North America Airless Packaging Market

Market Size in USD Billion

USD

1.26 Billion

USD

1.69 Billion

2024

2032

USD

1.26 Billion

USD

1.69 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.26 Billion | |

| USD 1.69 Billion | |

| % | |

|

North America Airless Packaging Market Size

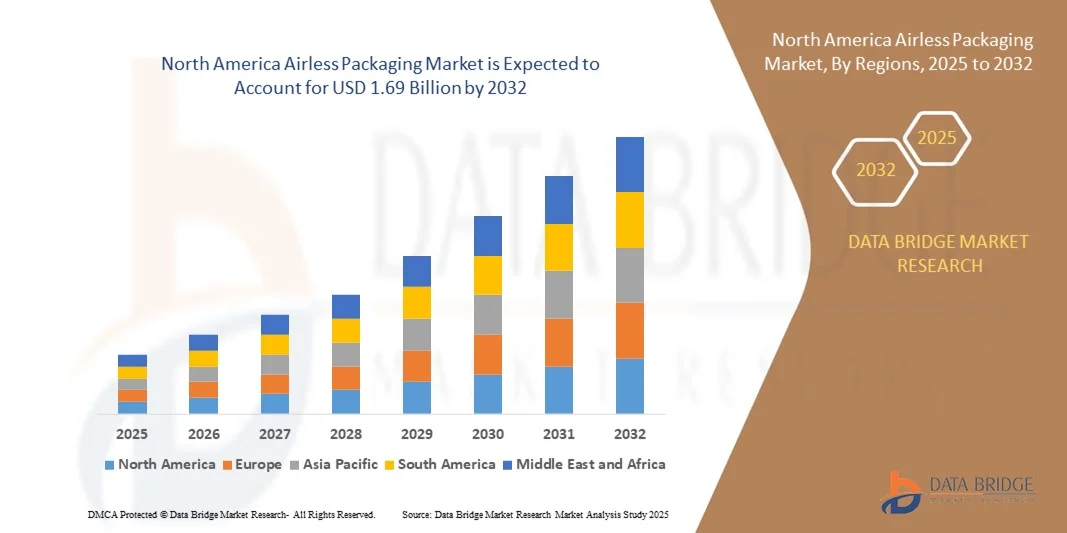

- The North America airless packaging market size was valued at USD 1.26 billion in 2024 and is expected to reach USD 1.69 billion by 2032, at a CAGR of 3.8% during the forecast period

- The market growth is largely fueled by the increasing demand for sustainable and contamination-free packaging solutions across the cosmetics, personal care, and healthcare industries. The shift toward eco-friendly, airless systems is driven by the need to preserve product integrity, prevent oxidation, and minimize waste, aligning with sustainability goals and consumer expectations for green packaging alternatives

- Furthermore, rising brand investments in advanced dispensing technologies and the introduction of refillable and recyclable airless containers are accelerating product innovation and adoption. These trends are reinforcing the market’s expansion by offering enhanced product protection, user convenience, and environmentally responsible solutions

North America Airless Packaging Market Analysis

- Airless packaging, designed to protect sensitive formulations from external contamination and air exposure, is gaining significant traction across cosmetics, pharmaceuticals, and skincare sectors. Its ability to extend product shelf life, reduce preservative use, and improve dosing precision makes it an ideal solution for premium and performance-driven products

- The rising consumer focus on hygiene, product safety, and sustainable consumption is the key driving force behind market growth. Manufacturers are increasingly adopting airless systems to meet evolving regulatory standards and sustainability requirements, thereby reinforcing the market’s evolution toward innovative, high-efficiency packaging solutions

- U.S. dominated the airless packaging market in 2024, due to strong demand from the cosmetics, personal care, and pharmaceutical sectors, alongside increasing adoption of sustainable and hygienic packaging solutions

- Canada is expected to be the fastest growing country in the airless packaging market during the forecast period due to rising adoption of premium personal care and cosmetic products and increasing consumer awareness of sustainable packaging

- Plastic segment dominated the market with a market share of 63.9% in 2024, due to its versatility, lightweight nature, and lower production cost compared to glass or metal alternatives. Plastic-based airless systems are widely used in skincare, cosmetics, and personal care applications, where they provide high design flexibility and resilience. The continuous advancements in recyclable and PCR (post-consumer resin) plastics further strengthen its dominance, catering to both performance and sustainability demands

Report Scope and Airless Packaging Market Segmentation

|

Attributes |

Airless Packaging Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

North America Airless Packaging Market Trends

Rise of Refillable and Recyclable Airless Packaging

- The airless packaging market is witnessing a strong shift toward refillable and recyclable solutions as sustainability becomes a central focus for packaging manufacturers and brands. This trend is driven by increasing regulatory pressures and changing consumer attitudes toward eco-conscious product consumption, pushing companies to adopt circular economy models in their packaging designs

- For instance, Lumson S.p.A. has introduced its refillable airless packaging line under the "TAG System," which allows consumers to replace inner cartridges while reusing the outer container. Similarly, Aptar Group has developed its Future Airless range designed for full recyclability while maintaining product integrity and premium aesthetics

- Sustainability-driven innovation in material science is enabling the development of airless systems constructed from mono-materials such as polyethylene and polypropylene to enhance recyclability. These designs ensure that the entire packaging system can be easily processed through existing recycling streams while maintaining the airless mechanism performance required for sensitive formulations

- Refillable formats are becoming increasingly popular among personal care and skincare brands seeking to reduce packaging waste while maintaining a luxurious and convenient user experience. The adoption of such designs is supported by consumers’ willingness to invest in products that align with environmental responsibilities and long-term usability

- The trend is also influencing supply chain models, with brands and manufacturers collaborating on reverse logistics for refill containers and developing modular designs to extend product lifecycles. This movement is supported by global packaging standards and rising investment in sustainable packaging production technologies

- The rise of refillable and recyclable airless solutions is setting a new benchmark for environmentally responsible packaging, encouraging continuous research and design improvements to balance sustainability with functionality, aesthetics, and user convenience across multiple product categories such as cosmetics, pharmaceuticals, and personal care

North America Airless Packaging Market Dynamics

Driver

Growing Demand for Sustainable, Contamination-Free Solutions

- The growing consumer demand for sustainable packaging aligned with health and hygiene awareness has become a primary driver for airless packaging adoption. The airless system ensures full product evacuation, preserves active ingredients, and prevents contamination through its non-vented dispensing method, appealing strongly to premium cosmetic and pharmaceutical brands

- For instance, Quadpack Industries introduced an eco-friendly airless jar collection using recyclable PET material to deliver hygienic and consistent dispensing for skincare products. This innovation reflects the ongoing industry push toward safer, waste-minimized packaging that offers both environmental and performance benefits

- Rising environmental consciousness among consumers is prompting manufacturers to integrate eco-certified materials and design recyclable dispensers. These systems prevent external contamination and also reduce residual product wastage, reinforcing efficiency and brand reliability for sensitive and high-value formulations

- Airless packaging is also favored for enabling oxygen-sensitive formulations to remain stable throughout their shelf life, which directly supports market growth across dermo-cosmetics and pharmaceutical segments. The absence of air ingress extends product longevity, reducing preservative requirements

- Growing technological advancement in airless systems through precision-engineered pumps, improved barrier coatings, and recyclable designs is gradually expanding their presence into mass-market products. The ongoing convergence of sustainability, safety, and functionality continues to strengthen airless packaging's role as a future-proof solution for brands seeking contamination-free and eco-conscious solutions

Restraint/Challenge

High Manufacturing Costs

- High production expenses associated with precision engineering and specialized components pose a major restraint for the airless packaging market. The mechanism requires complex designs involving pumps, valves, and airtight containers, which increases tooling and assembly costs compared to traditional packaging formats

- For instance, companies such as Albéa Group have reported higher production expenditures for their airless packaging lines due to the integration of multi-component molding and specialized pump assemblies. This cost difference often makes airless solutions less accessible to smaller brands or cost-sensitive product segments

- Manufacturing airless systems that maintain pressure stability while ensuring recyclability further adds to material and process costs. The challenge lies in balancing eco-friendly goals with mechanical integrity and production efficiency, as recyclable mono-material solutions often require advanced molding technologies

- Supply chain complexities also add to overheads, since precision parts in airless containers often need high-quality polymer resins and tight tolerances that increase testing, quality control, and mold maintenance requirements. These factors delay scalability and impact cost competitiveness across global markets

- Reducing production costs through automation, innovative molding technologies, and material efficiency remains critical for wider adoption. Overcoming this challenge through mass-production optimization and design standardization will be essential for the airless packaging market to achieve sustainable economic scalability in the coming years

North America Airless Packaging Market Scope

The market is segmented on the basis of packaging type, material type, category, distribution channel, and end-user.

- By Packaging Type

On the basis of packaging type, the airless packaging market is segmented into rigid plastic and flexible plastics. The rigid plastic segment dominated the market with the largest revenue share in 2024 due to its superior protection, durability, and ability to maintain product integrity without air exposure. Rigid airless packaging is highly preferred in the cosmetics and personal care sectors for its ability to prevent oxidation and contamination of sensitive formulations. The segment’s dominance is also supported by the increasing use of high-barrier rigid containers in skincare and pharmaceutical applications where product preservation is critical.

The flexible plastics segment is anticipated to witness the fastest growth rate from 2025 to 2032, driven by rising demand for lightweight, cost-efficient, and sustainable packaging solutions. Flexible airless pouches and tubes offer portability and ease of dispensing, aligning with the trend toward travel-friendly and single-use packaging formats. Growing innovations in recyclable and bio-based flexible materials are further encouraging manufacturers to adopt these formats, particularly across beauty, health, and wellness products.

- By Material Type

On the basis of material type, the airless packaging market is segmented into plastic, glass, and others. The plastic segment held the largest market share of 63.9% in 2024, attributed to its versatility, lightweight nature, and lower production cost compared to glass or metal alternatives. Plastic-based airless systems are widely used in skincare, cosmetics, and personal care applications, where they provide high design flexibility and resilience. The continuous advancements in recyclable and PCR (post-consumer resin) plastics further strengthen its dominance, catering to both performance and sustainability demands.

The glass segment is expected to witness the fastest growth from 2025 to 2032 due to its premium appeal and eco-friendly characteristics. Glass-based airless containers are increasingly preferred by luxury cosmetic and skincare brands seeking a sustainable yet high-end packaging appearance. Their chemical inertness and ability to preserve sensitive formulations enhance consumer trust, while innovations in lightweight and shatter-resistant glass designs further expand adoption.

- By Category

On the basis of category, the airless packaging market is segmented into premium and mass. The premium segment dominated the market in 2024, fueled by rising demand for luxury skincare, cosmetics, and high-end personal care products. Premium airless packaging ensures superior product protection, precision dispensing, and a sophisticated aesthetic, enhancing brand perception and consumer experience. High-income consumers’ preference for sustainable yet elegant packaging continues to drive innovation within this category.

The mass segment is projected to grow at the fastest CAGR from 2025 to 2032, driven by increasing adoption of airless systems by mid-range and affordable brands. Manufacturers are developing cost-efficient airless solutions that maintain functionality while catering to the price-sensitive market. Growing awareness about hygiene and product preservation in daily-use items, such as lotions and sanitizers, is also expanding airless packaging penetration in mass-market applications.

- By Distribution Channel

On the basis of distribution channel, the airless packaging market is segmented into supermarkets, hypermarkets, specialist retailers, convenience stores, and e-commerce. The supermarkets and hypermarkets segment held the largest revenue share in 2024 due to the high product visibility, consumer trust, and wide assortment of branded personal care and skincare items. These retail outlets provide direct consumer engagement, allowing premium airless-packaged products to attract attention through design and functionality.

The e-commerce segment is anticipated to witness the fastest growth rate from 2025 to 2032, supported by the shift toward online shopping and direct-to-consumer brand strategies. The increasing popularity of digital beauty and health retail platforms boosts demand for airless packaging that ensures leak-proof and tamper-resistant delivery. Moreover, online-exclusive cosmetic brands prefer customizable and visually appealing airless containers to enhance brand identity and customer unboxing experiences.

- By End-User

On the basis of end-user, the airless packaging market is segmented into personal care and home care, healthcare, food & beverages, and others. The personal care and home care segment dominated the market in 2024, driven by the high usage of airless packaging in skincare, cosmetics, and hygiene products. The segment benefits from rising consumer awareness about product safety and contamination-free dispensing, making airless systems essential for preserving active ingredients. Continuous product launches by beauty brands adopting airless designs further reinforce segment leadership.

The healthcare segment is expected to register the fastest growth from 2025 to 2032, driven by increasing application in pharmaceutical creams, topical treatments, and medical formulations requiring controlled dispensing. Airless packaging ensures dosage precision and prevents exposure to air and microbial contamination, which is critical for medical efficacy. The growing demand for sterile, preservative-free packaging solutions in the healthcare industry continues to boost adoption across pharmaceutical and therapeutic product lines.

North America Airless Packaging Market Regional Analysis

- U.S. dominated the airless packaging market with the largest revenue share in 2024, driven by strong demand from the cosmetics, personal care, and pharmaceutical sectors, alongside increasing adoption of sustainable and hygienic packaging solutions

- The country’s leadership is reinforced by advanced R&D capabilities, continuous innovation in refillable and multifunctional airless systems, and a well-established supply chain supporting large-scale production

- Growing consumer preference for contamination-free, travel-friendly, and eco-conscious packaging further strengthens the U.S. position. The presence of major global packaging manufacturers, robust investments in product innovation, and continuous focus on sustainability initiatives continue to support U.S. dominance in the regional market

Canada Airless Packaging Market Insight

Canada is projected to register the fastest CAGR in the North America airless packaging market from 2025 to 2032, supported by rising adoption of premium personal care and cosmetic products and increasing consumer awareness of sustainable packaging. Expanding e-commerce channels, collaborations between domestic manufacturers and global brands, and government-backed sustainability initiatives are driving market penetration. The growing preference for eco-friendly, refillable, and compact airless systems is accelerating adoption. Canada’s focus on innovation, clean manufacturing practices, and advanced retail infrastructure reinforces its strong growth outlook.

Mexico Airless Packaging Market Insight

Mexico is expected to witness steady growth between 2025 and 2032, fueled by increasing demand for hygienic and sustainable packaging in personal care, skincare, and pharmaceutical products. Growing foreign investments in cosmetics and packaging manufacturing, coupled with supportive government policies and expanding retail and e-commerce networks, are driving market expansion. Strategic partnerships with international packaging companies and introduction of cost-effective airless solutions enhance accessibility. Mexico’s emphasis on quality standards and sustainable practices underpins its stable long-term market growth.

North America Airless Packaging Market Share

The airless packaging industry is primarily led by well-established companies, including:

- Ball Corporation (U.S.)

- Viva Group (U.S.)

- Silgan Holdings Inc. (U.S.)

- Amcor plc (Switzerland)

- Sonoco Products Company (U.S.)

- ALBÉA (France)

- AptarGroup, Inc. (U.S.)

- FUSIONPKG (U.S.)

- HCT Group (U.S.)

- East Hill Industries, LLC. (U.S.)

- Rieke, a subsidiary of TriMas (U.S.)

- HCP Packaging (China)

- Ningbo Gidea Packaging Co., Ltd. (China)

- TricorBraun (U.S.)

- WWP (U.S.)

- RPC Group Plc (U.K.)

- RAEPAK LTD (U.K.)

Latest Developments in North America Airless Packaging Market

- In October 2023, Quadpack introduced its refillable airless pen, a significant advancement in sustainable beauty packaging. This innovation features an airless dispensing system that ensures maximum formulation preservation while minimizing product waste. The refillable functionality aligns with the growing consumer demand for eco-friendly and reusable solutions, strengthening Quadpack’s position as a frontrunner in sustainable airless packaging. The launch is expected to accelerate market adoption of refillable formats and influence other manufacturers to invest in circular packaging innovations within the cosmetics sector

- In October 2023, Lumson launched a new range of airless packaging solutions designed to meet the evolving requirements of the cosmetics industry. The introduction focuses on sustainability, hygiene, and extended shelf life, offering advanced systems that prevent contamination and product oxidation. This move enhances Lumson’s competitive edge by catering to the increasing market preference for eco-conscious and high-performance packaging. The innovation boosts Lumson’s brand value and also contributes to driving market growth through enhanced product protection and reduced packaging waste

- In November 2022, Embelia introduced a refillable version of its Baia pouch airless system, developed in collaboration with Lablabo, a specialist in pouch-based airless technologies. This development underscores Embelia’s dedication to sustainability and innovation in flexible airless packaging. The new refillable system allows brands to reduce plastic consumption while maintaining product integrity, marking a key advancement in eco-friendly beauty and personal care packaging solutions. The introduction is anticipated to expand the company’s influence across brands adopting green packaging alternatives

- In May 2022, Carlyle announced plans to acquire a 100% stake in HCP Packaging, a leading global cosmetic packaging company. This strategic acquisition aims to enhance HCP’s operational efficiency, broaden its global reach, and strengthen its innovation capabilities in airless and sustainable packaging. By leveraging Carlyle’s expertise in consumer and manufacturing sectors, the move is expected to stimulate further investments in high-quality, technology-driven airless packaging solutions, thereby supporting market consolidation and growth

- In December 2021, Qosmedix expanded its product portfolio with the launch of new stock airless packaging options, including a 1 oz. (30 ml) white jar made from 50% post-consumer recycled (PCR) material. This initiative highlights the company’s commitment to sustainable manufacturing practices and the increasing integration of recycled materials in airless systems. The development supports the market’s shift toward eco-responsible packaging solutions, enhancing Qosmedix’s role in promoting environmentally conscious product offerings in the cosmetics and personal care industries

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

North America Airless Packaging Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its North America Airless Packaging Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as North America Airless Packaging Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.