North America Bio Implants Market

Market Size in USD Billion

USD

126.47 Billion

USD

235.82 Billion

2025

2033

USD

126.47 Billion

USD

235.82 Billion

2025

2033

| 2026 - 2033 | |

| USD 126.47 Billion | |

| USD 235.82 Billion | |

| % | |

|

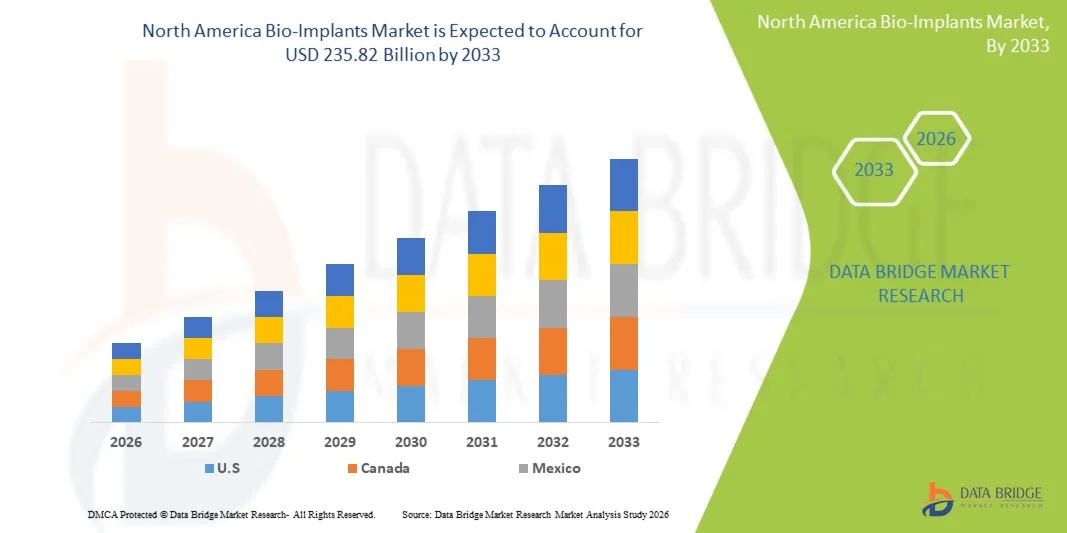

North America Bio-Implants Market Size

- The North America bio-implants market size was valued at USD 126.47 billion in 2025 and is expected to reach USD 235.82 billion by 2033, at a CAGR of 8.1% during the forecast period

- The market growth is largely fueled by advanced healthcare infrastructure, high volumes of surgical procedures and rapid technological progress in implant technologies such as 3D‑printed and biomaterial‑based implants, enhancing outcomes across orthopedic, dental, cardiovascular, and other clinical applications

- Furthermore, rising prevalence of chronic diseases, an aging population with increasing demand for joint replacements and reconstructive implants, and widespread adoption of innovative, patient‑centric bio‑implant solutions are establishing bio‑implants as essential components of modern medical care in North America. These converging factors are accelerating uptake across clinical settings, thereby significantly boosting the industry’s growth

North America Bio-Implants Market Analysis

- Bio‑implants, including orthopedic, dental, cardiovascular, and reconstructive implants, are increasingly vital components of modern medical care in both hospitals and outpatient settings due to their ability to restore function, improve patient outcomes, and integrate with advanced surgical technologies

- The escalating demand for bio‑implants is primarily fueled by the growing prevalence of chronic diseases, an aging population requiring joint replacements and reconstructive procedures, and the adoption of advanced materials and 3D‑printed implant technologies

- The United States dominated the North America bio‑implants market with the largest revenue share of 70.2% in 2025, characterized by advanced healthcare infrastructure, high surgical procedure volumes, and a strong presence of key industry players, with substantial growth in orthopedic and cardiovascular implant procedures driven by innovations from both established medtech companies and startups focusing on biomaterials and patient-specific implant solutions

- Canada is expected to be the fastest-growing country in North America bio‑implants market during forecast period, due to increasing surgical procedures among an aging population, well-developed healthcare infrastructure, and rising adoption of technologically advanced and minimally invasive implant solutions

- Orthopaedics and Trauma segment dominated the North America bio‑implants market with a market share of 38.8% in 2025, driven by high demand for joint replacements and spinal implants, along with their established clinical effectiveness and reliability

Report Scope and North America Bio-Implants Market Segmentation

|

Attributes |

North America Bio-Implants Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

North America Bio-Implants Market Trends

“Advancements in 3D-Printed and Patient-Specific Implants”

- A significant and accelerating trend in the North America bio‑implants market is the increasing adoption of 3D-printed and patient-specific implants, enabling highly personalized surgical solutions and improved post-operative outcomes

- For instance, Stryker’s 3D-printed knee and spinal implants are tailored to match individual patient anatomy, reducing recovery time and enhancing implant performance

- Advanced imaging and modeling technologies allow bio-implant manufacturers to design implants that fit precisely, improving surgical efficiency and minimizing complications

- This trend facilitates customized surgical planning and better integration with minimally invasive procedures, resulting in more predictable clinical results

- The shift towards patient-specific implants is driving manufacturers to invest in R&D and digital design platforms, such as Materialise’s 3D surgical modeling solutions

- The demand for bio-implants that are highly customized and compatible with advanced surgical techniques is growing rapidly across both hospitals and outpatient surgical centers

- Integration of smart bio-implants with sensors and monitoring devices is emerging, allowing post-surgical tracking of implant performance and patient recovery

- Collaborations between implant manufacturers and tech companies are expanding, promoting innovation in materials, designs, and surgical workflows

North America Bio-Implants Market Dynamics

Driver

“Increasing Surgical Procedures and Aging Population”

- The rising number of orthopedic, cardiovascular, and dental surgical procedures, coupled with a growing aging population, is a major driver for bio‑implant demand

- For instance, in March 2025, Zimmer Biomet launched advanced joint replacement solutions for hip and knee surgeries in the U.S., targeting the growing elderly patient base

- Patients are seeking durable and reliable implants to restore mobility and improve quality of life, driving adoption of high-performance bio-implants

- In addition, the growth of minimally invasive and technologically advanced procedures is increasing the need for sophisticated implant solutions

- Hospitals and surgical centers are increasingly integrating bio-implants into patient care programs due to improved clinical outcomes and reduced post-surgical complications

- Rising government healthcare spending and reimbursement policies for implant surgeries further encourage adoption of advanced bio-implant solutions

- Increasing awareness among patients and surgeons about the benefits of innovative implants is boosting demand for newer technologies and materials

- Technological collaborations between medtech companies and hospitals are driving faster adoption of next-generation implant solutions in key U.S. markets

Restraint/Challenge

“High Costs and Regulatory Compliance Hurdles”

- The high costs of advanced bio-implants and stringent regulatory requirements pose a significant challenge to market expansion in North America

- For instance, the FDA’s rigorous approval process for new implant materials and designs often delays product launches and increases compliance costs

- The premium pricing of custom and 3D-printed implants can limit adoption among smaller hospitals or budget-conscious patients

- Ensuring safety, biocompatibility, and long-term performance requires extensive testing, adding to manufacturing and regulatory burdens

- Manufacturers must balance innovation with cost-effectiveness, while navigating complex regulatory frameworks to gain approval and maintain market trust

- Potential post-surgical complications and liability concerns create hesitation among healthcare providers to adopt newer implant technologies quickly

- Supply chain disruptions for specialized implant materials can lead to production delays, affecting market availability and growth

- Lack of standardized training for surgeons on advanced implant technologies can slow adoption despite clinical benefits, posing a challenge for manufacturers

North America Bio-Implants Market Scope

The market is segmented on the basis of product type, type of graft, material, mode of administration, and end-user.

- By Product Type

On the basis of product type, the North America bio‑implants market is segmented into orthopaedics and trauma, pacing devices, stents and related implants, spinal implants, ophthalmic implants, structural cardiac implants, dental implants, neurostimulators implants, and prosthetic implants. The Orthopaedics and Trauma segment dominated the market with the largest revenue share of 38.8% in 2025, driven by high volumes of joint replacement surgeries, fracture repairs, and the prevalence of musculoskeletal disorders in an aging population. Hospitals and surgical centers often prioritize orthopedic implants due to their proven clinical outcomes and the high demand for durable, long-lasting solutions. The segment also benefits from the increasing adoption of minimally invasive orthopedic procedures and advanced implant materials such as titanium alloys and 3D-printed devices. Orthopedic implants have a well-established supply chain, strong surgeon familiarity, and consistent reimbursement coverage, further consolidating their market dominance.

The Spinal Implants segment is anticipated to witness the fastest growth rate of 12% from 2026 to 2033, fueled by rising incidence of spinal disorders, technological advancements in spinal fixation systems, and the growing preference for minimally invasive spinal procedures. Innovative implants such as 3D-printed vertebral cages and patient-specific spinal rods are driving adoption. The increase in spinal surgeries among aging populations and sports-related injuries contributes to sustained demand. The growing awareness among surgeons and patients regarding the benefits of advanced spinal implants is also accelerating uptake.

- By Type

On the basis of graft type, the market is segmented into allograft, autograft, xenograft, and synthetic. The Allograft segment dominated the market in 2025, accounting for the largest revenue share, due to the availability of donor tissues and wide application in orthopedic and dental surgeries. Allografts reduce operative time, eliminate donor site morbidity, and are clinically proven for bone and tissue regeneration. Hospitals prefer allografts for their accessibility, reliability, and standardized processing protocols. Regulatory approval frameworks and tissue banks support consistent supply, enhancing market confidence.

The Synthetic graft segment is expected to witness the fastest CAGR from 2026 to 2033, driven by innovations in biomaterials, biocompatible polymers, and hydrogel-based scaffolds. Synthetic grafts offer advantages such as reduced risk of disease transmission, tailored mechanical properties, and compatibility with minimally invasive procedures. They are increasingly used in orthopedic, dental, and cardiovascular applications. Advancements in tissue engineering and 3D printing are accelerating the development and adoption of synthetic implants.

- By Material

On the basis of material, the market is segmented into biomaterial metal, alloy, polymer, ceramics, and acrylic hydrogel. The Biomaterial Metal segment dominated the market in 2025, owing to its superior strength, durability, and compatibility for orthopedic, dental, and cardiovascular implants. Metals such as titanium and stainless steel are widely used for joint replacements, fracture fixation, and cardiovascular stents. Hospitals prefer metallic implants for their long-term reliability and proven clinical performance. Strong manufacturing infrastructure and surgeon familiarity reinforce their dominance.

The Polymer segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by innovations in biocompatible polymers for orthopedic, dental, and spinal applications. Polymers enable lightweight, flexible, and patient-specific implants, often in combination with 3D printing. Growing research in polymer composites and biodegradable materials is fueling adoption. Polymers also support drug-eluting implants and minimally invasive procedures, expanding their application scope.

- By Mode of Administration

On the basis of mode of administration, the market is segmented into surgical and non-surgical. The Surgical segment dominated the market with the largest revenue share in 2025 due to the high volume of hospital-based procedures requiring implantation of devices such as orthopedic, spinal, dental, and cardiovascular implants. Surgical implants provide precise placement, structural support, and improved patient outcomes. Surgeons favor surgical implants for complex procedures where stability and integration are critical. Established surgical protocols, reimbursement policies, and high adoption rates in hospitals reinforce this segment’s dominance.

The Non-Surgical segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the development of minimally invasive and percutaneous implantable devices such as certain stents, pacing devices, and neuromodulators. Non-surgical implants reduce hospital stays, improve patient recovery, and are increasingly preferred in outpatient and ambulatory surgical centers. Technological advances enabling remote monitoring and minimally invasive placement are accelerating adoption.

- By End-User

On the basis of end-user, the market is segmented into clinics, hospitals, and ambulatory surgical centres. The Hospitals segment dominated the North America bio‑implants market in 2025, accounting for the largest revenue share, due to the high volume of complex procedures, well-established infrastructure, and the availability of specialized surgical teams. Hospitals are equipped to handle multi-disciplinary implant surgeries including orthopedic, cardiovascular, spinal, and dental procedures. Strong insurance coverage and reimbursement systems further support hospital adoption.

The Ambulatory Surgical Centres segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing preference for outpatient surgeries, cost-effective procedures, and minimally invasive implant technologies. Rising patient demand for shorter hospital stays and faster recovery is encouraging the use of ASCs for joint replacements, dental implants, and minor orthopedic procedures. Growth in healthcare investments and expansion of ASC facilities are further supporting market adoption.

North America Bio-Implants Market Regional Analysis

- The United States dominated the North America bio‑implants market with the largest revenue share of 70.2% in 2025, characterized by advanced healthcare infrastructure, high surgical procedure volumes, and a strong presence of key industry players

- Patients and healthcare providers in the region highly value the reliability, clinical effectiveness, and technological advancements offered by bio‑implants, including 3D-printed, patient-specific, and minimally invasive solutions

- This widespread adoption is further supported by strong insurance coverage, government healthcare spending, an aging population with rising implant needs, and a growing focus on improving patient outcomes, establishing bio‑implants as essential components in hospitals, clinics, and ambulatory surgical centers across the United States

The U.S. Bio‑Implants Market Insight

The U.S. bio‑implants market captured the largest revenue share of 70.2% in 2025 within North America, fueled by the high volume of orthopedic, cardiovascular, and dental surgical procedures. Patients and healthcare providers increasingly prioritize advanced implant solutions, such as 3D-printed, patient-specific, and minimally invasive devices, to improve outcomes and reduce recovery time. The growing trend of technologically advanced surgeries, combined with strong insurance coverage and government healthcare spending, further propels the market. Moreover, collaborations between medtech companies and hospitals, as well as innovations in biomaterials and surgical planning software, are significantly contributing to market expansion.

Canada Bio‑Implants Market Insight

The Canada bio‑implants market is witnessing steady growth, driven by the country’s well-developed healthcare system, increasing surgical procedures among an aging population, and rising adoption of advanced implant technologies. Canadian hospitals and clinics prioritize implants that offer reliable clinical outcomes and compatibility with minimally invasive procedures. In addition, awareness among patients and surgeons regarding the benefits of innovative bio-implant solutions is supporting market growth. Government healthcare programs and reimbursement policies further enhance accessibility and adoption of bio-implants across the country.

Mexico Bio‑Implants Market Insight

The Mexico bio‑implants market is emerging as a key growth region within North America, fueled by increasing investments in healthcare infrastructure and rising awareness of advanced surgical treatments. The growing prevalence of musculoskeletal disorders and cardiovascular conditions is driving demand for implants in both hospitals and specialized surgical centers. In addition, initiatives to modernize healthcare facilities and train surgeons in advanced implant procedures are accelerating adoption. Mexico’s increasing medical tourism sector also supports demand for high-quality, technologically advanced bio-implant solutions.

North America Bio-Implants Market Share

The North America Bio-Implants industry is primarily led by well-established companies, including:

- Stryker (U.S.)

- Medtronic (U.S.)

- Boston Scientific Corporation (U.S.)

- Abbott (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Zimmer Biomet (U.S.)

- BioHorizons Implant Systems Incorporated (U.S.)

- Glidewell Dental (U.S.)

- Envista Holdings Corporation (U.S.)

- Implant Direct (U.S.)

- LifeNet Health, Inc. (U.S.)

- Integra LifeSciences Corporation (U.S.)

- Globus Medical, Inc. (U.S.)

- Orthofix Medical Inc. (U.S.)

- RTI Surgical Holdings, Inc. (U.S.)

- NuVasive, Inc. (U.S.)

- Cook Medical LLC (U.S.)

- Smith+Nephew (U.S.)

- CONMED Corporation (U.S.)

What are the Recent Developments in North America Bio-Implants Market?

- In November 2025, Paradromics, an Austin‑based neurotechnology company, received U.S. FDA approval to begin its first long‑term clinical trial of the Connexus Brain‑Computer Interface (BCI), a brain‑implantable device designed to help people who have lost the ability to speak due to neurological conditions or injury, marking a major step forward in neuro‑implant innovation and human efficacy testing

- In February 2025, Atreon Orthopedics, LLC received 510(k) FDA clearance and fully launched the BioCharge Autobiologic Matrix, a bioresorbable synthetic implant designed to improve rotator cuff repair integrity and long‑term patient outcomes, marking a key innovation in regenerative orthopedic treatments

- In December 2024, Zimmer Biomet received FDA clearance for the OsseoFit™ Stemless Shoulder System, an innovative implant that optimizes fit while preserving healthy bone using advanced porous metal technology, expected to be available commercially in early 2025 and enhancing shoulder reconstruction

- In September 2024, Establishment Labs Holdings, Inc. received U.S. FDA approval for Motiva SmoothSilk Ergonomix and Round breast implants for primary and revision augmentation, marking the first new breast implant PMA approval in the U.S. in over a decade and expanding the reconstructive implant landscape

- In March 2023, Bioretec Ltd became the first company worldwide to receive FDA approval for a bioresorbable metal orthopedic implant (RemeOs™ trauma screw), offering an alternative to traditional metal hardware that may eliminate the need for removal surgery after bone fracture healing

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.