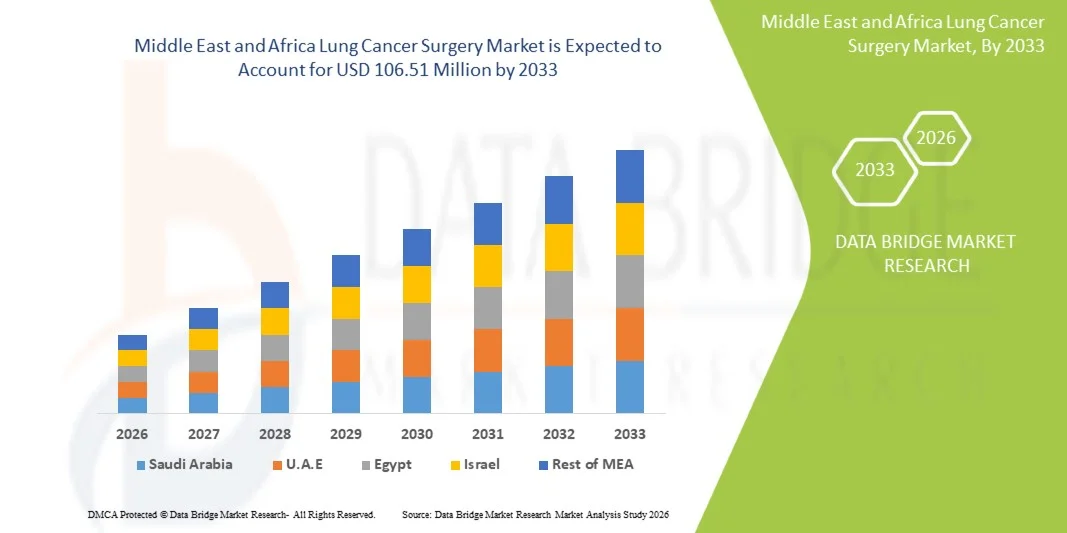

Middle East and Africa Lung Cancer Surgery Market Size

- The Middle East and Africa lung cancer surgery market size was valued at USD 78.43 million in 2025 and is expected to reach USD 106.51 million by 2033, at a CAGR of 3.9% during the forecast period

- The market growth is largely driven by the rising incidence of lung cancer across the region, along with gradual improvements in oncology infrastructure, surgical facilities, and access to advanced diagnostic technologies in both public and private healthcare systems

- Furthermore, increasing awareness regarding early cancer detection, coupled with growing adoption of minimally invasive and robotic-assisted surgical procedures, is supporting better treatment outcomes. These factors are collectively accelerating the uptake of lung cancer surgery solutions, thereby significantly boosting the industry's growth

Middle East and Africa Lung Cancer Surgery Market Analysis

- Lung cancer surgery, involving procedures such as lobectomy, pneumonectomy, and segmentectomy, is a critical treatment modality in the Middle East and Africa healthcare landscape due to its importance in managing early-stage and operable lung cancer cases with improved survival outcomes across specialized oncology centers and tertiary hospitals

- The escalating demand for lung cancer surgery is primarily driven by rising smoking prevalence, increasing exposure to environmental pollutants, growing cancer burden, and gradual improvements in diagnostic capabilities along with expanding surgical oncology infrastructure across select countries in the region

- South Africa dominated the Middle East and Africa lung cancer surgery market with the largest revenue share of 34.6% in 2025, supported by relatively advanced healthcare infrastructure, higher availability of thoracic surgeons, and a strong private hospital network with established oncology care services

- Saudi Arabia is expected to be the fastest growing country in the Middle East and Africa lung cancer surgery market during the forecast period, driven by healthcare modernization initiatives, rising investment in cancer specialty hospitals, and increasing adoption of advanced minimally invasive and robotic-assisted surgical techniques

- The minimally invasive surgery segment dominated the Middle East and Africa lung cancer surgery market with the largest share of 52.8% in 2025, attributed to shorter hospital stays, reduced postoperative complications, faster recovery times, and increasing preference for video-assisted thoracoscopic surgery (VATS) across advanced oncology centers

Report Scope and Middle East and Africa Lung Cancer Surgery Market Segmentation

|

Attributes |

Middle East and Africa Lung Cancer Surgery Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Middle East and Africa Lung Cancer Surgery Market Trends

“Rising Adoption of Minimally Invasive and Advanced Surgical Techniques”

- A significant and accelerating trend in the Middle East and Africa lung cancer surgery market is the growing adoption of minimally invasive procedures such as VATS and robotic-assisted thoracic surgery, improving patient outcomes and reducing recovery time

- For instance, the Da Vinci robotic surgical system is increasingly being adopted in leading hospitals across Saudi Arabia and South Africa to perform complex lung cancer resections with higher precision

- Integration of advanced imaging technologies and intraoperative navigation systems is enhancing surgical accuracy and enabling earlier detection of tumor margins, improving overall success rates of lung cancer surgeries

- Furthermore, hybrid operating rooms combining imaging and surgical capabilities are allowing surgeons to perform real-time decision-making during lung cancer procedures, improving treatment efficiency

- Growing training programs and surgical fellowships in thoracic oncology are further strengthening the availability of skilled surgeons capable of performing complex minimally invasive lung cancer surgeries

- This trend towards technologically advanced, precision-driven surgical approaches is fundamentally reshaping thoracic oncology practices across the region, with countries such as the United Arab Emirates expanding robotic surgery programs

- The demand for minimally invasive and robot-assisted lung cancer surgery is growing steadily across major healthcare systems as patients increasingly prefer less invasive treatment options with faster recovery

Middle East and Africa Lung Cancer Surgery Market Dynamics

Driver

“Rising Cancer Burden and Expanding Surgical Oncology Infrastructure”

- The increasing prevalence of lung cancer cases, coupled with improving awareness about early diagnosis and surgical treatment options, is a key driver for the growth of lung cancer surgery in the Middle East and Africa region

- For instance, in May 2025, Saudi Arabia expanded its National Cancer Center network, enhancing access to specialized thoracic surgery units and improving early-stage lung cancer treatment capabilities

- Governments and private healthcare providers are increasingly investing in advanced oncology infrastructure, including dedicated cancer hospitals and surgical oncology departments, to address rising patient demand

- Furthermore, growing tobacco consumption, air pollution, and occupational exposure to carcinogens are contributing to a higher incidence of lung cancer cases requiring surgical intervention

- The increasing availability of trained thoracic surgeons and improved hospital facilities is supporting the expansion of complex lung cancer surgeries across emerging healthcare markets

- Rising healthcare expenditure and government-led cancer control initiatives are significantly accelerating the adoption of advanced lung cancer surgical procedures across the region

- Expansion of medical tourism in countries such as the United Arab Emirates is further contributing to increased demand for advanced lung cancer surgical treatments

- Increasing adoption of multidisciplinary cancer care approaches combining surgery, chemotherapy, and radiotherapy is improving overall treatment outcomes and supporting surgical demand

Restraint/Challenge

“Limited Early Diagnosis and High Treatment Complexity”

- Limited early-stage lung cancer detection due to low screening coverage and delayed diagnosis remains a major challenge restricting the effectiveness of surgical intervention in the Middle East and Africa market

- For instance, in April 2025, reports from major oncology centers in Egypt highlighted that a large proportion of lung cancer patients are diagnosed at advanced stages, reducing eligibility for curative surgery

- Shortage of specialized thoracic surgeons and uneven distribution of advanced surgical facilities across countries further limits access to high-quality lung cancer surgical care

- Furthermore, high costs associated with robotic-assisted and minimally invasive surgical procedures pose affordability challenges, particularly in lower-income countries within the region

- The complexity of lung cancer surgeries and the need for highly skilled surgical teams increase procedural risks and limit widespread adoption in smaller healthcare facilities

- Limited healthcare insurance coverage for advanced oncological procedures restricts patient access to high-cost surgical interventions across several countries

- Addressing these challenges through improved screening programs, capacity building, and expansion of affordable surgical infrastructure will be essential for sustained market growth

Middle East and Africa Lung Cancer Surgery Market Scope

The market is segmented on the basis of product type, surgical procedure, patient type, end user, and distribution channel.

- By Product Type

On the basis of product type, the Middle East and Africa lung cancer surgery market is segmented into surgical instruments, monitoring & visualizing systems, endosurgical equipment, robotic-assisted thoracic surgery systems, and others. The surgical instruments segment dominated the market with the largest revenue share of 38.4% in 2025, driven by their fundamental role in all open and minimally invasive lung cancer procedures. These instruments, including forceps, retractors, and staplers, are widely used across hospitals due to their cost-effectiveness and repeat usability. The high procedural volume of thoracotomies and lobectomies further supports consistent demand for surgical instruments. In addition, increasing investments in upgrading operating rooms across South Africa and Saudi Arabia are strengthening adoption. Hospitals continue to prioritize essential surgical tools over advanced systems in cost-sensitive healthcare settings. The segment remains indispensable across all stages of lung cancer surgery.

The robotic-assisted thoracic surgery systems segment is expected to witness the fastest growth rate of 19.6% from 2026 to 2033, driven by rising adoption of precision-based surgical technologies in advanced healthcare facilities. Increasing investments in robotic surgery platforms such as Da Vinci systems in the United Arab Emirates and Saudi Arabia are significantly boosting demand. These systems offer enhanced accuracy, reduced surgical trauma, and faster patient recovery. Growing preference for minimally invasive cancer treatment is further accelerating adoption. Training programs for robotic surgery are expanding across tertiary hospitals, improving surgeon readiness. Rising healthcare modernization initiatives are also supporting deployment of high-cost robotic platforms.

- By Surgical Procedure

On the basis of surgical procedure, the market is segmented into thoracotomy and minimally invasive surgery. The minimally invasive surgery segment dominated the market with the largest revenue share of 52.8% in 2025, driven by increasing preference for video-assisted thoracoscopic surgery (VATS) and robotic-assisted procedures. These techniques offer reduced postoperative complications, shorter hospital stays, and improved patient recovery outcomes. Growing awareness among surgeons regarding less invasive approaches is strengthening adoption. Advanced hospitals in Saudi Arabia and South Africa are increasingly shifting toward minimally invasive lung resections. Technological advancements in imaging and surgical tools further support procedural accuracy. Patient preference for faster recovery is also contributing to segment dominance.

The minimally invasive surgery segment is also expected to witness the fastest growth rate of 18.3% from 2026 to 2033, driven by continuous technological advancements and increasing healthcare infrastructure development. Expanding access to robotic-assisted thoracic surgery systems is enhancing procedural efficiency. Rising investments in oncology centers are enabling wider adoption of advanced surgical techniques. Growing training initiatives for thoracic surgeons are improving procedural capabilities. Increasing healthcare expenditure in the UAE and Saudi Arabia is further supporting growth. The shift toward precision-based cancer treatment is accelerating long-term adoption of minimally invasive procedures.

- By Patient Type

On the basis of patient type, the market is segmented into male and female. The male segment dominated the market with the largest revenue share of 67.1% in 2025, primarily due to the higher prevalence of smoking-related lung cancer among men in the Middle East and Africa region. Occupational exposure to carcinogens and higher tobacco consumption rates contribute significantly to male patient dominance. Late-stage diagnosis in male patients also increases the need for surgical intervention. Awareness programs targeting male smokers are gradually improving early detection rates. Hospitals report a higher volume of thoracic surgeries performed on male patients. This trend continues to shape surgical demand patterns across the region.

The female segment is expected to witness the fastest growth rate of 14.8% from 2026 to 2033, driven by increasing lung cancer incidence among non-smoking women due to environmental pollution and secondhand smoke exposure. Rising awareness about cancer screening among women is improving diagnosis rates. Expanding access to healthcare services in urban centers is supporting early detection. Lifestyle changes and urbanization are contributing to increasing risk factors. Healthcare providers are focusing more on gender-specific oncology programs. This is gradually increasing surgical intervention rates among female patients.

- By End User

On the basis of end user, the market is segmented into hospitals, ambulatory surgical centres, academic & research laboratories, speciality cancer care centres, and others. The hospitals segment dominated the market with the largest revenue share of 58.9% in 2025, driven by their strong infrastructure, availability of advanced surgical equipment, and presence of skilled thoracic surgeons. Hospitals remain the primary centers for complex lung cancer surgeries such as lobectomy and pneumonectomy. Government and private hospitals in South Africa and Saudi Arabia are key contributors to procedural volume. Integrated oncology departments support comprehensive cancer care. Higher patient inflow further strengthens hospital dominance. Continuous investments in hospital infrastructure support advanced surgical capabilities.

The speciality cancer care centres segment is expected to witness the fastest growth rate of 17.2% from 2026 to 2033, driven by increasing establishment of dedicated oncology facilities across the region. These centres offer specialized thoracic surgery services with advanced technologies. Rising demand for focused cancer treatment is supporting their expansion. Governments are investing in building cancer hospitals under national healthcare programs. Collaboration with international oncology institutions is enhancing treatment quality. Growing patient preference for specialized care is accelerating adoption of these centres.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, retail sales, online sales, and others. The direct tender segment dominated the market with the largest revenue share of 64.5% in 2025, driven by bulk procurement of surgical equipment by hospitals and government healthcare institutions. Public hospitals in Saudi Arabia and South Africa largely depend on tender-based procurement for high-value surgical systems. Long-term supply contracts with manufacturers ensure consistent availability of surgical instruments. Cost efficiency in large-scale procurement further supports dominance. Government healthcare programs heavily rely on direct tendering systems. This channel remains the primary procurement method for advanced surgical technologies.

The online sales segment is expected to witness the fastest growth rate of 16.4% from 2026 to 2033, driven by increasing digitalization of medical procurement processes. Hospitals and clinics are gradually adopting online platforms for ordering surgical consumables and instruments. Improved transparency and faster delivery systems are supporting adoption. Expansion of medical e-commerce platforms in the UAE and South Africa is further accelerating growth. Smaller healthcare facilities prefer online procurement for cost efficiency. Growing digital infrastructure across the healthcare sector is enabling long-term expansion of this channel.

Middle East and Africa Lung Cancer Surgery Market Regional Analysis

- South Africa dominated the Middle East and Africa lung cancer surgery market with the largest revenue share of 34.6% in 2025, supported by relatively advanced healthcare infrastructure, higher availability of thoracic surgeons, and a strong private hospital network with established oncology care services

- Patients in the country are increasingly accessing surgical oncology services due to better awareness of lung cancer treatment options and improved referral systems within both public and private healthcare facilities

- This dominance is further supported by strong penetration of private hospital networks, availability of advanced surgical technologies, and growing adoption of minimally invasive procedures such as VATS, establishing South Africa as the leading hub for lung cancer surgical interventions in the region

The South Africa Lung Cancer Surgery Market Insight

South Africa dominated the Middle East and Africa lung cancer surgery market with the largest revenue share of 34.6% in 2025, fueled by relatively advanced oncology infrastructure and higher availability of specialized thoracic surgeons. Patients in the country are increasingly prioritizing access to surgical treatment for early and operable lung cancer due to improved awareness and referral systems. The growing adoption of minimally invasive procedures such as VATS, along with strong penetration of private hospitals, further propels market growth. Moreover, the integration of advanced imaging systems and increasing investment in cancer care facilities is significantly contributing to the market’s expansion.

Saudi Arabia Lung Cancer Surgery Market Insight

The Saudi Arabia lung cancer surgery market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by strong government-led healthcare transformation programs and rising investment in oncology infrastructure. The increase in lung cancer awareness, coupled with growing demand for advanced surgical treatments, is fostering adoption of minimally invasive and robotic-assisted surgeries. Patients are also drawn to improved hospital facilities and access to specialized cancer centers. Furthermore, expanding digital health initiatives and integration of advanced surgical technologies are supporting market growth across both public and private healthcare sectors.

United Arab Emirates Lung Cancer Surgery Market Insight

The United Arab Emirates lung cancer surgery market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising medical tourism and a strong focus on advanced healthcare services. The country’s high adoption of robotic surgery systems and minimally invasive techniques is improving surgical outcomes and attracting regional patients. In addition, increasing prevalence of lifestyle-related risk factors and enhanced cancer screening programs are supporting early diagnosis and treatment. The UAE’s robust healthcare infrastructure and continuous investment in smart hospitals are expected to further stimulate market growth.

Egypt Lung Cancer Surgery Market Insight

The Egypt lung cancer surgery market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing lung cancer incidence and gradual improvements in healthcare accessibility. Rising awareness about cancer diagnosis and treatment options is encouraging more patients to opt for surgical intervention. The expansion of public oncology hospitals and collaborations with international healthcare organizations are improving surgical capacity. Moreover, increasing investments in medical training and infrastructure development are strengthening the availability of thoracic surgery services across the country.

Middle East and Africa Lung Cancer Surgery Market Share

The Middle East and Africa Lung Cancer Surgery industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Intuitive Surgical, Inc. (U.S.)

- Olympus Corporation (Japan)

- FUJIFILM Corporation (Japan)

- Ambu A/S (Denmark)

- Teleflex Incorporated (U.S.)

- Accuray Incorporated (U.S.)

- KARL STORZ SE & Co. KG (Germany)

- Richard Wolf GmbH (Germany)

- KLS Martin Group (Germany)

- Ackermann Instrumente GmbH (Germany)

- TROKAMED GmbH (Germany)

- asap endoscopic products GmbH (Germany)

- Surgical Holdings (U.K.)

- AngioDynamics, Inc. (U.S.)

- Scanlan International, Inc. (U.S.)

- Sontec Instruments, Inc. (U.S.)

- FusionKraft (Germany)

- Lepu Medical Technology (Beijing) Co., Ltd. (China)

What are the Recent Developments in Middle East and Africa Lung Cancer Surgery Market?

- In April 2026, Burjeel Medical City in the United Arab Emirates performed the country’s first uniportal robotic lung cancer lobectomy, marking a major milestone in minimally invasive thoracic surgery. The procedure was completed using the da Vinci Xi system on an early-stage lung cancer patient through a single small incision. The surgery demonstrated reduced recovery time and minimal complications, reinforcing the UAE’s leadership in advanced robotic surgical care in the region

- In January 2026, American Hospital Dubai launched the da Vinci 5 robotic surgical system, making it one of the first healthcare institutions in the Middle East to deploy next-generation robotic surgery technology. The system enhances precision in complex thoracic and lung cancer surgeries, supporting minimally invasive approaches. This advancement is strengthening Dubai’s role as a regional hub for advanced oncological surgery and medical innovation

- In October 2025, Johns Hopkins Aramco Healthcare (JHAH) announced the expansion of its robot-assisted thoracic surgery program in Saudi Arabia, successfully performing complex lung procedures including robotic lobectomy and diaphragm surgeries. The development highlights the increasing adoption of minimally invasive lung cancer surgery in the Kingdom, supported by advanced da Vinci robotic systems and international surgical collaboration

- In February 2025, advancements in robot-assisted thoracic surgery (RATS) were highlighted in clinical research, showcasing improved precision, better visualization, and reduced surgical trauma in complex lung cancer procedures. These developments are increasingly being adopted in advanced healthcare systems across the Middle East and Africa, particularly in countries such as the United Arab Emirates and Saudi Arabia

- In January 2025, clinical evidence emphasized the growing adoption of video-assisted thoracoscopic surgery (VATS) as a preferred minimally invasive technique for lung cancer treatment. The technique is gaining traction in Middle East and Africa hospitals due to reduced postoperative complications, shorter hospital stays, and faster patient recovery. Healthcare systems in South Africa and Gulf countries are increasingly shifting from open thoracotomy to VATS-based procedures

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.