Middle East And Africa Smart Home Market

Market Size in USD Billion

USD

17.00 Billion

USD

58.88 Billion

2025

2033

USD

17.00 Billion

USD

58.88 Billion

2025

2033

| 2026 - 2033 | |

| USD 17.00 Billion | |

| USD 58.88 Billion | |

| % | |

|

Middle East and Africa Smart Home Market Overview

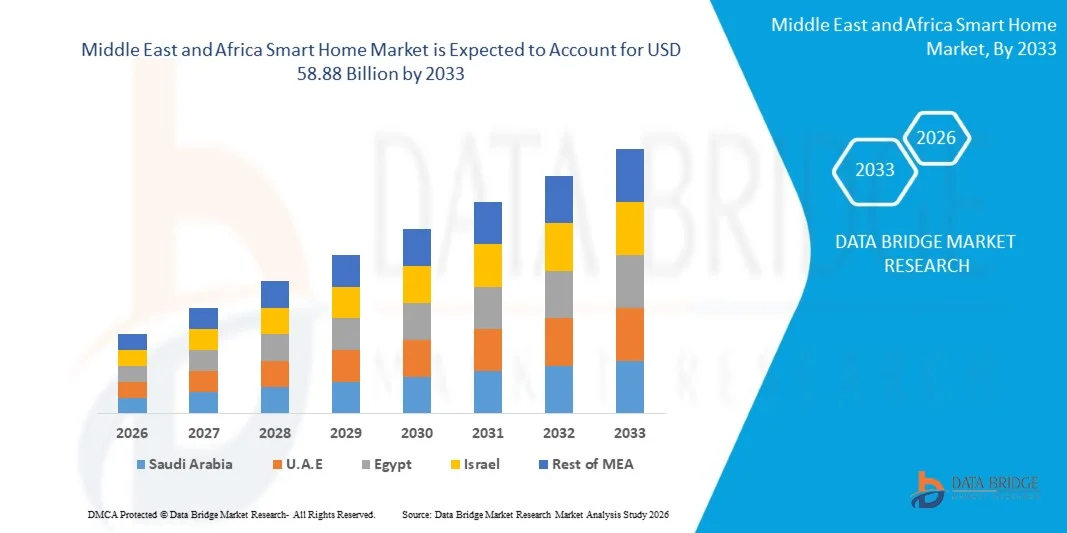

The Middle East and Africa smart home market was valued at USD 17.00 billion in 2025 and is projected to reach USD 58.88 billion by 2033, growing at a CAGR of 16.80% from 2026 to 2033. The market is witnessing strong expansion driven by rising urbanization, increasing disposable income, and growing consumer preference for connected and automated home solutions across security, energy management, lighting, and entertainment applications.

The rapid penetration of smartphones and high-speed internet connectivity, along with the expansion of IoT-enabled devices, is significantly accelerating smart home adoption across both developed and emerging economies in the region. Governments and private developers are increasingly integrating smart technologies into residential projects, particularly in high-growth markets such as the U.A.E. and Saudi Arabia. In addition, growing awareness of energy efficiency, enhanced home security requirements, and the rising trend of luxury and smart living lifestyles are further fueling market growth across Middle Eastern and African countries.

Key Market Trends & Insights

- U.A.E. dominated the Middle East and Africa smart home market with the largest revenue share in 2025, supported by strong smart city infrastructure development, high penetration of luxury residential projects, advanced digital connectivity, and early adoption of AI-based home automation systems.

- Saudi Arabia is expected to be the fastest-growing region, recording a strong CAGR from 2026 to 2033. Growth is driven by large-scale Vision 2030 smart city projects, increasing investment in intelligent residential infrastructure, rising demand for energy-efficient housing, and rapid deployment of IoT-enabled smart living ecosystems.

- The Security and Access Control segment held the largest market revenue share of approximately 28.6% in 2025, driven by rising concerns over residential safety, increasing adoption of AI-enabled surveillance systems, and strong demand for smart locks and biometric access solutions across urban housing developments in the U.A.E. and Saudi Arabia. High-value residential communities and gated villa projects are increasingly integrating centralized monitoring systems linked to mobile applications. In addition, growing expatriate population density in major cities is further strengthening demand for advanced home security infrastructure. Integration of cloud-based video analytics and remote access control is also enhancing adoption across premium housing projects.

- The Lighting Control segment is projected to register the fastest growth at a CAGR of 18.4% from 2026 to 2033, driven by increasing focus on energy efficiency, smart city initiatives, and widespread adoption of automated lighting systems integrated with IoT platforms in luxury residential and commercial buildings. Government-led sustainability programs are encouraging energy-efficient building designs, particularly in GCC countries. Smart lighting systems are increasingly being combined with motion sensors and AI-based occupancy detection. Rising adoption in hospitality and commercial real estate sectors is further supporting segment expansion.

- The Wireless segment accounted for the largest market revenue share of approximately 72.3% in 2025, supported by rapid penetration of Wi-Fi, Zigbee, and Bluetooth-enabled smart devices, along with ease of installation and growing consumer preference for flexible, retrofit-friendly solutions in both developed and emerging markets. Strong smartphone dependency among consumers is also accelerating wireless ecosystem adoption. Compatibility with multiple smart home platforms such as Alexa, Google Home, and Apple HomeKit is further boosting demand. Lower installation costs compared to wired systems make it highly attractive for mass-market residential adoption. Rapid expansion of broadband infrastructure across urban Africa is also supporting wireless penetration.

- The Wired segment is expected to grow at a CAGR of 11.2% from 2026 to 2033, driven by increasing deployment in high-end residential projects and commercial smart buildings where reliability, security, and stable connectivity are critical requirements, particularly in large-scale infrastructure developments in GCC countries. Wired systems are increasingly preferred in luxury villas and smart skyscraper projects for uninterrupted performance. They offer enhanced cybersecurity compared to wireless alternatives, making them suitable for sensitive environments. Integration with centralized building management systems is also increasing adoption in commercial real estate. Demand from premium smart city infrastructure projects is further accelerating growth.

- The Behavioral segment held the largest market revenue share of approximately 59.7% in 2025, driven by widespread adoption of user-controlled automation systems that allow manual customization of lighting, temperature, and security preferences through mobile applications and voice assistants. Consumers prefer direct control over smart devices, especially in early-stage adoption markets. Continuous improvements in app-based interfaces are enhancing user engagement. Strong integration with IoT ecosystems is supporting widespread usage across residential applications. Affordability and ease of deployment are also contributing to segment dominance.

- The Proactive segment is projected to register the fastest growth at a CAGR of 17.6% from 2026 to 2033, supported by increasing integration of AI and machine learning algorithms that enable predictive automation, energy optimization, and real-time behavioral adaptation in smart residential environments. Smart homes are increasingly shifting toward self-learning systems that anticipate user needs. Rising deployment of AI-powered energy management systems is improving efficiency in large residential complexes. Integration with big data analytics is enabling personalized living experiences. Expansion of smart city ecosystems is further accelerating adoption across advanced urban developments.

- The Indirect segment accounted for the largest market revenue share of approximately 66.1% in 2025, driven by strong presence of distributors, system integrators, and retail networks across the Middle East and Africa, enabling wider accessibility of smart home devices to consumers. Established electronics retail chains play a key role in product penetration. System integrators are widely used in large-scale residential and commercial projects. Availability of bundled smart home packages is increasing indirect sales. Growing e-commerce platforms are also strengthening distribution reach across urban and semi-urban areas.

- The Direct segment is expected to grow at a CAGR of 12.5% from 2026 to 2033, supported by increasing adoption of customized smart home solutions offered directly by manufacturers and technology providers, particularly in premium residential projects and large-scale smart city developments across the region. OEMs are increasingly offering end-to-end installation and subscription-based services. Direct engagement allows better personalization and system integration for high-value customers. Growing demand for enterprise-level smart building solutions is also supporting expansion. Strategic partnerships with real estate developers are further strengthening direct sales channels.

Market Size & Forecast

- Market Value (2025): USD 17.00 Billion

- Expected Market Value (2033): USD 58.88 Billion

- Forecast CAGR (2026–2033): 16.80%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Middle East and Africa Smart Home Market Segmentation

|

Attributes |

Middle East and Africa Smart Home Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

• Al-Futtaim Technologies (U.A.E.) |

|

Market Opportunities |

• Expansion Of IoT Enabled Smart Home Ecosystems |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Middle East and Africa Smart Home Market Trends

Trend: Growth In IoT Enabled Automation And AI Powered Smart Living Systems

Increasing demand for connected, intelligent, and energy-efficient residential ecosystems is driving the adoption of smart home technologies across the Middle East and Africa. Rising urbanization, high disposable income in GCC countries, and growing preference for luxury and convenience-based lifestyles are accelerating the deployment of smart security systems, lighting control, and energy management solutions. Traditional housing systems are being replaced by integrated IoT-enabled platforms that allow centralized control of multiple home functions through smartphones and voice assistants.

In modern residential developments, particularly in Saudi Arabia’s NEOM smart city project and large-scale housing projects in the U.A.E., developers are integrating smart home ecosystems with AI-driven automation for energy optimization and predictive maintenance. For instance, smart thermostats and AI-based lighting systems are being widely deployed to reduce electricity consumption by up to 20–30% in high-end residential buildings, improving sustainability performance while lowering utility costs.

The increasing penetration of 5G networks and fiber-optic infrastructure is also enhancing the responsiveness and reliability of smart home devices, enabling real-time automation and remote monitoring. In addition, growing demand for advanced home security solutions, such as AI-powered surveillance cameras and biometric access control systems, is expanding rapidly due to rising safety concerns in urban centers. Pilot smart residential projects launched in the U.A.E. in 2025 integrating fully connected IoT home ecosystems reported improved energy efficiency and a reduction of nearly 25% in household energy consumption under optimized usage conditions

Global Smart Home Market Dynamics

Key Market Driver: Rising Urbanization And Increasing Demand For Connected Living Solutions

Rapid urban population growth across the Middle East and Africa is significantly increasing demand for modern housing infrastructure integrated with smart technologies. Governments and private developers are actively promoting smart city initiatives that include automated homes, intelligent infrastructure, and energy-efficient buildings. Consumers are increasingly adopting smart devices such as connected appliances, smart lighting, and AI-enabled home assistants to enhance convenience, security, and energy management.

Large-scale infrastructure projects such as Saudi Arabia’s Vision 2030 smart city developments and the U.A.E.’s Smart Dubai initiative are accelerating adoption of IoT-based residential solutions. For instance, smart home integration in newly developed luxury apartments in Dubai has shown energy savings of around 18–25% through automated climate control and lighting systems.

In addition, increasing smartphone penetration and improved internet connectivity across emerging African economies are expanding access to affordable smart home solutions, enabling wider market penetration beyond high-income urban segments

Key Restraint/Challenge: High Initial Installation Costs And Limited Infrastructure Readiness

Despite strong growth potential, high upfront installation costs of smart home systems remain a significant barrier in price-sensitive markets across Africa and parts of the Middle East. Advanced IoT devices, AI-enabled security systems, and integrated home automation platforms require substantial investment, limiting adoption among middle-income consumers.

In addition, lack of standardized infrastructure and interoperability between devices from different manufacturers creates integration challenges, reducing user convenience and slowing adoption rates. Limited technical awareness and shortage of skilled installation professionals in several African countries further restrict market penetration.

Market assessments indicate that initial smart home setup costs in GCC luxury residential projects can be 30–50% higher compared to conventional housing systems, making affordability a key concern for broader mass-market adoption, especially in emerging economies

Key Market Opportunity: Expansion Of Smart City Projects And AI Driven Residential Ecosystems

Rapid expansion of smart city initiatives across Saudi Arabia, the U.A.E., and emerging African urban hubs is creating strong opportunities for smart home technology providers. Integration of AI, IoT, and cloud-based platforms in residential infrastructure is enabling fully automated living environments with predictive energy management and enhanced security features.

Developers are increasingly embedding smart home systems in new residential projects to enhance property value and attract tech-savvy consumers. For instance, large-scale developments in NEOM and Dubai South are incorporating centralized smart home ecosystems that connect security, energy, and entertainment systems into unified digital platforms.

In addition, increasing investments by global technology companies and regional telecom operators in smart infrastructure are supporting ecosystem expansion. Pilot projects in 2025 across the U.A.E. demonstrated up to 30% improvement in building energy optimization through AI-driven smart home management systems, highlighting strong future scalability potential across both developed and emerging markets in the region.

Middle East and Africa Smart Home Market Scope

The market is segmented on the basis of product type, technology, software and service, and sales channel.

• By Product Type

On the basis of product type, the Middle East and Africa smart home market is segmented into Entertainment Controls, Security and Access Control, HVAC Control, Home Appliances, Smart Kitchen, Lighting Control, Smart Furniture, Home Healthcare, and Others. The Security and Access Control segment held the largest market revenue share of approximately 28.6% in 2025, driven by rising concerns over residential safety, increasing adoption of AI-enabled surveillance systems, and strong demand for smart locks and biometric access solutions across urban housing developments in the U.A.E. and Saudi Arabia. High-value residential communities and gated villa projects are increasingly integrating centralized monitoring systems linked to mobile applications. In addition, growing expatriate population density in major cities is further strengthening demand for advanced home security infrastructure. Integration of cloud-based video analytics and remote access control is also enhancing adoption across premium housing projects.

The Lighting Control segment is projected to register the fastest growth at a CAGR of 18.4% from 2026 to 2033, driven by increasing focus on energy efficiency, smart city initiatives, and widespread adoption of automated lighting systems integrated with IoT platforms in luxury residential and commercial buildings. Government-led sustainability programs are encouraging energy-efficient building designs, particularly in GCC countries. Smart lighting systems are increasingly being combined with motion sensors and AI-based occupancy detection. Rising adoption in hospitality and commercial real estate sectors is further supporting segment expansion.

• By Technology

On the basis of technology, the market is segmented into Wireless and Wired systems. The Wireless segment accounted for the largest market revenue share of approximately 72.3% in 2025, supported by rapid penetration of Wi-Fi, Zigbee, and Bluetooth-enabled smart devices, along with ease of installation and growing consumer preference for flexible, retrofit-friendly solutions in both developed and emerging markets. Strong smartphone dependency among consumers is also accelerating wireless ecosystem adoption. Compatibility with multiple smart home platforms such as Alexa, Google Home, and Apple HomeKit is further boosting demand. Lower installation costs compared to wired systems make it highly attractive for mass-market residential adoption. Rapid expansion of broadband infrastructure across urban Africa is also supporting wireless penetration.

The Wired segment is expected to grow at a CAGR of 11.2% from 2026 to 2033, driven by increasing deployment in high-end residential projects and commercial smart buildings where reliability, security, and stable connectivity are critical requirements, particularly in large-scale infrastructure developments in GCC countries. Wired systems are increasingly preferred in luxury villas and smart skyscraper projects for uninterrupted performance. They offer enhanced cybersecurity compared to wireless alternatives, making them suitable for sensitive environments. Integration with centralized building management systems is also increasing adoption in commercial real estate. Demand from premium smart city infrastructure projects is further accelerating growth.

• By Software and Service

On the basis of software and service, the market is segmented into Behavioral and Proactive systems. The Behavioral segment held the largest market revenue share of approximately 59.7% in 2025, driven by widespread adoption of user-controlled automation systems that allow manual customization of lighting, temperature, and security preferences through mobile applications and voice assistants. Consumers prefer direct control over smart devices, especially in early-stage adoption markets. Continuous improvements in app-based interfaces are enhancing user engagement. Strong integration with IoT ecosystems is supporting widespread usage across residential applications. Affordability and ease of deployment are also contributing to segment dominance.

The Proactive segment is projected to register the fastest growth at a CAGR of 17.6% from 2026 to 2033, supported by increasing integration of AI and machine learning algorithms that enable predictive automation, energy optimization, and real-time behavioral adaptation in smart residential environments. Smart homes are increasingly shifting toward self-learning systems that anticipate user needs. Rising deployment of AI-powered energy management systems is improving efficiency in large residential complexes. Integration with big data analytics is enabling personalized living experiences. Expansion of smart city ecosystems is further accelerating adoption across advanced urban developments.

• By Sales Channel

On the basis of sales channel, the market is segmented into Direct and Indirect channels. The Indirect segment accounted for the largest market revenue share of approximately 66.1% in 2025, driven by strong presence of distributors, system integrators, and retail networks across the Middle East and Africa, enabling wider accessibility of smart home devices to consumers. Established electronics retail chains play a key role in product penetration. System integrators are widely used in large-scale residential and commercial projects. Availability of bundled smart home packages is increasing indirect sales. Growing e-commerce platforms are also strengthening distribution reach across urban and semi-urban areas.

The Direct segment is expected to grow at a CAGR of 12.5% from 2026 to 2033, supported by increasing adoption of customized smart home solutions offered directly by manufacturers and technology providers, particularly in premium residential projects and large-scale smart city developments across the region. OEMs are increasingly offering end-to-end installation and subscription-based services. Direct engagement allows better personalization and system integration for high-value customers. Growing demand for enterprise-level smart building solutions is also supporting expansion. Strategic partnerships with real estate developers are further strengthening direct sales channels.

Middle East and Africa Smart Home Market Regional Analysis

U.A.E. Smart Home Market Insight

The U.A.E. smart home market was dominated by U.A.E. with the largest revenue share of 38.6% in 2025, supported by rapid smart city development initiatives, high adoption of luxury residential technologies, and strong government-backed digital transformation programs. Consumers in the region highly value convenience, advanced security systems, and seamless integration of IoT-enabled devices across lighting, HVAC, entertainment, and home security applications. This widespread adoption is further supported by high disposable income levels, a strong expatriate population base, and increasing demand for energy-efficient and automated living solutions, establishing the U.A.E. as the leading smart home market in the region.

Saudi Arabia Smart Home Market Insight

The Saudi Arabia smart home market captured the largest revenue share in 2025 within the Middle East and Africa region, driven by large-scale smart city projects such as NEOM and Vision 2030 housing developments. Consumers are increasingly prioritizing intelligent home automation systems for security, energy management, and convenience. The rapid expansion of high-end residential projects, combined with rising demand for AI-powered surveillance systems and smart appliances, is further accelerating market growth. In addition, increasing investments in digital infrastructure and strong government support for smart living ecosystems are significantly contributing to the market’s expansion.

Middle East and Africa Smart Home Market Share

The Middle East and Africa Smart Home industry is primarily led by well-established companies, including:

• Al-Futtaim Technologies (U.A.E.)

• Etisalat Digital (U.A.E.)

• Emaar Technologies (U.A.E.)

• Du Smart Services (U.A.E.)

• Sahara Net (Saudi Arabia)

• Solutions by stc (Saudi Arabia)

• Saudi Controls Ltd (Saudi Arabia)

• Al Salem Johnson Controls (Saudi Arabia)

• Morpho Technologies Africa (South Africa)

• CBI Electric Telecom Solutions (South Africa)

• DStv Smart Technologies (South Africa)

• Smart Technology Group (Egypt)

• Raya Information Technology (Egypt)

• Orascom Smart Solutions (Egypt)

• Altron Smart Systems (South Africa)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Middle East And Africa Smart Home Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Middle East And Africa Smart Home Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Middle East And Africa Smart Home Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.