North America Angiography Devices Market

Market Size in USD Billion

USD

3.75 Billion

USD

10.50 Billion

2024

2032

USD

3.75 Billion

USD

10.50 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.75 Billion | |

| USD 10.50 Billion | |

| % | |

|

Angiography Devices Market Size

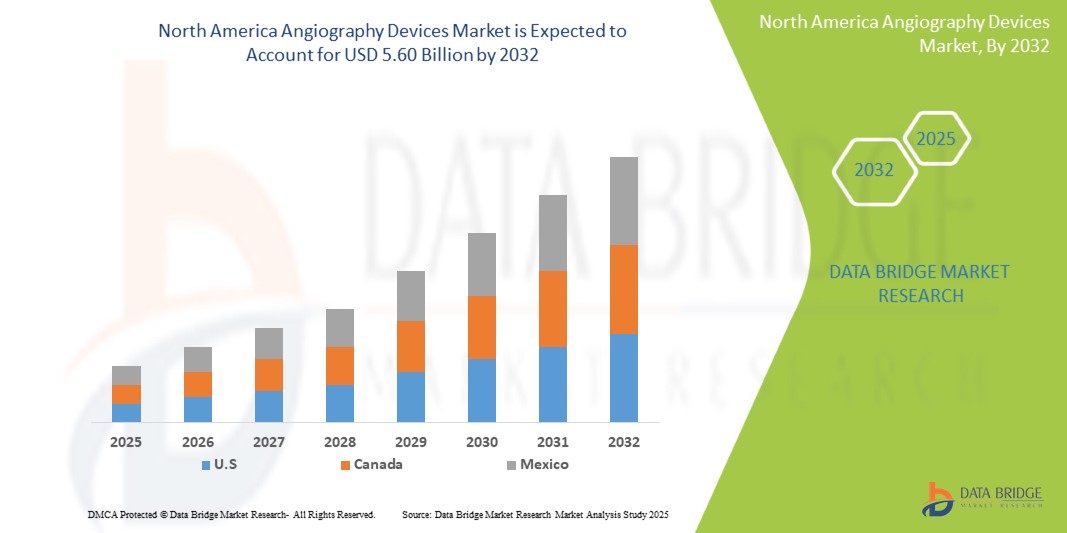

- The North America Angiography Devices market size was valued at USD 3,75 billion in 2024 and is expected to reach USD 5.60 billion by 2032, at a CAGR of 5.8% during the forecast period

- The market growth is largely fueled by the rising incidence of cardiovascular diseases, the increasing aging population, and the growing demand for early and accurate diagnosis of vascular conditions.

- Furthermore, technological advancements in angiography systems, such as 3D imaging capabilities and advanced navigation systems, are driving market expansion. These converging factors are accelerating the adoption of angiography devices across various medical applications, thereby significantly boosting the industry's growth.

Angiography Devices Market Analysis

- The angiography devices market encompasses a range of medical imaging equipment and consumables used to visualize blood vessels and organs. This includes angiography systems (C-arms, cath labs), catheters, guide wires, contrast media injectors, and other accessories. These devices are crucial for diagnosing and treating various cardiovascular, neurological, and peripheral vascular diseases. The market is driven by the increasing prevalence of cardiovascular diseases, technological advancements in imaging, and the growing demand for minimally invasive procedures.

- The escalating demand for angiography devices is primarily fueled by the increasing number of interventional cardiology and radiology procedures, the growing adoption of minimally invasive techniques, and the rising awareness of the benefits of early diagnosis and intervention in vascular diseases.

- The U.S. dominates the Angiography Devices market in North America with the largest revenue share of 87.45% in 2025, attributed to its well-established healthcare infrastructure, higher adoption rates of minimally invasive procedures, increased prevalence of cardiovascular diseases, and strong investments in interventional cardiology. The presence of leading manufacturers and high R&D spending further supports the market growth.

- The U.S. is expected to be the fastest-growing country in the North America Angiography Devices market driven by rising geriatric population, favorable reimbursement policies, and growing demand for technologically advanced devices such as flat-panel detectors and 3D rotational angiography systems. Continuous clinical advancements and strategic collaborations among key players are also contributing to market expansion.

- Angiography Catheters is expected to dominate the North America Angiography Devices market with a market share of 38.2% in 2025, owing to its precision in imaging vascular conditions, wide applicability in coronary and peripheral angiography procedures, and increasing adoption in both diagnostic and interventional cardiology due to its minimally invasive nature and clinical efficacy.

Report Scope and Angiography Devices Market Segmentation

|

Attributes |

Angiography Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Angiography Devices Market Trends

“Integration of 3D imaging and advanced navigation systems”

- Integration of Advanced Imaging and Navigation Technologies: A significant trend in the North America angiography devices market is the deepening integration of advanced imaging modalities and navigation technologies. This fusion is significantly enhancing diagnostic precision, procedural efficiency, and patient safety during complex interventional procedures.

- For instance, modern angiography systems combine 2D fluoroscopy with 3D imaging capabilities (e.g., CT-like imaging or rotational angiography) to provide comprehensive anatomical views. This allows clinicians to visualize intricate vascular structures and plan procedures with greater accuracy.

- The development of advanced navigation systems, including robotic-assisted angiography and electromagnetic tracking, is improving catheter maneuverability and reducing radiation exposure for both patients and clinicians. Furthermore, the seamless integration with patient data management systems (PACS/HIS) streamlines workflows and facilitates real-time decision-making.

- This trend towards more intelligent, integrated, and precise angiography systems is fundamentally reshaping interventional cardiology and radiology practices. Consequently, companies are investing heavily in R&D to develop next-generation angiography platforms with enhanced automation and real-time guidance features.

- The demand for angiography devices that offer seamless integration of advanced imaging and navigation is growing rapidly across hospitals and specialized cardiac/vascular centers, as clinicians prioritize optimal patient outcomes and procedural efficiency.

Angiography Devices Market Dynamics

Driver

“Rising incidence of cardiovascular diseases”

- The increasing incidence of cardiovascular diseases (CVDs) in North America is a major driver for the growth of the angiography devices market.

- For instance, according to the American Heart Association, CVD remains a leading cause of morbidity and mortality in the U.S., necessitating a high volume of diagnostic and interventional procedures. Angiography plays a critical role in diagnosing coronary artery disease, peripheral artery disease, and other vascular conditions, as well as guiding interventional treatments

- The aging population, coupled with lifestyle factors such as obesity, diabetes, and hypertension, contributes to the rising burden of CVDs, thereby increasing the demand for angiography procedures.

- Furthermore, advancements in interventional techniques and the growing preference for minimally invasive procedures are fueling the adoption of advanced angiography devices.

- Increasing awareness about early diagnosis and treatment of vascular diseases is also driving market growth

Restraint/Challenge

“High Cost of Angiography Systems and Reimbursement Issues”

- The high cost of advanced angiography systems and the complexities associated with reimbursement pose a significant challenge to broader market adoption, particularly for smaller healthcare facilities and those with budget constraints.

- For instance, a state-of-the-art angiography system can cost several million dollars, representing a substantial capital investment for hospitals and diagnostic centers. This high initial cost can limit access to advanced angiography technologies, especially in underserved areas.

- The need for specialized infrastructure, such as dedicated cath labs, and highly trained personnel (interventional cardiologists, radiologists, and technologists) further adds to the operational burden.

- Additionally, variations in reimbursement policies across different healthcare systems and insurance providers can create financial uncertainty, potentially limiting the volume of procedures performed.

- Addressing these challenges requires efforts to reduce manufacturing costs, develop more cost-effective solutions, and advocate for favorable reimbursement policies to ensure wider accessibility of angiography procedures

Angiography Devices Market Scope

The market is segmented on the basis product, technology, procedure, indication, application and end user.

- By Product

On the basis of product, the North America angiography devices market is segmented into angiography systems, angiography contrast media, vascular closure devices, angiography balloons, angiography catheters, angiography guidewires and angiography accessories. The Angiography Catheters segment dominates the largest market revenue share of 38.2% in 2025, driven by high demand for advanced imaging platforms that provide precise visualization of vascular structures. These systems are integral in both diagnostic and interventional procedures and are continually evolving with innovations such as flat-panel detectors, rotational angiography, and hybrid OR integration.

The vascular closure devices segment is anticipated to witness the fastest growth rate of 9.6% from 2025 to 2032, due to the growing shift toward minimally invasive procedures. These devices enable rapid hemostasis and early ambulation, reducing patient discomfort and improving hospital workflow efficiency.

- By technology

On the basis of technology, the market is segmented into X-ray angiography, CT angiography, and MRA angiography and other. X-ray angiography is further segmented into image Intensifiers and flat-panel detectors. X-ray angiography segment held the largest market revenue share in 2025, due to its established use in coronary and peripheral vascular assessments, and its compatibility with catheter-based procedures. It remains the backbone of interventional cardiology owing to its real-time visualization capabilities and precision.

The CT angiography segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by advancements in multi-slice CT systems, increased preference for non-invasive imaging, and broader applications in detecting aortic aneurysms, pulmonary embolism, and peripheral artery disease.

- By Procedure

On the basis of procedure, the market segmented into coronary angiography, endovascular angiography, neurovascular angiography, onco-angiography and other. The Coronary angiography segment accounted for the largest market revenue share in 2025, owing to the high burden of coronary artery disease in the region and the growing demand for timely diagnosis and treatment. This procedure remains a critical diagnostic step before interventions such as angioplasty or stenting.

The Neurovascular angiography segment is projected to witness the fastest CAGR from 2025 to 2032, attributed to increasing incidence of stroke and cerebrovascular anomalies, along with expanding access to specialized neurological centers and interventional neuroradiology capabilities.

- By Indication

On the basis of Indication, the market segmented into coronary artery disease, valvular heart disease, congenital heart disease, congestive heart failure, and other indications. The Coronary artery disease segment accounted for the largest market revenue share in 2025, driven by lifestyle-related risk factors, an aging population, and widespread screening initiatives across North America.

The Congestive heart failure segment is projected to witness the fastest CAGR from 2025 to 2032, as angiography increasingly supports both diagnosis and interventional planning in patients with complex heart failure conditions, particularly in the elderly.

- By Application

On the basis of Application, the market segmented into diagnostics and therapeutics. The diagnostics segment accounted for the largest market revenue share in 2025, as angiography remains the cornerstone for identifying vascular obstructions, aneurysms, and structural anomalies. Its high sensitivity and ability to guide subsequent interventions support its leading role.

The therapeutics segment is projected to witness the fastest CAGR from 2025 to 2032, reflecting the rise in image-guided procedures such as angioplasty, stenting, and embolization therapies—supported by hybrid ORs and improved device compatibility.

- By End User

On the basis of end user, the market is segmented into hospitals and clinics, diagnostic and imaging centers and research institutes. The Hospitals and clinics segment holds the largest market revenue share in 2025, due to their capacity to perform complex angiographic procedures, access to high-end imaging systems, and multidisciplinary expertise. These facilities are central to both routine diagnostics and emergency cardiovascular care.

The Diagnostic and imaging centers segment is expected to witness the fastest growth from 2025 to 2032, driven by the increasing preference for outpatient diagnostics, shorter patient wait times, and cost-effectiveness. Technological advancements enabling high-quality non-invasive angiographic imaging also support this trend.

Angiography Devices Market Regional Analysis

- U.S. dominates the Angiography Devices market with the largest revenue share of 87.45% in 2024, primarily driven by a high burden of cardiovascular diseases, robust diagnostic infrastructure, and strong reimbursement frameworks.

- The widespread adoption of advanced imaging systems—including digital flat-panel detectors and AI-assisted angiography platforms—continues to enhance procedural accuracy and clinical outcomes.

- Government initiatives such as the Million Hearts program and the American Heart Association’s screening campaigns have led to greater uptake of preventive and diagnostic cardiovascular imaging, boosting demand for angiography procedures.

- The presence of major industry players like GE HealthCare, Siemens Healthineers, and Philips, along with aggressive investments in R&D and product innovation, strengthens the U.S. market.

- Additionally, the shift toward minimally invasive and outpatient-based interventions—supported by ambulatory surgical centers—is accelerating the use of catheter-based angiography devices across multiple clinical settings.

Canada Angiography Devices Market Insight

The Canada Angiography Devices market is projected to expand at a substantial CAGR throughout the forecast period, driven by the growing incidence of breast cancer and increased investments in public health diagnostics. Canada’s national health strategy emphasizes early cancer detection, and provinces have rolled out organized breast screening programs (such as Ontario Breast Screening Program), boosting demand for advanced biopsy systems. Additionally, rising awareness about the benefits of minimally invasive biopsies over surgical alternatives and the growing availability of MRI-guided and stereotactic-guided techniques in diagnostic centers are contributing to market expansion. Strong regulatory standards set by Health Canada and increasing collaborations with U.S.-based device companies further support the growth of innovative biopsy technologies in the Canadian market

Mexico Angiography Devices Market Insight

The Mexico Angiography Devices market is expected to grow at a notable CAGR over the forecast period, driven by ongoing improvements in healthcare infrastructure and increased government focus on cardiovascular health. Initiatives such as the National Strategy for the Prevention and Control of Overweight, Obesity, and Diabetes have increased the demand for cardiovascular diagnostics, including angiography. While access to advanced interventional systems remains limited to urban tertiary care centers, public-private partnerships and international collaborations are gradually enhancing technology penetration in secondary and rural care settings. Growing awareness of early cardiovascular risk screening, coupled with improved training programs for cardiologists and radiologists, is supporting the wider adoption of both catheter-based and CT/MR angiography.

Angiography Devices Market Share

The Angiography Devices industry is primarily led by well-established companies, including:

- Siemens Healthineers (Germany)

- GE Healthcare (U.S.)

- Philips Healthcare (Netherlands)

- Canon Medical Systems Corporation (Japan)

- Boston Scientific Corporation (U.S.)

- Medtronic (Ireland)

- Abbott Laboratories (U.S.)

- Terumo Corporation (Japan)

- Cordis (U.S.)

- Shimadzu Corporation (Japan)

Latest Developments in North America Angiography Devices Market

- In March 2024, Siemens Healthineers launched a next-generation angiography system featuring advanced 3D imaging and AI-powered image processing. The system enhances visualization of complex vascular structures, improving diagnostic precision and interventional planning, especially in neurovascular and peripheral procedures. It supports clinicians with real-time decision-making and optimized workflow in high-acuity environments.

- In February 2024, GE HealthCare introduced a novel angiography catheter engineered for superior steerability and access to difficult anatomical areas. Designed to improve navigation during peripheral vascular interventions, the catheter enhances clinical precision, reduces procedure time, and supports improved outcomes in treating complex vascular pathologies.

- In January 2024, Philips Healthcare announced a strategic partnership with a leading robotic surgery firm to co-develop a robotic-assisted angiography system. The collaboration aims to deliver enhanced catheter navigation accuracy and control in neurovascular procedures, combining Philips’ imaging expertise with robotic precision for minimally invasive vascular interventions.

- In December 2023, Boston Scientific received FDA clearance for its latest guide wire, which features improved lubricity and enhanced tip flexibility. Engineered to navigate complex coronary anatomy, the device aims to increase procedural success and reduce complication rates in high-risk coronary interventions.

- In November 2023, Medtronic unveiled a new contrast media injector system offering next-generation dose management and full integration with patient information systems. Designed to enhance workflow efficiency and optimize contrast agent usage, the system supports improved imaging safety and precision during diagnostic and interventional angiography procedures.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.