Middle East And Africa Primary Angle Closure Glaucoma Market

Market Size in USD Million

USD

278.26 Million

USD

417.43 Million

2024

2032

USD

278.26 Million

USD

417.43 Million

2024

2032

| 2025 - 2032 | |

| USD 278.26 Million | |

| USD 417.43 Million | |

| % | |

|

Middle East and Africa Primary Angle-Closure Glaucoma Market Size

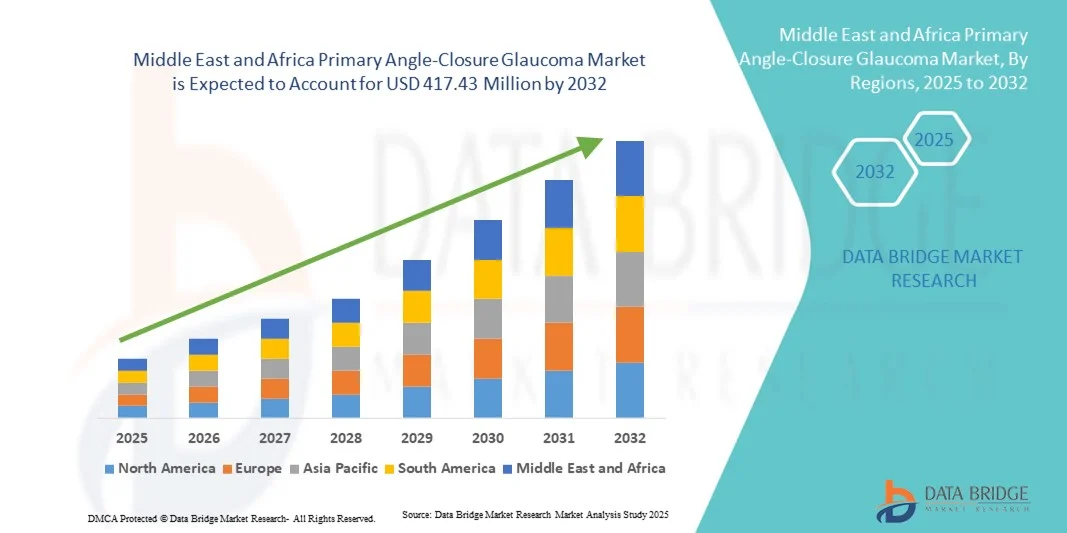

- The Middle East and Africa primary angle-closure glaucoma market size was valued at USD 278.26 million in 2024 and is expected to reach USD 417.43 million by 2032, at a CAGR of 5.2% during the forecast period

- The market growth is largely fueled by the rising prevalence of angle-closure glaucoma, increasing awareness of eye health, and advancements in diagnostic and surgical treatment options in the region

- Furthermore, the growing geriatric population and higher susceptibility among females are driving demand for effective management and treatment solutions, establishing advanced PACG therapies as the preferred clinical approach. These converging factors are accelerating the adoption of PACG solutions, thereby significantly boosting the industry’s growth

Middle East and Africa Primary Angle-Closure Glaucoma Market Analysis

- Primary angle-closure glaucoma (PACG), involving sudden or chronic blockage of the eye’s drainage angle, is increasingly a critical focus in ophthalmic care across MEA countries due to its risk of irreversible vision loss and growing awareness of early diagnosis and treatment options

- The escalating demand for PACG management is primarily fueled by rising prevalence of glaucoma, increasing geriatric populations, limited access to ophthalmic care in some areas, and growing adoption of advanced diagnostic and treatment solutions

- South Africa dominated the MEA PACG market with the largest revenue share of 29% in 2024, driven by higher disease awareness, well-established hospital networks, and adoption of advanced diagnostic and treatment devices

- Saudi Arabia is expected to be the fastest growing market during the forecast period due to expanding healthcare services, government initiatives to address vision health, and increasing availability of advanced ophthalmic procedures

- Acute angle-closure glaucoma segment dominated the PACG market with a market share of 46.5% in 2024, driven by urgent clinical management needs, rapid diagnosis, and high adoption of treatment procedures in hospitals and specialty clinics

Report Scope and Middle East and Africa Primary Angle-Closure Glaucoma Market Segmentation

|

Attributes |

Middle East and Africa Primary Angle-Closure Glaucoma Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Middle East and Africa Primary Angle-Closure Glaucoma Market Trends

Advancement in Minimally Invasive Surgical Techniques

- A significant and accelerating trend in the MEA PACG market is the increasing adoption of minimally invasive surgical procedures such as laser peripheral iridotomy and lens extraction, improving patient outcomes with reduced recovery time

- For instance, hospitals in South Africa and UAE are increasingly using femtosecond laser-assisted iridotomy devices to treat acute angle-closure glaucoma more effectively and safely

- These procedures enable precise treatment of the blocked drainage angle while minimizing complications, which is particularly beneficial in geriatric populations who represent a large portion of glaucoma patients

- The integration of these surgical techniques with advanced imaging and diagnostic tools facilitates better preoperative planning, allowing ophthalmologists to tailor interventions to individual patient needs

- This trend towards safer, more precise, and patient-friendly surgical solutions is fundamentally reshaping treatment protocols in the MEA region. Consequently, key players are investing in training programs and device availability to enhance adoption

- The demand for minimally invasive surgical solutions is growing rapidly across both hospitals and specialty clinics, as healthcare providers prioritize clinical efficacy, patient safety, and faster recovery

Middle East and Africa Primary Angle-Closure Glaucoma Market Dynamics

Driver

Increasing Prevalence and Awareness of Glaucoma

- The rising prevalence of angle-closure glaucoma and growing awareness among populations are key drivers for the heightened demand for diagnostic and treatment solutions

- For instance, government-led vision screening programs in Saudi Arabia and Egypt have increased early detection rates, encouraging timely intervention and treatment

- As patients become more aware of the risks of untreated PACG, healthcare providers are witnessing higher demand for advanced diagnostic devices and treatment procedures

- The expansion of ophthalmology clinics and specialized eye hospitals in countries such as UAE and South Africa supports greater patient access to PACG care

- The availability of advanced laser and lens-based treatment devices, coupled with growing training of ophthalmologists, is further propelling market growth

- In addition, the increasing adoption of hospital and specialty clinic-based PACG management solutions is enhancing early diagnosis and treatment outcome

- Rising private sector investment in ophthalmic infrastructure is creating new opportunities for PACG care in urban areas

- Collaborative initiatives between device manufacturers and healthcare providers to offer training and awareness programs are further driving market expansion

Restraint/Challenge

Limited Access to Eye Care and High Treatment Costs

- Limited access to specialized ophthalmic care in rural and underserved areas poses a significant challenge to broader PACG market penetration in the MEA region

- For instance, patients in remote regions of Egypt and South Africa often face delays in diagnosis and treatment due to lack of ophthalmologists and advanced facilities

- The high cost of surgical interventions and diagnostic equipment can restrict adoption, especially in lower-income populations and smaller clinics

- While government initiatives and NGO programs aim to improve access, disparities in healthcare infrastructure remain a major barrier to market growth

- Ensuring affordability, expanding training for ophthalmologists, and increasing distribution of diagnostic and treatment devices are essential to overcome these challenges

- Addressing these obstacles through public health programs, subsidized treatment schemes, and mobile screening units will be vital for sustained market expansion

- Lack of awareness among rural populations regarding glaucoma symptoms continues to delay diagnosis and treatment initiation

- Regulatory approvals and import restrictions for advanced ophthalmic devices in some MEA countries can slow market adoption

Middle East and Africa Primary Angle-Closure Glaucoma Market Scope

The market is segmented on the basis of disease type, type, end user, and distribution channel.

- By Disease Type

On the basis of disease type, the PACG market is segmented into acute angle-closure glaucoma and chronic angle-closure glaucoma. The acute angle-closure glaucoma segment dominated the market with the largest revenue share of 46.5% in 2024, driven by the urgent clinical need for diagnosis and treatment. Patients experiencing acute episodes require immediate intervention, which often leads them to hospitals and specialty clinics equipped with advanced diagnostic and treatment devices. The high prevalence of acute cases in geriatric populations across MEA countries further strengthens its dominance. Hospitals prioritize acute PACG management due to its potential to cause irreversible vision loss if untreated. The segment also benefits from increasing awareness campaigns highlighting early detection and treatment of acute glaucoma. Moreover, the availability of minimally invasive laser and lens-based interventions has improved patient outcomes, making this segment highly significant in the MEA PACG market.

The chronic angle-closure glaucoma segment is expected to witness the fastest growth during 2025–2032, fueled by rising awareness of long-term glaucoma management and increasing adoption of early screening programs. Chronic cases require ongoing monitoring and gradual intervention, which creates demand for diagnostic devices and follow-up treatments in both hospitals and specialty clinics. Growing patient education initiatives in countries such as Saudi Arabia, UAE, and Egypt are encouraging routine eye check-ups, driving early detection. The segment’s growth is also supported by teleophthalmology and portable diagnostic devices that facilitate management in underserved regions. In addition, the expanding healthcare infrastructure and increasing number of ambulatory surgical centers in MEA countries contribute to the faster adoption of chronic PACG management solutions.

- By Type

On the basis of type, the PACG market is segmented into diagnosis and treatment. The treatment segment dominated the market in 2024, accounting for the largest revenue share, due to the high demand for surgical interventions such as laser peripheral iridotomy and lens extraction. Treatment is essential to prevent permanent vision loss, making it a priority in hospitals and specialty clinics. Adoption of minimally invasive procedures has enhanced patient outcomes and reduced recovery times, increasing the preference for treatment-focused solutions. Healthcare providers in MEA countries are investing in state-of-the-art surgical devices to manage PACG efficiently. Government initiatives and hospital programs promoting advanced ophthalmic care further reinforce the segment’s dominance. Patients often prefer immediate intervention in acute cases, which positions treatment as the key revenue-driving subsegment.

The diagnosis segment is expected to witness the fastest growth from 2025 to 2032, driven by increasing awareness of early detection and the adoption of advanced diagnostic technologies such as anterior segment imaging and handheld tonometers. Early diagnosis helps prevent disease progression and reduces the risk of irreversible blindness. Teleophthalmology and portable diagnostic tools are enabling remote monitoring and screening, particularly in rural and underserved areas. Rising investment in community eye care programs and training of ophthalmologists in MEA countries is also boosting adoption. The segment benefits from the increasing number of specialty clinics and hospital-based screening initiatives. In addition, public health campaigns highlighting the importance of glaucoma detection are further driving the growth of the diagnostic segment.

- By End User

On the basis of end user, the PACG market is segmented into hospitals, specialty clinics, ambulatory surgical centers, and others. The hospitals segment dominated the market in 2024 with the largest revenue share, due to the comprehensive services provided for PACG patients including advanced diagnostics, surgical treatment, and post-operative care. Hospitals are the preferred choice for both acute and chronic cases, especially in South Africa, UAE, and Saudi Arabia, where healthcare infrastructure is well-established. High patient volumes and access to sophisticated treatment technologies make hospitals the primary revenue source. Hospitals also lead adoption of laser and lens-based interventions and employ specialized ophthalmologists, enhancing their market dominance. The integration of diagnostic and treatment services in hospitals ensures continuity of care and improved patient outcomes. Moreover, hospitals often participate in government and NGO-led screening programs, further increasing patient inflow.

The specialty clinics segment is expected to witness the fastest growth during 2025–2032, driven by their focus on eye care and ability to provide personalized treatment and follow-up. These clinics offer advanced diagnostic services and minimally invasive surgical solutions, catering to both acute and chronic PACG patients. The expansion of specialty clinics in UAE, Saudi Arabia, and Egypt improves access to quality ophthalmic care in urban and semi-urban areas. They are increasingly adopting portable and teleophthalmology devices to reach remote patients. Patients often prefer specialty clinics for shorter waiting times and specialized expertise. Furthermore, partnerships with diagnostic device manufacturers and government health programs accelerate the adoption of specialty clinic-based PACG care.

- By Distribution Channel

On the basis of distribution channel, the PACG market is segmented into direct tender, retail sales, and others. The direct tender segment dominated the market in 2024, owing to the procurement of diagnostic and treatment devices by hospitals and government healthcare programs. Large-scale tenders allow healthcare institutions to acquire high-cost surgical devices and imaging systems efficiently. Direct tender agreements often include maintenance and training, which encourages hospitals and specialty clinics to adopt advanced equipment. Countries such as Saudi Arabia, UAE, and South Africa utilize direct tender processes extensively for public hospital procurement. These agreements ensure standardized deployment of PACG solutions across multiple facilities, increasing revenue concentration. In addition, direct tenders facilitate bulk purchases for nationwide screening initiatives and government-supported eye care programs.

The retail sales segment is expected to witness the fastest growth from 2025 to 2032, fueled by increasing adoption of portable diagnostic devices and smaller treatment tools by specialty clinics and private practitioners. Retail channels allow quick access to equipment for smaller hospitals and clinics without lengthy procurement processes. The rise of teleophthalmology and community-based screening programs creates demand for easily deployable devices, boosting retail sales. Availability of affordable diagnostic and treatment tools for chronic PACG management in retail channels further supports growth. In addition, awareness programs and training workshops encourage clinics to directly purchase devices from manufacturers. The convenience of retail access and rapid product delivery strengthens this segment’s adoption in the MEA region.

Middle East and Africa Primary Angle-Closure Glaucoma Market Regional Analysis

- South Africa dominated the MEA PACG market with the largest revenue share of 29% in 2024, driven by higher disease awareness, well-established hospital networks, and adoption of advanced diagnostic and treatment devices

- Patients in the region increasingly value early detection, minimally invasive surgical interventions, and access to specialized ophthalmic care, which improves treatment outcomes and reduces the risk of irreversible vision loss

- This widespread adoption is further supported by government and NGO-led screening initiatives, growing geriatric populations, and expanding healthcare infrastructure, establishing hospitals and specialty clinics as the preferred providers for PACG management across the region

The South Africa Middle East and Africa Primary Angle-Closure Glaucoma Market Insight

The South Africa PACG market captured the largest revenue share of 28.5% in 2024 within the MEA region, driven by well-established hospitals, higher disease awareness, and widespread adoption of advanced diagnostic and treatment devices. Patients are increasingly prioritizing early detection and minimally invasive interventions to prevent irreversible vision loss. The growing geriatric population, combined with government and NGO-led glaucoma screening programs, further propels market growth. Moreover, the availability of laser and lens-based treatment options, alongside teleophthalmology initiatives, is significantly contributing to the market’s expansion.

Saudi Arabia Middle East and Africa Primary Angle-Closure Glaucoma Market Insight

The Saudi Arabia PACG market is expected to grow at a substantial CAGR during the forecast period, primarily driven by expanding healthcare infrastructure and rising awareness of glaucoma management. Increasing investments in hospitals and specialty clinics, coupled with the adoption of advanced diagnostic and surgical devices, are fostering market growth. Patients are drawn to accessible, high-quality care for both acute and chronic PACG cases. Government initiatives promoting eye health awareness and early diagnosis programs are further supporting the adoption of PACG solutions in the region.

UAE Middle East and Africa Primary Angle-Closure Glaucoma Market Insight

The UAE PACG market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by the country’s modern healthcare facilities and focus on advanced ophthalmic care. Rising prevalence of glaucoma, coupled with patient preference for minimally invasive treatment, encourages the adoption of laser and lens-based interventions. The UAE’s urbanized population and high healthcare spending power facilitate rapid integration of advanced devices. Teleophthalmology and specialty clinic expansion are also driving accessibility and early detection, further stimulating market growth.

Egypt Middle East and Africa Primary Angle-Closure Glaucoma Market Insight

The Egypt PACG market is poised to grow steadily during the forecast period, driven by rising patient awareness and expansion of hospital-based ophthalmic services. Government and NGO-led screening campaigns for early detection are increasing adoption of diagnostic devices. The growing number of specialty clinics, coupled with increasing availability of treatment options, is facilitating better patient outcomes. In addition, training programs for ophthalmologists and investments in portable diagnostic technologies are supporting both urban and semi-urban adoption of PACG care solutions.

Middle East and Africa Primary Angle-Closure Glaucoma Market Share

The Middle East and Africa Primary Angle-Closure Glaucoma industry is primarily led by well-established companies, including:

- Alcon Inc. (Switzerland)

- Bausch + Lomb (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Santen Pharmaceutical Co., Ltd. (Japan)

- Sun Pharmaceutical Industries Ltd. (India)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Novartis AG (Switzerland)

- Merck & Co., Inc. (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- AstraZeneca (U.K.)

- Sanofi (France)

- Reichert Inc. (U.S.)

- NIDEK CO., LTD (Japan)

- Oertli Instrumente AG (Switzerland)

- Thea Pharma Inc. (France)

- Viatris Inc. (U.S.)

- BVI (U.S.)

- TECHNOLAS PERFECT VISION GMBH (Germany)

What are the Recent Developments in Middle East and Africa Primary Angle-Closure Glaucoma Market?

- In May 2025, a study conducted in Tamale, Ghana, revealed that 36% of patients presenting with glaucoma had primary angle-closure glaucoma (PACG), highlighting the significant prevalence of PACG in the region. This study, the largest clinic-based investigation of its kind in Northern Ghana, underscores the urgent need for targeted screening and early intervention strategies. The high prevalence of PACG among glaucoma patients in this area calls for increased awareness and resource allocation to address this pressing health concern

- In April 2025, a scoping review synthesized current literature on glaucoma prevalence and management options among older adults in sub-Saharan Africa, emphasizing the need for early screening and detection, as well as reliable and long-term treatment options. The review highlighted that glaucoma, including PACG, is a leading cause of blindness in the elderly population of sub-Saharan Africa

- In February 2025, the Democratic Republic of Congo (DRC) announced a four-month cobalt export ban to address market oversupply and lift prices, marking the first major policy intervention by the DRC government in the cobalt market. This decision was prompted by a significant drop in cobalt prices, which had fallen to a nine-year low. The export ban aimed to stabilize the market and ensure fair pricing, affecting global supply chains and highlighting the DRC's strategic role in the global cobalt market

- In January 2025, the Boston Consulting Group (BCG) published its M&A Outlook 2025, forecasting a revival in mergers and acquisitions activity due to declining inflation, lower interest rates, and recovering valuations. The report indicated a cautious optimism among dealmakers, with expectations of increased activity in the technology sector, particularly in software and semiconductors. This outlook suggests a potential for growth and consolidation in industries related to healthcare and medical devices, which could impact the ophthalmic sector

- In June 2024, a study in Northern Ghana found that 36% of glaucoma patients had PACG, underscoring the need for increased awareness and screening programs in the region. The study emphasized the importance of early detection and appropriate management of PACG to prevent irreversible vision loss. It recommended the integration of regular eye examinations into public health initiatives to address the high burden of glaucoma in the region

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.