North America Benign Prostatic Hyperplasia Devices Market

Market Size in USD Billion

USD

9.98 Billion

USD

25.42 Billion

2024

2032

USD

9.98 Billion

USD

25.42 Billion

2024

2032

| 2025 - 2032 | |

| USD 9.98 Billion | |

| USD 25.42 Billion | |

| % | |

|

North America Benign Prostatic Hyperplasia Devices Market Size

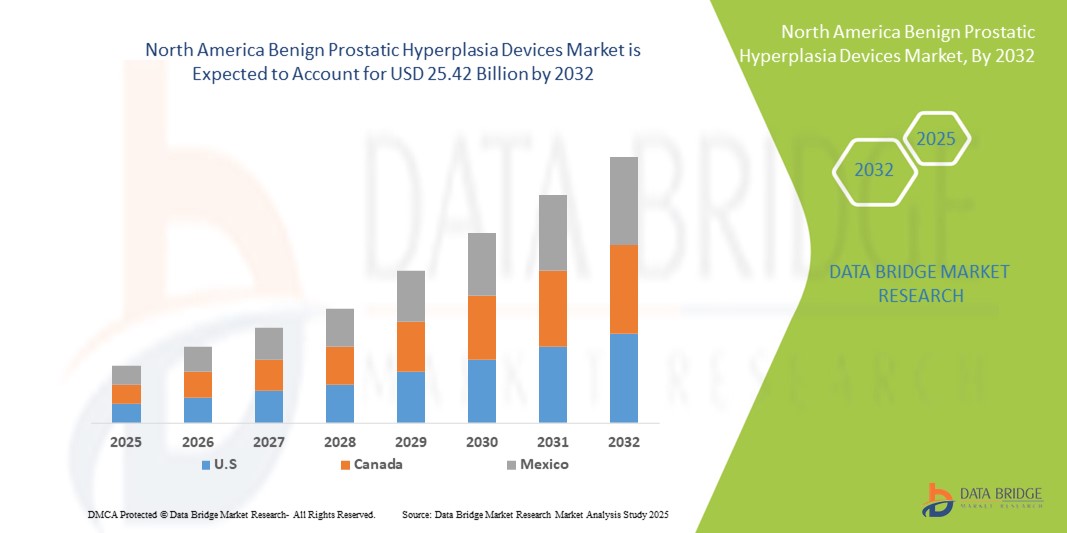

- The North America benign prostatic hyperplasia devices market size was valued at USD 9.98 billion in 2024 and is expected to reach USD 25.42 billion by 2032, at a CAGR of 12.40% during the forecast period

- The market growth is largely fueled by the increasing prevalence of benign prostatic hyperplasia among the aging male population, coupled with the rising demand for minimally invasive treatment options that reduce hospital stays and recovery time

- Furthermore, continuous advancements in medical device technologies, such as prostatic urethral lift systems and laser therapy devices, are enhancing treatment outcomes and patient comfort. These converging factors are accelerating the adoption of BPH devices, thereby significantly boosting the industry's growth

North America Benign Prostatic Hyperplasia Devices Market Analysis

- Benign Prostatic Hyperplasia (BPH) devices, offering advanced minimally invasive and surgical solutions for prostate enlargement, are increasingly vital in modern urological care due to their effectiveness in symptom relief, reduced hospitalization, and enhanced patient outcomes

- The escalating demand for BPH devices is primarily fueled by the rising prevalence of prostate disorders among aging male populations, technological advancements in minimally invasive therapies, and growing awareness among both physicians and patients of superior treatment options

- U.S. dominated the benign prostatic hyperplasia devices market with the largest revenue share of 86.8% in 2024, characterized by its advanced healthcare infrastructure, high prevalence of prostate conditions, and strong adoption of innovative minimally invasive treatment devices, supported by continuous product launches and robust reimbursement frameworks

- Canada is expected to be the fastest-growing country in the benign prostatic hyperplasia devices market during the forecast period, projected to register a strong CAGR driven by increasing access to urological care, growing government initiatives to improve men’s health services, and rising adoption of minimally invasive technologies across hospitals and specialty clinics

- The Transurethral Resection of the Prostate (TURP) segment dominated the benign prostatic hyperplasia devices market with the largest market revenue share of 38.5% in 2024, owing to its long-established status as the gold-standard surgical treatment for BPH. TURP procedures remain highly preferred by urologists because of their effectiveness in significantly reducing symptoms of urinary retention and obstruction

Report Scope and Benign Prostatic Hyperplasia Devices Market Segmentation

|

Attributes |

Benign Prostatic Hyperplasia Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

North America Benign Prostatic Hyperplasia Devices Market Trends

Advancements in Minimally Invasive and Laser-Based Therapies

- A significant and accelerating trend in the North America benign prostatic hyperplasia (BPH) devices market is the growing adoption of minimally invasive and laser-based therapies, such as transurethral resection of the prostate (TURP), UroLift, and GreenLight laser treatment. These procedures are gaining popularity due to their ability to provide effective symptom relief while reducing hospital stays, blood loss, and recovery time

- For instance, in March 2023, Teleflex Incorporated (U.S.) announced expanded availability of its UroLift System across North American healthcare centers, following strong clinical evidence supporting its role as a safe, minimally invasive alternative to traditional surgery. Such product rollouts are strengthening the market presence of leading companies

- The adoption of next-generation devices is also being driven by the rising incidence of prostate enlargement in aging male populations. According to the American Urological Association, nearly 50% of men over the age of 60 are affected by benign prostatic hyperplasia, creating a substantial patient pool for advanced treatment options

- Furthermore, growing preference among patients for outpatient and day-care procedures is encouraging hospitals and specialty clinics to expand their portfolios of minimally invasive BPH devices. Reimbursement coverage in the U.S. for advanced surgical therapies is also positively influencing adoption rates

- The North American market is also witnessing strong investments in research and development for new device technologies, such as water vapor therapy and laser enucleation systems, which aim to further reduce side effects while improving clinical outcomes. These innovations are attracting significant attention from both healthcare providers and patients

- The demand for Benign Prostatic Hyperplasia Devices that offer faster recovery, reduced complications, and enhanced quality of life is growing rapidly across hospitals, ambulatory surgical centers, and specialty clinics, reinforcing the market’s steady growth trajectory

North America Benign Prostatic Hyperplasia Devices Market Dynamics

Driver

Growing Prevalence of BPH and Rising Demand for Minimally Invasive Treatments

- The rising prevalence of benign prostatic hyperplasia among the global aging male population is one of the most significant drivers of market growth. With increasing life expectancy, the number of men suffering from urinary retention, bladder obstruction, and related complications continues to expand, fueling the demand for effective treatment devices

- For instance, in May 2022, PROCEPT BioRobotics announced positive adoption trends of its Aquablation Therapy system, highlighting strong growth momentum in hospitals and surgical centers. Such advancements underscore the growing preference for innovative and minimally invasive BPH devices

- Minimally invasive procedures such as laser therapy, prostatic urethral lift (PUL), and robotic-assisted surgeries are gaining traction as they provide faster recovery, shorter hospital stays, and fewer complications compared to traditional open surgeries

- Furthermore, the introduction of advanced technologies—such as robotic systems, improved stent designs, and precision laser therapies—are expanding treatment options for patients and supporting wider adoption by healthcare providers

- The combination of clinical benefits, rising awareness, and technological innovation is propelling the uptake of BPH devices across hospitals, ambulatory surgical centers, and specialty urology clinics

Restraint/Challenge

High Cost of Advanced Devices and Limited Access in Developing Regions

- One of the major restraints for the Benign Prostatic Hyperplasia Devices Market is the high cost associated with advanced treatment systems such as laser therapy platforms, robotic-assisted surgical devices, and innovative prostatic implants. These systems often require significant capital investment from hospitals and surgical centers, which can act as a barrier for adoption—particularly in small to mid-sized healthcare facilities. The costs are not limited to device acquisition but also extend to installation, maintenance, and consumables, which further adds to the financial burden

- For instance, robotic-assisted BPH surgeries, while clinically effective, are substantially more expensive than traditional transurethral resection of the prostate (TURP), making it difficult for many institutions to justify widespread adoption, especially in regions with constrained healthcare budgets

- Another critical challenge lies in the limited reimbursement frameworks for minimally invasive BPH procedures across several countries. In many developing markets, advanced device-based treatments are either partially reimbursed or not covered at all, leading to higher out-of-pocket costs for patients. This reduces the affordability of modern BPH therapies and restricts their use to wealthier segments of the population, leaving a large pool of patients reliant on older, more invasive surgical methods

- Moreover, there is a shortage of skilled urologists trained in the use of modern devices in emerging markets. Advanced procedures such as prostatic urethral lift or laser vaporization require specialized expertise, and the lack of training opportunities limits the penetration of these devices in low-resource settings

- These combined factors—high upfront cost, inadequate reimbursement, and shortage of skilled professionals—create a significant barrier to market growth. To overcome these restraints, manufacturers and healthcare stakeholders will need to work together to reduce equipment costs, expand training programs for urologists, and advocate for stronger reimbursement support. Without addressing these challenges, the full clinical and commercial potential of BPH devices may remain underutilized, especially in regions with the fastest-growing patient populations

North America Benign Prostatic Hyperplasia Devices Market Scope

The market is segmented on the basis of procedure type and end-user.

- By Procedure Type

On the basis of procedure type, the benign prostatic hyperplasia devices market is segmented into Transurethral Resection of the Prostate (TURP), Prostatic Urethral Lift (PUL), Prostatectomy, Laser Surgery, Transurethral Microwave Therapy (TUMT), Transurethral Needle Ablation of the Prostate (TUNA), Prostatic Stenting/Implants, and Others. The TURP segment accounted for the largest market revenue share of 38.5% in 2024, owing to its long-established status as the gold-standard surgical treatment for BPH. TURP procedures remain highly preferred by urologists because of their effectiveness in significantly reducing symptoms of urinary retention and obstruction. Strong clinical outcomes, widespread reimbursement coverage, and the presence of well-trained surgeons across North America contribute to the continued dominance of TURP. In addition, TURP is widely available in hospitals and surgical centers, ensuring accessibility even in smaller facilities. Despite emerging minimally invasive alternatives, the proven efficacy and reliability of TURP help it retain its leadership position in the BPH devices market.

The PUL segment is projected to witness the fastest CAGR of 22.1% from 2025 to 2032, driven by the growing demand for minimally invasive treatments that preserve sexual function and offer shorter recovery times. The UroLift system, a leading PUL device, has gained rapid acceptance across urology practices in North America due to its safety profile and outpatient procedure advantages. Patients are increasingly seeking treatments that minimize hospital stays, which favors PUL adoption in both hospital and ambulatory settings. Moreover, ongoing clinical studies and expanding FDA indications are expected to further support adoption. Insurance coverage is also improving, which will likely accelerate patient access and help PUL achieve the highest growth rate among all procedure types.

- By End-User

On the basis of end-user, the benign prostatic hyperplasia devices market is segmented into hospitals and clinics, ambulatory surgical centers, and others. The hospitals and clinics segment held the largest revenue share of 65.7% in 2024, primarily due to the availability of advanced infrastructure and specialized urology departments in North American hospitals. Patients often prefer hospitals for BPH procedures because of the comprehensive care, access to experienced surgeons, and better post-operative monitoring facilities. Hospitals also benefit from established reimbursement mechanisms for TURP, laser therapies, and other BPH procedures, making them the primary treatment centers. Additionally, the presence of advanced surgical tools, robotic systems, and specialized medical staff in hospital environments further supports the dominance of this segment. The ability to manage complications and comorbidities in a hospital setting also enhances patient trust and preference for hospital-based procedures.

The ambulatory surgical centers segment is expected to register the fastest CAGR of 18.6% from 2025 to 2032, fueled by the rising trend of minimally invasive, same-day BPH procedures. ASCs are increasingly being chosen by both patients and physicians for their cost-effectiveness, reduced waiting times, and faster turnaround. Procedures such as PUL and laser therapies are well-suited for ASCs, as they can often be completed within a few hours with minimal post-operative monitoring. The growing emphasis on reducing hospital stays and overall healthcare costs is pushing insurers and payers to encourage ASC-based treatments. Furthermore, the expansion of outpatient urology practices across the U.S. and Canada is expected to drive sustained growth in this segment throughout the forecast period.

North America Benign Prostatic Hyperplasia Devices Market Regional Analysis

- North America dominated the benign prostatic hyperplasia devices market with the largest revenue share in 2024, driven by advanced healthcare systems, rising prevalence of BPH among the aging male population, and strong adoption of innovative minimally invasive treatment devices such as laser therapies, UroLift, and water vapor therapy systems

- The demand in the region is further accelerated by high healthcare spending, growing awareness of advanced treatment options, and supportive reimbursement frameworks, which together strengthen patient access to modern BPH solutions

- Increasing product launches by leading medical device companies and ongoing clinical studies in North America are further fueling adoption, establishing the region as a global hub for innovative BPH treatment technologies

U.S. Benign Prostatic Hyperplasia Devices Market Insight

The U.S. benign prostatic hyperplasia devices market dominated the benign prostatic hyperplasia devices market with the largest revenue share of 86.8% in 2024, characterized by its advanced healthcare infrastructure, high prevalence of prostate conditions, and strong adoption of innovative minimally invasive treatment devices. The market growth is supported by continuous product launches, favorable reimbursement frameworks, and increasing patient preference for outpatient procedures. The U.S. also benefits from strong investments in R&D and rapid regulatory approvals, ensuring early access to the latest device-based therapies for BPH.

Canada Benign Prostatic Hyperplasia Devices Market Insight

The Canada benign prostatic hyperplasia devices market is expected to be the fastest-growing country in the benign prostatic hyperplasia devices market during the forecast period, projected to register a strong CAGR. Growth is driven by expanding access to urological care, rising awareness of men’s health issues, and government initiatives aimed at improving treatment accessibility. The increasing adoption of minimally invasive technologies in hospitals and specialty clinics, combined with rising healthcare expenditure, is expected to make Canada a key contributor to the region’s future market expansion.

North America Benign Prostatic Hyperplasia Devices Market Share

The benign prostatic hyperplasia devices industry is primarily led by well-established companies, including:

- KARL STORZ (Germany)

- OmniGuide Holdings, Inc. (U.S.)

- Olympus Corporation (Japan)

- Richard Wolf GmbH (Germany)

- Lumenis Be Ltd. (Israel)

- Urologix, LLC (U.S.)

- Boston Scientific Corporation (U.S.)

- Coloplast Corp (U.S.)

- Medifocus Inc. (U.S.)

- biolitec AG (Germany)

- Teleflex Incorporated (U.S.)

- Urotech Devices (Singapore)

- PROCEPT BioRobotics Corporation (U.S.)

Latest Developments in North America Benign Prostatic Hyperplasia Devices Market

- In April 2025, Rivermark Medical announced that its minimally invasive nitinol FloStent System had begun enrollment in its pivotal RAPID III clinical trial in North America. Delivered via routine cystoscopy in an outpatient setting, the FloStent is a non-surgical, reversible treatment that gently relieves lower urinary tract symptoms (LUTS) with minimal tissue damage. The first patient was treated in Las Vegas, and the multicenter study plans to enroll 215 patients across the U.S. and Australia

- In December 2024, Teleflex Incorporated received FDA clearance and announced the upcoming full market release of the UroLift 2 System with Advanced Tissue Control (ATC). Building on the established UroLift platform, the ATC version introduces a unified delivery system designed for treating all prostate anatomies up to 100g. Innovations include tissue control wings and laser-etched needle markers for enhanced accuracy, a streamlined one-handle, individual implant cartridge delivery system for procedural efficiency, and expanded physician versatility

- In March 2024, Olympus achieved a major distribution milestone for its iTind device, a minimally invasive, temporarily implanted nitinol device for treating BPH. Olympus announced that iTind became available through 13 major U.S. healthcare Group Purchasing Organization (GPO) contracts—dramatically expanding patient and physician access across hospitals, ambulatory surgical centers, and other care facilities

- In October 2023, the FDA approved the Optilume BPH catheter system, a novel outpatient treatment for enlarged prostates. The system uses an inflatable catheter that splits the prostate lobes and releases paclitaxel to reduce inflammation and maintain patency. Clinical trial data presented at the American Urological Association (AUA) meeting showed sustained symptom relief—including lower International Prostate Symptom Score (IPSS) values—persisting for up to four years. Experts have heralded Optilume as a potential game changer in BPH therapy

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.