Middle East And Africa Malaria Treatment Market

Market Size in USD Billion

USD

2.22 Billion

USD

3.72 Billion

2025

2033

USD

2.22 Billion

USD

3.72 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.22 Billion | |

| USD 3.72 Billion | |

| % | |

|

Middle East and Africa Malaria Treatment Market Overview

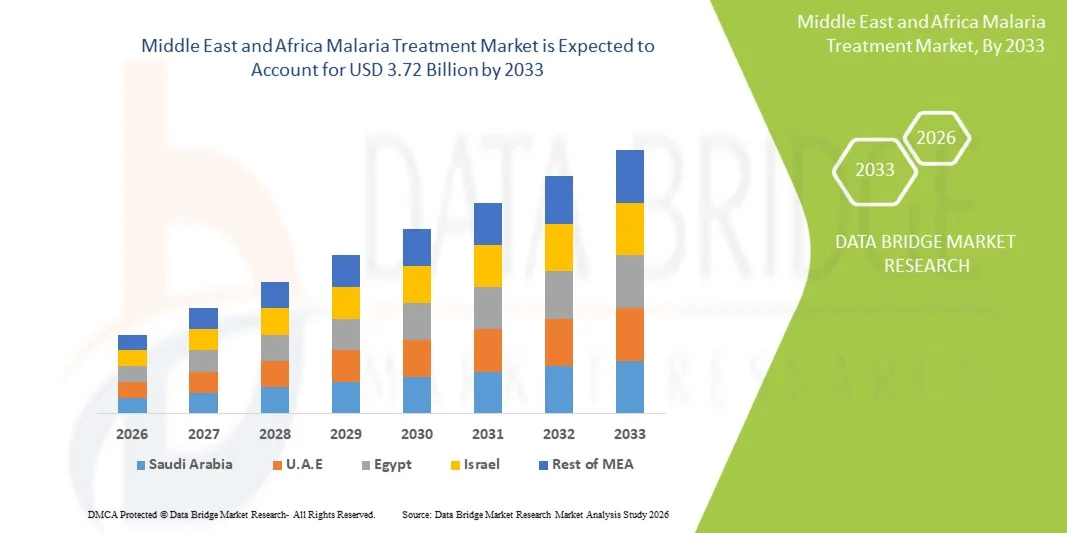

The Middle East and Africa malaria treatment market was valued at USD 2.22 billion in 2025 and is projected to reach USD 3.72 billion by 2033, growing at a CAGR of 6.70% from 2026 to 2033. The market is witnessing steady expansion driven by the high burden of malaria in Sub-Saharan Africa, increasing international funding for malaria eradication programs, and growing access to diagnostic and treatment services in rural and underserved regions. Rising deployment of artemisinin-based combination therapies (ACTs), improved availability of rapid diagnostic tests, and strengthened public health initiatives are further supporting market growth.

The increasing focus on malaria elimination strategies, combined with large-scale government and NGO-led intervention programs, is significantly boosting treatment adoption across endemic countries. Expansion of healthcare infrastructure, improved supply chain networks for anti-malarial drugs, and rising awareness regarding early diagnosis and treatment are also contributing to market development. In addition, ongoing research into next-generation antimalarial drugs and combination therapies is enhancing treatment effectiveness, supporting long-term disease control efforts across the Middle East and Africa region.

Key Market Trends & Insights

- Saudi Arabia dominated the Middle East and Africa malaria treatment market with the largest revenue share of 28.74% in 2025, supported by strong healthcare infrastructure, high investment in infectious disease surveillance, and significant treatment demand from imported and border-region malaria cases.

- The Plasmodium falciparum segment led the market with a 68.45% share in 2025, driven by high prevalence across sub-Saharan Africa and its association with severe and life-threatening malaria cases requiring immediate treatment intervention.

- United Arab Emirates (UAE) is expected to be the fastest-growing country at a CAGR of 7.4% from 2026 to 2033, driven by increasing travel-related malaria cases, expansion of advanced diagnostic infrastructure, and growing hospital modernization programs.

- vivax are the fastest-growing agent type, projected to register a CAGR of 6.8%, reflecting the surge in demand for detection in parts of East Africa and Middle Eastern regions.

- The artemisinin compounds segment dominated the drug class category with a 46.12% revenue share in 2025, led by widespread use of WHO-recommended artemisinin-based combination therapies (ACTs) as first-line treatment for Plasmodium falciparum, strong government procurement programs in high-burden countries.

- Generics accounted for 74.28% of the market, preferred by large-scale public procurement programs and cost-sensitive healthcare systems across MEA countries.

- The molecular diagnostic tests segment is the fastest-growing software category, with a CAGR of 7.1%, driven by increasing demand for high-accuracy detection and resistance monitoring.

Market Size & Forecast

- Global Market Value (2025): USD 2.22 Billion

- Expected Market Value (2033): USD 3.72 Billion

- Forecast CAGR (2026–2033): 6.70%

- Leading Country in 2025: Saudi Arabia

- Fastest Growing Country: United Arab Emirates

Report Scope and Middle East and Africa Malaria Treatment Market Segmentation

|

Attributes |

Middle East and Africa Malaria Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa |

|

Key Market Players |

· Novartis AG (Switzerland) · GSK plc (U.K.) · Sanofi (France) · Pfizer Inc. (U.S.) · F. Hoffmann-La Roche Ltd (Switzerland) · Abbott (U.S.) · Siemens Healthineers AG (Germany) · BD (U.S.) · Bio-Rad Laboratories, Inc. (U.S.) · Viatris Inc. (U.S.) · Cipla Limited (India) · Sun Pharmaceutical Industries Ltd. (India) · Dr. Reddy’s Laboratories Ltd. (India) · Ipca Laboratories Ltd. (India) · Ajanta Pharma Ltd. (India) · Strides Pharma Science Limited (India) · AstraZeneca (U.K.) · Johnson & Johnson Services, Inc. (U.S.) · Medicines for Malaria Venture (Switzerland) · PATH (U.S.) |

|

Market Opportunities |

· Expansion of rapid diagnostic testing (RDT) and point-of-care screening · Scaling rollout of malaria vaccines such as RTS,S and R21 · Increasing investment in artemisinin resistance monitoring and next-generation combination therapies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Middle East and Africa Malaria Treatment Market Trends

Trend: Expansion of Community-Based Malaria Diagnosis and Treatment Programs

National malaria control strategies across the Middle East and Africa are increasingly focusing on decentralized, community-driven healthcare delivery models to improve early diagnosis and rapid treatment initiation. This shift is particularly important in rural and remote areas where access to hospitals and diagnostic laboratories is limited, leading to delayed treatment and higher mortality rates. The deployment of rapid diagnostic tests (RDTs) at the community level is significantly improving detection accuracy and enabling immediate treatment decisions without reliance on centralized facilities. In parallel, mobile health platforms and digital surveillance tools are being introduced to track malaria cases, monitor drug distribution, and identify outbreak hotspots in real time, improving responsiveness and resource allocation.

For instance, in Nigeria and Uganda, community health worker programs supported by RDT kits and pre-positioned antimalarial drugs are enabling same-day diagnosis and treatment initiation, reducing progression to severe malaria and improving survival rates in high-risk populations.

Middle East and Africa Malaria Treatment Market Dynamics

Key Market Driver: Rising Burden of Malaria and Expanding Public Health Funding

The MEA region continues to bear the highest global malaria burden, with persistent transmission in many sub-Saharan African countries creating sustained demand for effective and accessible treatment options. Governments, along with international funding organizations such as the Global Fund, WHO-backed initiatives, and bilateral aid programs, are significantly increasing investments in malaria control and elimination efforts. These funds are primarily directed toward large-scale procurement of artemisinin-based combination therapies (ACTs), strengthening diagnostic infrastructure, and expanding preventive care programs. In addition, national health systems are gradually integrating malaria treatment into broader universal healthcare frameworks, improving affordability and patient reach. This combination of high disease prevalence and expanding funding is creating a stable and continuously growing treatment market.

For instance, Nigeria and the Democratic Republic of Congo receive substantial donor-supported procurement assistance, allowing large-scale distribution of subsidized antimalarial drugs across public hospitals and rural clinics, thereby expanding treatment coverage even in underserved communities.

Key Restraint/Challenge: Drug Resistance and Weak Healthcare Infrastructure Limitations

A major challenge facing the malaria treatment market in MEA is the increasing threat of partial resistance to artemisinin-based therapies, which can reduce treatment effectiveness and require more complex combination regimens. This issue is compounded by weak healthcare infrastructure in several countries, where limited diagnostic facilities, inadequate cold-chain logistics, and inconsistent drug supply chains hinder timely and effective treatment delivery. Rural and conflict-affected areas are particularly vulnerable due to poor healthcare access and shortages of trained medical personnel. These systemic issues result in delayed diagnosis, incomplete treatment adherence, and higher risk of disease complications.

For instance, inconsistent drug availability and treatment interruptions in regions of South Sudan and Mozambique highlight how infrastructure gaps and logistical constraints can directly undermine malaria control efforts and slow progress toward elimination goals

Key Market Opportunity: Scaling Next-Generation Antimalarial Therapies and Integrated Vaccine Deployment

A significant opportunity in the MEA malaria treatment market lies in the integration of advanced therapeutic solutions with large-scale preventive vaccination programs to create a more holistic disease management approach. The introduction of malaria vaccines such as RTS,S and R21 is opening new pathways for reducing infection rates, which in turn complements existing drug-based treatment strategies and reduces overall disease burden. At the same time, pharmaceutical innovation is accelerating the development of next-generation antimalarial combinations designed to address emerging drug resistance and improve treatment efficacy. There is also growing interest in long-acting injectable therapies and simplified single-dose regimens that can improve patient compliance in resource-limited settings

For instance, coordinated rollout of RTS,S and R21 vaccines in countries such as Ghana, Kenya, and Malawi, alongside continued ACT-based treatment programs, is demonstrating how combined prevention and treatment strategies can significantly reduce malaria incidence and improve long-term disease control outcomes.

Middle East and Africa Malaria Treatment Market Scope

The Middle East and Africa malaria treatment market is segmented on the basis of agent, drug class, drug type, treatment, diagnosis, route of administration, age group, dosage form, end-users, and distribution channel.

- By Agent

On the basis of agent, the Middle East and Africa malaria treatment market is segmented into Plasmodium falciparum, P. vivax, P. ovale, P. malariae, and P. knowlesi. The Plasmodium falciparum segment dominated the market with a 68.45% share in 2025, due to its high prevalence across sub-Saharan Africa and its association with severe and life-threatening malaria cases requiring immediate treatment intervention. This species drives the majority of hospital admissions and antimalarial drug consumption, particularly in high-burden countries such as Nigeria, the Democratic Republic of Congo, and Mozambique. Strong reliance on ACT-based therapies for P. falciparum further reinforces its dominance in treatment demand. Continuous transmission in tropical climates and resistance concerns also increase its clinical importance. Public health programs prioritize P. falciparum elimination due to its high mortality risk. Its dominance is expected to persist due to limited reduction in transmission intensity.

The P. vivax segment is expected to be the fastest-growing, registering a CAGR of 6.8% from 2026 to 2033, driven by increasing detection in parts of East Africa and Middle Eastern regions. Improved diagnostic capabilities are enabling better identification of non-falciparum infections that were previously underreported. Rising cross-border migration and travel are also contributing to its spread in low-to-moderate transmission areas. Treatment complexity due to relapse patterns is increasing demand for specialized therapies. Expansion of surveillance programs is improving reporting accuracy. Growing focus on elimination of all malaria species is further supporting segment growth.

- By Drug Class

On the basis of drug class, the market is segmented into aryl aminoalcohol compounds, antifolate compounds, artemisinin compounds, and others. The artemisinin compounds segment dominated the market with a 46.12% share in 2025, owing to WHO recommendation as first-line therapy for uncomplicated malaria, especially P. falciparum infections. Artemisinin-based combination therapies (ACTs) are widely distributed across public healthcare systems due to their high efficacy and rapid parasite clearance. Large-scale procurement by governments and donor agencies ensures consistent availability across endemic countries. Their ability to reduce resistance development when used in combination therapies strengthens clinical preference. Continuous inclusion in national treatment guidelines further reinforces dominance. Strong supply chain integration across Africa sustains widespread usage.

The aryl aminoalcohol compounds segment is the fastest-growing, projected to register a CAGR of 6.5% from 2026 to 2033, driven by increasing use in severe malaria and drug-resistant cases. These compounds are gaining importance in hospital settings where advanced treatment protocols are required. Rising ICU admissions and complicated malaria cases are boosting demand. Improved clinical guidelines recommending combination therapies are supporting adoption. Pharmaceutical innovation is enhancing drug safety and effectiveness. Expansion of tertiary healthcare infrastructure is further accelerating usage.

- By Drug Type

On the basis of drug type, the market is segmented into branded and generics. The generics segment dominated the market with a 74.28% share in 2025, driven by large-scale public procurement programs and cost-sensitive healthcare systems across MEA countries. Generic antimalarial drugs are widely used in national malaria control programs due to affordability and bulk purchasing by governments and NGOs. Strong presence of WHO-prequalified generic manufacturers ensures steady supply. High disease burden and limited healthcare budgets further reinforce dependence on generics. They are extensively distributed through public hospitals and rural clinics. Their accessibility ensures treatment continuity in underserved populations.

The branded drugs segment is the fastest-growing, registering a CAGR of 6.3% from 2026 to 2033, supported by increasing adoption in private hospitals and specialty clinics. Rising demand for higher-quality, fast-acting formulations is driving preference for branded therapies. Expanding private healthcare infrastructure in urban MEA regions is supporting segment growth. Pharmaceutical companies are introducing improved formulations with better compliance profiles. Patients in higher-income segments prefer branded drugs for perceived efficacy and safety. Growing healthcare expenditure is further accelerating adoption.

- By Treatment

On the basis of treatment, the market is segmented into antimalarial drugs and others. The antimalarial drugs segment dominated the market with a 92.15% share in 2025, due to its central role as the primary treatment method for all malaria cases across MEA. ACTs, injectable artesunate, and supportive therapies form the backbone of national malaria treatment guidelines. Widespread government procurement and donor funding ensure continuous availability. High disease incidence and rapid treatment requirement sustain dominance. Clinical protocols strongly prioritize immediate pharmacological intervention. Hospitals and clinics rely almost entirely on drug-based treatment pathways.

The others segment is the fastest-growing, projected to register a CAGR of 6.7% from 2026 to 2033, driven by increasing adoption of supportive care, preventive therapies, and integrated vaccination programs. Expansion of malaria vaccines such as RTS,S and R21 is gradually diversifying treatment approaches. Improved vector control and preventive interventions are complementing drug-based therapies. Rising focus on holistic malaria management strategies is accelerating adoption. Public health systems are integrating multi-layered treatment frameworks. This shift supports long-term disease control objectives.

- By Diagnosis

On the basis of diagnosis, the market is segmented into rapid diagnostics, microscopy, and molecular diagnostic tests. The rapid diagnostic tests (RDTs) segment dominated the market with a 58.62% share in 2025, due to their ease of use, low cost, and suitability for rural and resource-limited settings. RDTs enable quick detection and immediate treatment initiation, reducing mortality rates. They are widely deployed in community health programs across Africa. Strong government and NGO support ensures large-scale distribution. Minimal infrastructure requirements make them highly scalable. Their role in field-level diagnosis strengthens disease control programs.

The molecular diagnostic tests segment is the fastest-growing, projected to register a CAGR of 7.1% from 2026 to 2033, driven by increasing demand for high-accuracy detection and resistance monitoring. Advanced laboratories are adopting PCR-based testing for surveillance and research applications. These methods help identify low-density infections and drug-resistant strains. Expansion of healthcare infrastructure is supporting adoption in urban centers. International funding for malaria elimination programs is further accelerating usage. Improved diagnostic precision is driving long-term growth.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, parenteral, and others. The oral segment dominated the market with a 71.36% share in 2025, due to widespread use of ACT tablets for uncomplicated malaria treatment. Oral therapies are easy to administer, cost-effective, and suitable for outpatient and community-level care. Large-scale distribution programs rely heavily on oral formulations. Patient compliance is higher due to non-invasive administration. They are widely used across rural and primary healthcare settings. Their simplicity ensures dominance in large population treatment programs.

The parenteral segment is the fastest-growing, registering a CAGR of 6.9% from 2026 to 2033, driven by increasing hospital admissions for severe malaria cases. Injectable artesunate is widely used in critical care management. Rising awareness of severe malaria complications is boosting hospital-based treatment demand. Expansion of emergency healthcare infrastructure supports growth. Improved clinical guidelines recommend parenteral therapy for complicated cases. This segment is critical for reducing malaria mortality rates.

- By Age Group

On the basis of age group, the market is segmented into pediatric, adult, and geriatric. The pediatric segment dominated the market with a 52.84% share in 2025, as children under five are the most vulnerable population group affected by malaria in MEA. High infection rates and mortality among children drive strong treatment demand. National immunization and treatment programs prioritize pediatric care. Donor-funded initiatives focus heavily on child health interventions. Hospitals and clinics maintain dedicated pediatric malaria treatment protocols. This segment remains central to public health strategies.

The geriatric segment is the fastest-growing, projected to register a CAGR of 6.6% from 2026 to 2033, driven by increasing life expectancy and improved healthcare access in MEA countries. Elderly populations are becoming more susceptible due to weakened immunity. Rising chronic disease prevalence increases complication risks. Healthcare systems are expanding geriatric care services. Improved diagnosis in older age groups is supporting treatment uptake. This segment is gradually gaining clinical importance.

- By Dosage Form

On the basis of dosage form, the market is segmented into tablet, injection, and others. The tablet segment dominated the market with a 63.47% share in 2025, due to widespread use of oral ACT regimens for uncomplicated malaria treatment. Tablets are easy to distribute, store, and administer in low-resource settings. Public health programs rely heavily on tablet formulations for mass treatment campaigns. They ensure high patient compliance and affordability. Their stability under varying environmental conditions supports rural usage. This makes them the most widely used dosage form.

The injection segment is the fastest-growing, registering a CAGR of 6.8% from 2026 to 2033, driven by rising severe malaria cases requiring hospital-based care. Injectable artesunate is increasingly used in emergency treatment protocols. Expansion of ICU and hospital infrastructure supports growth. Improved survival outcomes are driving clinical preference for injectables. Government guidelines strongly recommend parenteral therapy for severe cases. This segment is essential for critical care management.

- By End-Users

On the basis of end-users, the market is segmented into hospitals, specialty clinics, homecare, and others. The hospitals segment dominated the market with a 54.18% share in 2025, due to high patient admissions for severe malaria cases requiring immediate medical intervention. Hospitals serve as primary treatment centers for complicated infections. They are equipped with diagnostic and intensive care facilities. Government funding and infrastructure investments support hospital-based treatment systems. Large patient inflow ensures consistent drug demand. They remain the backbone of malaria treatment delivery.

The homecare segment is the fastest-growing, projected to register a CAGR of 7.0% from 2026 to 2033, driven by expansion of community healthcare programs and self-administered oral therapies. Increasing use of rapid diagnostics enables early home-based treatment. Mobile health initiatives support remote patient monitoring. Rising awareness of early treatment benefits is driving adoption. Cost reduction in hospital visits is further supporting growth. This segment is expanding rapidly in rural regions.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, online pharmacy, and others. The hospital pharmacy segment dominated the market with a 48.92% share in 2025, due to centralized procurement and distribution of antimalarial drugs through public healthcare systems. Hospitals act as key distribution hubs for government-funded programs. Bulk purchasing agreements ensure steady drug supply. Strong integration with national malaria control programs supports dominance. Rural hospitals rely heavily on centralized distribution systems. This ensures consistent treatment availability.

The online pharmacy segment is the fastest-growing, projected to register a CAGR of 7.2% from 2026 to 2033, driven by rising digital health adoption and improved internet penetration in urban MEA regions. E-pharmacy platforms are improving access to medicines in remote areas. Growing smartphone usage is supporting digital procurement of drugs. Logistics improvements are enabling faster drug delivery. Regulatory support for telemedicine is strengthening adoption. This segment is transforming healthcare accessibility in urbanizing regions.

Middle East and Africa Malaria Treatment Market Regional Analysis

Saudi Arabia dominated the Middle East and Africa malaria treatment market with the largest revenue share of 28.74% in 2025, supported by strong healthcare infrastructure, high investment in infectious disease surveillance, and significant treatment demand from imported and border-region malaria cases. The country also benefits from effective border health screening, increasing imported malaria case management, and rapid adoption of advanced diagnostic technologies such as rapid diagnostic tests and molecular assays. Continuous modernization of hospital systems, strong pharmaceutical procurement networks, and integration of digital health platforms further strengthen Saudi Arabia’s leadership position in the regional malaria treatment market.

The Saudi Arabia Malaria Treatment Market Insight

The Saudi Arabia malaria treatment market is witnessing steady growth due to increasing imported malaria cases, strong border health surveillance systems, and advanced healthcare infrastructure. The country’s well-developed hospital network and government-led infectious disease control programs are supporting early diagnosis and effective treatment management. In addition, rising adoption of rapid diagnostic tests, molecular testing methods, and advanced antimalarial therapies is enhancing treatment efficiency. Continuous investment in digital health systems and public health monitoring, along with strong pharmaceutical procurement frameworks, is further strengthening Saudi Arabia’s position in the regional malaria treatment landscape.

UAE Malaria Treatment Market Insight

The UAE malaria treatment market is experiencing rapid growth, driven by increasing travel-related malaria cases, a large expatriate population, and strong investments in advanced healthcare infrastructure. The country’s focus on modernizing hospital systems and expanding infectious disease surveillance is boosting demand for rapid diagnostic tools and effective antimalarial therapies. In addition, growing adoption of AI-enabled diagnostics, telemedicine platforms, and integrated healthcare solutions is improving treatment accessibility and efficiency. Continuous healthcare innovation and strong government support for preventive and curative care are positioning the UAE as one of the fastest-growing markets in the region.

Nigeria Malaria Treatment Market Insight

The Nigeria malaria treatment market is witnessing strong expansion due to the highest malaria burden globally, widespread transmission of Plasmodium falciparum, and large-scale government-led malaria control programs. The country’s reliance on donor-funded procurement systems and extensive distribution of artemisinin-based combination therapies (ACTs) is driving consistent treatment demand across public healthcare facilities. In addition, increasing deployment of rapid diagnostic tests (RDTs), expansion of community health worker programs, and improved access to subsidized antimalarial drugs are strengthening early diagnosis and treatment coverage. Continuous investments from global health organizations and national malaria elimination initiatives further reinforce Nigeria’s dominant position in the regional market.

Kenya Malaria Treatment Market Insight

The Kenya malaria treatment market is experiencing steady growth due to expanding healthcare infrastructure, strong vector control programs, and increasing adoption of rapid diagnostic testing across rural and urban areas. The country’s focus on malaria elimination strategies, including insecticide-treated bed nets and improved surveillance systems, is supporting early detection and timely treatment. In addition, rising availability of subsidized antimalarial drugs through public healthcare channels is improving treatment accessibility. Growing investment in digital health systems and community-based care programs is further enhancing malaria management efficiency, positioning Kenya as one of the key emerging markets in the region.

Middle East and Africa Malaria Treatment Market Share

The Middle East and Africa malaria treatment industry is primarily led by well-established companies, including:

- Novartis AG (Switzerland)

- GSK plc (U.K.)

- Sanofi (France)

- Pfizer Inc. (U.S.)

- Hoffmann-La Roche Ltd (Switzerland)

- Abbott (U.S.)

- Siemens Healthineers AG (Germany)

- BD (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Viatris Inc. (U.S.)

- Cipla Limited (India)

- Sun Pharmaceutical Industries Ltd. (India)

- Reddy’s Laboratories Ltd. (India)

- Ipca Laboratories Ltd. (India)

- Ajanta Pharma Ltd. (India)

- Strides Pharma Science Limited (India)

- AstraZeneca (U.K.)

- Johnson & Johnson Services, Inc. (U.S.)

- Medicines for Malaria Venture (Switzerland)

- PATH (U.S.)

Latest Developments in Middle East and Africa Malaria Treatment Market

- In October 2024, Nigeria officially launched the routine rollout of the RTS,S malaria vaccine into its national immunization program, marking a major step in integrating malaria prevention with existing treatment strategies such as ACT-based therapies and rapid diagnostic testing. The program targets children under five in high-burden regions and is supported by WHO, UNICEF, and Gavi to reduce malaria-related mortality. This initiative represents a significant shift toward combining preventive vaccination with established malaria treatment frameworks to strengthen disease control efforts across the country

- In October 2023, the World Health Organization recommended the R21/Matrix-M malaria vaccine for widespread use in malaria-endemic countries, expanding the global vaccine toolkit alongside RTS,S. This approval enabled African countries across the Middle East and Africa region to accelerate procurement and immunization planning for high-risk populations. The recommendation significantly strengthened preventive strategies when combined with existing antimalarial drug treatments and diagnostic systems

- In April 2023, Ghana expanded its RTS,S malaria vaccine program from pilot regions into a broader national immunization rollout, becoming one of the first countries in Africa to scale up malaria vaccination. The expansion integrated vaccine delivery into routine child immunization services alongside existing malaria control measures such as insecticide-treated nets and ACT treatments. This development strengthened real-world implementation evidence for malaria vaccine integration across other MEA countries

- In July 2022, Gavi, the Vaccine Alliance approved expanded funding support for malaria vaccine rollout across multiple sub-Saharan African countries, enabling large-scale procurement of RTS,S doses and strengthening cold chain and immunization infrastructure. The funding accelerated access to malaria prevention tools in high-burden regions and complemented existing treatment-based malaria control programs. This initiative played a key role in scaling vaccine deployment across MEA healthcare systems

- In June 2021, the World Health Organization recommended the RTS,S malaria vaccine for widespread use in children at risk across Africa following successful pilot implementation in Ghana, Kenya, and Malawi. The recommendation marked the first-ever approval of a malaria vaccine for routine use, significantly strengthening preventive malaria control strategies alongside existing antimalarial treatments. This milestone laid the foundation for large-scale vaccine integration across malaria-endemic countries in the Middle East and Africa region

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.