North America Acute Coronary Syndrome Market

Market Size in USD Billion

USD

4.78 Billion

USD

7.28 Billion

2025

2033

USD

4.78 Billion

USD

7.28 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.78 Billion | |

| USD 7.28 Billion | |

| % | |

|

North America Acute Coronary Syndrome Market Size

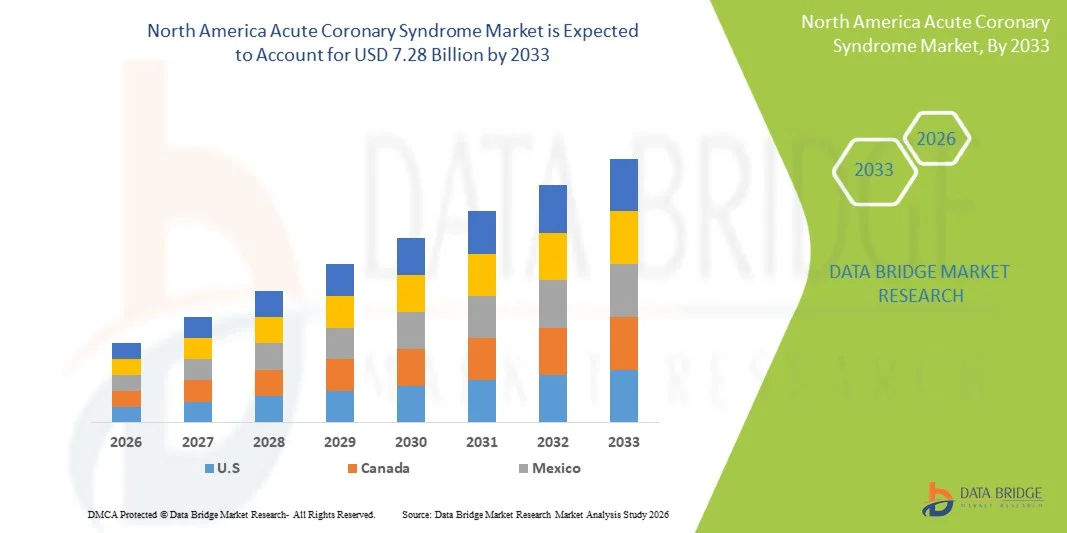

- The North America acute coronary syndrome market size was valued at USD 4.78 billion in 2025and is expected to reach USD 7.28 billion by 2033, at a CAGR of 5.40% during the forecast period

- The market growth is largely fueled by the rising global prevalence of cardiovascular diseases, increasing incidence of heart attacks and unstable angina, and continuous advancements in diagnostic technologies, interventional cardiology devices, and emergency cardiac care systems across healthcare settings

- Furthermore, growing awareness regarding early diagnosis, increasing demand for rapid treatment solutions, and expanding adoption of advanced medications, stents, and minimally invasive procedures are establishing Acute Coronary Syndrome solutions as a critical component of modern cardiovascular care. These converging factors are accelerating the uptake of Acute Coronary Syndrome solutions, thereby significantly boosting the industry's growth

North America Acute Coronary Syndrome Market Analysis

- Acute Coronary Syndrome solutions, including diagnostic biomarkers, ECG monitoring systems, antiplatelet drugs, anticoagulants, thrombolytics, coronary stents, and emergency interventional procedures, are increasingly vital components of modern cardiovascular care due to their role in enabling rapid diagnosis and timely treatment of life-threatening cardiac events

- The escalating demand for Acute Coronary Syndrome solutions is primarily fueled by rising prevalence of coronary artery disease, growing aging population, increasing incidence of obesity and diabetes, and expanding access to advanced cardiac care and emergency treatment services

- S. dominated the acute coronary syndrome market in North America with the largest revenue share of approximately 38.7% in 2025, characterized by advanced healthcare infrastructure, high awareness regarding cardiovascular diseases, increasing adoption of modern cardiac diagnostics, strong availability of emergency care services, and growing use of minimally invasive interventional cardiology procedures across major hospitals

- Canada is expected to be the fastest growing market in the acute coronary syndrome sector during the forecast period due to rising aging population, increasing prevalence of heart disease risk factors, expanding investments in cardiac specialty centers, strong demand for technologically advanced treatment solutions, and continuous improvements in emergency and preventive cardiovascular care services

- The Medication segment accounted for the largest market revenue share of 58.3% in 2025, driven by routine use of antiplatelets, anticoagulants, beta blockers, statins, and thrombolytics in immediate and long-term management

Report Scope and North America Acute Coronary Syndrome Market Segmentation

|

Attributes |

North America Acute Coronary Syndrome Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Mexico · Canada |

|

Key Market Players |

· Pfizer Inc. (U.S.) · AstraZeneca plc (U.K.) · Sanofi S.A. (France) · Novartis AG (Switzerland) · Bristol-Myers Squibb Company (U.S.) · Johnson & Johnson (U.S.) · Bayer AG (Germany) · Boehringer Ingelheim GmbH (Germany) · Eli Lilly and Company (U.S.) · Abbott Laboratories (U.S.) · Medtronic plc (Ireland) · Boston Scientific Corporation (U.S.) · Terumo Corporation (Japan) · Edwards Lifesciences Corporation (U.S.) · Siemens Healthineers AG (Germany) · GE HealthCare Technologies Inc. (U.S.) · F. Hoffmann-La Roche Ltd. (Switzerland) · Merck & Co., Inc. (U.S.) · Daiichi Sankyo Company, Limited (Japan) · Amgen Inc. (U.S.) |

|

Market Opportunities |

· Expansion of Advanced Cardiac Diagnostics and Early Detection Programs · Rising Demand for Minimally Invasive Interventional Procedures |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

North America Acute Coronary Syndrome Market Trends

“Enhanced Treatment Outcomes Through Rapid Diagnosis and Minimally Invasive Cardiac Intervention Advances”

- A significant and accelerating trend in the global Acute Coronary Syndrome market is the increasing adoption of rapid diagnostic technologies, high-sensitivity cardiac biomarkers, and minimally invasive revascularization procedures that improve survival rates and reduce treatment delays. These innovations are transforming emergency cardiac care worldwide

- Advanced diagnostic protocols and catheter-based interventions are increasingly being used to enable faster clinical decision-making and improved patient outcomes

- For instance, hospitals and cardiac centers globally are expanding use of high-sensitivity troponin testing, coronary angiography, and percutaneous coronary intervention (PCI) systems from companies such as Abbott, Roche, Medtronic, and Boston Scientific

- The growing use of drug-eluting stents, thrombectomy devices, and next-generation antiplatelet therapies is also improving post-event recovery and lowering recurrence risks

- Another major trend is the integration of telecardiology, remote ECG monitoring, and AI-assisted imaging tools that help identify high-risk patients earlier

- In addition, healthcare systems are increasingly developing specialized chest pain centers and STEMI response networks to reduce door-to-balloon treatment times

- This shift toward faster diagnosis, precision intervention, and coordinated emergency cardiac care is fundamentally reshaping the management of acute coronary events globally

North America Acute Coronary Syndrome Market Dynamics

Driver

“Rising Cardiovascular Disease Burden and Expanding Access to Emergency Cardiac Care”

- Increasing prevalence of cardiovascular disease, hypertension, diabetes, obesity, smoking, and sedentary lifestyles is a major driver for the Acute Coronary Syndrome market. These risk factors continue to increase the global incidence of myocardial infarction and unstable angina

- Expanding access to emergency cardiac treatment and awareness of early symptom recognition is further accelerating market growth

- For instance, countries such as the U.S., China, India, Germany, Japan, and Brazil are investing in cath labs, ambulance response systems, and acute cardiac care infrastructure

- Aging populations worldwide are also contributing to higher hospitalization rates for coronary events and related complications

- Furthermore, increasing adoption of evidence-based therapies including statins, antiplatelets, anticoagulants, and PCI procedures is improving treatment volumes and outcomes

- Government and private healthcare investments in cardiovascular screening and treatment programs are expected to further strengthen market demand during the forecast period

Restraint/Challenge

“High Treatment Costs, Unequal Access, and Delayed Diagnosis”

- One of the major challenges restraining the Acute Coronary Syndrome market is the high cost associated with emergency hospitalization, coronary interventions, intensive care, and long-term secondary prevention therapies, particularly in low- and middle-income countries

- Delayed diagnosis and limited access to specialized cardiac centers remain significant barriers in many regions

- For instance, patients in rural Asia-Pacific, Africa, and parts of Latin America may experience slower access to ECG testing, thrombolysis, or PCI-capable hospitals during critical treatment windows

- Shortages of trained interventional cardiologists, nurses, and emergency personnel can also constrain treatment capacity

- In addition, poor adherence to lifestyle modification and long-term medication regimens increases recurrence risks after initial events

- Overcoming these barriers through broader healthcare coverage, faster referral systems, infrastructure investment, and preventive cardiovascular education will be essential for sustained market growth

North America Acute Coronary Syndrome Market Scope

The market is segmented on the basis of type, diagnosis, treatment, and end user.

- By Type

On the basis of type, the Acute Coronary Syndrome market is segmented into Non-ST-Elevation Myocardial Infarction, ST-Elevation Myocardial Infarction, and Unstable Angina. The Non-ST-Elevation Myocardial Infarction segment dominated the largest market revenue share of 46.7% in 2025, driven by its higher incidence rate compared with other acute coronary conditions and increasing diagnosis through advanced cardiac biomarkers. NSTEMI cases are common among aging populations and patients with diabetes, hypertension, and obesity. Growing awareness regarding early cardiac symptom recognition is supporting timely hospital admissions. Availability of effective medications and catheter-based interventions further strengthens treatment demand. Expansion of emergency cardiac care units is also contributing to segment leadership. Improved diagnostic protocols across hospitals continue to support strong market share.

The ST-Elevation Myocardial Infarction segment is expected to witness the fastest growth rate of 21.9% from 2026 to 2033, driven by increasing emergency care capabilities and rapid adoption of advanced reperfusion therapies. STEMI requires immediate treatment, resulting in high demand for specialized procedures and hospital resources. Expansion of ambulance networks and chest pain centers is improving patient access. Rising investment in cardiac catheterization laboratories is accelerating treatment volumes. Growing public awareness campaigns about heart attack symptoms are further supporting growth. Technological advances in interventional cardiology are increasing recovery outcomes. Expanding healthcare access in emerging economies continues to fuel segment growth.

- By Diagnosis

On the basis of diagnosis, the Acute Coronary Syndrome market is segmented into Stress Test, Blood Tests, Imaging and Others. The Blood Tests segment held the largest market revenue share of 42.8% in 2025, driven by widespread use of troponin and biomarker testing for rapid and accurate confirmation of cardiac injury. Blood tests are essential in emergency departments due to quick turnaround time and strong clinical reliability. Increasing adoption of high-sensitivity troponin assays is improving early detection rates. Rising patient inflow with chest pain symptoms supports strong testing demand. Hospitals prioritize blood diagnostics as a first-line evaluation tool. Expansion of laboratory infrastructure further strengthens segment dominance. Continuous innovation in cardiac biomarkers supports future demand.

The Imaging segment is expected to witness the fastest CAGR of 23.6% from 2026 to 2033, driven by growing use of echocardiography, CT angiography, and MRI for comprehensive cardiac assessment. Imaging tools help physicians evaluate artery blockage, heart damage, and treatment planning. Rising preference for non-invasive diagnostic methods is boosting adoption. Increasing availability of advanced imaging equipment in hospitals supports growth. Improved accuracy and faster scanning technologies are enhancing outcomes. Growth in preventive cardiology screening also contributes to expansion. Healthcare digitization continues to accelerate imaging demand globally.

- By Treatment

On the basis of treatment, the Acute Coronary Syndrome market is segmented into Medication and Surgery. The Medication segment accounted for the largest market revenue share of 58.3% in 2025, driven by routine use of antiplatelets, anticoagulants, beta blockers, statins, and thrombolytics in immediate and long-term management. Medications are widely used across all stages of acute coronary syndrome treatment. Rising prevalence of cardiovascular disease is significantly increasing prescription volumes. Cost-effectiveness and easy accessibility further support segment dominance. Improved adherence programs and guideline-based therapy strengthen demand. Hospitals and outpatient clinics rely heavily on pharmacological management. Continuous drug innovation supports sustained market leadership.

The Surgery segment is expected to witness the fastest growth rate of 24.4% from 2026 to 2033, driven by increasing use of angioplasty, stent placement, and coronary artery bypass procedures. Growing availability of minimally invasive cardiac interventions is accelerating patient preference. Rising incidence of severe coronary blockages is boosting procedural volumes. Expansion of catheterization labs and cardiac surgery centers supports growth. Technological advances in stents and surgical tools are improving success rates. Faster recovery times and better survival outcomes encourage treatment adoption. Increasing healthcare expenditure is further driving segment expansion.

- By End User

On the basis of end user, the Acute Coronary Syndrome market is segmented into Hospitals and Clinics, Diagnostic Centers, Academic Institutes and Others. The Hospitals and Clinics segment dominated the largest market revenue share of 64.5% in 2025, driven by their role as the primary treatment centers for emergency cardiac events. Most acute coronary syndrome patients require immediate hospitalization, intensive monitoring, and specialist intervention. Hospitals provide access to diagnostics, medications, catheterization labs, and surgery under one setting. Rising investments in emergency cardiac care units support demand. Growing patient admissions due to heart disease prevalence strengthen segment leadership. Multidisciplinary treatment capabilities further reinforce dominance. Continuous healthcare infrastructure expansion supports long-term growth.

The Diagnostic Centers segment is expected to witness the fastest CAGR of 22.7% from 2026 to 2033, driven by increasing demand for early cardiac screening and outpatient diagnostic services. These centers offer blood tests, imaging, ECGs, and stress testing with shorter waiting times. Rising preventive healthcare awareness is supporting adoption. Expansion of private diagnostic chains is accelerating access. Cost-effective testing services are attracting a wider patient base. Technological upgrades in standalone centers are improving service quality. Increasing physician referrals continue to boost segment growth.

North America Acute Coronary Syndrome Market Regional Analysis

- The North America acute coronary syndrome market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the rising prevalence of cardiovascular diseases, increasing aging population, and growing burden of obesity, hypertension, and diabetes across the region

- Advancements in cardiac diagnostics, strong emergency healthcare systems, and expanding access to minimally invasive treatment procedures are fostering market growth. Healthcare providers across the region are increasingly focused on early diagnosis, preventive cardiology, and improved patient outcomes

- The region is experiencing significant demand across hospitals, specialty cardiac centers, and emergency care units, with continuous investments in modern cardiovascular treatment infrastructure

U.S. Acute Coronary Syndrome Market Insight

The U.S. acute coronary syndrome market dominated the acute coronary syndrome market in North America with the largest revenue share of approximately 38.7% in 2025, driven by advanced healthcare infrastructure, high awareness regarding cardiovascular diseases, and increasing adoption of modern cardiac diagnostics. Strong availability of emergency care services, growing use of minimally invasive interventional cardiology procedures, and supportive reimbursement systems are encouraging market growth. The country’s focus on rapid treatment pathways, technological innovation, and preventive heart health initiatives is expected to continue to stimulate demand.

Canada Acute Coronary Syndrome Market Insight

The Canada acute coronary syndrome market is expected to expand at a considerable CAGR during the forecast period, fueled by the rising aging population, increasing prevalence of heart disease risk factors, and expanding investments in cardiac specialty centers. Canada’s well-developed healthcare infrastructure, combined with strong demand for technologically advanced treatment solutions, supports market expansion. Continuous improvements in emergency response systems, diagnostic capabilities, and preventive cardiovascular care services are also becoming increasingly prevalent, aligning with growing patient care expectations.

North America Acute Coronary Syndrome Market Share

The Acute Coronary Syndrome industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- AstraZeneca plc (U.K.)

- Sanofi S.A. (France)

- Novartis AG (Switzerland)

- Bristol-Myers Squibb Company (U.S.)

- Johnson & Johnson (U.S.)

- Bayer AG (Germany)

- Boehringer Ingelheim GmbH (Germany)

- Eli Lilly and Company (U.S.)

- Abbott Laboratories (U.S.)

- Medtronic plc (Ireland)

- Boston Scientific Corporation (U.S.)

- Terumo Corporation (Japan)

- Edwards Lifesciences Corporation (U.S.)

- Siemens Healthineers AG (Germany)

- GE HealthCare Technologies Inc. (U.S.)

- Hoffmann-La Roche Ltd. (Switzerland)

- Merck & Co., Inc. (U.S.)

- Daiichi Sankyo Company, Limited (Japan)

- Amgen Inc. (U.S.)

Latest Developments in North America Acute Coronary Syndrome Market

- In June 2021, the European Society of Cardiology (ESC) highlighted results from the MASTER DAPT trial showing that abbreviated dual antiplatelet therapy after percutaneous coronary intervention in high bleeding risk patients, including those with acute coronary syndrome (ACS), reduced bleeding without increasing ischemic events. The findings supported more individualized post-ACS antithrombotic treatment strategies

- In August 2021, the IAMI trial reported that administering influenza vaccination shortly after myocardial infarction or during hospitalization for ACS significantly reduced the composite risk of death, myocardial infarction, or stent thrombosis over 12 months. This marked an important preventive care development in ACS management

- In August 2023, the European Society of Cardiology released its updated Guidelines for the Management of Acute Coronary Syndromes, unifying prior STEMI and NSTEMI recommendations into a single framework. The guideline emphasized rapid diagnosis using high-sensitivity troponin testing, risk-based invasive strategies, and personalized antithrombotic therapy

- In June 2023, the American Heart Association and American College of Cardiology issued updated chronic coronary disease guidelines recommending consideration of low-dose colchicine for selected patients with prior myocardial infarction or established coronary disease. This expanded interest in inflammation-targeted therapies relevant to post-ACS secondary prevention

- In February 2024, major cardiovascular market analyses highlighted growing adoption of PCSK9 inhibitors, advanced lipid-lowering therapies, and digital monitoring tools in post-ACS care. These developments reflected increasing focus on long-term risk reduction following acute coronary events

- In February 2025, the ACC/AHA/ACEP/NAEMSP/SCAI released updated U.S. guidelines for acute coronary syndromes, integrating unstable angina, NSTEMI, and STEMI management. The guidance emphasized serial troponin testing, intracoronary imaging, individualized revascularization timing, and modern antiplatelet strategies

- In April 2025, AGEPHA Pharma presented new clinical trial data at the American College of Cardiology Annual Meeting showing that low-dose colchicine (0.5 mg) significantly reduced progression of coronary plaque. The development strengthened the role of anti-inflammatory therapy in secondary prevention after ACS

- In May 2025, EuroPCR presented results from the 4D-ACS trial demonstrating that one month of dual antiplatelet therapy followed by low-dose prasugrel monotherapy reduced bleeding events without increasing ischemic risk after PCI in ACS patients. The study supported shorter and safer antiplatelet regimens

- In July 2025, pipeline reviews of the global ACS market identified active late-stage development programs involving Factor XIa inhibitors, PCSK9 inhibitors, ischemia-reperfusion injury therapies, and biomarker-guided treatments. These innovations indicated continued expansion beyond traditional antiplatelet and statin therapies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.