Middle East And Africa Womens Health Diagnostics Market

Market Size in USD Million

USD

834.22 Million

USD

1,631.98 Million

2025

2033

USD

834.22 Million

USD

1,631.98 Million

2025

2033

| 2026 - 2033 | |

| USD 834.22 Million | |

| USD 1,631.98 Million | |

| % | |

|

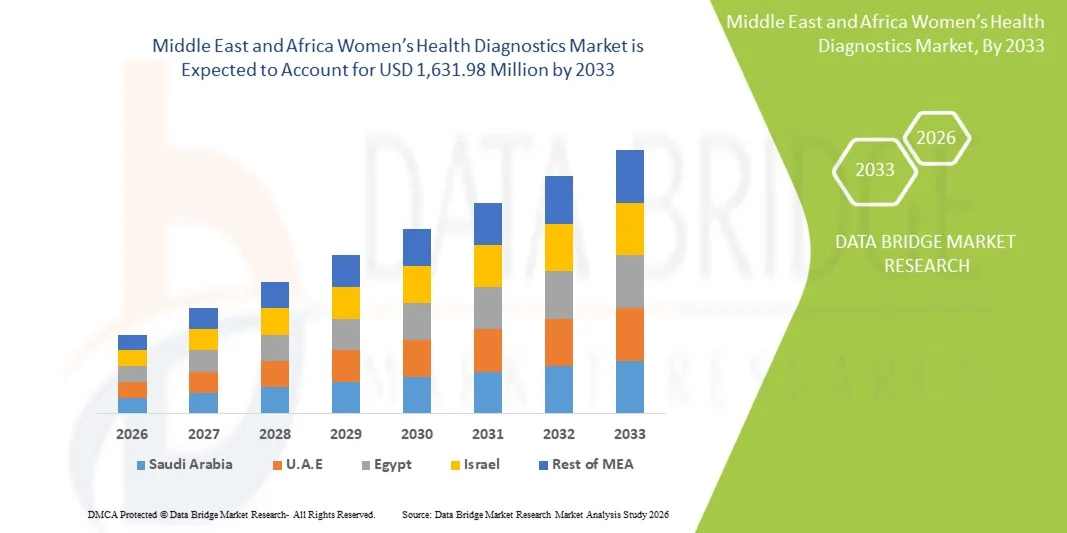

Middle East and Africa Women’s Health Diagnostics Market Size

- The Middle East and Africa women’s health diagnostics market size was valued at USD 834.22 million in 2025 and is expected to reach USD 1,631.98 million by 2033, at a CAGR of 8.75% during the forecast period

- The market growth is largely fueled by increasing awareness of women’s health issues, rising prevalence of gynecological disorders, and advancements in diagnostic technologies, driving the adoption of modern diagnostic solutions across the region

- Furthermore, growing government initiatives, healthcare infrastructure development, and rising consumer preference for early detection and personalized care are positioning women’s health diagnostics as an essential segment within healthcare services. These converging factors are accelerating the uptake of diagnostic solutions, thereby significantly boosting the market’s growth

Middle East and Africa Women’s Health Diagnostics Market Analysis

- Women’s health diagnostics, encompassing tests and technologies for gynecological, reproductive, and hormonal health, are increasingly critical in improving healthcare outcomes for women across both urban and rural areas due to their role in early disease detection, personalized care, and preventive health management

- The escalating demand for women’s health diagnostics is primarily fueled by rising awareness of women-specific health issues, increasing prevalence of reproductive and hormonal disorders, and growing preference for early detection and minimally invasive testing methods

- Saudi Arabia dominated the market with the largest revenue share of 38.5% in 2025, characterized by improving healthcare infrastructure, government initiatives supporting women’s health, and the presence of leading diagnostic service providers, with substantial adoption of advanced diagnostic solutions in private clinics and specialized women’s health centers

- Nigeria is expected to be the fastest-growing country in the women’s health diagnostics market during the forecast period due to rising healthcare accessibility, urbanization, and increasing government and NGO-led awareness programs

- Cervical cancer testing segment dominated the market with a share of 42.2% in 2025, driven by high prevalence of cervical cancer, increasing government-led screening programs, and growing adoption of advanced diagnostic technologies in hospitals, diagnostic centers, and clinics

Report Scope and Middle East and Africa Women’s Health Diagnostics Market Segmentation

|

Attributes |

Middle East and Africa Women’s Health Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Middle East and Africa Women’s Health Diagnostics Market Trends

“Expansion of AI-Enabled and Home-Based Diagnostic Solution”

- A significant and accelerating trend in the Middle East and Africa women’s health diagnostics market is the rapid integration of artificial intelligence (AI) and digitally enabled home-based diagnostic tools, enhancing accuracy, accessibility, and diagnostic convenience for women across diverse population groups

- For instance, AI-driven breast cancer screening platforms are being adopted in countries such as the UAE and Saudi Arabia, enabling faster image analysis and improved detection compared to traditional radiology workflows

- AI-powered diagnostic systems are also supporting early detection in areas such as cervical cancer, fertility analysis, and prenatal risk screening, with smart algorithms helping clinicians interpret complex data more efficiently and improving outcomes; for instance, several regional healthcare providers now employ AI-enhanced colposcopy imaging for more precise cervical assessments

- The growing availability of digital home testing devices for pregnancy, ovulation tracking, and infectious disease detection is increasing user convenience, supporting remote monitoring, and expanding access for underserved populations

- This shift toward intelligent, automated, and patient-centric diagnostic solutions is reshaping expectations for women’s healthcare across the region, encouraging companies to invest in connected diagnostic devices and mobile-enabled platforms tailored for women’s health

- The demand for AI-integrated and home-based women’s health diagnostic systems is rising rapidly across both developed and emerging markets within MEA, as consumers increasingly prioritize convenience, accuracy, and personalized testing options

- A growing focus on telehealth and remote consultations is further supporting the adoption of digital diagnostic tools, enabling women to receive clinical guidance without the need for frequent hospital visits

- For instance, several telemedicine platforms in the UAE and South Africa now offer integrated women’s health diagnostic services, allowing seamless data sharing between home devices and healthcare providers

Middle East and Africa Women’s Health Diagnostics Market Dynamics

Driver

“Growing Demand Due to Rising Women’s Health Awareness and Advances in Screening Technologies”

- The increasing awareness of women-specific health issues, combined with the rising prevalence of breast cancer, cervical cancer, infertility, and sexually transmitted diseases, is a major driver accelerating the adoption of women’s health diagnostics across MEA

- For instance, in 2025, Saudi Arabia expanded national breast cancer awareness and screening programs, incorporating advanced digital mammography systems to strengthen early detection efforts

- As women become more informed about preventive healthcare, there is growing demand for routine screening, fertility assessments, and prenatal testing, driving the uptake of modern diagnostic technologies

- Furthermore, improvements in healthcare infrastructure across the UAE, Saudi Arabia, South Africa, and Nigeria are increasing access to advanced imaging centers, laboratories, and women’s specialty clinics

- The convenience of early-detection tools, digital screening platforms, and improved diagnostic accuracy is further propelling the adoption of women’s health diagnostics in both public and private healthcare settings

- The increasing affordability of diagnostic procedures and government-led awareness campaigns is expected to further strengthen market growth across the forecast period

- Rapid urbanization and rising healthcare expenditures in emerging economies such as Kenya and Ghana are expanding patient access to modern diagnostic services

- For instance, new private diagnostic centers equipped with ultrasound and molecular testing technologies have opened across major African cities, boosting availability of women’s health tests

Restraint/Challenge

“Limited Access to Advanced Diagnostics and Regulatory Compliance Hurdles”

- Restricted availability of advanced diagnostic equipment and skilled medical professionals in several African countries presents a significant barrier to widespread adoption of women’s health diagnostics

- For instance, many regions still lack adequate screening infrastructure for cervical cancer, limiting early detection and contributing to higher mortality rates

- In addition, regulatory delays associated with the approval of diagnostic devices and laboratory equipment can slow market entry for global manufacturers, affecting innovation uptake

- High testing costs for advanced procedures such as prenatal genetic screening or digital breast imaging can also restrict access for price-sensitive populations across developing markets

- Moreover, limited awareness regarding the importance of routine diagnostic testing, combined with cultural barriers in certain regions, can hinder the adoption of women’s health solutions

- Overcoming these challenges through regulatory streamlining, broader insurance coverage, public health education, and expansion of low-cost diagnostic solutions will be essential for sustained market growth

- Infrastructure limitations such as inconsistent electricity supply and lack of laboratory automation systems further constrain the reliability and scalability of diagnostic services in rural areas

- For instance, several healthcare facilities in sub-Saharan Africa still rely on manual diagnostic processes, resulting in delayed results and reduced testing capacity

Middle East and Africa Women’s Health Diagnostics Market Scope

The market is segmented on the basis of application and end user.

- By Application

On the basis of application, the Middle East and Africa women’s health diagnostics market is segmented into osteoporosis testing, OVC testing, cervical cancer testing, breast cancer testing, pregnancy and fertility testing, prenatal genetic screening and carrier testing, infectious disease testing, STD testing, and ultrasound tests. The cervical cancer testing segment dominated the market with the largest market revenue share of 42.2% in 2025, driven by the high prevalence of cervical cancer and strong government-led screening programs across Saudi Arabia, South Africa, Kenya, and the UAE. The adoption of Pap smears, HPV DNA testing, and AI-supported colposcopy tools has expanded rapidly, improving early detection rates across both urban and semi-urban regions. International health organizations and national ministries of health continue to promote mass-screening initiatives, raising awareness and encouraging routine testing among women of reproductive age. Investments in diagnostic infrastructure and mobile screening units have further strengthened access in underserved areas. Hospitals and diagnostic centers are increasingly integrating advanced molecular assays, expanding the overall testing capacity. As early screening becomes a regional public health priority, cervical cancer testing is expected to maintain its dominant position across the MEA market.

The prenatal genetic screening and carrier testing segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising maternal age, growing demand for early detection of chromosomal abnormalities, and wider availability of non-invasive prenatal testing (NIPT) in major MEA countries. Increasing access to advanced genomic and sequencing technologies is strengthening adoption in private maternity centers and fertility clinics. Urban populations across the UAE, Qatar, Kuwait, and South Africa are increasingly seeking personalized maternity care, including expanded genetic screening panels. The rise in assisted reproductive technology (ART) procedures further supports the demand for genetic and carrier screening. Strategic collaborations between regional hospitals and global genomics companies are making these tests more accessible and affordable. As awareness of inherited conditions improves, prenatal genetic screening continues to gain rapid momentum across the region.

- By End User

On the basis of end user, the Middle East and Africa women’s health diagnostics market is segmented into hospitals, diagnostic and imaging centers, clinics, and home care settings. The hospitals segment dominated the market with the largest market revenue share in 2025, driven by high patient volumes, strong diagnostic infrastructure, and the presence of multidisciplinary women’s health departments. Hospitals across Saudi Arabia, the UAE, Egypt, and South Africa are equipped with advanced imaging modalities such as ultrasound, mammography, CT, MRI, and colposcopy systems, enabling comprehensive diagnostic services. Government investments in public hospitals and specialized women’s healthcare programs are improving access to screening services. Hospitals are also preferred for complex diagnostic procedures, including prenatal genetic analysis, infectious disease testing, and oncology-related diagnostics. The availability of skilled radiologists, gynecologists, and laboratory personnel strengthens the clinical reliability of hospital-based diagnostics. Their ability to manage emergencies, follow-up care, and integrated testing ensures continued dominance in the MEA market.

The home care setting segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by the rising adoption of home-based pregnancy tests, ovulation trackers, self-administered infectious disease kits, and digital fertility monitoring devices. Increasing use of smartphones, telehealth platforms, and remote monitoring tools is enabling women to conduct tests at home and share results electronically with healthcare providers. Growing preference for privacy, convenience, and reduced hospital visits is making home diagnostics increasingly popular, particularly among working women and younger demographics. Affordable and accurate self-testing kits are becoming widely available in markets such as the UAE, Saudi Arabia, and South Africa. AI-enabled fertility wearables and connected maternal health devices are expanding the scope of home-based diagnostics. As consumer acceptance of remote healthcare continues to rise, this segment is expected to demonstrate the quickest expansion across MEA.

Middle East and Africa Women’s Health Diagnostics Market Regional Analysis

- Saudi Arabia dominated the market with the largest revenue share of 38.5% in 2025, characterized by improving healthcare infrastructure, government initiatives supporting women’s health, and the presence of leading diagnostic service providers, with substantial adoption of advanced diagnostic solutions in private clinics and specialized women’s health centers

- Consumers and patients in Saudi Arabia increasingly prioritize high-quality diagnostic services, supported by rising awareness initiatives, improved insurance coverage, and the availability of technologically advanced imaging and molecular testing solutions across hospitals and specialized diagnostic centers

- The market’s growth is further strengthened by Saudi Arabia’s growing female workforce participation, expanding private healthcare sector, and significant adoption of digital health platforms, positioning the country as the leading hub for women’s health diagnostics within the Middle East and Africa region

The Saudi Arabia Women’s Health Diagnostics Market Insight

Saudi Arabia captured the largest revenue share in the Middle East and Africa women’s health diagnostics market in 2025, driven by nationwide healthcare modernization and the rapid deployment of advanced diagnostic technologies. The country’s strong focus on breast cancer screening, cervical cancer testing, and fertility diagnostics has significantly boosted adoption rates across public and private healthcare facilities. Rising health awareness among women, coupled with expanding insurance coverage and government-led early detection programs, continues to strengthen market growth. The increasing penetration of digital health platforms, AI-based imaging tools, and molecular diagnostics further enhances diagnostic accuracy and accessibility. Saudi Arabia’s growing female workforce participation and expanding network of specialized diagnostic centers position it as the leading hub for women’s health diagnostics in the region.

United Arab Emirates Women’s Health Diagnostics Market Insight

The UAE women’s health diagnostics market is projected to grow at a substantial CAGR throughout the forecast period, supported by world-class healthcare infrastructure and strong government initiatives focused on women’s preventive care. Increasing awareness of breast cancer, cervical cancer, and prenatal screening drives high adoption of advanced imaging and molecular diagnostic tools. The UAE’s rapidly urbanizing population, combined with rising lifestyle-related diseases, accelerates demand for early diagnosis and regular health checkups. The presence of technologically advanced hospitals and diagnostic chains further fuels innovation in reproductive health and genetic testing. In addition, the UAE’s focus on medical tourism continues to attract international patients seeking high-quality women’s health diagnostics.

South Africa Women’s Health Diagnostics Market Insight

The South Africa women’s health diagnostics market is anticipated to expand at a noteworthy CAGR, driven by the growing burden of infectious diseases, reproductive health disorders, and cancers among women. The country’s emphasis on improving public healthcare access and strengthening diagnostic capabilities plays a crucial role in market acceleration. Increasing government and NGO awareness programs for breast cancer, cervical cancer, and STD testing promote early detection and screening participation. South Africa’s expanding private diagnostic sector, supported by investments in imaging centers and molecular labs, is boosting the adoption of advanced tools. Furthermore, rising interest in home-based pregnancy and fertility test kits contributes to market growth, particularly in urban areas.

Nigeria Women’s Health Diagnostics Market Insight

Nigeria is expected to register considerable growth during the forecast period, driven by increasing awareness of maternal health, infectious disease screening, and reproductive health diagnostics. Despite infrastructural challenges, rising investments in diagnostic centers and mobile health solutions enhance accessibility for women across both urban and semi-urban regions. Government programs targeting cervical cancer screening, STD testing, and prenatal care are improving diagnostic coverage. Nigeria’s large population and high birth rates also fuel strong demand for pregnancy, fertility, and ultrasound testing. The growing role of private healthcare providers and NGOs in women’s health further supports the adoption of modern diagnostic tools across the country.

Middle East and Africa Women’s Health Diagnostics Market Share

The Middle East and Africa Women’s Health Diagnostics industry is primarily led by well-established companies, including:

- F. Hoffmann-La Roche Ltd (Switzerland)

- Abbott (U.S.)

- Siemens Healthineers AG (Germany)

- Thermo Fisher Scientific Inc. (U.S.)

- BD (U.S.)

- BIOMÉRIEUX (France)

- Illumina, Inc. (U.S.)

- PerkinElmer (U.S.)

- DIASORIN S.p.A. (Italy)

- Myriad Genetics, Inc. (U.S.)

- NIPD Genetics Ltd (Cyprus)

- Randox Laboratories Ltd (U.K.)

- QuidelOrtho (QuidelOrtho) (U.S.)

- Sysmex Corporation (Japan)

- Omega Diagnostics (U.K.)

- BGI Group (China)

- Eurofins Scientific SE (Luxembourg)

- Seegene Inc. (South Korea)

- Menarini Group (Italy)

- Promega Corporation (U.S.)

What are the Recent Developments in Middle East and Africa Women’s Health Diagnostics Market?

- In November 2025, Ethiopia’s Ministry of Health, with support from WHO and multiple partners, initiated a large-scale national campaign to deliver cervical cancer screening and treatment across six regions. The program combined facility-based services with mobile outreach units, ensuring women in remote and rural locations could receive VIA screening and follow-up care. This effort aligns with WHO’s cervical cancer elimination framework and strengthens diagnostic coverage across the country

- In October 2024, BD Africa launched a high-throughput molecular PCR genotyping device designed specifically to strengthen HPV screening across African countries. The platform supports extended HPV genotyping, enabling more precise identification of high-risk strains responsible for cervical cancer. It also accepts self-collected vaginal samples, expanding access for women in rural or resource-limited settings. This development aims to significantly enhance diagnostic capacity across national screening programs and accelerate early detection efforts

- In May 2024, the Global Alliance for Women’s Health, backed by Siemens Healthineers, formed a new “Cervical and Breast Cancer Coalition” during a high-level global health meeting in Kenya. The coalition aims to accelerate early detection, strengthen diagnostic infrastructure, and support capacity-building among healthcare workers. With a focus on both breast and cervical cancers, the initiative addresses two of the region’s most critical women’s health challenges

- In June 2023, Zulekha Healthcare Group introduced its “Chance to Change” campaign in the UAE, offering free cervical cancer screening, HPV vaccinations, and gynecology consultations. Conducted across Dubai and Sharjah, the initiative aimed to reduce screening gaps among women and promote early detection. By combining public awareness, preventive vaccinations, and diagnostic access, the program strengthened regional efforts toward lowering cervical cancer incidence

- In March 2023, FIND and KILELE Health Association launched a community-based coalition in sub-Saharan Africa focused on scaling cervical cancer screening. The initiative works to identify social, cultural, and healthcare system barriers, improve diagnostic uptake, and support community-level education. By expanding screening accessibility and improving care pathways, the program aims to reduce preventable cervical cancer mortality across underserved regions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.