Middle East And Africa Medical Robots Market

Market Size in USD Million

USD

748.88 Million

USD

2,062.42 Million

2025

2033

USD

748.88 Million

USD

2,062.42 Million

2025

2033

| 2026 - 2033 | |

| USD 748.88 Million | |

| USD 2,062.42 Million | |

| % | |

|

Middle East and Africa Medical Robots Market Overview

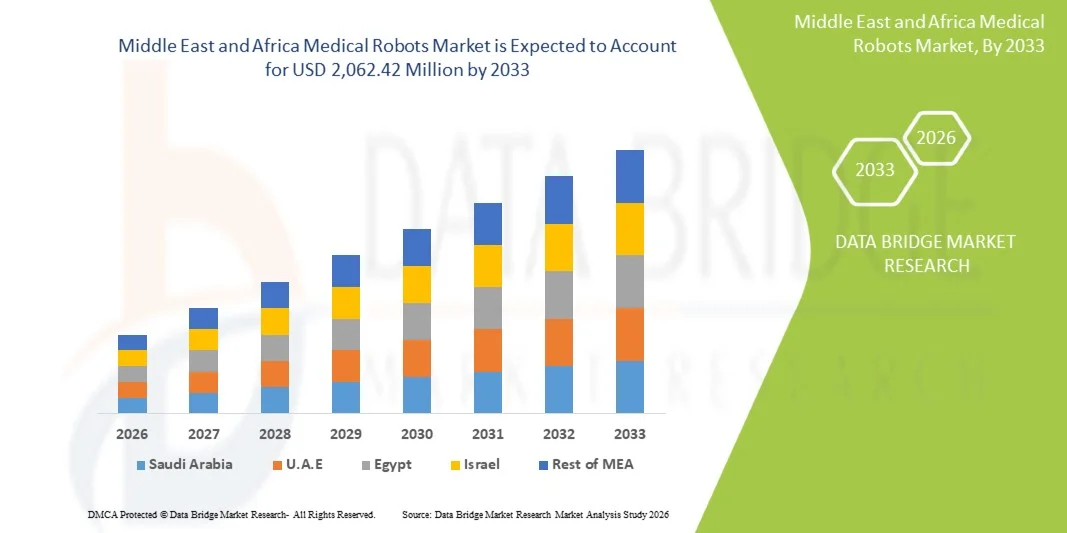

The Middle East and Africa medical robots market was valued at USD 748.88 million in 2025 and is projected to reach USD 2,062.42 million by 2033, growing at a CAGR of 13.50% from 2026 to 2033. The market is witnessing robust growth driven by increasing government investments in advanced healthcare infrastructure, rising adoption of minimally invasive surgical procedures, and accelerating deployment of AI-powered robotic systems across hospitals and specialty care centers in the region. The growing focus on healthcare modernization under national visions — such as Saudi Vision 2030 and UAE Vision 2031 — coupled with expanding medical tourism and a rising burden of chronic diseases, is further propelling demand for medical robotic solutions across the MEA region.

The high prevalence of cardiovascular diseases, cancer, and orthopedic conditions — alongside rising geriatric populations — is driving healthcare providers to invest heavily in robotic-assisted surgical systems and rehabilitation robots. Innovations in telesurgery, AI-integrated robotic platforms, and compact modular robotic systems are improving surgical precision and patient outcomes, supporting widespread institutional adoption across hospitals, ambulatory surgical centers, and rehabilitation facilities throughout the Middle East and Africa.

Key Market Trends & Insights

- The Middle East and Africa region accounted for 5.0% of the global medical robots market revenue in 2025, with increasing government-backed investments in smart hospitals and advanced surgical robotics driving accelerated adoption across Saudi Arabia, UAE, and South Africa.

- The Surgical Robots segment led the product market with a 48.2% share in 2025, driven by increasing adoption of robotic-assisted laparoscopy, urology, and orthopedic surgeries across flagship hospitals and medical cities in the region.

- Sanitation and Disinfectant Robots are the fastest-growing product sub-segment, projected to register a CAGR of 17.8% over the forecast period, driven by heightened infection control protocols and hospital hygiene demands post-pandemic across MEA healthcare facilities.

- The Hospitals segment dominated the end-user category with a revenue share of 62.4% in 2025, benefiting from high patient volumes, established institutional infrastructure, and increasing government mandates for robotic surgical adoption.

- Direct Tender dominated the distribution channel segment in 2025 with a 54.6% share, as healthcare ministries and government hospital networks in the region procure medical robotic systems through centralized procurement frameworks.

- Saudi Arabia remains the leading country-level market, benefiting from Vision 2030 healthcare modernization, increased robotic cardiac surgery milestones, and growing adoption of da Vinci systems in major specialist hospitals.

Market Size & Forecast

- Middle East and Africa Market Value (2025): USD 748.88 Million

- Expected Market Value (2033): USD 2,062.42 Million

- Forecast CAGR (2026–2033): 13.50%

Report Scope and Middle East and Africa Medical Robots Market Segmentation

|

Attributes |

Medical RobotsKey Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa |

|

Key Market Players |

· Intuitive Surgical, Inc. (U.S.) · Stryker Corporation (U.S.) · Medtronic plc (Ireland) · CMR Surgical Ltd. (U.K.) · Johnson & Johnson MedTech (U.S.) · Zimmer Biomet Holdings, Inc. (U.S.) · Smith + Nephew (U.K.) · Accuray Incorporated (U.S.) · Hocoma AG (Switzerland) · ReWalk Robotics Ltd. (Israel) · Stereotaxis, Inc. (U.S.) · Kuka AG (Germany) · Capsa Healthcare (U.S.) · PARO Robots U.S., Inc. (U.S.) · Corindus, A Siemens Healthineers Company (U.S.) |

|

Market Opportunities |

· Expansion of robotic surgery programs under national healthcare modernization initiatives · Increasing adoption of AI-powered robotic platforms for minimally invasive surgeries and rehabilitation across MEA hospitals |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Middle East and Africa Medical Robots Market Trends

Trend: Rising Adoption of AI-Driven Robotic Surgical Systems and Smart Hospital Infrastructure

The growing integration of artificial intelligence and next-generation robotic surgical platforms is emerging as a defining trend in the Middle East and Africa medical robots market. Healthcare ministries, hospital networks, and private medical operators across the region are increasingly deploying AI-powered surgical robots, autonomous hospital logistics systems, and robotic rehabilitation platforms — driven by national healthcare transformation agendas and rising demand for precision medicine. The deployment of advanced robotic systems is enabling healthcare institutions in the MEA region to improve surgical accuracy, reduce complication rates, and accelerate patient recovery timelines across oncology, orthopedics, urology, and cardiac surgery applications.

For instance, in July 2024, Saudi Arabia’s King Faisal Specialist Hospital and Research Centre (KFSH and RC) announced a landmark milestone — achieving a 98% survival rate across 400 robotic cardiac surgeries since the program’s inception in February 2019 — firmly establishing the institution as a global leader in robotic cardiac care and reinforcing Saudi Arabia’s commitment to advanced surgical robotics adoption. Furthermore, AI-driven robotic platforms integrating real-time imaging, machine learning, and haptic feedback are enhancing the predictability of complex surgical interventions, reducing procedural errors, and shortening operating room times across MEA hospital networks. These technological advancements — spanning AI-based surgical planning, autonomous disinfection robots, and telesurgery platforms — are collectively accelerating the adoption of medical robots throughout the Middle East and Africa.

Middle East and Africa Medical Robots Market Dynamics

Key Market Driver: Rising Healthcare Infrastructure Investments and Government Modernization Programs

The rapid expansion of healthcare infrastructure under government-led modernization programs is significantly driving demand for medical robotic systems across the Middle East and Africa. Healthcare authorities, hospital administrators, and national health ministries across the region are investing heavily in robotic-assisted surgical technologies, hospital automation platforms, and rehabilitation robotic systems to elevate care standards, reduce dependence on clinical staff, and improve patient outcomes. Increasing adoption of compact robotic systems, AI-integrated surgery platforms, and modular robotic architectures is accelerating demand for advanced medical robots across hospitals, specialty clinics, and ambulatory surgical centers throughout the MEA region.

For instance, in February 2026, Johnson & Johnson MedTech submitted a De Novo application for the OTTAVA robotic system incorporating machine-learning collision prediction, marking a significant milestone in next-generation robotic surgery system development. In January 2026, Intuitive Surgical obtained FDA clearance for cardiac surgery applications on the da Vinci 5 platform, including mitral valve repair and coronary artery bypass grafting, expanding the platform’s clinical reach in MEA centers performing advanced cardiac procedures.

Key Restraint/Challenge: High Capital Investment Requirements and Limited Skilled Robotics Workforce

A major challenge in the Middle East and Africa medical robots market is the substantial capital investment required for the acquisition, installation, maintenance, and training associated with advanced medical robotic systems. Premium surgical robots, rehabilitation platforms, and hospital automation solutions involve significant upfront procurement costs alongside recurring service contracts, consumable expenditures, and surgeon training programs. In addition, limited availability of robotics-trained surgical professionals, inconsistent healthcare reimbursement frameworks, and complex regulatory approval pathways in several MEA countries create barriers to widespread adoption across cost-sensitive healthcare markets in the region.

For instance, the average capital cost of a da Vinci surgical system ranges between USD 1.5 million and USD 2.5 million, with annual maintenance costs of approximately USD 150,000–USD 200,000, creating significant financial barriers for mid-tier hospitals and public healthcare facilities across emerging MEA markets including sub-Saharan Africa and North Africa.

Key Market Opportunity: Expansion of Medical Tourism and Telesurgery Platforms Across MEA

The increasing positioning of countries such as the UAE and Saudi Arabia as global medical tourism destinations — combined with growing investments in telesurgery infrastructure and remote robotic procedure capabilities — presents significant opportunities for the Middle East and Africa medical robots market. Expanding adoption of portable robotic systems, AI-enhanced teleconsultation platforms, and modular robotic architectures is enabling healthcare providers to improve surgical access, expand clinical service offerings, and serve both domestic and international patient populations across the region.

For instance, in March 2023, the first-ever Global Robotic MedTech Forum was held in Dubai, hosted by the US Society of Robotic Surgery and Crescent Healthcare, bringing together international surgical robotics experts to explore latest advancements and accelerate robotics adoption across MEA healthcare systems — signaling the region’s growing strategic commitment to medical robotics integration.

Middle East and Africa Medical Robots Market Scope

The Middle East and Africa medical robots market is segmented on the basis of type, product, modality, components, application, end user, and distribution channel.

- By Type

On the basis of type, the Middle East and Africa medical robots market is segmented into external large robots, geriatric robots, assistive robots, and miniature in vivo robots. The External Large Robots segment held the largest market share of 42.3% in 2025, owing to their widespread deployment in high-volume surgical procedures including laparoscopy, orthopedics, urology, and cardiac surgery across major tertiary hospitals in Saudi Arabia, UAE, and South Africa. The segment is underpinned by the growing installed base of da Vinci surgical systems, Mako robotic platforms, and CMR Surgical’s Versius systems across leading MEA healthcare institutions.

The Miniature in Vivo Robots segment is expected to witness the fastest CAGR of 18.2% over the forecast period, driven by advances in capsule endoscopy, targeted drug delivery robotics, and microrobotics research programs at MEA academic medical centers and research institutes. Growing investments in nanotechnology-integrated medical robotics and AI-guided in vivo navigation are further accelerating segment growth.

- By Product

On the basis of product, the Middle East and Africa medical robots market is segmented into surgical robots, rehabilitation robots, hospital and pharmacy robots, bio robotics, non-invasive radio surgery robots, telepresence robots, medical transportation robots, and sanitation and disinfectant robots. The Surgical Robots segment dominated the product market with a 48.2% share in 2025, driven by increasing adoption of robotic-assisted minimally invasive procedures — including urological surgery, cardiac surgery, and orthopedic arthroplasty — across leading hospitals in Saudi Arabia, UAE, and South Africa. The growing installed base of Intuitive Surgical’s da Vinci systems, Stryker’s Mako platform, and CMR Surgical’s Versius robots across MEA medical centers continues to reinforce segment dominance.

The Sanitation and Disinfectant Robots segment is expected to witness the fastest CAGR of 17.8% over the forecast period, driven by heightened focus on hospital infection control following the COVID-19 pandemic, rising adoption of UV-C disinfection robots in MEA hospitals, and growing government mandates for infection prevention protocols across healthcare facilities in the region.

- By Modality

On the basis of modality, the Middle East and Africa medical robots market is segmented into compact and portable robots. The Compact modality segment held the largest market share of 63.7% in 2025, as the majority of high-value surgical robot deployments across MEA flagship hospitals and medical cities utilize fixed, room-integrated robotic platforms. These systems offer superior precision, stability, and integration with advanced surgical workflows, making them highly suitable for complex procedures. Increasing investments in tertiary care infrastructure, growing demand for minimally invasive surgeries, and the presence of specialized surgical centers continue to support the segment’s dominant position across the region.

The Portable segment is expected to witness the fastest CAGR of 15.6%, driven by growing adoption of modular, transportable robotic systems—such as CMR Surgical’s Versius—which can be moved between operating rooms and hospital departments, improving operational efficiency and capital utilization across healthcare facilities. Rising demand for flexible robotic solutions, expanding access to robotic-assisted surgery in mid-sized hospitals, and ongoing technological advancements are further contributing to strong segment growth.

- By Components

On the basis of components, the Middle East and Africa medical robots market is segmented into actuators, sensors, robot controller, patient cart, surgeon console, vision cart, dispensing system, and additional products. The Surgeon Console segment held the largest component market share of 24.6% in 2025, as it represents the primary physician-robot interaction interface across all major surgical robotic platforms deployed in MEA hospitals. Rising investments in ergonomic console design, haptic feedback integration, and AI-assisted motion scaling are driving component upgrades and replacement cycles across the installed base.

The Sensors segment is expected to witness significant growth, driven by increasing integration of force sensing, intraoperative imaging, and real-time collision avoidance capabilities into next-generation medical robot architectures. These advanced sensor technologies enhance surgical precision, improve patient safety, enable better visualization during procedures, and support more accurate robotic movements. Growing demand for intelligent, data-driven surgical systems and continuous technological advancements are further accelerating adoption across healthcare facilities.

- By Application

On the basis of application, the Middle East and Africa medical robots market is segmented into research, clinic, pharmacy, and others. The Clinic application segment accounted for the highest market share of 58.4% in 2025, driven by the primary deployment of surgical, rehabilitation, and telepresence robots within hospital surgical suites and specialty care facilities. Rapid expansion of smart hospital infrastructure across Saudi Arabia and UAE, alongside growing patient volumes requiring robotic-assisted surgical intervention, continues to reinforce clinical application dominance.

The Pharmacy segment is expected to witness the fastest growth, fueled by increasing hospital pharmacy automation investments, adoption of robotic dispensing systems, and growing demand for error reduction and efficiency improvements in medication management across MEA. Rising prescription volumes, workforce optimization needs, and advancements in automated inventory management technologies are further supporting segment expansion. Additionally, healthcare providers are increasingly adopting pharmacy robotics to enhance accuracy, reduce operational costs, and improve patient safety.

- By End User

On the basis of end user, the Middle East and Africa medical robots market is segmented into hospitals, specialty clinics, research institutes, ambulatory surgical centers, laboratories, rehabilitation centers, and others. The Hospitals segment held the dominant end-user share of 62.4% in 2025, leveraging established infrastructure, high patient volumes, and dedicated surgical robotics programs to maximize clinical utilization across multiple specialties. The strong presence of government-mandated smart hospital programs in Saudi Arabia and UAE, including King Faisal Specialist Hospital’s robotic cardiac surgery program and Johns Hopkins Aramco Healthcare’s robotic-assisted gynecological procedures, continues to reinforce hospital segment leadership.

The Ambulatory Surgical Centers segment is expected to grow at a CAGR of 16.4%, driven by increasing adoption of compact, portable robotic surgery platforms — such as CMR Surgical’s Versius — specifically designed for multi-room use in ASCs, reducing cost-per-procedure and expanding robotic access beyond major academic hospital centers across the MEA region.

- By Distribution Channel

On the basis of distribution channel, the Middle East and Africa medical robots market is segmented into direct tender, retail sales, third-party distributors, and others. The Direct Tender channel dominated the distribution landscape with a 54.6% revenue share in 2025, driven by centralized government procurement of medical robotic systems through national health ministry tender processes across Saudi Arabia, UAE, Egypt, and South Africa. The structured tender frameworks enable large-scale, multi-unit acquisitions of surgical robots and hospital automation systems, reinforcing direct tender channel dominance in the MEA market.

The Third Party Distributors segment is anticipated to witness the fastest CAGR of 15.9% during the forecast period, driven by expanding regional medical device distribution networks, growing partnerships between global robotic OEMs and MEA-based distributors, and increasing penetration of robotic systems into private hospital groups and specialty clinics across the region.

Middle East and Africa Medical Robots Market Regional Analysis

The Middle East and Africa medical robots market is characterized by significant country-level heterogeneity, with market maturity ranging from well-established robotic surgery programs in Saudi Arabia and UAE to emerging adoption ecosystems in sub-Saharan Africa and North Africa. Saudi Arabia and the UAE collectively represent the dominant revenue contributors, supported by high healthcare expenditure, ambitious national health modernization programs, and the presence of internationally accredited hospital networks with established robotic surgery capabilities. The broader MEA region is witnessing growing adoption momentum driven by medical tourism expansion, increasing private sector healthcare investment, and rising patient demand for minimally invasive surgical options.

Saudi Arabia Medical Robots Market Insight

Saudi Arabia is the leading country-level medical robots market in the MEA region, supported by Vision 2030 healthcare transformation initiatives, strong government investment in advanced medical technologies, and the presence of world-class hospitals pioneering robotic surgical programs. The country is anticipated to grow at a robust CAGR over the forecast period, driven by the rapid expansion of robotic-assisted procedures in cardiac, urological, and oncological surgery across institutions including King Faisal Specialist Hospital and Research Centre, Johns Hopkins Aramco Healthcare, and the National Guard Health Affairs network. Saudi Arabia is among the world leaders in robotic cardiac surgery, having achieved a 98% survival rate across 400 robotic cardiac procedures as of July 2024, further reinforcing institutional commitment to next-generation robotic surgical adoption.

UAE Medical Robots Market Insight

The UAE medical robots market is the second-largest in the MEA region, positioned at the intersection of advanced healthcare infrastructure, rapidly expanding medical tourism, and strong government support for digital health and robotics innovation. The UAE hosts approximately three active da Vinci surgical systems and is actively expanding robotic capabilities across Dubai Health Authority and Abu Dhabi Health Services hospitals. The country’s strategic positioning as a global medical tourism hub — attracting patients from across the Middle East, South Asia, and Africa — creates significant incremental demand for premium robotic surgical procedures. The first-ever Global Robotic MedTech Forum, held in Dubai in March 2023, demonstrated the UAE’s growing role as a regional center for medical robotics advancement and knowledge exchange.

Middle East and Africa Medical Robots Market Share

The Middle East and Africa Medical Robots industry is primarily led by well-established global companies, including:

- Intuitive Surgical, Inc. (U.S.)

- Stryker Corporation (U.S.)

- Medtronic plc (Ireland)

- CMR Surgical Ltd. (U.K.)

- Johnson & Johnson MedTech (U.S.)

- Zimmer Biomet Holdings, Inc. (U.S.)

- Smith + Nephew (U.K.)

- Accuray Incorporated (U.S.)

- Hocoma AG (Switzerland)

- ReWalk Robotics Ltd. (Israel)

- Stereotaxis, Inc. (U.S.)

- Kuka AG (Germany)

- Capsa Healthcare (U.S.)

- PARO Robots U.S., Inc. (U.S.)

- Corindus, A Siemens Healthineers Company (U.S.)

Latest Developments in Middle East and Africa Medical Robots Market

- In February 2026, Medtronic secured FDA clearance for the Stealth AXiS spine robot, integrating advanced imaging and navigation to guide pedicle-screw placement within sub-millimeter tolerances — marking a major step in robotic spinal surgery precision. The system’s real-time intraoperative navigation integration is expected to accelerate adoption across leading MEA spine surgery centers in Saudi Arabia and UAE.

- In February 2026, CMR Surgical secured FDA clearance for its Versius Plus platform, featuring advanced visualization and enhanced arm articulation capabilities. Cleared in over 80 countries, the modular Versius architecture is specifically positioned to expand robotic surgery access in MEA ambulatory surgical centers and multi-department hospital environments where portability and flexibility are critical procurement considerations.

- In January 2026, Intuitive Surgical obtained FDA clearance for cardiac surgery applications on its da Vinci 5 platform — including mitral valve repair and coronary artery bypass grafting — expanding the system’s clinical reach into advanced cardiac procedures. Given Saudi Arabia’s established robotic cardiac surgery programs, this regulatory milestone is expected to drive significant da Vinci 5 adoption upgrades across MEA cardiac surgical centers.

- In December 2025, Medtronic received FDA clearance for its Hugo robotic-assisted surgery system for urologic procedures — the first major medtech company to offer a credible competitive alternative to Intuitive Surgical’s da Vinci system in soft tissue surgery. The Hugo RAS system’s modular design and competitive pricing model positions it as a strong candidate for adoption across cost-sensitive MEA hospital procurement programs, particularly in public health system tenders across Saudi Arabia and Egypt.

- In July 2024, Saudi Arabia’s King Faisal Specialist Hospital and Research Centre (KFSH and RC) announced a landmark milestone, achieving a 98% survival rate across 400 robotic cardiac surgeries since the program’s launch in February 2019. This achievement firmly established KFSH and RC as a global leader in robotic cardiac care and reinforced Saudi Arabia’s position as the most advanced robotic surgery market in the MEA region, driving further institutional investment in surgical robotics across the Kingdom.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.