Middle East And Africa Medical Equipment Maintenance Market

Market Size in USD Billion

USD

2.34 Billion

USD

4.29 Billion

2025

2033

USD

2.34 Billion

USD

4.29 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.34 Billion | |

| USD 4.29 Billion | |

| % | |

|

Middle East and Africa Medical Equipment Maintenance Market Overview

The Middle East and Africa Medical Equipment Maintenance market was valued at USD 2.34 billion in 2025 and is projected to reach USD 4.29 billion by 2033, growing at a CAGR of 7.90% from 2026 to 2033. The market is experiencing consistent growth driven by increasing demand for efficient healthcare asset management solutions, rising adoption of advanced medical devices across hospitals and diagnostic centers, and growing emphasis on reducing equipment downtime and operational costs. Expanding healthcare infrastructure, coupled with the rapid integration of technologically advanced imaging systems, patient monitoring devices, and surgical equipment, is further supporting the growth of the medical equipment maintenance market globally.

The rising prevalence of chronic diseases, increasing patient admissions, and growing dependence on sophisticated medical technologies are compelling healthcare providers, hospitals, and diagnostic laboratories to adopt preventive and corrective maintenance services for medical equipment. Predictive maintenance solutions, remote monitoring technologies, and AI-enabled maintenance systems are increasingly replacing conventional reactive servicing models in many healthcare facilities, offering cost-effective, reliable, and efficient equipment performance management. In addition, stringent regulatory requirements regarding patient safety, device calibration, and healthcare quality standards continue to accelerate the adoption of comprehensive medical equipment maintenance solutions across developed and emerging markets.

Key Market Trends & Insights

- North America dominated the global Medical Equipment Maintenance market with the largest revenue share of 37.45% in 2025, supported by advanced healthcare infrastructure, high adoption of technologically advanced medical devices, and increasing investments in preventive healthcare equipment management solutions.

- The Preventive Maintenance segment led the market with a 42.35% share in 2025, driven by growing focus on reducing equipment downtime, improving operational efficiency, and ensuring regulatory compliance across hospitals and diagnostic centers.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.1% from 2026 to 2033, fueled by expanding healthcare infrastructure, rising healthcare expenditure, and increasing adoption of advanced medical technologies across China, India, and Japan.

- The Imaging Equipment segment dominates the device type category with a 39.84% revenue share in 2025, led by increasing utilization of MRI systems, CT scanners, ultrasound devices, and X-ray equipment across hospitals and diagnostic laboratories.

- The Hospitals segment dominates the end-user category with a 47.95% revenue share in 2025, supported by high surgical volumes, advanced infrastructure, and strong presence of specialized operating theatres and multidisciplinary care teams.

- Preventive maintenance is the leading service type, accounting for 44.80% of the market, as healthcare facilities increasingly focus on equipment uptime, reduced operational failures, and improved lifecycle management of critical surgical devices.

- The external service providers segment dominated the market with a 54.36% share in 2025, due to strong reliance on OEMs and third-party vendors for specialized maintenance services

Market Size & Forecast

- Global Medical Equipment Maintenance Market Value (2025): USD 2.34 Billion

- Expected Market Value (2033): USD 4.29 Billion

- Forecast CAGR (2026–2033): 7.90%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Middle East and Africa Medical Equipment Maintenance Market Segmentation

|

Attributes |

Medical Equipment Maintenance Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

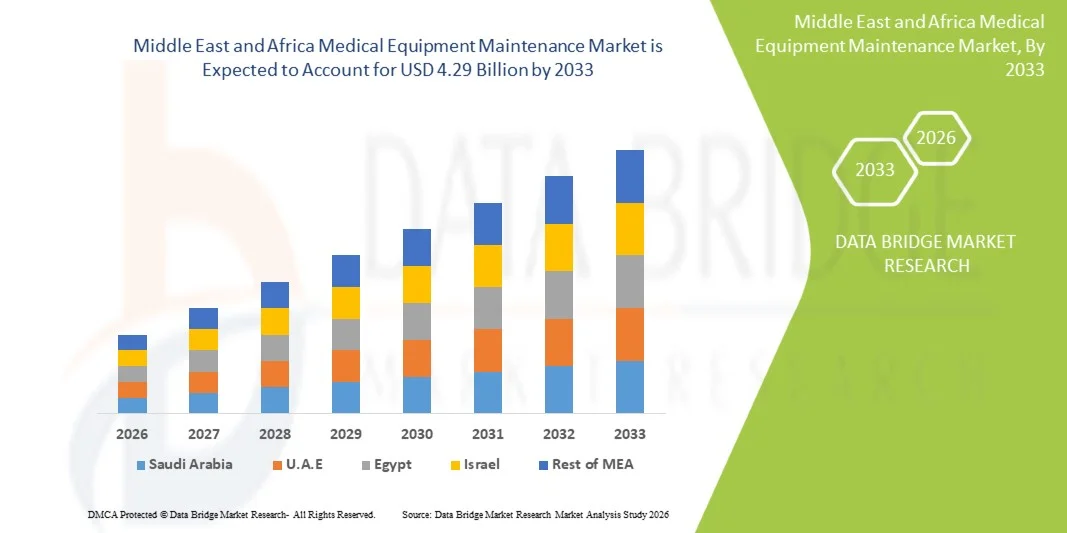

Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa |

|

Key Market Players |

· GE HealthCare Technologies Inc. (U.S.) · Siemens Healthineers AG (Germany) · Koninklijke Philips N.V. (Netherlands) · Canon Medical Systems Corporation (Japan) · Fujifilm Holdings Corporation (Japan) · Hitachi, Ltd. (Japan) · Carestream Health (U.S.) · Agfa-Gevaert Group (Belgium) · Stryker Corporation (U.S.) · Medtronic plc (Ireland) · Boston Scientific Corporation (U.S.) · Becton, Dickinson and Company (U.S.) · Drägerwerk AG & Co. KGaA (Germany) · Getinge AB (Sweden) · Althea Group (U.S.) · Crothall Healthcare Technology Solutions (U.S.) · Aramark Healthcare Technologies (U.S.) · TriMedx LLC (U.S.) · Sodexo Healthcare Technology Management (France) · UHS Biomedical Services, Inc. (U.S.) · Elekta AB (Sweden) · Smith & Nephew plc (U.K.) · Olympus Corporation (Japan) · Karl Storz SE & Co. KG (Germany) · Mindray Medical International Limited (China) · Shenzhen Anke High-tech Co., Ltd. (China) · Nihon Kohden Corporation (Japan) · Spacelabs Healthcare (U.S.) · Zimmer Biomet Holdings, Inc. (U.S.) · STERIS plc (Ireland) · TRIMEDX Foundation (U.S.) · Renovo Solutions LLC (U.S.) · BCAS Biomedical Services Ltd. (Canada) |

|

Market Opportunities |

· Expansion of Predictive Maintenance and AI-Enabled Monitoring Solutions · Growing Demand for Third-Party Maintenance Services in Emerging Markets · Increasing Adoption of Advanced Imaging and Diagnostic Equipment |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Middle East and Africa Medical Equipment Maintenance Market Trends

Trend: Growing Adoption of Predictive and AI-Enabled Medical Equipment Maintenance

Healthcare providers are increasingly adopting predictive and AI-enabled medical equipment maintenance solutions to improve operational efficiency, reduce equipment downtime, and enhance patient safety. Hospitals, diagnostic laboratories, and ambulatory care centers are leveraging IoT-enabled monitoring systems, cloud-based asset management platforms, and AI-powered predictive analytics to monitor equipment performance in real time and identify potential failures before breakdowns occur. Advanced technologies such as remote diagnostics, automated maintenance scheduling, and digital twin systems are helping healthcare facilities optimize equipment utilization and extend device lifespan. For instance, leading healthcare institutions across North America and Europe are increasingly deploying AI-driven maintenance systems for MRI scanners, CT systems, ventilators, and patient monitoring devices to minimize operational disruptions and improve clinical workflow efficiency. In addition, growing adoption of connected healthcare technologies and increasing integration of cybersecurity-enabled maintenance platforms are further strengthening demand for advanced medical equipment maintenance solutions globally.

Middle East and Africa Medical Equipment Maintenance Market Dynamics

Key Market Driver: Rising Adoption of Advanced Medical Devices Across Healthcare Facilities

The increasing adoption of technologically advanced medical devices across hospitals, clinics, and diagnostic laboratories is creating substantial demand for medical equipment maintenance services globally. Growing utilization of imaging systems, robotic surgical equipment, patient monitoring devices, laboratory automation systems, and minimally invasive surgical technologies requires regular preventive, corrective, and operational maintenance to ensure device accuracy, safety, and compliance with healthcare regulations. Healthcare providers are increasingly investing in maintenance contracts and predictive servicing models to reduce equipment downtime, optimize operational efficiency, and improve patient care outcomes. According to healthcare industry estimates, hospitals spend a significant portion of their operational budgets on equipment servicing and lifecycle management due to the growing complexity of connected medical technologies. In addition, rising healthcare expenditure, expanding healthcare infrastructure, and increasing patient volumes are accelerating the adoption of comprehensive maintenance solutions across developed and emerging markets.

Key Restraint/Challenge: High Cost Associated with Advanced Equipment Maintenance and Skilled Workforce Shortage

A significant restraint in the global medical equipment maintenance market is the high cost associated with servicing technologically advanced medical devices and the shortage of skilled biomedical technicians. Modern healthcare equipment integrates AI-enabled software systems, digital imaging platforms, robotic technologies, and complex electronic components, requiring specialized technical expertise and expensive calibration tools for maintenance and repair. The total cost of ownership extends beyond procurement to include software upgrades, preventive servicing, replacement components, and regulatory compliance requirements, creating financial pressure for smaller hospitals and healthcare facilities. For instance, maintenance and servicing costs for advanced MRI and CT imaging systems can account for a substantial share of hospital operational expenditure annually. In addition, inadequate availability of trained biomedical engineers and technical professionals in developing regions continues to limit efficient maintenance service delivery and equipment uptime management.

Key Market Opportunity: Expansion of Remote Monitoring and Third-Party Maintenance Services

The expansion of remote monitoring technologies and third-party maintenance services presents a significant market opportunity for the medical equipment maintenance industry. AI-enabled remote diagnostics platforms can provide real-time equipment performance monitoring, predictive failure alerts, and automated maintenance scheduling, helping healthcare providers reduce operational disruptions and maintenance costs. The growing demand for outsourced maintenance solutions among hospitals and diagnostic centers is further supporting the expansion of independent service organizations and third-party maintenance providers globally. In addition, the increasing adoption of refurbished medical equipment, rising investments in healthcare infrastructure across emerging markets, and growing focus on cost-efficient healthcare operations are creating new growth opportunities for maintenance service providers. Cloud-based maintenance management platforms and IoT-integrated asset tracking systems are further democratizing access to advanced equipment servicing solutions across cost-sensitive healthcare markets in Asia-Pacific, Latin America, and the Middle East & Africa.

Middle East and Africa Medical Equipment Maintenance Market Scope

The Medical Equipment Maintenance market is segmented on the basis of device type, service type, service providers, level of maintenance, and end user.

- By Device Type

On the basis of device type, the Middle East and Africa Medical Equipment Maintenance market is segmented into imaging equipment, endoscopic devices, surgical instruments, electromedical equipment, and other medical equipment. The imaging equipment segment dominated the market with a 31.42% share in 2025, owing to high deployment of MRI, CT scanners, ultrasound systems, and X-ray equipment across hospitals and diagnostic centers. Rising prevalence of chronic diseases, increasing demand for early and accurate diagnosis, and expanding healthcare infrastructure further support market growth. Growing integration of AI-enabled diagnostic imaging systems is increasing maintenance complexity and service requirements. Expanding hospital modernization programs are strengthening adoption. Increasing private healthcare investments are also supporting demand. Regulatory compliance requirements are further driving maintenance frequency. Continuous technological advancements are improving imaging precision. Rising diagnostic workloads are increasing equipment utilization rates.

The electromedical equipment segment is expected to witness the fastest growth at a CAGR of 6.9% from 2026 to 2033, driven by increasing adoption of ventilators, infusion pumps, dialysis machines, and patient monitoring systems. Expanding ICU capacity and critical care infrastructure across MEA is significantly boosting demand. Rising prevalence of chronic and lifestyle diseases is further supporting adoption. Growth in connected and IoT-enabled medical devices is increasing predictive maintenance needs. Healthcare digitalization is improving equipment lifecycle management. Expansion of emergency care facilities is accelerating usage. Increasing hospital investments in smart healthcare systems is strengthening demand. Continuous technological upgrades are increasing servicing requirements. Growing emphasis on patient safety is further driving maintenance services.

- By Service Type

On the basis of service type, the market is segmented into performance/operational, preventive, and corrective maintenance. The preventive maintenance segment dominated the market with a 46.18% share in 2025, owing to increasing focus on equipment uptime, patient safety, and regulatory compliance. Hospitals and diagnostic centers are widely adopting scheduled maintenance programs to reduce unexpected breakdowns. Increasing deployment of high-value medical equipment is strengthening preventive servicing demand. Rising healthcare operational costs are encouraging planned maintenance strategies. Regulatory frameworks across MEA are enforcing strict equipment safety standards. Growing hospital infrastructure expansion is further supporting adoption. Increasing digitization in healthcare is improving maintenance tracking systems. Adoption of predictive maintenance tools is enhancing operational efficiency.

The corrective maintenance segment is expected to witness the fastest growth at a CAGR of 6.7% from 2026 to 2033, driven by increasing complexity of advanced medical equipment and rising failure incidents. Growing use of imaging, surgical, and monitoring devices is increasing repair demand. Expansion of emergency healthcare services is boosting urgent maintenance needs. Increasing outsourcing of technical repair services is improving response time. Integration of AI-based fault detection systems is enhancing repair efficiency. Rising equipment utilization rates are increasing breakdown frequency. Growth in rural healthcare infrastructure is adding service demand. Aging medical equipment base is further contributing to corrective maintenance needs. Hospitals are increasingly adopting hybrid service contracts.

- By Service Providers

On the basis of service providers, the market is segmented into external service providers and in-house service providers. The external service providers segment dominated the market with a 54.36% share in 2025, due to strong reliance on OEMs and third-party vendors for specialized maintenance services. Hospitals prefer outsourcing to reduce operational burden and ensure technical accuracy. Increasing complexity of medical devices is further supporting outsourcing trends. Expanding healthcare infrastructure is strengthening vendor networks. Rising demand for cost-efficient service models is reinforcing dominance. Regulatory compliance requirements are encouraging certified external servicing. Growth in multi-vendor hospital systems is increasing outsourcing dependency. Availability of skilled external engineers is supporting market leadership.

The in-house service providers segment is expected to witness the fastest growth at a CAGR of 6.4% from 2026 to 2033, driven by increasing investment in internal biomedical engineering teams. Large hospital chains are developing in-house maintenance capabilities to reduce dependency on external vendors. Demand for faster service response is supporting adoption. Expansion of multi-specialty hospitals is strengthening internal teams. Increasing technician training programs are improving service efficiency. Adoption of digital maintenance platforms is enhancing workflow management. Hybrid maintenance models are gaining traction. Rising healthcare investment in Gulf countries is supporting internal capability building. Equipment complexity is further driving in-house expertise demand.

- By Level of Maintenance

On the basis of level of maintenance, the market is segmented into Level 1 user, Level 2 technician, and Level 3 specialized maintenance. The Level 2 technician segment dominated the market with a 41.73% share in 2025, due to its role in routine maintenance, calibration, and troubleshooting. Hospitals rely heavily on trained technicians for operational continuity. Increasing medical equipment installations are strengthening demand. Growth in diagnostic centers is further supporting segment dominance. Rising need for operational efficiency is boosting technician-level servicing. Expanding healthcare infrastructure is increasing maintenance workloads. Adoption of digital service tools is improving technician productivity. Training programs for biomedical staff are further strengthening capabilities.

The Level 3 specialized maintenance segment is expected to witness the fastest growth at a CAGR of 7.1% from 2026 to 2033, driven by increasing complexity of advanced medical systems. Demand for OEM-level expertise is rising in critical care environments. Expansion of robotic surgery and AI-enabled medical devices is increasing servicing requirements. Growth in tertiary healthcare centers is supporting adoption. Rising regulatory compliance standards are increasing need for certified experts. Increasing connected medical devices are adding technical complexity. Hospitals are investing in specialized service partnerships. Predictive maintenance systems are driving demand for advanced engineers. Continuous innovation in medical technology is further accelerating growth.

- By End User

On the basis of end user, the market is segmented into hospitals, clinics, laboratories, and other healthcare centers. The hospitals segment dominated the market with a 48.91% share in 2025, owing to high patient inflow and extensive use of advanced medical equipment. Rising hospital expansion and ICU growth are further supporting dominance. Increasing demand for continuous equipment uptime is strengthening maintenance services. Growth in multi-specialty hospitals is boosting adoption. Rising healthcare investments are improving infrastructure. Integration of digital healthcare systems is increasing equipment dependency. Regulatory compliance requirements are reinforcing servicing needs. Increasing medical device installations are further supporting market growth.

The laboratories segment is expected to witness the fastest growth at a CAGR of 6.8% from 2026 to 2033, driven by rising diagnostic testing volumes and expansion of laboratory infrastructure. Increasing adoption of automated diagnostic systems is boosting maintenance requirements. Growth in chronic disease prevalence is increasing test demand. Expansion of private diagnostic chains is strengthening adoption. Integration of AI-based lab systems is increasing equipment complexity. Rising healthcare outsourcing is supporting service demand. Government investments in diagnostic facilities are improving access. Demand for precision testing is increasing calibration needs. Digital pathology adoption is further accelerating growth.

Middle East and Africa Medical Equipment Maintenance Market Regional Analysis

North America dominated the Medical Equipment Maintenance market and accounted for the largest revenue share of 37.45% in 2025, supported by advanced healthcare infrastructure, high adoption of technologically advanced medical devices, and strong integration of preventive healthcare equipment management systems. The region benefits from widespread deployment of MRI, CT, ventilators, and surgical systems that require continuous servicing, calibration, and performance monitoring. In addition, strong presence of OEM service providers, well-established hospital networks, and strict regulatory compliance standards are driving demand for structured maintenance programs. Increasing investments in predictive maintenance technologies, IoT-enabled medical devices, and AI-based diagnostic equipment monitoring is further strengthening the region’s leadership position in the global Medical Equipment Maintenance market.

U.S. Medical Equipment Maintenance Market Insight

The U.S. Medical Equipment Maintenance market is witnessing strong growth due to rising healthcare expenditure, increasing adoption of advanced medical imaging and diagnostic systems, and growing focus on patient safety and equipment uptime. Hospitals and diagnostic centers are heavily investing in preventive and predictive maintenance solutions to reduce equipment failure rates and operational downtime. The country’s mature healthcare ecosystem, along with widespread use of electromedical devices such as patient monitors, infusion pumps, and ventilators, is driving consistent service demand. In addition, increasing integration of AI-powered diagnostics, remote monitoring systems, and digital hospital infrastructure is accelerating the shift toward intelligent maintenance solutions across healthcare facilities.

Europe Medical Equipment Maintenance Market Insight

The Europe Medical Equipment Maintenance market is steadily expanding, supported by strong public healthcare systems, high adoption of advanced diagnostic equipment, and strict regulatory requirements for medical device safety and performance. The region has a strong presence of hospitals and research institutions that rely heavily on imaging systems, surgical equipment, and laboratory instruments requiring continuous maintenance. Increasing focus on preventive healthcare, combined with rising adoption of digital hospital management systems and predictive maintenance technologies, is strengthening service demand. Furthermore, aging healthcare infrastructure in several European countries is driving replacement, servicing, and lifecycle management of medical equipment.

U.K. Medical Equipment Maintenance Market Insight

The U.K. Medical Equipment Maintenance market is growing steadily due to strong National Health Service (NHS) infrastructure, increasing deployment of advanced diagnostic systems, and rising focus on healthcare quality assurance. Hospitals are increasingly adopting structured maintenance contracts to ensure uptime of imaging systems, ventilators, and surgical devices. In addition, growing integration of digital health technologies, remote diagnostics, and AI-based equipment monitoring is improving maintenance efficiency. The U.K.’s strong regulatory framework and emphasis on patient safety are further supporting demand for standardized preventive maintenance services across healthcare facilities.

Germany Medical Equipment Maintenance Market Insight

The Germany Medical Equipment Maintenance market is expanding steadily, driven by strong hospital infrastructure, advanced biomedical engineering capabilities, and high adoption of precision medical technologies. German healthcare institutions are increasingly relying on preventive and predictive maintenance systems to ensure optimal performance of high-value equipment such as MRI scanners, CT systems, and robotic surgical devices. The country’s strong focus on healthcare innovation, combined with rising digitalization of hospitals and integration of IoT-based monitoring systems, is improving equipment reliability and reducing downtime. In addition, a strong presence of OEM service providers is reinforcing structured maintenance adoption across the healthcare sector.

Asia-Pacific Medical Equipment Maintenance Market Insight

The Asia-Pacific Medical Equipment Maintenance market is expected to witness rapid growth, driven by expanding healthcare infrastructure, rising healthcare expenditure, and increasing adoption of advanced medical technologies across China, India, and Japan. Growing demand for diagnostic imaging, surgical procedures, and critical care services is significantly increasing the installed base of medical equipment requiring maintenance. In addition, government initiatives to improve healthcare access, along with rising private hospital investments and medical tourism, are strengthening market expansion. The region is also witnessing increasing adoption of predictive maintenance, digital healthcare systems, and OEM service partnerships.

Japan Medical Equipment Maintenance Market Insight

The Japan Medical Equipment Maintenance market is experiencing steady growth due to advanced healthcare infrastructure, high adoption of precision medical devices, and strong focus on patient safety and operational efficiency. Hospitals and diagnostic centers are increasingly investing in preventive maintenance systems for imaging equipment, surgical robots, and critical care devices. Japan’s aging population is also driving higher demand for healthcare services, increasing equipment utilization rates and maintenance requirements. In addition, integration of AI-based monitoring systems and robotic-assisted healthcare technologies is improving maintenance accuracy and reducing equipment downtime.

China Medical Equipment Maintenance Market Insight

The China Medical Equipment Maintenance market is growing rapidly, driven by expanding hospital infrastructure, rising healthcare expenditure, and increasing adoption of advanced diagnostic and therapeutic equipment. Government-led healthcare reforms and investments in modern hospital systems are significantly increasing the deployment of MRI, CT, and ICU equipment requiring regular servicing. In addition, growing adoption of digital healthcare platforms, AI-powered maintenance systems, and IoT-enabled medical devices is improving operational efficiency. China’s rapidly expanding private healthcare sector and increasing demand for high-quality medical services are further accelerating maintenance market growth.

Middle East and Africa Medical Equipment Maintenance Market Share

The Medical Equipment Maintenance industry is primarily led by well-established companies, including:

- GE HealthCare Technologies Inc. (U.S.)

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V. (Netherlands)

- Canon Medical Systems Corporation (Japan)

- Fujifilm Holdings Corporation (Japan)

- Hitachi, Ltd. (Japan)

- Carestream Health (U.S.)

- Agfa-Gevaert Group (Belgium)

- Stryker Corporation (U.S.)

- Medtronic plc (Ireland)

- Boston Scientific Corporation (U.S.)

- Becton, Dickinson and Company (U.S.)

- Drägerwerk AG & Co. KGaA (Germany)

- Getinge AB (Sweden)

- Althea Group (U.S.)

- Crothall Healthcare Technology Solutions (U.S.)

- Aramark Healthcare Technologies (U.S.)

- TriMedx LLC (U.S.)

- Sodexo Healthcare Technology Management (France)

- UHS Biomedical Services, Inc. (U.S.)

- Elekta AB (Sweden)

- Smith & Nephew plc (U.K.)

- Olympus Corporation (Japan)

- Karl Storz SE & Co. KG (Germany)

- Mindray Medical International Limited (China)

- Shenzhen Anke High-tech Co., Ltd. (China)

- Nihon Kohden Corporation (Japan)

- Spacelabs Healthcare (U.S.)

- Zimmer Biomet Holdings, Inc. (U.S.)

- STERIS plc (Ireland)

- TRIMEDX Foundation (U.S.)

- Renovo Solutions LLC (U.S.)

- BCAS Biomedical Services Ltd. (Canada)

Latest Developments in Middle East and Africa Medical Equipment Maintenance Market

- In January 2021, Siemens Healthineers, a global leader in medical imaging and healthcare technology solutions, expanded its “Teamplay Fleet” digital service platform to strengthen predictive maintenance capabilities across hospitals. The upgrade enabled real-time monitoring of imaging equipment such as MRI and CT scanners, helping healthcare providers reduce downtime and improve service efficiency. This development reflects the growing shift toward AI-enabled predictive maintenance in medical devices

- In June 2021, GE Healthcare enhanced its “Asset Performance Management (APM)” solution for hospitals, integrating advanced analytics and remote diagnostics for critical imaging and patient monitoring systems. The initiative focused on improving preventive maintenance scheduling and reducing unplanned equipment failures, supporting the global trend toward data-driven healthcare equipment servicing

- In March 2022, Philips Healthcare expanded its “Managed Equipment Services (MES)” contracts across Europe and Asia-Pacific, offering end-to-end maintenance and lifecycle management for diagnostic imaging and surgical systems. The expansion strengthened long-term service agreements with hospitals, ensuring uptime guarantees and cost optimization for healthcare providers

- In October 2022, Siemens Healthineers announced the expansion of its digital service portfolio with enhanced remote servicing and AI-powered diagnostics for imaging equipment. The solution allowed technicians to resolve a large share of service issues remotely, reducing on-site intervention time and improving hospital operational continuity

- In May 2023, GE Healthcare introduced upgraded digital maintenance capabilities within its Edison platform, integrating AI-driven predictive maintenance for MRI and CT systems. The update enabled early fault detection and automated service alerts, significantly improving equipment reliability and reducing downtime across hospital networks

- In September 2023, Philips Healthcare launched expanded remote service operations in emerging markets, strengthening its ability to deliver preventive maintenance for diagnostic imaging systems in regions with limited biomedical engineering capacity. The initiative supported improved healthcare accessibility and equipment uptime in developing countrie

- In February 2024, Siemens Healthineers expanded its “Smart Service” ecosystem, incorporating cloud-based monitoring and advanced predictive analytics for hospital equipment fleets. The system enhanced lifecycle management of diagnostic and laboratory devices, enabling hospitals to shift toward proactive maintenance strategies

- In July 2024, GE Healthcare announced strategic enhancements to its service contracts for imaging equipment, focusing on AI-based predictive maintenance and integrated remote diagnostics. The update aimed to reduce equipment downtime in high-volume hospitals and improve service response efficiency across global healthcare network

- In March 2025, Philips Healthcare further expanded its AI-enabled service and maintenance ecosystem by strengthening integration of IoT-based monitoring for hospital imaging and patient care equipment. This development improved real-time equipment tracking, predictive servicing, and operational efficiency across healthcare facilities

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.