Middle East And Africa Ventilators Market

Market Size in USD Million

USD

343.58 Million

USD

612.76 Million

2025

2033

USD

343.58 Million

USD

612.76 Million

2025

2033

| 2026 - 2033 | |

| USD 343.58 Million | |

| USD 612.76 Million | |

| % | |

|

Middle East and Africa Ventilators Market Overview

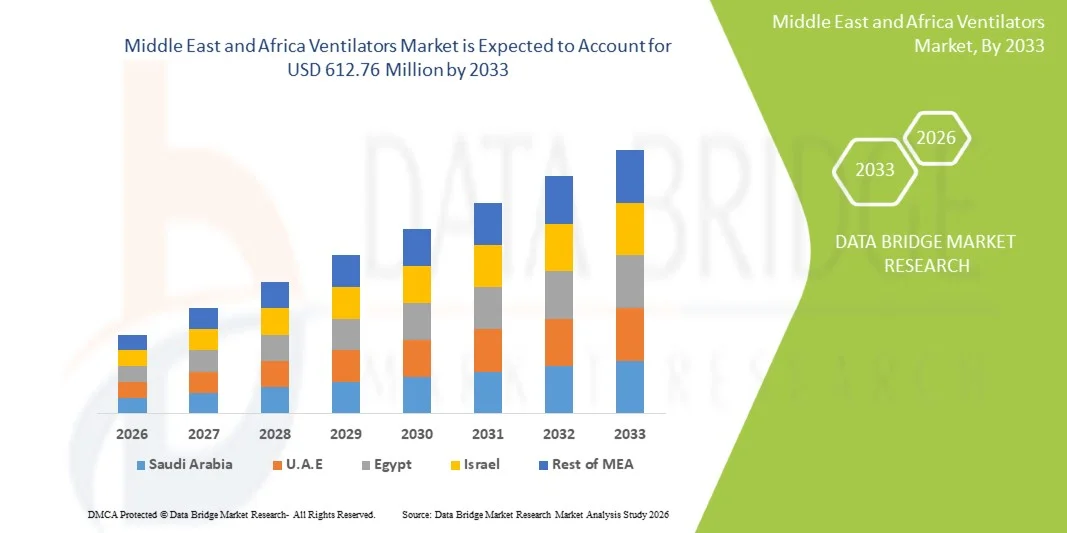

The Middle East and Africa ventilators market was valued at USD 343.58 million in 2025 and is projected to reach USD 612.76 million by 2033, growing at a CAGR of 7.50% from 2026 to 2033. The market is witnessing steady expansion driven by rising prevalence of respiratory diseases, increasing healthcare infrastructure development, and growing demand for critical care equipment across hospitals and emergency care settings.

The increasing burden of chronic respiratory conditions such as COPD, asthma, and complications arising from infectious diseases, along with a higher incidence of emergency and trauma cases, is significantly boosting the adoption of advanced ventilator systems across the region. Government investments in ICU expansion, coupled with improving access to healthcare in Gulf countries and parts of Africa, are accelerating the deployment of both invasive and non-invasive ventilators. In addition, the integration of portable, AI-enabled, and high-efficiency ventilators is further enhancing patient care outcomes in critical care environments.

Key Market Trends & Insights

- Saudi Arabia dominated the Middle East and Africa ventilators market with the largest revenue share of 36.8% in 2025, supported by advanced tertiary healthcare infrastructure, strong ICU expansion programs, and high adoption of critical care technologies.

- The Intensive Care Ventilators segment led the market with a 58.4% share in 2025, driven by high demand in ICU setups across tertiary hospitals for managing acute respiratory failure, post-surgical complications, and emergency critical care cases

- South Africa is expected to be the fastest-growing country at a strong CAGR of 8.9% from 2026 to 2033, fueled by rising healthcare investments, expanding hospital capacity, and increasing burden of chronic respiratory diseases.

- Portable Ventilators are the fastest-growing product type, projected to register a CAGR of 7.6%, reflecting the surge in demand for emergency transport, ambulatory care, and decentralized healthcare delivery.

- The Invasive Ventilation segment dominated the modality category with a 62.1% revenue share in 2025, led by its widespread use in ICUs for critically ill patients requiring full respiratory support.

- Adult accounted for 64.7% of the market, preferred by the high prevalence of chronic respiratory diseases, lifestyle-related conditions, and critical care admissions among the adult population.

- The Combined-Mode Ventilation segment is the fastest-growing mode category, with a CAGR of 8.3%, driven by its flexibility in adapting to patient-specific respiratory needs.

Market Size & Forecast

- Global Market Value (2025): USD 343.58 Million

- Expected Market Value (2033): USD 612.76 million

- Forecast CAGR (2026–2033): 7.50%

- Leading Country in 2025: Saudi Arabia

- Fastest Growing Country: South Africa

Report Scope and Middle East and Africa Ventilators Market Segmentation

|

Attributes |

Middle East and Africa Ventilators Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa |

|

Key Market Players |

· Medtronic (Ireland) · Koninklijke Philips N.V. (Netherlands) · Drägerwerk AG & Co. KGaA (Germany) · Getinge AB (Sweden) · Fisher & Paykel Healthcare Limited (New Zealand) · ResMed Inc. (U.S.) · VYAIRE MEDICAL, INC. (U.S.) · GE HealthCare (U.S.) · Smiths Group (U.K.) · Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China) · NIHON KOHDEN CORPORATION (Japan) · Air Liquide (France) · Hamilton Medical AG (Switzerland) · BPL Medical Technologies Private Limited (India) · Premier Medical Systems and Devices Pvt. Ltd. (India) · Avasarala Technologies Limited (India) · Metran Co., Ltd. (Japan) · HEYER Medical AG (Germany) · Allied Healthcare Products, Inc. (U.S.) · ZOLL Medical Corporation (U.S.) |

|

Market Opportunities |

· Rising expansion of home healthcare services · Increasing investments in rural and secondary hospital ICU infrastructure · Growing adoption of AI-enabled smart ventilators for predictive monitoring and automated respiratory management |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Middle East and Africa Ventilators Market Trends

Trend: Expansion of Critical Care Infrastructure and ICU Modernization

Healthcare providers across the Middle East and Africa are increasingly investing in advanced intensive care units and hospital modernization programs to address rising respiratory disease burdens and improve emergency response capacity. The adoption of high-performance ventilators with integrated monitoring systems and real-time patient analytics is growing rapidly, enabling clinicians to optimize respiratory support and improve treatment outcomes. Hospitals and emergency care centers are also incorporating portable and transport ventilators to strengthen pre-hospital and inter-facility care capabilities. For instance, Saudi Arabia’s hospital expansion programs and South Africa’s ICU upgrades are accelerating ventilator deployment across critical care settings.

Middle East and Africa Ventilators Market Dynamics

Key Market Driver: Rising Burden of Chronic and Infectious Respiratory Diseases

The increasing prevalence of chronic respiratory conditions such as COPD, asthma, and sleep apnea, combined with recurrent infectious disease outbreaks, is significantly driving demand for mechanical ventilators across the region. Growing geriatric populations and higher exposure to environmental pollution are further contributing to respiratory complications requiring advanced life-support systems. Governments and healthcare systems are expanding ICU capacity and investing in respiratory care technologies to manage rising patient loads effectively. For instance, Egypt’s public healthcare expansion and UAE’s critical care modernization initiatives are boosting ventilator adoption across hospitals.

Key Restraint/Challenge: High Equipment Cost and Limited Healthcare Access in Emerging Markets

A major challenge in the Middle East and Africa ventilators market is the high cost of advanced ventilator systems, which limits adoption in smaller hospitals and underfunded healthcare facilities. In addition, disparities in healthcare infrastructure and limited access to skilled critical care professionals in parts of Africa hinder effective utilization of advanced respiratory equipment. Maintenance costs, import dependency, and supply chain constraints further add to operational challenges for healthcare providers. For instance, rural healthcare facilities in Nigeria and underserved regions in Kenya continue to face barriers in acquiring and maintaining advanced ventilator systems.

Key Market Opportunity: Adoption of Portable, AI-Enabled, and Smart Ventilation Systems

The integration of smart technologies, including AI-driven ventilation modes and remote patient monitoring, presents a significant growth opportunity in the Middle East and Africa ventilators market. Increasing demand for portable and homecare ventilators is enabling decentralized respiratory care, particularly for chronic disease patients requiring long-term support. Cloud-connected and data-driven ventilators are also improving clinical decision-making and ICU efficiency across hospitals. For instance, Saudi Arabia’s adoption of smart ICU systems and South Africa’s growing home healthcare sector are driving demand for next-generation ventilator solutions.

Middle East and Africa Ventilators Market Scope

The Middle East and Africa ventilators market is segmented on the basis of product type, modality, type, mode, and end user.

- By Product Type

On the basis of product type, the Middle East and Africa ventilators market is segmented into intensive care ventilators, portable ventilators, and neonatal ventilators. The Intensive Care Ventilators segment dominated the market with a 58.4% share in 2025, driven by high demand in ICU setups across tertiary hospitals for managing acute respiratory failure, post-surgical complications, and emergency critical care cases. These ventilators are widely deployed in well-established healthcare systems in countries such as Saudi Arabia, the UAE, and Egypt due to increasing ICU bed capacity. They offer advanced monitoring, precision ventilation modes, and integration with hospital information systems, making them essential in critical care environments. Rising prevalence of chronic respiratory diseases and infectious outbreaks further strengthens their adoption. Government investments in hospital infrastructure and emergency preparedness are reinforcing segment dominance. Continuous technological upgrades such as AI-assisted ventilation are improving patient outcomes and efficiency in ICU management.

The Portable Ventilators segment is expected to register the fastest growth at a CAGR of 7.6% from 2026 to 2033, driven by rising demand for emergency transport, ambulatory care, and decentralized healthcare delivery. These devices are increasingly used in ambulances, inter-hospital transfers, and homecare settings due to their compact design and ease of use. Growing emphasis on emergency medical services and disaster response readiness is accelerating adoption across countries such as Saudi Arabia, South Africa, and Nigeria. Improvements in battery life, device miniaturization, and wireless monitoring capabilities are enhancing usability. Expanding home healthcare trends for chronic respiratory patients are further supporting demand. Increasing investments in pre-hospital care infrastructure are also boosting market growth across the region.

- By Modality

On the basis of modality, the market is segmented into invasive ventilation and non-invasive ventilation. The Invasive Ventilation segment dominated the market with a 62.1% share in 2025, due to its widespread use in ICUs for critically ill patients requiring full respiratory support. It is extensively used in cases of severe respiratory failure, trauma, and post-operative care across major hospitals in Saudi Arabia, the UAE, and Egypt. These systems allow precise control of oxygen delivery, ventilation pressure, and patient monitoring, making them essential in life-support situations. High ICU admission rates and growing surgical volumes are reinforcing demand. Strong hospital infrastructure development across Gulf countries is further supporting adoption. Continuous improvements in ventilator safety features and monitoring systems are enhancing clinical reliability.

The Non-Invasive Ventilation segment is expected to grow at the fastest CAGR of 8.1% from 2026 to 2033, driven by increasing preference for patient-friendly respiratory support and reduced risk of ventilator-associated infections. It is widely used in emergency care, sleep apnea management, and chronic respiratory disease treatment. Growing adoption in homecare settings and ambulatory care centers is further accelerating expansion. Countries such as South Africa, Saudi Arabia, and Kenya are witnessing rising usage due to improving healthcare accessibility. Technological advancements in mask interfaces and pressure support systems are enhancing patient comfort and compliance. Expanding awareness of early respiratory intervention is also boosting demand.

- By Type

On the basis of type, the market is segmented into adult, paediatric, and neonatal ventilators. The Adult Ventilators segment dominated the market with a 64.7% share in 2025, driven by the high prevalence of chronic respiratory diseases, lifestyle-related conditions, and critical care admissions among the adult population. These ventilators are widely used in ICUs, emergency departments, and post-operative recovery units across hospitals in Saudi Arabia, Egypt, and the UAE. Rising incidence of COPD, asthma, and infectious respiratory diseases is further increasing demand. Strong hospital infrastructure and ICU expansion projects are reinforcing dominance. Continuous improvements in ventilation modes and monitoring accuracy are enhancing clinical effectiveness. Government initiatives to improve critical care capacity are also supporting adoption.

The Neonatal Ventilators segment is expected to register the fastest growth at a CAGR of 7.9% from 2026 to 2033, driven by increasing focus on neonatal intensive care and rising incidence of premature births. These ventilators are critical in NICUs for supporting underdeveloped lungs in newborns requiring respiratory assistance. Expanding maternal and child healthcare programs in countries such as Saudi Arabia, South Africa, and the UAE are boosting demand. Technological advancements in gentle ventilation and non-invasive neonatal support systems are improving survival rates. Increasing hospital investments in specialized NICU infrastructure is further supporting growth. Rising awareness of neonatal care standards is also contributing to adoption.

- By Mode

On the basis of mode, the market is segmented into combined-mode ventilation, volume-mode ventilation, pressure-mode ventilation, and others. The Volume-Mode Ventilation segment dominated the market with a 39.8% share in 2025, owing to its widespread use in ICUs for delivering consistent tidal volume regardless of lung compliance changes. It is highly preferred in critical care settings across major hospitals in Saudi Arabia, Egypt, and the UAE due to its reliability and precision. This mode is essential for managing patients with unstable respiratory conditions requiring controlled ventilation. Integration with advanced monitoring systems enhances safety and clinical control. Increasing ICU admissions and surgical procedures are further driving adoption. Continuous software improvements are enhancing ventilator responsiveness and efficiency.

The Combined-Mode Ventilation segment is expected to grow at the fastest CAGR of 8.3% from 2026 to 2033, driven by its flexibility in adapting to patient-specific respiratory needs. It combines advantages of both pressure and volume control, making it suitable for complex ICU cases. Rising demand for personalized ventilation strategies in critical care is accelerating adoption. Hospitals in Saudi Arabia, South Africa, and the UAE are increasingly integrating advanced ventilators with adaptive ventilation modes. Technological advancements in AI-driven ventilation adjustments are further supporting growth. Expanding critical care infrastructure and rising awareness of lung-protective ventilation strategies are boosting demand.

- By End User

On the basis of end user, the market is segmented into hospitals and clinics, home care, ambulatory centres, specialty clinics, rehabilitation centres, long-term care centres, homecare settings, and others. The Hospitals and Clinics segment dominated the market with a 65.2% share in 2025, driven by high concentration of ICU facilities, emergency departments, and surgical units requiring continuous ventilatory support. These institutions represent the primary deployment centers for advanced ventilators across Saudi Arabia, the UAE, and Egypt. Strong government investment in healthcare infrastructure is supporting expansion of critical care capacity. Increasing patient inflow due to respiratory diseases and trauma cases is further reinforcing demand. Availability of skilled healthcare professionals enhances effective ventilator utilization. Continuous upgrades in hospital equipment and ICU modernization programs are strengthening this segment.

The Homecare Settings segment is expected to register the fastest growth at a CAGR of 8.5% from 2026 to 2033, driven by rising demand for long-term respiratory support outside hospital environments. Increasing prevalence of chronic respiratory diseases and aging populations is fueling adoption of home-based ventilator solutions. Countries such as South Africa, Saudi Arabia, and Kenya are witnessing growing investment in home healthcare infrastructure. Technological advancements in portable and user-friendly ventilators are improving patient independence. Cost-effective long-term care solutions are encouraging shift from hospital to home settings. Expanding awareness of home-based chronic care management is further accelerating growth.

Middle East and Africa Ventilators Market Regional Analysis

Saudi Arabia dominated the Middle East and Africa ventilators market with the largest revenue share of 36.8% in 2025, supported by advanced tertiary healthcare infrastructure, strong ICU expansion programs, and high adoption of critical care technologies. The country also benefits from rising prevalence of chronic respiratory diseases, increasing surgical volumes, and strong adoption of advanced critical care technologies across public and private hospitals. Expanding emergency response systems, continuous modernization of healthcare facilities, and integration of smart ventilator systems further reinforce Saudi Arabia’s leadership position in the regional market.

The Saudi Arabia Ventilators Market Insight

The Saudi Arabia ventilators market is witnessing strong growth due to rising investments in advanced critical care infrastructure, expanding ICU capacity, and government-led healthcare modernization programs. The country’s well-developed hospital network, along with increasing prevalence of respiratory diseases and strong demand for emergency care services, is driving adoption of invasive and portable ventilators. In addition, growing integration of smart ICU systems, AI-enabled respiratory support devices, and increased focus on emergency preparedness is accelerating ventilator demand across public and private healthcare facilities.

UAE Ventilators Market Insight

The UAE ventilators market is experiencing steady expansion, supported by advanced healthcare infrastructure, high adoption of cutting-edge medical technologies, and strong investment in hospital digitization. The country’s focus on world-class critical care services, coupled with rising cases of chronic respiratory conditions and post-surgical complications, is boosting ventilator usage in ICUs and emergency departments. Furthermore, increasing deployment of portable ventilators in ambulatory care and emergency transport systems is strengthening market growth across the healthcare ecosystem.

South Africa Ventilators Market Insight

The South Africa ventilators market is growing at a strong pace, driven by increasing healthcare investments, rising burden of respiratory diseases, and expansion of public and private hospital infrastructure. Limited ICU capacity in certain regions is encouraging procurement of both invasive and non-invasive ventilators to improve critical care access. In addition, growing adoption of homecare ventilators for chronic respiratory patients and increasing government focus on healthcare modernization are further supporting market expansion across the country.

Egypt Ventilators Market Insight

The Egypt ventilators market is expanding steadily due to rising demand for critical care equipment, increasing hospital admissions for respiratory illnesses, and government initiatives to strengthen healthcare infrastructure. Growing investments in ICU development across public hospitals, along with rising prevalence of infectious respiratory diseases, are driving ventilator adoption. Moreover, increasing use of cost-effective invasive ventilators and gradual integration of modern respiratory support systems are contributing to market growth.

Middle East and Africa Ventilators Market Share

The Middle East and Africa Ventilators industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Koninklijke Philips N.V. (Netherlands)

- Drägerwerk AG & Co. KGaA (Germany)

- Getinge AB (Sweden)

- Fisher & Paykel Healthcare Limited (New Zealand)

- ResMed Inc. (U.S.)

- VYAIRE MEDICAL, INC. (U.S.)

- GE HealthCare (U.S.)

- Smiths Group (U.K.)

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China)

- NIHON KOHDEN CORPORATION (Japan)

- Air Liquide (France)

- Hamilton Medical AG (Switzerland)

- BPL Medical Technologies Private Limited (India)

- Premier Medical Systems and Devices Pvt. Ltd. (India)

- Avasarala Technologies Limited (India)

- Metran Co., Ltd. (Japan)

- HEYER Medical AG (Germany)

- Allied Healthcare Products, Inc. (U.S.)

- ZOLL Medical Corporation (U.S.)

Latest Developments in Middle East and Africa Ventilators Market

- In May 2025, global ventilator manufacturers expanded production and distribution networks to meet rising demand across Middle East and Africa healthcare systems, particularly for ICU and portable ventilators. Companies such as Getinge and other critical care equipment providers increased supply capacity to support hospital expansion projects and emergency care requirements

- In January 2024, Response Plus Medical, a leading emergency medical services provider in the Middle East, expanded its critical care and ambulance support network across Saudi Arabia and the UAE, enhancing ventilator-equipped emergency response systems. The expansion included deployment of advanced ICU-equipped ambulances capable of providing mechanical ventilation support during patient transport

- In September 2023, South Africa increased procurement of mechanical ventilators to strengthen ICU capacity in public hospitals, supported by government healthcare improvement programs. The initiative aimed to address rising respiratory disease burden and limited critical care infrastructure in several regions

- In July 2022, Saudi Arabia accelerated ICU expansion and modernization programs under its national healthcare transformation initiative, significantly increasing procurement of advanced ventilators in public hospitals. The initiative focused on strengthening intensive care capacity and upgrading respiratory support systems across major tertiary hospitals. Procurement included modern invasive ventilators to improve management of respiratory failure and post-operative care

- In March 2021, the United Arab Emirates expanded ICU infrastructure across major hospitals, increasing the deployment of advanced non-invasive and invasive ventilators in both public and private healthcare facilities. The expansion was driven by post-pandemic healthcare strengthening initiatives aimed at improving respiratory care capacity

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.