North America Ablation Devices Market

Market Size in USD Billion

USD

2.79 Billion

USD

6.24 Billion

2024

2032

USD

2.79 Billion

USD

6.24 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.79 Billion | |

| USD 6.24 Billion | |

| % | |

|

North America Ablation Devices Market Size

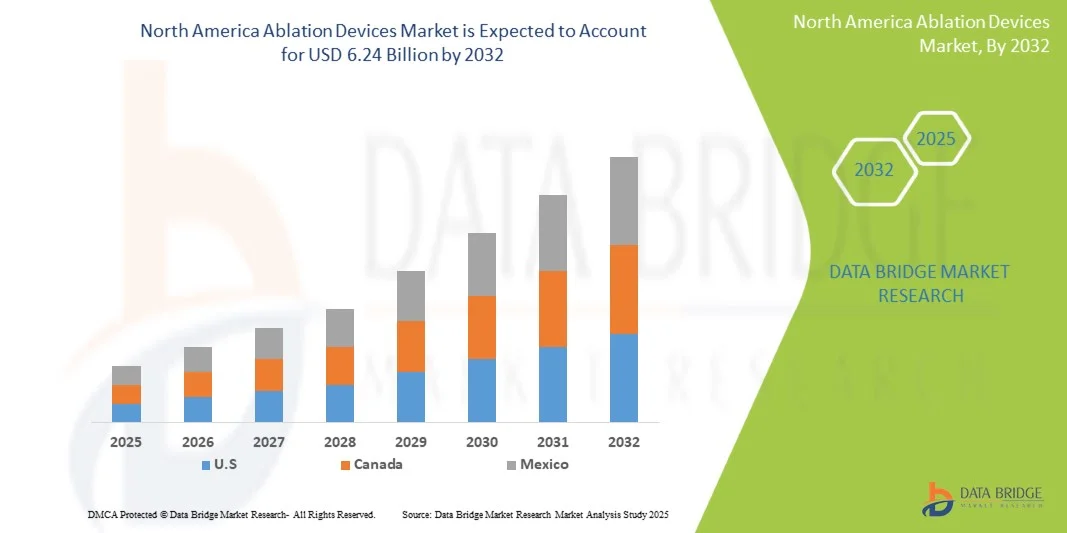

- The North America Ablation Devices Market size was valued at USD 2.79 billion in 2024 and is expected to reach USD 6.24 billion by 2032, at a CAGR of 10.55% during the forecast period

- The market growth is largely fueled by the increasing prevalence of chronic diseases, particularly cardiac arrhythmias, cancer, and urological disorders, which drive the demand for precise and minimally invasive treatment options

- Furthermore, technological advancements in ablation devices, including radiofrequency, cryoablation, laser, and high-intensity focused ultrasound systems, are enabling improved procedural efficiency, safety, and patient outcomes

North America Ablation Devices Market Analysis

- Ablation devices, offering minimally invasive treatment solutions for cardiac arrhythmias, tumors, and other medical conditions, are increasingly vital components of modern healthcare systems in both hospitals and specialty clinics due to their enhanced precision, safety, and efficacy

- The escalating demand for ablation devices is primarily fueled by the rising prevalence of cardiovascular and oncological diseases, increasing adoption of minimally invasive procedures, and continuous technological advancements in ablation therapies

- U.S. dominated the North America Ablation Devices Market with the largest revenue share of 82.3% in 2024, driven by advanced healthcare infrastructure, growing awareness among clinicians and patients, and a strong presence of leading market players. The country witnessed substantial growth in ablation device installations across hospitals and specialty clinics, particularly in cardiac and tumor ablation procedures, supported by continuous innovations from both established companies and emerging startups

- Canada is expected to witness the fastest growth in the North America Ablation Devices Market, with a projected CAGR of 8.9% from 2025 to 2032, fueled by rising adoption of minimally invasive procedures, increasing awareness of ablation therapies, and expanding healthcare infrastructure in urban and semi-urban regions

- The Thermal Ablation segment dominated the North America Ablation Devices Market with a revenue share of 62.5% in 2024, driven by its wide clinical adoption in oncology, cardiology, urology, and aesthetics

Report Scope and North America Ablation Devices Market Segmentation

|

Attributes |

North America Ablation Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

North America Ablation Devices Market Trends

“Rising Demand for Minimally Invasive and Technology-Driven Procedures”

- A significant and accelerating trend in the North America Ablation Devices Market is the increasing adoption of minimally invasive and image-guided procedures, which enhance precision, reduce recovery times, and improve patient outcomes

- For instance, advanced tumor ablation systems and cardiac ablation technologies are being integrated with real-time imaging platforms such as ultrasound, CT, and MRI, enabling physicians to accurately target affected tissues while minimizing damage to surrounding areas

- Integration with robotic-assisted and automated systems in ablation procedures allows for more consistent and precise energy delivery, improving procedural efficiency and reducing the risk of complications

- These advancements enable hospitals and specialized clinics to offer a wider range of treatments, including tumor ablation, cardiac arrhythmia management, and varicose vein therapy, with improved safety and efficacy

- The trend toward more precise, technology-enabled procedures is fundamentally reshaping clinical expectations, with healthcare providers increasingly prioritizing systems that combine reliability, safety, and procedural versatility

- Consequently, leading ablation device manufacturers are developing next-generation platforms that support multi-modality imaging, robotic guidance, and customizable ablation protocols to meet the growing demand across both hospital and outpatient settings

- The demand for advanced ablation devices is growing rapidly across oncology, cardiology, urology, and aesthetics procedures, as medical facilities aim to improve patient outcomes while optimizing workflow efficiency

North America Ablation Devices Market Dynamics

Driver

“Growing Need Due to Rising Prevalence of Cardiovascular and Oncological Disorders”

- The increasing prevalence of cardiovascular diseases, arrhythmias, and cancer, coupled with the rising preference for minimally invasive treatment options, is a significant driver for the heightened demand for ablation devices

- For instance, in April 2024, Medtronic announced the launch of its next-generation cardiac ablation system, designed to enhance precision, reduce procedure time, and improve patient safety. Such innovations by leading companies are expected to drive Ablation Devices industry growth during the forecast period

- As healthcare providers seek safer and more efficient treatment modalities, ablation devices offer advanced features such as real-time imaging guidance, automated energy delivery, and targeted tissue ablation, providing superior clinical outcomes compared to conventional surgical approaches

- Furthermore, the growing adoption of minimally invasive procedures and the integration of ablation systems with diagnostic imaging and monitoring platforms are making these devices essential components of modern clinical workflows

- The convenience of reduced hospital stays, faster patient recovery, and lower procedural risks are key factors propelling the adoption of ablation devices in both hospitals and specialty clinics. The trend towards advanced, patient-friendly device designs and the increasing availability of innovative Ablation Devices options further contribute to market growth

Restraint/Challenge

“Concerns Regarding High Costs and Procedural Complexity”

- The relatively high cost of advanced ablation devices, along with the need for specialized training for clinicians, poses a challenge to broader market penetration. High initial capital investment can be a barrier, especially for smaller hospitals or clinics with limited budgets

- For instance, complex cardiac and oncological ablation systems often require additional imaging and monitoring equipment, which can increase overall procedural costs and limit adoption in cost-sensitive regions

- Addressing these challenges through simplified device designs, clinician training programs, and cost-effective solutions is crucial for expanding market reach. Leading companies such as Boston Scientific and Abbott are continuously developing more intuitive and user-friendly ablation platforms to improve adoption

- While prices for some devices are gradually decreasing, the perceived premium for cutting-edge technology can still hinder widespread adoption, particularly in regions with constrained healthcare spending

- Overcoming these challenges through innovations in device affordability, enhanced procedural efficiency, and educational initiatives for healthcare providers will be vital for sustained growth in the North America Ablation Devices Market

- Regulatory hurdles and stringent compliance requirements in different countries can delay product approvals and market entry, limiting the speed of adoption and expansion for new ablation technologies

- Limited awareness among patients regarding the benefits of ablation procedures compared to conventional surgery can reduce procedure volumes, particularly in emerging markets where minimally invasive technologies are still gaining traction

North America Ablation Devices Market Scope

The market is segmented on the basis of technology, function, procedure, and application.

• By Technology

On the basis of technology, the North America Ablation Devices Market is segmented into thermal ablation and non-thermal ablation. The thermal ablation segment dominated the market with a revenue share of 62.5% in 2024, driven by its wide clinical adoption in oncology, cardiology, urology, and aesthetics. Thermal ablation techniques such as radiofrequency, microwave, and laser-based ablation provide precise energy delivery, predictable outcomes, and minimal invasiveness. Hospitals and outpatient centers prefer thermal ablation due to its ability to reduce patient recovery times and post-procedural complications. Advancements in imaging guidance, robotic integration, and real-time monitoring further support adoption. The segment benefits from high procedural efficiency and reproducibility across multiple specialties. Strong physician familiarity, extensive clinical data, and cost-effectiveness compared to emerging techniques solidify its dominance.

The Non-Thermal Ablation segment is expected to witness the fastest CAGR of 8.1% from 2025 to 2032, driven by increasing use in delicate procedures where heat may damage surrounding tissues, including nerve modulation, ophthalmology, and certain cardiac interventions. Techniques such as cryoablation, irreversible electroporation, and pulsed field ablation are gaining popularity due to safety, minimal invasiveness, and rapid patient recovery. Expanding indications, growing awareness among clinicians, and technological improvements in energy delivery and imaging integration are fueling adoption. The rise of personalized treatment protocols and minimally invasive approaches in specialty clinics supports rapid growth.

• By Function

On the basis of function, the North America Ablation Devices Market is segmented into automated/robotic and conventional. The Conventional segment dominated with a revenue share of 58.3% in 2024, supported by its widespread acceptance in routine hospital and outpatient procedures. Conventional devices are valued for their reliability, lower upfront costs, and compatibility with existing clinical workflows. Hospitals and surgical centers continue to favor conventional ablation systems for established procedures such as tumor ablation, cardiac arrhythmias, and urological interventions. The segment benefits from extensive physician training, proven clinical outcomes, and broad availability across North America. Long-standing adoption in multiple specialties and ease of use further strengthen its market position. The segment’s dominance is reinforced by integration with standard imaging systems and predictable procedural efficiency.

The Automated/Robotic segment is projected to grow at the fastest CAGR of 9.2% from 2025 to 2032, fueled by increasing demand for precision-guided ablation procedures in oncology, cardiology, and gynecology. Robotic-assisted and automated systems improve procedural accuracy, consistency, and efficiency, reducing complications and enhancing patient outcomes. Integration with real-time imaging and energy-monitoring platforms allows for advanced treatment planning and execution. Growing adoption in specialized hospitals, coupled with rising investment in advanced surgical platforms, supports rapid growth. The ability to standardize complex procedures, reduce operator dependency, and improve procedural reproducibility is driving uptake.

• By Procedure

On the basis of procedure, the North America Ablation Devices Market is segmented into Aesthetics-Skin Rejuvenation and Tightening, Aesthetics-Body Sculpting, Fat Reduction, and Reduction in the Appearance of Cellulite, Benign Prostatic Hyperplasia, Transurethral Needle Ablation, Laser and Other Energy-Based Therapies/Holmium Laser Ablation/Enucleation of the Prostate, Stress Urinary Incontinence, Menorrhagia/Endometrial Ablation, Uterine Fibroids, Spinal Decompression and Denervation, Varicose Veins, Atrial Fibrillation, Tumor Ablation, and Others. The Tumor Ablation segment dominated with a revenue share of 39.8% in 2024, driven by rising cancer prevalence, preference for minimally invasive procedures, and increasing availability of imaging-guided ablation platforms. Tumor ablation enables precise targeting of malignant tissue while preserving healthy structures, reducing hospital stays and improving patient recovery. Adoption is supported by physician expertise, technological advancements, and growing awareness of less-invasive cancer treatments. Increasing clinical evidence demonstrating effectiveness and safety compared to surgical resection strengthens market dominance. Rising demand in oncology centers and outpatient clinics further accelerates adoption.

The Aesthetics-Body Sculpting, Fat Reduction, and Reduction in the Appearance of Cellulite segment is expected to witness the fastest CAGR of 10.5% from 2025 to 2032, fueled by increasing interest in non-invasive cosmetic procedures, rising disposable income, and growing demand for outpatient aesthetic interventions. Advancements in energy-based devices for body contouring and cellulite reduction improve procedural efficacy and patient satisfaction. The segment benefits from shorter recovery times, lower complication rates, and high patient demand. Expanding aesthetic clinics, rising awareness of body contouring procedures, and technological improvements in device precision support rapid adoption. Increasing social media influence and demand for minimally invasive cosmetic enhancements also drive growth.

• By Application

On the basis of application, the North America Ablation Devices Market is segmented into cancer, cardiovascular, ophthalmology, gynecology, urology, orthopedics, and others. The Cancer segment dominated with a revenue share of 42.7% in 2024, fueled by increasing cancer incidence, preference for minimally invasive treatments, and adoption of advanced thermal and non-thermal ablation techniques in oncology centers. The ability to precisely target tumors while minimizing damage to healthy tissue drives adoption. Availability of advanced imaging guidance, robotic integration, and favorable clinical outcomes further supports dominance. Physicians and hospitals prefer ablation for its effectiveness, safety, and reduced post-procedure complications. Rising investment in oncology infrastructure, increasing patient awareness, and broader reimbursement policies also contribute to market leadership.

The Urology segment is expected to witness the fastest CAGR of 9.8% from 2025 to 2032, driven by increasing prevalence of benign prostatic hyperplasia, stress urinary incontinence, and urinary tract disorders. Adoption of minimally invasive ablation therapies such as laser, radiofrequency, and energy-based procedures is growing rapidly. Rising investment in specialized urology centers, advanced imaging, and targeted treatment protocols supports segment growth. Advantages such as reduced recovery time, lower complication rates, and outpatient suitability fuel adoption. Expanding awareness among physicians and patients, coupled with rising healthcare infrastructure in North America, further accelerates uptake.

North America Ablation Devices Market Regional Analysis

- U.S. dominated the North America Ablation Devices Market with the largest revenue share of 82.3% in 2024, driven by advanced healthcare infrastructure, growing awareness among clinicians and patients, and a strong presence of leading market players. The country witnessed substantial growth in ablation device installations across hospitals and specialty clinics, particularly in cardiac and tumor ablation procedures, supported by continuous innovations from both established companies and emerging startups

- Canada is expected to witness the fastest growth in the North America Ablation Devices Market, with a projected CAGR of 8.9% from 2025 to 2032, fueled by rising adoption of minimally invasive procedures, increasing awareness of ablation therapies, and expanding healthcare infrastructure in urban and semi-urban regions

- High adoption of minimally invasive procedures, continuous technological advancements in energy-based ablation devices, and growing investments in hospitals and specialty clinics are supporting the widespread use of Ablation Devices across the region

U.S. North America Ablation Devices Market Insight

The U.S. North America Ablation Devices Market captured the largest revenue share of 82.3% in 2024 within North America, fueled by increasing demand for cardiac, tumor, and renal ablation procedures. Growth is supported by the introduction of innovative energy-based platforms, robotic-assisted systems, and image-guided ablation technologies, as well as extensive hospital and outpatient adoption. Expanding clinician awareness and patient preference for minimally invasive treatments are further propelling market growth.

Canada North America Ablation Devices Market Insight

The Canada North America Ablation Devices Market is expected to witness the fastest growth in the North America Ablation Devices Market, with a projected CAGR of 8.9% from 2025 to 2032, driven by rising adoption of minimally invasive procedures, increasing awareness of ablation therapies, and expanding healthcare infrastructure in urban and semi-urban regions. Government initiatives to modernize healthcare facilities and enhanced training programs for clinicians are anticipated to accelerate market growth.

North America Ablation Devices Market Share

The Ablation Devices industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Boston Scientific Corporation (U.S.)

- Johnson & Johnson and its affiliates (U.S.)

- Abbott (U.S.)

- AngioDynamics (U.S.)

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V. (Netherlands)

- Stryker (U.S.)

- Terumo Corporation (Japan)

- Merit Medical Systems (U.S.)

- Hologic, Inc. (U.S.)

- B. Braun SE (Germany)

- Varian Medical Systems (U.S.)

- Apyx Medical (U.S.)

- Cook (U.S.)

- Olympus Corporation (Japan)

Latest Developments in North America Ablation Devices Market

- In February 2025, Johnson & Johnson (J&J) resumed the limited market release of its Varipulse heart device in the United States after an investigation confirmed that the devices functioned as intended. The Varipulse device utilizes pulsed field ablation to treat abnormal heart rhythms. The initial rollout was paused in January 2025 due to reports of four stroke events. The investigation revealed that while the devices operated correctly, the risk of neurovascular events may increase if ablations are performed excessively, stacked, or misplaced outside the pulmonary veins. As a result, J&J updated the usage guidance for the Varipulse Catheter device globally. Despite the pause in the U.S., the Varipulse rollout has completed over 3,000 commercial cases worldwide and remains available in all launched markets

- In December 2024, the U.S. Food and Drug Administration (FDA) classified the recall of Boston Scientific's POLARx Cryoablation Balloon Catheters as "most serious" due to a significant number of esophageal injuries, specifically atrio-esophageal fistulas, which can lead to fatal complications such as air bubbles blocking brain blood vessels. The recall aimed to update the catheters' instructions for use rather than remove the product. These catheters are utilized in minimally invasive ablation procedures to treat atrial fibrillation, which causes rapid and irregular heartbeats. The FDA cited seven injuries and four deaths linked to the product. Boston Scientific issued an urgent medical device advisory instructing affected customers on appropriate use following the revised guidelines

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.