Middle East And Africa Sugar Substitutes Market

Market Size in USD Billion

USD

2.14 Billion

USD

3.73 Billion

2025

2033

USD

2.14 Billion

USD

3.73 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.14 Billion | |

| USD 3.73 Billion | |

| % | |

|

Middle East and Africa Sugar Substitute Market Overview

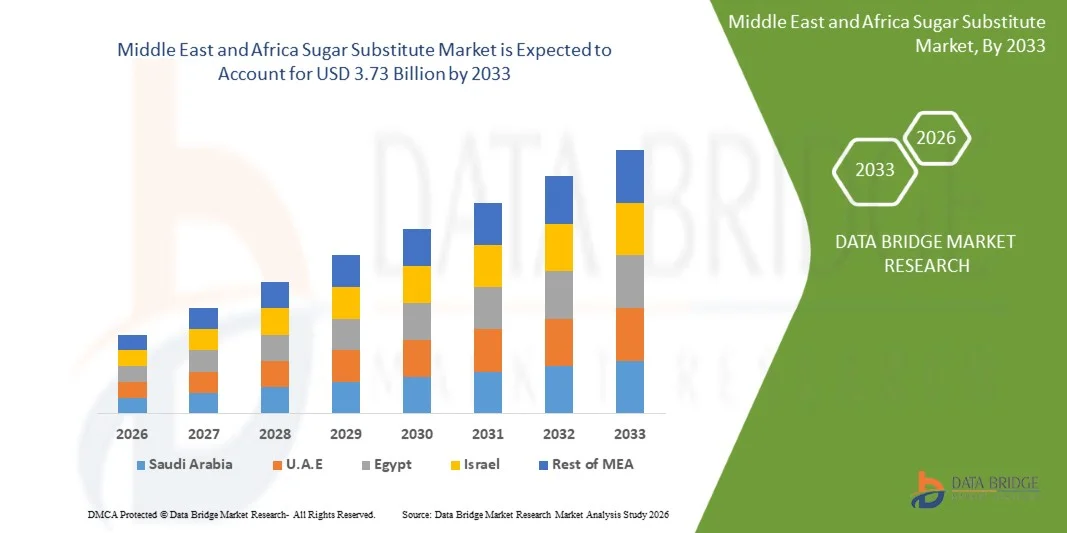

The Middle East and Africa sugar substitute market was valued at USD 2.14 Billion in 2025 and is projected to reach USD 3.73 Billion by 2033, growing at a CAGR of 7.2% from 2026 to 2033. The market is experiencing consistent growth driven by rising consumer awareness regarding sugar-related health concerns, increasing demand for low-calorie and diabetic-friendly food products, and growing adoption of clean-label sweetening ingredients across the food and beverage industry. Expanding utilization of natural sweeteners in functional foods, beverages, and nutraceutical products, along with continuous innovation in sugar reduction technologies, is further supporting market expansion across developed and emerging economies.

The increasing global focus on healthier dietary habits and sugar reduction initiatives, combined with rising prevalence of obesity and diabetes, is encouraging food manufacturers to incorporate alternative sweetening solutions into product formulations. Sugar substitutes are increasingly being utilized in beverages, bakery products, confectionery, dairy items, pharmaceuticals, and oral care applications to maintain sweetness while reducing calorie content. Growing regulatory support for reduced-sugar food products and rising consumer preference for plant-based and naturally sourced ingredients are further accelerating adoption across global food processing industries.

Key Market Trends & Insights

- South Africa dominated the Middle East and Africa sugar substitute market with the largest revenue share of 22.58% in 2025, supported by strong demand for low-calorie and diabetic-friendly food products, rising prevalence of lifestyle-related diseases, and well-established food and beverage manufacturing industries

- The powder segment led the market with a 72.12% share in 2025, driven by its extensive use across bakery, confectionery, dairy, and tabletop sweetener applications

- A.E. is expected to be the fastest-growing country at a CAGR of 6.9% from 2026 to 2033, fueled by rising consumer shift toward healthy and functional food products, strong demand for premium low-sugar beverages, and rapid expansion of the foodservice and hospitality sector

- Natural is the fastest-growing category type, projected to register a CAGR of 9.28% from 2026 to 2033, supported by increasing consumer inclination toward clean-label and naturally sourced ingredients

- The High-Intensity sweeteners segment dominated the type category with a 61.34% revenue share in 2025, led by rising consumer demand for low-calorie and sugar-free food products across beverages, bakery, and processed food categories

- Synthetic segment accounted for 56.90% of the market in 2025, preferred by its cost-effectiveness, high sweetness intensity, and widespread commercial availability

- The pharmaceuticals segment is the fastest-growing application category, with a CAGR of 9.13% from 2026 to 2033, driven by increasing use of sugar substitutes in syrups, chewable tablets, nutraceuticals, and diabetic-friendly medicinal formulations

Market Size & Forecast

- Market Value (2025): USD 2.14 Billion

- Expected Market Value (2033): USD 3.73 Billion

- Forecast CAGR (2026–2033): 7.2%

- Leading Country in 2025: South Africa

- Fastest Growing Country: A.E.

Report Scope and Middle East and Africa Sugar Substitute Market Segmentation

|

Attributes |

Sugar Substitute Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa |

|

Key Market Players |

|

|

Market Opportunities |

· Expansion of Sugar Substitutes in Functional and Fortified Beverages · Growing Utilization of Plant-Based Sweeteners in Bakery and Confectionery Applications · Increasing Adoption of Sugar Alternatives in Pharmaceutical and Nutraceutical Formulations |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Middle East and Africa Sugar Substitute Market Trends

Trend: Growth of Natural Clean-Label Sweeteners

The Sugar Substitute market is witnessing strong adoption of natural and clean-label sweeteners driven by rising consumer preference for plant-based, non-synthetic sugar alternatives in food and beverage products. Increasing demand for stevia, monk fruit, and other botanical sweeteners is reshaping product formulations across beverages, bakery, and dairy applications. Food manufacturers are reformulating products to reduce artificial additives and align with healthier dietary preferences, especially in developed markets.

Companies such as Cargill, Incorporated and Ingredion are actively expanding their stevia-based portfolios through innovations in taste optimization and blending solutions to improve consumer acceptance of natural sweeteners.

Middle East and Africa Sugar Substitute Market Dynamics

Key Market Driver: Rising Demand for Low-Calorie Diabetic-Friendly Products

The increasing prevalence of obesity and diabetes is significantly driving demand for low-calorie and sugar-free food products across global markets. Food and beverage manufacturers are widely adopting sugar substitutes to maintain sweetness while reducing glycemic impact in beverages, confectionery, and processed foods. Government-led sugar reduction initiatives and nutritional labeling regulations are further supporting market penetration of alternative sweeteners.

Companies such as Tate & Lyle and Ajinomoto Health & Nutrition North America, Inc. are expanding their low-calorie sweetener portfolios, including stevia and amino acid-based sweeteners, to meet rising demand for diabetic-friendly formulations.

Key Restraint/Challenge: Taste and Formulation Limitations of Substitutes

Despite strong demand growth, sugar substitutes face challenges related to aftertaste, solubility, and stability in complex food formulations. High-intensity sweeteners often require blending systems to replicate sugar-like taste profiles, increasing formulation complexity for manufacturers. These limitations can restrict adoption in premium bakery and confectionery products where sensory experience is critical.

Companies such as Roquette Frères and BENEO are investing in advanced formulation technologies and polyol-based solutions to improve taste masking and functional performance in sugar reduction applications.

Key Market Opportunity: Expansion in Functional Beverages

The growing demand for functional beverages, including sports drinks, energy drinks, and fortified waters, is creating strong opportunities for sugar substitute adoption. Manufacturers are increasingly incorporating low-calorie sweeteners to enhance product appeal while meeting health-focused consumer expectations. Rising consumption of ready-to-drink beverages and nutraceutical drinks is further accelerating market expansion.

Companies such as Cargill, Incorporated and JK Sucralose Inc. are actively supplying high-performance sweeteners tailored for beverage applications, supporting large-scale reformulation efforts across global beverage brands.

Middle East and Africa Sugar Substitute Market Scope

The sugar substitute market is segmented on the basis of type, form, category, and application.

- By Type

On the basis of type, the Sugar Substitute market is segmented into high-fructose syrups, high-intensity sweeteners, and low-intensity sweeteners. The High-Intensity Sweeteners segment dominated the market with the largest share of 61.34% in 2025, driven by rising consumer demand for low-calorie and sugar-free food products across beverages, bakery, and processed food categories. Increasing awareness regarding obesity, diabetes, and excessive sugar consumption is encouraging manufacturers to adopt high-intensity sweeteners such as stevia, sucralose, and aspartame in large-scale food formulations. The segment benefits from strong utilization in carbonated drinks and functional beverages where sweetness with minimal caloric impact is highly preferred. Continuous innovation in taste-masking technologies and improved product formulations are further supporting consumer acceptance. Expanding approvals from food safety authorities across major economies continue to strengthen the segment’s leading position.

The high-fructose syrups segment is projected to register the fastest growth at a CAGR of 8.12% from 2026 to 2033, driven by increasing demand from the processed food and beverage industry for cost-effective and high-stability sweetening solutions. High-fructose syrups are widely utilized in carbonated drinks, packaged juices, bakery products, and confectionery applications due to their superior sweetness retention and extended shelf life. Rising consumption of convenience foods and ready-to-drink beverages across emerging economies is further accelerating product adoption. Manufacturers are increasingly preferring high-fructose syrups because of their easy blending capabilities and efficient large-scale production compatibility.

- By Form

On the basis of form, the Sugar Substitute market is segmented into crystallized, liquid, and powder. The Powder segment dominated the market with a share of 72.12% in 2025, supported by its extensive use across bakery, confectionery, dairy, and tabletop sweetener applications. Powdered sugar substitutes provide excellent blending properties, longer shelf life, and ease of transportation, making them highly suitable for large-scale food manufacturing operations. The segment also benefits from rising demand for sachet-based sweeteners used in cafes, restaurants, and household consumption. Strong compatibility with dry food processing systems and packaged food formulations continues to enhance industrial adoption. Increasing use of powdered natural sweeteners in health-focused products further strengthens market dominance.

The Liquid segment is projected to register the fastest growth at a CAGR of 7.95% from 2026 to 2033, driven by rising demand for ready-to-drink beverages, flavored syrups, and liquid nutritional products. Liquid sugar substitutes are increasingly preferred in beverage manufacturing due to their superior solubility and ease of formulation in cold and hot drinks. Growing consumption of low-calorie soft drinks, energy drinks, and flavored water products is accelerating demand across global beverage industries. Advancements in liquid sweetener stabilization and preservation technologies are improving product quality and shelf performance. Expanding use in pharmaceutical syrups and oral healthcare formulations is also contributing significantly to segment growth.

- By Category

On the basis of category, the Sugar Substitute market is segmented into natural and synthetic. The Synthetic segment dominated the market with the largest share of 56.90% in 2025, driven by its cost-effectiveness, high sweetness intensity, and widespread commercial availability. Synthetic sweeteners such as aspartame, saccharin, and sucralose are extensively utilized in carbonated beverages, packaged foods, and pharmaceutical products due to their stability and scalability in industrial production. The segment benefits from strong penetration in mass-market food and beverage manufacturing where pricing efficiency remains a key purchasing factor. Continuous demand from processed food industries and expanding low-sugar product portfolios are supporting large-scale consumption globally. Strong regulatory approvals across multiple countries further reinforce the segment’s market leadership.

The Natural segment is projected to register the fastest growth at a CAGR of 9.28% from 2026 to 2033, driven by increasing consumer inclination toward clean-label and naturally sourced ingredients. Growing concerns regarding the long-term health effects of artificial additives are encouraging food manufacturers to shift toward natural alternatives such as stevia, monk fruit, and thaumatin. Rising demand for organic beverages, healthy snacks, and functional nutrition products is significantly accelerating adoption across premium product categories. Technological advancements in natural sweetener extraction and flavor enhancement are improving taste acceptance among consumers. Increasing investments by food companies in sustainable and plant-based ingredient sourcing are further strengthening future market expansion.

- By Application

On the basis of application, the Sugar Substitute market is segmented into beverages, food products, oral care, pharmaceuticals, and others. The Beverages segment dominated the market with a share of 44.70% in 2025, driven by rising global demand for low-calorie soft drinks, flavored water, sports beverages, and sugar-free energy drinks. Beverage manufacturers are increasingly incorporating sugar substitutes to reduce calorie content while maintaining sweetness and flavor consistency in products. The segment benefits from growing consumer awareness regarding sugar-related health conditions including obesity and diabetes. Strong innovation in functional beverages and fortified drinks is further increasing the use of alternative sweetening solutions. Expanding regulatory initiatives promoting sugar reduction across beverage industries continue to support segment dominance.

The Pharmaceuticals segment is projected to register the fastest growth at a CAGR of 9.13% from 2026 to 2033, driven by increasing use of sugar substitutes in syrups, chewable tablets, nutraceuticals, and diabetic-friendly medicinal formulations. Pharmaceutical manufacturers are focusing on improving patient compliance by enhancing taste profiles without increasing sugar content in medicines. Rising prevalence of chronic diseases and diabetes is encouraging development of low-sugar therapeutic products across pediatric and adult healthcare applications. Advancements in excipient technologies and formulation stability are improving compatibility of sugar substitutes in pharmaceutical production. Growing expansion of nutraceutical and wellness industries is further accelerating adoption across global healthcare markets.

Middle East and Africa Sugar Substitute Market Regional Analysis

South Africa dominated the sugar substitute market and accounted for the largest revenue share of 22.58% in 2025, driven by strong demand for low-calorie and diabetic-friendly food products, rising prevalence of lifestyle-related diseases, and well-established food and beverage manufacturing industries. The country has a growing health-conscious consumer base, which is accelerating adoption of sugar-free beverages, bakery products, and dairy alternatives. Increasing penetration of international food brands and strong retail expansion are further supporting widespread availability of sugar substitutes across urban markets. Growing usage of high-intensity sweeteners such as stevia and sucralose in processed foods continues to reinforce South Africa’s dominant position in the regional market.

U.A.E. Sugar Substitute Market Insight

The U.A.E. is projected to register the fastest CAGR of 6.9% during 2026–2033, driven by rising consumer shift toward healthy and functional food products, strong demand for premium low-sugar beverages, and rapid expansion of the foodservice and hospitality sector. Increasing awareness of obesity and diabetes risks is encouraging manufacturers to reformulate products with alternative sweeteners across beverages, confectionery, and nutraceutical applications. Government-led health initiatives and nutrition labeling regulations are further accelerating adoption of sugar reduction solutions. Strong investments in innovation-driven food manufacturing and the presence of multinational food brands are enhancing market growth. Expanding product availability in supermarkets and premium retail channels continues to position the U.A.E. as the fastest-growing market in the region.

Saudi Arabia Sugar Substitute Market Insight

The Saudi Arabia market is anticipated to grow steadily from 2026 to 2033, supported by rising health awareness, increasing consumption of low-sugar food and beverage products, and strong government initiatives promoting healthier dietary habits under Vision 2030. The country is witnessing growing adoption of sugar substitutes in carbonated drinks, bakery products, and dairy applications due to increasing prevalence of diabetes and obesity. Expanding food processing industries and rising investments in modern retail infrastructure are further strengthening market accessibility. Strong presence of global ingredient manufacturers and increasing localization of food production are accelerating the use of alternative sweeteners. Continuous development of functional and fortified food products continues to support long-term market expansion across Saudi Arabia.

Middle East and Africa Sugar Substitute Market Share

The Sugar Substitute industry is primarily led by well-established companies, including:

- zuChem Inc. (U.S.)

- Ingredion (U.S.)

- BENEO (Belgium)

- Cargill, Incorporated (U.S.)

- DuPont (U.S.)

- Foodchem International Corporation (China)

- JK Sucralose Inc. (China)

- HYET Sweet (U.S.)

- Roquette Frères (France)

- Mitsui Sugar Co.,Ltd. (Japan)

- ADM (U.S.)

- Tate & Lyle (U.K.)

- Pyure Brands LLC (U.S.)

- PureCircle (Japan)

- Ajinomoto Health & Nutrition North America, Inc. (U.S.)

- NutraSweet Co. (U.S.)

- MAFCO Worldwide LLC (U.S.)

- Matsutani Chemical Industry Co., Ltd. (Japan)

Latest Developments in Middle East and Africa sugar substitute Market

- In November 2025, Cargill expanded its next-generation sweetener portfolio with new plant-based sugar reduction solutions designed for beverages and functional foods. The development strengthened the company’s position in the clean-label ingredient market while supporting rising manufacturer demand for low-calorie and naturally sourced sweetening systems. The launch is expected to accelerate innovation in sugar reduction formulations and enhance adoption across health-focused food and beverage applications

- In November 2024, Tate & Lyle completed the acquisition of CP Kelco for USD 1.8 billion to strengthen its global specialty food ingredient portfolio. The acquisition significantly enhanced the company’s capabilities in sweetening, mouthfeel, and fortification technologies, enabling broader product innovation across low-sugar and reduced-calorie food applications. This strategic expansion is expected to intensify competition and support the growing global demand for healthier ingredient solutions

- In July 2024, Roquette partnered with Bonumose to improve the commercial scalability of tagatose production for sugar alternative applications. The collaboration combined advanced enzymatic processing technology with starch-based sweetener expertise to strengthen production efficiency and expand availability of low-glycemic sweeteners. This development is expected to support rising demand for diabetic-friendly confectionery and functional food products globally

- In June 2024, Fooditive Group introduced Keto-Fructose, a sustainable sweetener produced from apple and pear waste streams to support circular economy initiatives in the food ingredients industry. The innovation highlighted the increasing industry focus on environmentally sustainable sugar substitutes while addressing consumer demand for natural and low-calorie alternatives. Ongoing FDA GRAS assessment is expected to further enhance commercial adoption opportunities across beverage and processed food markets

- In July 2023, Tate & Lyle launched TASTEVA SOL Stevia Sweetener to expand its advanced stevia-based sweetening portfolio for food and beverage manufacturers. The patented technology addressed solubility challenges associated with stevia formulations, enabling improved taste performance and formulation flexibility in sugar-reduced products. This innovation strengthened the company’s ability to support growing consumer demand for healthier, low-calorie, and naturally sweetened food products

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Middle East And Africa Sugar Substitutes Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Middle East And Africa Sugar Substitutes Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Middle East And Africa Sugar Substitutes Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.