Middle East And Africa Pharmacogenetic Testing In Psychiatry Depression Market

Market Size in USD Million

USD

37.73 Million

USD

65.31 Million

2025

2033

USD

37.73 Million

USD

65.31 Million

2025

2033

| 2026 - 2033 | |

| USD 37.73 Million | |

| USD 65.31 Million | |

| % | |

|

Middle East and Africa Pharmacogenetics Testing in Psychiatry/Depression Market Overview

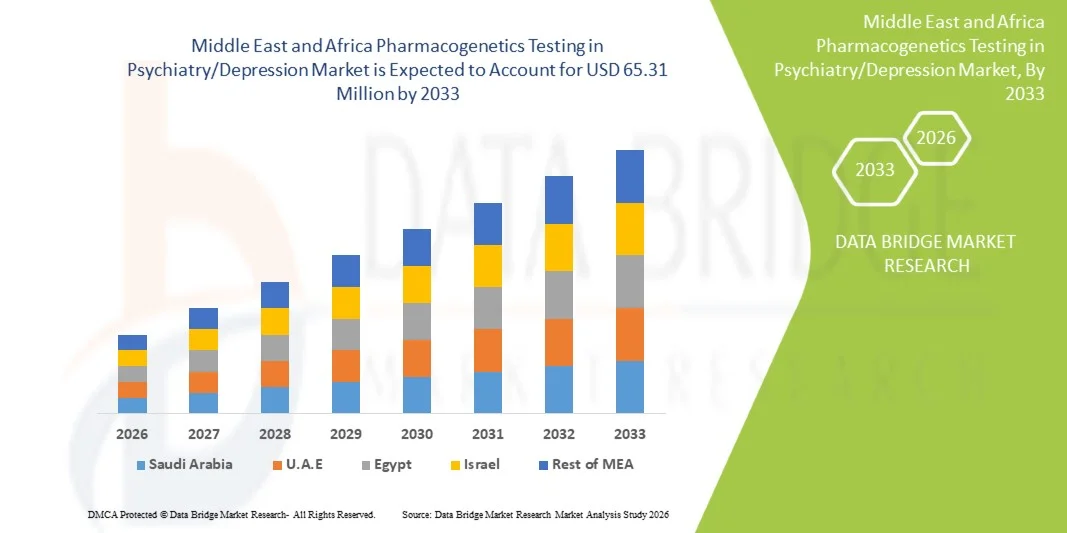

The Middle East and Africa pharmacogenetics testing in psychiatry/depression market was valued at USD 37.73 million in 2025 and is projected to reach USD 65.31 million by 2033, growing at a CAGR of 7.1% from 2026 to 2033. The market is witnessing steady expansion driven by increasing awareness of precision medicine in mental health care, rising prevalence of depression and other psychiatric disorders, and growing adoption of genetic testing to optimize antidepressant treatment outcomes.

The expanding burden of treatment-resistant depression, coupled with healthcare modernization initiatives and improving genomic infrastructure across key countries such as the UAE, Saudi Arabia, and South Africa, is encouraging adoption of pharmacogenetic testing solutions. Increasing collaboration between diagnostic laboratories, healthcare providers, and research institutions is further supporting clinical integration, while growing interest in personalized psychiatry is gradually positioning pharmacogenetics as a key tool in improving patient response rates and reducing adverse drug reactions.

Key Market Trends & Insights

- Saudi Arabia dominated the Middle East and Africa pharmacogenetics testing in psychiatry/depression market in 2025 with a 38.6% revenue share, supported by strong national genomics initiatives, expanding precision medicine programs, and increasing investment in mental health infrastructure.

- The Depression segment led the market with a 39.6% share in 2025, driven by the high prevalence of major depressive disorder and increasing rates of treatment-resistant cases requiring personalized medication strategies.

- South Africa is expected to be the fastest-growing country from 2026 to 2033, expanding at a CAGR of 7.8%, fueled by genomic research initiatives, improving healthcare access, and rising adoption of personalized mental health treatment approaches.

- Bipolar Disorders are the fastest-growing type, projected to register a CAGR of 7.9%, reflecting the surge in diagnosis rates and growing recognition of genetic influence on mood stabilization therapy response.

- The Chromosomal Array-Based Tests segment dominated the test type category with a 54.3% revenue share in 2025, led by its cost-effectiveness, faster turnaround time, and established clinical utility in psychiatric pharmacogenetics.

- Adult accounted for 61.2% of the market, preferred by the higher prevalence of depression and anxiety disorders in the working-age population.

- The Software & Services segment is the fastest-growing products category, with a CAGR of 8.6%, driven by the rising demand for AI-based interpretation platforms and clinical decision-support tools.

Market Size & Forecast

- Global Market Value (2025): USD 37.73 Million

- Expected Market Value (2033): USD 65.31 Million

- Forecast CAGR (2026–2033): 7.1%

- Leading Country in 2025: Saudi Arabia

- Fastest Growing Country: South Africa

Report Scope and Middle East and Africa Pharmacogenetics Testing in Psychiatry/Depression Market Segmentation

|

Attributes |

Middle East and Africa Pharmacogenetics Testing in Psychiatry/Depression Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa |

|

Key Market Players |

· Illumina, Inc. (U.S.) · Thermo Fisher Scientific Inc. (U.S.) · QIAGEN (Germany) · F. Hoffmann-La Roche Ltd (Switzerland) · Agilent Technologies, Inc. (U.S.) · PerkinElmer Inc. (U.S.) · Centogene N.V. (Germany) · Eurofins Scientific SE (Luxembourg) · Abbott (U.S.) · Labcorp (U.S.) · BGI Group (China) · Quest Diagnostics Incorporated (U.S.) · Revvity, Inc. (U.S.) · Azenta Life Sciences (U.S.) · Oxford Nanopore Technologies plc (U.K.) · PathCare Laboratories (South Africa) · Ampath Laboratories (South Africa) · Lancet Laboratories (South Africa) · Al Borg Diagnostics (Saudi Arabia) · Synlab International GmbH (Germany) |

|

Market Opportunities |

· Expansion of pharmacogenetic testing into treatment-resistant depression management · Integration of pharmacogenetic decision-support tools within electronic health record (EHR) systems · Growing adoption of direct-to-provider genomic testing services |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Middle East and Africa Pharmacogenetics Testing in Psychiatry/Depression Market Trends

Trend: Expansion of Precision Psychiatry and Multi-Gene Testing Adoption

Pharmacogenetics testing is increasingly being integrated into psychiatric care pathways across Middle East and Africa as clinicians shift toward personalized antidepressant selection and dose optimization. The adoption of multi-gene panels is improving treatment outcomes for depression patients, particularly in cases of treatment-resistant depression where conventional therapies show limited effectiveness. The integration of digital health platforms and clinical decision-support tools is enabling faster interpretation of genetic data, while hospitals and diagnostic networks are standardizing testing protocols to support routine psychiatric use. For instance, Saudi Arabia’s national genomics programs are expanding pharmacogenetic screening in psychiatric hospitals, while the United Arab Emirates is embedding genetic testing into hospital-based mental health services.

Middle East and Africa Pharmacogenetics Testing in Psychiatry/Depression Market Dynamics

Key Market Driver: Rising Burden of Depression and Demand for Personalized Treatment

The increasing prevalence of depression and other psychiatric disorders across Middle East and Africa is driving demand for more effective and personalized treatment strategies supported by pharmacogenetic testing. High rates of antidepressant non-response and adverse drug reactions are encouraging clinicians to adopt genetic testing to guide drug selection and dosage decisions. Government-led healthcare modernization initiatives and growing awareness of mental health are further accelerating clinical adoption of precision psychiatry approaches. For instance, South Africa’s expanding mental health programs are promoting pharmacogenetic-guided therapy in public healthcare systems, while Israel is integrating AI-supported genetic interpretation tools into psychiatric treatment planning.

Key Restraint/Challenge: High Cost and Limited Accessibility of Genetic Testing Infrastructure

The high cost of pharmacogenetic testing, coupled with limited laboratory infrastructure and uneven access to advanced diagnostics, remains a major barrier to market expansion across several Middle East and Africa countries. Many healthcare systems face budget constraints, and the lack of reimbursement policies for genetic testing further restricts adoption in public healthcare settings. In addition, shortage of trained genetic counselors and specialized laboratory professionals slows clinical integration and limits widespread use in psychiatric practice. For instance, while Qatar and Saudi Arabia have advanced centralized genomic facilities, several African countries still rely on outsourced testing services, increasing turnaround time and overall testing costs.

Key Market Opportunity: Expansion of AI-Driven Genomic Interpretation and Digital Health Integration

The integration of artificial intelligence with pharmacogenetic testing platforms presents a major opportunity by enabling faster interpretation of complex genetic profiles and improving clinical decision-making in psychiatry. Cloud-based genomic analysis, telepsychiatry platforms, and digital health ecosystems are expanding access to personalized mental health care across both developed and emerging healthcare systems. These technologies are helping bridge the gap between limited specialist availability and growing patient demand for precision treatment. For instance, Israel’s advanced digital health infrastructure is accelerating AI-powered pharmacogenomic analysis, while the United Arab Emirates is piloting cloud-based precision psychiatry platforms in hospital networks.

Middle East and Africa Pharmacogenetics Testing in Psychiatry/Depression Market Scope

The Middle East and Africa pharmacogenetics testing in psychiatry/depression market is segmented on the basis of type, test type, patient type, gene type, products, end user, and distribution channel.

- By Disorder Type

On the basis of disorder type, the Middle East and Africa pharmacogenetics testing in psychiatry/depression market is segmented into anxiety, mood disorders, depression, bipolar disorders, psychotic disorders, and eating disorders. The Depression segment dominated the market with a 39.6% share in 2025, driven by the high prevalence of major depressive disorder and increasing rates of treatment-resistant cases requiring personalized medication strategies. Clinicians are increasingly adopting pharmacogenetic testing to optimize antidepressant selection and reduce adverse drug reactions. Growing mental health awareness campaigns and government-led psychiatric healthcare programs are further strengthening demand. Hospitals and psychiatric clinics are integrating genetic testing into standard depression treatment pathways. Expanding insurance coverage for mental health diagnostics in select countries is also supporting adoption. The segment continues to benefit from rising demand for precision psychiatry solutions across both public and private healthcare systems.

The Bipolar Disorders segment is projected to register the fastest growth at a CAGR of 7.9% from 2026 to 2033, driven by increasing diagnosis rates and growing recognition of genetic influence on mood stabilization therapy response. Pharmacogenetic testing is being increasingly used to guide lithium and mood stabilizer dosing, improving treatment safety and effectiveness. Expanding psychiatric infrastructure in countries such as Saudi Arabia and South Africa is supporting early diagnosis and intervention. Rising awareness among clinicians about adverse drug reactions in bipolar treatment is accelerating adoption. Integration of AI-based decision-support tools is further enhancing clinical utility. Growing investment in mental health research is also contributing to segment expansion.

- By Test Type

On the basis of test type, the market is segmented into whole genome sequencing and chromosomal array-based tests. The Chromosomal Array-Based Tests segment dominated the market with a 54.3% share in 2025, owing to its cost-effectiveness, faster turnaround time, and established clinical utility in psychiatric pharmacogenetics. These tests are widely used in hospital laboratories for identifying gene-drug interactions relevant to antidepressant and antipsychotic response. Their relatively lower complexity compared to whole genome sequencing makes them more accessible in developing healthcare systems. Increasing demand for targeted gene panels further supports this segment’s dominance. Regulatory familiarity and reimbursement alignment in select countries also favor adoption. The segment remains the primary choice for routine clinical psychiatric testing.

The Whole Genome Sequencing segment is expected to witness the fastest growth at a CAGR of 8.4% from 2026 to 2033, driven by declining sequencing costs and increasing demand for comprehensive genetic profiling. It enables deeper insights into complex psychiatric disorders by analyzing broader genetic variations. Growing research collaborations and precision psychiatry initiatives are accelerating adoption in academic and advanced hospital settings. Integration with AI-driven interpretation platforms is improving clinical usability. Countries such as Israel and the United Arab Emirates are investing heavily in genomic medicine infrastructure. Expanding applications in treatment-resistant depression cases are further driving demand.

- By Patient Type

On the basis of patient type, the market is segmented into child, adult, and geriatric populations. The Adult segment dominated the market with a 61.2% share in 2025, primarily due to the higher prevalence of depression and anxiety disorders in the working-age population. Adults are more frequently prescribed antidepressants, making pharmacogenetic testing highly relevant for optimizing treatment response. Increasing workplace stress and urban lifestyle factors are contributing to rising mental health cases. Hospitals and psychiatric clinics are the primary testing points for adult patients. Growing awareness of personalized medicine is further boosting adoption. Insurance coverage expansion for adult mental health care is also supporting segment growth.

The Geriatric segment is projected to grow at the fastest CAGR of 7.6% from 2026 to 2033, driven by rising elderly population and increased sensitivity to psychotropic medications. Older patients are more prone to drug interactions and adverse effects, making pharmacogenetic guidance critical. Expanding elderly care programs in Gulf countries are supporting adoption. Clinicians are increasingly using genetic testing to improve medication safety in dementia-related depression cases. Rising healthcare expenditure for aging populations is further boosting demand. Integration of pharmacogenetics into geriatric psychiatry protocols is accelerating growth.

- By Gene Type

On the basis of gene type, the market is segmented into CYP2C19, CYP2C9, VKORC1, CYP2D6, HLA-B, HTR2A/C, HLA-A, CYP3A4, SLC6A4, MTHFR, COMT, and others. The CYP2D6 segment dominated the market with a 28.7% share in 2025, due to its critical role in metabolizing widely prescribed antidepressants and antipsychotics. Variations in this gene significantly influence drug efficacy and side-effect profiles, making it a primary focus of psychiatric pharmacogenetic testing. Clinical guidelines strongly support CYP2D6 testing in antidepressant selection. High clinical awareness among psychiatrists further strengthens its dominance. It is widely included in standard multi-gene pharmacogenetic panels. Increasing adoption in hospital laboratories is sustaining its leadership position.

The SLC6A4 gene segment is expected to register the fastest growth at a CAGR of 8.1% from 2026 to 2033, driven by its association with serotonin transport and antidepressant response variability. Rising research into serotonin-related depression mechanisms is increasing its clinical relevance. Growing demand for SSRI optimization is accelerating testing adoption. AI-based psychiatric decision-support systems are increasingly incorporating SLC6A4 markers. Expanding mental health research initiatives in Israel and South Africa are contributing to growth. Its inclusion in advanced pharmacogenetic panels is further boosting uptake.

- By Products

On the basis of products, the market is segmented into instruments, consumables, and software & services. The Consumables segment dominated the market with a 46.8% share in 2025, driven by recurring demand for reagents, test kits, and sample processing materials used in genetic testing workflows. Consumables are essential for routine laboratory operations, ensuring continuous revenue generation for suppliers. Increasing testing volumes across hospitals and diagnostic laboratories is supporting steady demand. Expansion of pharmacogenetic panel testing is further boosting consumable usage. Standardization of testing protocols across healthcare systems strengthens market stability. Rising adoption of multi-gene assays is also contributing to dominance.

The Software & Services segment is projected to grow at the fastest CAGR of 8.6% from 2026 to 2033, driven by rising demand for AI-based interpretation platforms and clinical decision-support tools. These systems help clinicians translate complex genetic data into actionable psychiatric treatment plans. Cloud-based genomic analytics are improving accessibility across healthcare networks. Increasing integration with electronic health records is enhancing workflow efficiency. Countries such as the United Arab Emirates and Israel are leading adoption of digital psychiatry solutions. Expanding telemedicine and precision psychiatry platforms are further accelerating growth.

- By End User

On the basis of end user, the market is segmented into hospitals and clinics, diagnostic laboratories, academic and research institutes, and others. The Hospitals and Clinics segment dominated the market with a 52.4% share in 2025, driven by high patient inflow for psychiatric disorders and integration of pharmacogenetic testing into routine clinical workflows. Hospitals serve as the primary point for diagnosis and treatment of depression and mood disorders. Increasing availability of psychiatric specialists is strengthening adoption. Government healthcare programs are promoting precision medicine in hospital settings. Integration of laboratory services within hospital networks is improving efficiency. Expanding mental health infrastructure across Gulf countries further supports dominance.

The Academic and Research Institutes segment is expected to grow at the fastest CAGR of 8.3% from 2026 to 2033, driven by increasing genomic research initiatives and clinical trials in psychiatric pharmacogenetics. These institutions are actively studying gene-drug interactions to improve treatment guidelines. Rising government funding for mental health research is supporting expansion. Collaboration with biotechnology companies is accelerating innovation. Countries such as South Africa and Israel are key contributors to research growth. Increasing publication output and clinical validation studies are further strengthening this segment.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, third-party distribution, hospital pharmacy, and others. The Direct Tender segment dominated the market with a 48.1% share in 2025, driven by large-scale procurement by government hospitals and national healthcare programs. Direct procurement ensures cost efficiency and standardized supply of testing kits and services. It is widely used in public healthcare systems across Gulf countries. Centralized purchasing agreements support bulk testing adoption. Strong regulatory oversight enhances transparency and quality control. This channel remains dominant in institutional procurement structures.

The Third-Party Distribution segment is projected to grow at the fastest CAGR of 7.7% from 2026 to 2033, driven by increasing demand from private diagnostic networks and smaller healthcare facilities. These distributors improve accessibility of pharmacogenetic testing products in emerging healthcare markets. Expanding laboratory outsourcing trends are supporting growth. Improved logistics and supply chain networks are enhancing distribution efficiency. Growing private healthcare expansion in Africa is accelerating adoption. Partnerships between global diagnostics firms and regional distributors are further strengthening this segment.

Middle East and Africa Pharmacogenetics Testing in Psychiatry/Depression Market Regional Analysis

Saudi Arabia dominated the Middle East and Africa pharmacogenetics testing in psychiatry/depression market in 2025 with a 38.6% revenue share, supported by strong national genomics initiatives, expanding precision medicine programs, and increasing investment in mental health infrastructure. The country also benefits from growing integration of pharmacogenetic testing into psychiatric hospitals, rising awareness of personalized medicine among clinicians, and expanding adoption of multi-gene testing panels for antidepressant optimization. Increasing focus on treatment-resistant depression management and AI-enabled clinical decision-support tools continues to strengthen Saudi Arabia’s leadership position in the regional market.

The Saudi Arabia Pharmacogenetics Testing in Psychiatry/Depression Market Insight

The Saudi Arabia pharmacogenetics testing in psychiatry/depression market is witnessing strong growth due to increasing national investment in genomics programs, rising mental health awareness, and expanding adoption of precision medicine in psychiatric care. The country’s advanced healthcare infrastructure, along with growing integration of genetic testing in hospitals and specialty clinics, is driving demand across depression, bipolar disorder, and anxiety treatment pathways. In addition, increasing focus on treatment-resistant depression management and AI-supported clinical decision tools is accelerating pharmacogenetic testing adoption across healthcare institutions.

United Arab Emirates Pharmacogenetics Testing in Psychiatry/Depression Market Insight

The United Arab Emirates pharmacogenetics testing in psychiatry/depression market remains a major contributor in the Middle East and Africa region, driven by strong government healthcare modernization initiatives and rapid adoption of personalized medicine. The widespread use of advanced diagnostic laboratories and hospital-based genetic testing services is supporting market expansion across psychiatric applications. Increasing investments in digital health platforms, AI-enabled clinical decision support systems, and integrated hospital networks continue to enhance pharmacogenetic adoption throughout the country.

South Africa Pharmacogenetics Testing in Psychiatry/Depression Market Insight

The South Africa pharmacogenetics testing in psychiatry/depression market is experiencing steady growth, supported by rising mental health burden, improving healthcare infrastructure, and expanding genomic research initiatives. Increasing awareness of personalized treatment approaches and growing collaboration between research institutions and diagnostic laboratories are driving adoption of pharmacogenetic testing. Furthermore, government-led healthcare programs and rising investments in precision medicine are strengthening the country’s position as a key emerging market in the region.

Qatar Pharmacogenetics Testing in Psychiatry/Depression Market Insight

The Qatar pharmacogenetics testing in psychiatry/depression market is witnessing gradual growth, driven by increasing investments in healthcare infrastructure, national genomics initiatives, and growing adoption of personalized medicine. The country’s centralized healthcare system and advanced laboratory facilities are supporting integration of pharmacogenetic testing into psychiatric care. In addition, rising focus on mental health awareness and precision treatment approaches is further contributing to market expansion across hospitals and specialized clinics.

Middle East and Africa Pharmacogenetics Testing in Psychiatry/Depression Market Share

The Middle East and Africa pharmacogenetics testing in psychiatry/depression industry is primarily led by well-established companies, including:

- Illumina, Inc. (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- QIAGEN (Germany)

- Hoffmann-La Roche Ltd (Switzerland)

- Agilent Technologies, Inc. (U.S.)

- PerkinElmer Inc. (U.S.)

- Centogene N.V. (Germany)

- Eurofins Scientific SE (Luxembourg)

- Abbott (U.S.)

- Labcorp (U.S.)

- BGI Group (China)

- Quest Diagnostics Incorporated (U.S.)

- Revvity, Inc. (U.S.)

- Azenta Life Sciences (U.S.)

- Oxford Nanopore Technologies plc (U.K.)

- PathCare Laboratories (South Africa)

- Ampath Laboratories (South Africa)

- Lancet Laboratories (South Africa)

- Al Borg Diagnostics (Saudi Arabia)

- Synlab International GmbH (Germany)

Latest Developments in Middle East and Africa Pharmacogenetics Testing in Psychiatry/Depression Market

- In March 2025, Saudi Ministry of Health expanded the Saudi Human Genome Program into clinical healthcare integration, strengthening precision medicine applications including pharmacogenomics for psychiatric and neurological disorders. The initiative aims to translate genomic data into clinical decision-making tools, supporting personalized treatment approaches for conditions such as depression and treatment-resistant psychiatric illnesses. This development reinforces Saudi Arabia’s leadership in regional genomics adoption and its growing use in hospital-based precision psychiatry services

- In October 2024, the United Arab Emirates accelerated its national genomics strategy under the Emirates Genome Program, focusing on integrating genomic data into healthcare systems to enable personalized treatment pathways. The program supports clinical adoption of pharmacogenomics across multiple therapeutic areas, including mental health and antidepressant response optimization. It also enhances AI-driven clinical interpretation systems used in hospital networks

- In July 2023, Israel’s Clalit Health Services expanded its precision medicine and pharmacogenomics initiatives, integrating genetic testing into routine clinical decision-making for drug response optimization. The program supports large-scale genomic screening and AI-based drug response modeling, which is increasingly applied in psychiatric treatment planning for depression and anxiety disorders. This advancement strengthens Israel’s position as a digital health and genomics leader in the region

- In November 2022, the Qatar Genome Programme under Qatar Foundation advanced its national genomic database initiative, supporting research and clinical translation of pharmacogenetic insights into healthcare. The program focuses on identifying population-specific genetic variations that influence drug response, including those relevant to psychiatric medications. This initiative is helping establish precision medicine frameworks within Qatar’s healthcare system

- In June 2021, the Centre for Proteomic and Genomic Research (CPGR) in South Africa expanded collaborative genomic research programs aimed at improving precision medicine adoption in African healthcare systems. The initiative supports translational genomics and biomarker discovery, enabling future pharmacogenetic applications in psychiatric and neurological disorders. This development contributes to building regional capacity for advanced molecular diagnostics

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.