Middle East And Africa Medical Device Testing Market

Market Size in USD Million

USD

72.42 Million

USD

139.09 Million

2025

2033

USD

72.42 Million

USD

139.09 Million

2025

2033

| 2026 - 2033 | |

| USD 72.42 Million | |

| USD 139.09 Million | |

| % | |

|

Middle East and Africa Medical Device Testing Market Overview

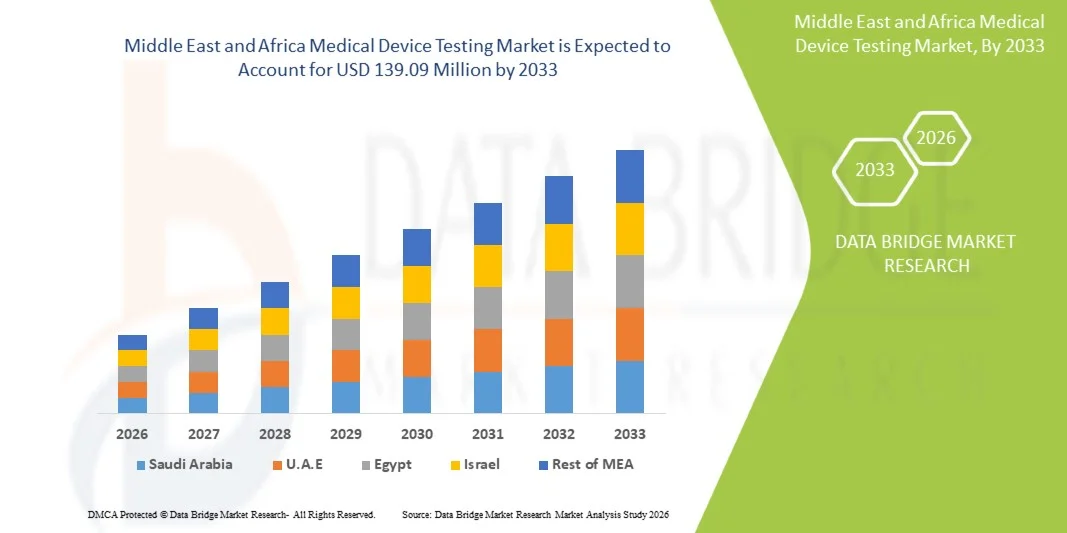

The Middle East and Africa medical device testing market was valued at USD 72.42 million in 2025 and is projected to reach USD 139.09 million by 2033, growing at a CAGR of 8.50% from 2026 to 2033. The market is witnessing steady growth driven by increasing demand for regulatory compliance, rising medical device manufacturing activities, and growing investments in healthcare infrastructure across the region.

The expansion of healthcare systems, coupled with stricter quality and safety requirements imposed by regulatory authorities, is encouraging medical device manufacturers to adopt comprehensive testing and certification services. Biocompatibility testing, sterility testing, performance validation, and electrical safety assessments are becoming essential for product approvals and market access. In addition, the growing presence of international medical device companies, increasing adoption of advanced diagnostic and therapeutic devices, and rising focus on patient safety are further supporting the demand for specialized testing services throughout the Middle East and Africa.

Key Market Trends & Insights

- Saudi Arabia dominated the Middle East and Africa medical device testing market with the largest revenue share of 28.64% in 2025, supported by expanding healthcare infrastructure, increasing regulatory requirements, and strong investments in medical technology manufacturing and imports.

- The Testing Services segment led the market with a 52.84% share in 2025, driven by the growing requirement for product safety, quality validation, and regulatory compliance before commercialization.

- The United Arab Emirates (UAE) is expected to be the fastest-growing country at a CAGR of 8.3% from 2026 to 2033, fueled by rising healthcare expenditures, growth of medical device distribution hubs, and increasing adoption of international regulatory standards.

- Certification Services are the fastest-growing service type, projected to register a CAGR of 8.1%, reflecting the surge in regulatory harmonization and demand for internationally recognized certifications

- The Chemical/Biological Testing segment dominated the testing type category with a 30.67% revenue share in 2025, led by stringent requirements for biocompatibility and material safety assessments.

- Outsourced accounted for 57.36% of the market, preferred by the availability of specialized expertise, accredited laboratories, and cost-effective testing solutions.

- The Class III segment is the fastest-growing device type category, with a CAGR of 8.3%, driven by the increasing demand for high-risk and technologically advanced medical devices

Market Size & Forecast

- Global Market Value (2025): USD 72.42 Million

- Expected Market Value (2033): USD 139.09 Million

- Forecast CAGR (2026–2033): 8.50%

- Leading Country in 2025: Saudi Arabia

- Fastest Growing Country: United Arab Emirates

Report Scope and Middle East and Africa Medical Device Testing Market Segmentation

|

Attributes |

Middle East and Africa Medical Device Testing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa |

|

Key Market Players |

· Intertek Group plc (U.K.) · SGS SA (Switzerland) · Eurofins Scientific SE (Luxembourg) · TÜV SÜD AG (Germany) · TÜV Rheinland AG (Germany) · UL LLC (U.S.) · Bureau Veritas (France) · DEKRA SE (Germany) · Element Materials Technology Group Limited (U.K.) · NAMSA (U.S.) · WuXi AppTec Co., Ltd. (China) · Labcorp (U.S.) · Charles (U.S.) · QIMA Ltd. (Hong Kong) · BSI Group (U.K.) · NELSON LABORATORIES, LLC (U.S.) · Sterigenics U.S., LLC (U.S.) · Medical Engineering Technologies Ltd (U.K.) · Pacific BioLabs, Inc. (U.S.) · AsureQuality Limited (New Zealand) |

|

Market Opportunities |

· Expansion of domestic medical device manufacturing · Growing adoption of connected medical devices, wearable health technologies, and software-enabled diagnostics · The increasing development of high-value implantable devices and minimally invasive surgical products |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Middle East and Africa Medical Device Testing Market Trends

Trend: Increasing Focus on Regulatory Compliance and Quality Assurance

Medical device manufacturers across the Middle East and Africa are increasingly investing in comprehensive testing services to ensure compliance with evolving regulatory requirements and international quality standards. The growing adoption of advanced diagnostic, monitoring, and therapeutic devices has heightened the need for biocompatibility, sterility, performance, and electrical safety testing before commercialization. Healthcare providers and regulatory agencies are emphasizing patient safety and product reliability, while accredited laboratories are expanding capabilities to support local and international manufacturers seeking market approvals across multiple jurisdictions.

For instance, in February 2025, the Saudi Food and Drug Authority continued strengthening medical device conformity assessment and post-market surveillance requirements, encouraging greater demand for accredited testing and certification services across the Kingdom.

Middle East and Africa Medical Device Testing Market Dynamics

Key Market Driver: Rising Medical Device Imports and Expanding Healthcare Infrastructure

The rapid expansion of healthcare infrastructure and increasing imports of sophisticated medical technologies have created substantial demand for medical device testing services across the Middle East and Africa. Hospitals, clinics, and diagnostic centers are adopting advanced equipment that must meet stringent safety, quality, and performance standards before deployment. Medical device manufacturers, distributors, and healthcare providers are relying on testing laboratories to support regulatory compliance, accelerate product approvals, and ensure patient safety while reducing operational and product-related risks.

For instance, in May 2024, Dubai Health Authority expanded initiatives supporting healthcare technology adoption and quality compliance, reinforcing the need for certified medical device testing and validation services in the region.

Key Restraint/Challenge: Limited Availability of Advanced Testing Infrastructure

A significant restraint in the Middle East and Africa medical device testing market is the limited availability of advanced testing infrastructure and specialized laboratory capabilities. Comprehensive testing services such as biocompatibility assessments, electromagnetic compatibility evaluations, and complex performance validation often require highly skilled personnel and sophisticated equipment. The overall cost of establishing and maintaining accredited laboratories remains substantial, while dependence on external testing facilities can increase turnaround times and regulatory approval delays for manufacturers operating across diverse regional markets.

For instance, several manufacturers in African markets continue to rely on overseas laboratories for specialized medical device validation and certification, highlighting infrastructure gaps that can slow product commercialization and increase compliance costs.

Key Market Opportunity: Growth of Local Manufacturing and International Regulatory Harmonization

The expansion of local medical device manufacturing and ongoing alignment with international regulatory frameworks presents a significant market opportunity. Governments across the region are promoting domestic healthcare production capabilities while encouraging adherence to globally recognized quality standards. Increased investments in testing laboratories, certification services, and technical expertise are supporting broader market development. The emergence of digital health technologies, connected medical devices, and innovative diagnostic platforms is further creating demand for specialized testing solutions across both established and emerging healthcare markets.

For instance, in 2024, the Gulf Health Council continued initiatives supporting regulatory cooperation and healthcare quality improvement, creating favorable conditions for expanded medical device testing and certification activities throughout the Gulf region.

Middle East and Africa Medical Device Testing Market Scope

The Middle East and Africa medical device testing market is segmented on the basis of service type, testing type, phase, sourcing type, device class, and product.

- By Service Type

On the basis of service type, the Middle East and Africa medical device testing market is segmented into testing services, inspection services, and certification services. The Testing Services segment dominated the market with an estimated share of 52.84% in 2025, owing to the growing requirement for product safety, quality validation, and regulatory compliance before commercialization. Manufacturers increasingly rely on testing laboratories to evaluate device performance, biocompatibility, sterility, and electrical safety. The expansion of healthcare infrastructure and rising imports of advanced medical devices are driving testing volumes across the region. Testing services also help manufacturers accelerate product approvals and reduce the risk of product recalls. Growing adoption of international quality standards is further supporting demand. The segment remains the cornerstone of regulatory and product development activities.

The Certification Services segment is projected to register the fastest growth at a CAGR of 8.1% from 2026 to 2033, driven by increasing regulatory harmonization and demand for internationally recognized certifications. Medical device manufacturers are seeking certifications to improve market access and strengthen customer confidence. Certification services help demonstrate compliance with global standards and regulatory requirements. Rising exports of medical devices from regional manufacturers are further boosting demand. Governments are also encouraging adherence to quality management systems and conformity assessment frameworks. Growing investments in healthcare manufacturing are expected to sustain segment growth over the forecast period.

- By Testing Type

On the basis of testing type, the market is segmented into physical testing, chemical/biological testing, cybersecurity testing, microbiology and sterility testing, and others. The Chemical/Biological Testing segment dominated the market with a share of 30.67% in 2025, driven by stringent requirements for biocompatibility and material safety assessments. Medical devices that come into contact with patients require extensive biological evaluation before approval. Increasing use of implantable devices, catheters, and surgical instruments is supporting demand for these services. Regulatory authorities place significant emphasis on toxicity and material compatibility assessments. Manufacturers are investing heavily in testing to ensure patient safety and product reliability. The segment continues to benefit from growing healthcare technology adoption throughout the region.

The Cybersecurity Testing segment is expected to witness the fastest growth at a CAGR of 8.7% from 2026 to 2033, driven by the rapid adoption of connected medical devices and digital health technologies. Hospitals are increasingly utilizing network-enabled diagnostic and monitoring systems that require protection from cyber threats. Regulatory agencies are placing greater emphasis on device security and data privacy compliance. Manufacturers are investing in cybersecurity assessments to reduce vulnerabilities and safeguard patient information. The growing use of remote monitoring and telehealth solutions is further accelerating demand. Rising awareness of healthcare cybersecurity risks is expected to strengthen long-term growth.

- By Phase

On the basis of phase, the market is segmented into preclinical and clinical. The Preclinical segment dominated the market with a 61.42% share in 2025, owing to the extensive testing requirements before devices can proceed to human use and regulatory submissions. Preclinical evaluations assess device functionality, safety, durability, and biocompatibility under controlled conditions. Manufacturers conduct these assessments to identify risks and improve product performance early in development. Increasing innovation in medical technologies is generating higher demand for preclinical validation services. The segment also benefits from growing investments in research and product development. Strong regulatory scrutiny continues to support its market leadership.

The Clinical segment is projected to register the fastest growth at a CAGR of 7.9% from 2026 to 2033, driven by increasing requirements for real-world evidence and clinical performance validation. Regulatory authorities are emphasizing clinical data to support product approvals and market access. The growing introduction of advanced therapeutic and diagnostic devices is creating demand for clinical evaluations. Expanding healthcare infrastructure and patient recruitment capabilities are supporting regional clinical testing activities. Manufacturers are increasingly investing in clinical studies to strengthen product credibility. Rising focus on patient outcomes is expected to further accelerate growth.

- By Sourcing Type

On the basis of sourcing type, the market is segmented into in-house and outsourced. The Outsourced segment led the market with a 57.36% share in 2025, driven by the availability of specialized expertise, accredited laboratories, and cost-effective testing solutions. Outsourcing enables manufacturers to access advanced testing capabilities without significant capital investment. Third-party laboratories also help accelerate regulatory approvals and reduce operational complexity. Increasing regulatory requirements are encouraging companies to partner with experienced testing providers. Small and mid-sized manufacturers particularly benefit from outsourcing arrangements. The segment continues to gain traction across both domestic and international medical device companies.

The In-House segment is expected to witness the fastest growth at a CAGR of 7.4% from 2026 to 2033, driven by growing investments in internal quality control and product development capabilities. Large manufacturers are increasingly establishing dedicated testing facilities to improve efficiency and shorten development timelines. In-house testing provides greater control over confidential product information and testing processes. Advances in laboratory technologies are making internal testing operations more feasible. Companies are also seeking to reduce long-term dependence on external providers. Increasing regional manufacturing activities are expected to support segment expansion.

- By Device Class

On the basis of device class, the market is segmented into Class I, Class II, and Class III. The Class II segment dominated the market with a 44.81% share in 2025, owing to the broad range of moderately complex medical devices requiring regulatory evaluation and testing. Products such as infusion pumps, diagnostic imaging accessories, and monitoring devices fall within this category. The segment benefits from widespread adoption across hospitals and diagnostic centers. Regulatory requirements for safety and performance testing are driving demand for validation services. Growing healthcare expenditures are increasing the use of Class II devices throughout the region. Their balance between complexity and market volume supports segment dominance.

The Class III segment is projected to register the fastest growth at a CAGR of 8.3% from 2026 to 2033, driven by increasing demand for high-risk and technologically advanced medical devices. Implantable devices, cardiovascular products, and life-supporting technologies require extensive testing and regulatory scrutiny. Manufacturers are investing heavily in validation and clinical evidence generation for these products. Rising prevalence of chronic diseases is supporting adoption of advanced treatment technologies. Regulatory agencies continue to strengthen approval requirements for high-risk devices. These factors are expected to accelerate growth during the forecast period.

- By Product

On the basis of product, the market is segmented into active implant medical device, active medical device, non-active medical device, in-vitro diagnostics medical device, ophthalmic medical device, orthopedic and dental medical device, vascular medical device, and others. The In-vitro Diagnostics (IVD) Medical Device segment dominated the market with a 29.87% share in 2025, driven by rising demand for laboratory diagnostics, disease screening, and preventive healthcare services. Increasing prevalence of infectious and chronic diseases is supporting the adoption of diagnostic technologies. Regulatory authorities require extensive testing to ensure accuracy, reliability, and performance. Expanding laboratory infrastructure across the region is further boosting demand. The segment also benefits from advancements in molecular diagnostics and point-of-care testing. Strong healthcare modernization initiatives continue to support growth.

The Active Implant Medical Device segment is expected to be the fastest-growing segment at a CAGR of 8.5% from 2026 to 2033, driven by increasing adoption of pacemakers, neurostimulators, and other implantable therapeutic technologies. These devices require extensive testing to verify safety, durability, and long-term performance. Rising incidences of cardiovascular and neurological disorders are fueling demand. Technological advancements are improving device functionality and patient outcomes. Manufacturers are investing heavily in regulatory approvals and product innovation. Growing healthcare access across the Middle East and Africa is expected to accelerate adoption and testing requirements.

Middle East and Africa Medical Device Testing Market Regional Analysis

Saudi Arabia dominated the Middle East and Africa medical device testing market with the largest revenue share of 28.64% in 2025, supported by expanding healthcare infrastructure, increasing regulatory requirements, and strong investments in medical technology manufacturing and imports. The country also benefits from rising imports of advanced medical devices, strong demand for compliance testing services, and the presence of accredited laboratories supporting product validation and certification activities. Increasing focus on patient safety, adherence to international quality standards, and expansion of local medical device manufacturing continue to drive testing requirements across multiple device categories. Ongoing healthcare transformation programs and regulatory advancements further strengthen Saudi Arabia’s leadership position in the regional market.

The Saudi Arabia Medical Device Testing Market Insight

The Saudi Arabia medical device testing market is witnessing strong growth due to rising investments in healthcare infrastructure, regulatory modernization initiatives, and increasing demand for advanced medical technologies. The country’s expanding healthcare sector, along with growing adoption of internationally recognized testing and certification standards, is driving demand across manufacturers, importers, and healthcare providers. In addition, increasing emphasis on patient safety, product quality assurance, and compliance with evolving regulatory requirements is accelerating the adoption of medical device testing services across the Kingdom.

United Arab Emirates Medical Device Testing Market Insight

The United Arab Emirates medical device testing market is experiencing steady growth, supported by rising adoption of advanced healthcare technologies, increasing medical device imports, and strong regulatory oversight. Growing investments in healthcare infrastructure and demand for efficient quality assurance solutions are contributing to market growth. Furthermore, the integration of digital health technologies, connected medical devices, and internationally aligned regulatory standards is improving testing requirements and service demand, positioning the UAE as a key healthcare innovation hub in the region.

South Africa Medical Device Testing Market Insight

The South Africa medical device testing market is expanding steadily due to the country’s well-established healthcare sector, growing diagnostic capabilities, and increasing adoption of advanced medical technologies. Medical device manufacturers, healthcare institutions, and distributors are increasingly utilizing testing services for regulatory compliance, product validation, and quality assurance activities. Continuous advancements in diagnostic technologies, increasing healthcare investments, and greater focus on patient safety and product reliability are further driving market

Qatar Medical Device Testing Market Insight

The Qatar medical device testing market is witnessing consistent growth due to rising investments in healthcare modernization, advanced diagnostic technologies, and regulatory compliance initiatives. Healthcare providers, medical device suppliers, and regulatory authorities are increasingly emphasizing quality assurance and product safety verification. Moreover, increasing adoption of digital healthcare solutions and the country’s focus on delivering high-quality healthcare services are further contributing to market growth.

Middle East and Africa Medical Device Testing Market Share

The Middle East and Africa medical device testing industry is primarily led by well-established companies, including:

- Intertek Group plc (U.K.)

- SGS SA (Switzerland)

- Eurofins Scientific SE (Luxembourg)

- TÜV SÜD AG (Germany)

- TÜV Rheinland AG (Germany)

- UL LLC (U.S.)

- Bureau Veritas (France)

- DEKRA SE (Germany)

- Element Materials Technology Group Limited (U.K.)

- NAMSA (U.S.)

- WuXi AppTec Co., Ltd. (China)

- Labcorp (U.S.)

- Charles (U.S.)

- QIMA Ltd. (Hong Kong)

- BSI Group (U.K.)

- NELSON LABORATORIES, LLC (U.S.)

- Sterigenics U.S., LLC (U.S.)

- Medical Engineering Technologies Ltd (U.K.)

- Pacific BioLabs, Inc. (U.S.)

- AsureQuality Limited (New Zealand)

Latest Developments in Middle East and Africa Medical Device Testing Market

- In August 2025, Wimpey Laboratories, part of the Cotecna Group, launched a new state-of-the-art molecular testing laboratory in Dubai, United Arab Emirates, equipped with advanced DNA and RNA analytical technologies. The facility significantly expands regional laboratory testing capabilities and supports growing demand for high-quality analytical, validation, and compliance services. The launch reinforces the UAE’s position as a key healthcare and life sciences testing hub in the Middle East and Africa

- In July 2025, the Saudi Food and Drug Authority (SFDA) announced that it had evaluated 295 medical device clinical studies and approved 157 studies that fulfilled regulatory requirements, while 84 studies remained actively underway. This development strengthens the Kingdom’s medical device regulatory ecosystem and increases demand for clinical evaluation, safety validation, and performance testing services. The initiative is expected to support faster commercialization of innovative medical technologies while maintaining high standards of patient safety and product effectiveness

- In June 2025, the Saudi Food and Drug Authority (SFDA) suspended imports from an international medical device manufacturer following inspections that identified significant quality management and manufacturing compliance deficiencies. The action highlights the growing emphasis on regulatory oversight, product quality assurance, and conformity assessment in the regional medical device industry. This move is expected to encourage manufacturers to invest further in accredited testing and validation services to meet evolving regulatory requirements

- In December 2024, PureHealth inaugurated the UAE’s largest AI-powered standalone diagnostic laboratory in Abu Dhabi through its PureLab network. The advanced facility was designed to process more than 30 million samples annually and incorporates artificial intelligence technologies to improve testing efficiency and diagnostic accuracy. This development strengthens regional laboratory infrastructure and supports the expansion of advanced testing and validation capabilities across the healthcare sector

- In May 2023, TÜV SÜD announced the accreditation of its new biology and chemistry laboratory under ISO/IEC 17025:2017, enabling the facility to provide biological, chemical, microbiological, biocompatibility, and packaging testing services for medical devices. The accreditation expands access to internationally recognized testing services for manufacturers operating across Middle Eastern and African markets. It also supports regulatory compliance, product quality improvement, and accelerated market entry for medical device companies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.