North America Bladder Disorders Market

Market Size in USD Billion

USD

6.76 Billion

USD

16.49 Billion

2025

2033

USD

6.76 Billion

USD

16.49 Billion

2025

2033

| 2026 - 2033 | |

| USD 6.76 Billion | |

| USD 16.49 Billion | |

| % | |

|

North America Bladder Disorders Market Overview

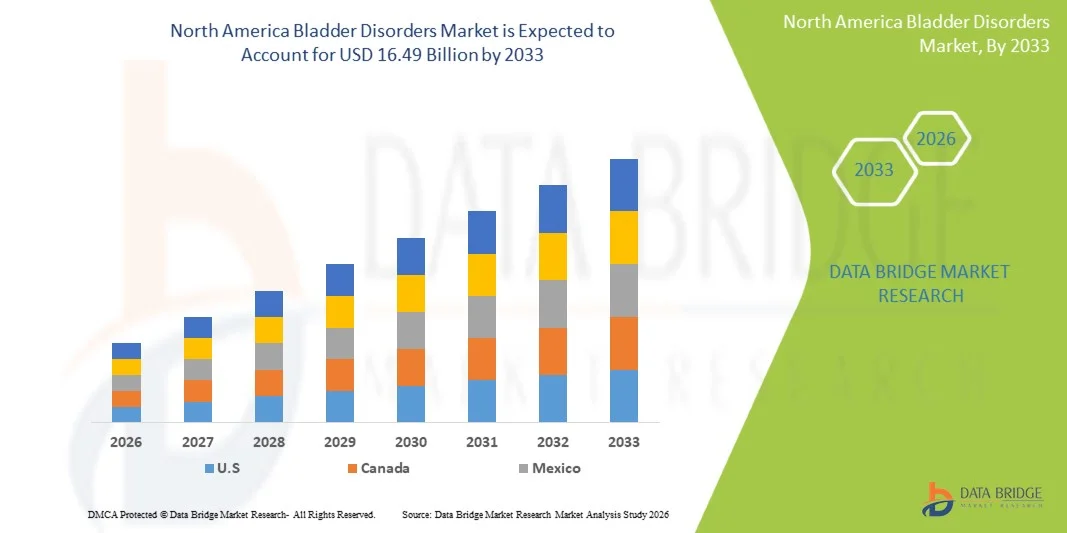

The North America bladder disorders market was valued at USD 6.76 billion in 2025 and is projected to reach USD 16.49 billion by 2033, growing at a CAGR of 11.80% from 2026 to 2033. The market is experiencing steady growth driven by the rising prevalence of bladder-related conditions, increasing awareness of urinary health, and continuous advancements in diagnostic and therapeutic technologies.

The growing burden of disorders such as overactive bladder, urinary incontinence, interstitial cystitis, and bladder cancer, coupled with an aging population and changing lifestyle patterns, is encouraging healthcare providers to adopt advanced treatment approaches. Favorable reimbursement frameworks, strong healthcare infrastructure, and increasing availability of minimally invasive procedures are supporting market expansion across the region. Additionally, ongoing research activities, product innovations, and the introduction of novel pharmaceuticals and neuromodulation therapies are improving patient outcomes and driving the adoption of effective bladder disorder management solutions.

Key Market Trends & Insights

- The United States dominated the North America bladder disorders market with the largest revenue share of 82.4% in 2025, supported by a high prevalence of urinary disorders, advanced healthcare infrastructure, strong reimbursement coverage, and early adoption of innovative treatment technologies.

- The Overactive Bladder segment led the market with a 36.8% share in 2025, driven by its high prevalence among aging populations and increasing diagnosis rates across the United States.

- Canada is expected to be the fastest-growing country in the region, registering a CAGR of 5.9% from 2026 to 2033, fueled by increasing healthcare investments, rising awareness of urinary health conditions, and expanding access to specialized urology services.

- Bladder Cancer are the fastest-growing type, projected to register a CAGR of 6.2%, reflecting the surge in incidence rates and advancements in early detection technologies

- The Medication segment dominated the treatment type category with a 48.3% revenue share in 2025, led by its role as the first-line treatment for most bladder disorders such as overactive bladder and urinary incontinence.

- Cystoscopy accounted for 31.5% of the market, preferred by its high diagnostic accuracy and widespread use in evaluating bladder abnormalities.

- The Urodynamic Testing segment is the fastest-growing diagnosis category, with a CAGR of 6.3%, driven by the increasing demand for functional assessment of bladder performance.

Market Size & Forecast

- Global Market Value (2025): USD 6.76 Billion

- Expected Market Value (2033): USD 16.49 Billion

- Forecast CAGR (2026–2033): 11.80%

- Leading Country in 2025: United States

- Fastest Growing Country: Canada

Report Scope and North America Bladder Disorders Market Segmentation

|

Attributes |

North America Bladder Disorders Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico |

|

Key Market Players |

· Astellas Pharma Inc. (Japan) · Pfizer Inc. (U.S.) · AbbVie Inc. (U.S.) · Bayer AG (Germany) · Johnson & Johnson Services, Inc. (U.S.) · Boston Scientific Corporation (U.S.) · Medtronic (Ireland) · Coloplast A/S (Denmark) · Teleflex Incorporated (U.S.) · BD (U.S.) · Hollister Incorporated (U.S.) · Cook (U.S.) · Laborie Medical Technologies Corp. (Canada) · UroMems SAS (France) · Olympus Corporation (Japan) · Karl Storz SE & Co. KG (Germany) · Ferring Pharmaceuticals (Switzerland) · Ipsen (France) · Recordati S.p.A. (Italy) · Pierre Fabre Médicament (France) |

|

Market Opportunities |

· Expanding adoption of sacral neuromodulation and tibial nerve stimulation therapies · Growing demand for home-based bladder monitoring and digital health solutions · Increasing investment in regenerative medicine and next-generation biologic therapies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

North America Bladder Disorders Market Trends

Trend: Growth in Advanced Urology Care & Minimally Invasive Treatments

The North America bladder disorders market is witnessing strong adoption of minimally invasive and precision-based treatment approaches to improve patient outcomes and reduce hospital stays. Clinicians are increasingly using neuromodulation therapies, botulinum toxin injections, and advanced diagnostic tools to manage complex conditions such as overactive bladder and urinary incontinence. Integration of digital health monitoring and tele-urology solutions is further enhancing patient follow-up and long-term disease management, while improving treatment adherence across aging populations. For instance, the increasing use of sacral neuromodulation systems in specialized urology centers highlights this shift toward technology-driven bladder disorder management.

North America Bladder Disorders Market Dynamics

Key Market Driver: Rising Prevalence of Chronic Bladder Disorders & Aging Population

The growing burden of chronic bladder conditions, particularly among the elderly population, is significantly driving demand for advanced diagnostic and therapeutic solutions across North America. Increasing incidence of conditions such as overactive bladder, interstitial cystitis, and urinary incontinence is prompting higher clinical consultations and treatment adoption rates. Strong healthcare infrastructure, high awareness levels, and favorable reimbursement policies further support early diagnosis and treatment uptake. For instance, the rising diagnosis rates of overactive bladder in the United States reflect the expanding patient pool requiring long-term therapeutic management.

Key Restraint/Challenge: High Cost of Advanced Therapies & Limited Accessibility in Certain Segments

A key restraint in the North America bladder disorders market is the high cost associated with advanced treatment options such as neuromodulation devices, biologic therapies, and minimally invasive surgical procedures. These treatments often require specialized infrastructure, trained professionals, and ongoing maintenance, which increases overall healthcare expenditure. Additionally, access disparities persist among uninsured or underinsured populations, limiting widespread adoption of advanced care solutions. For instance, the high procedural cost of implantable bladder stimulation devices restricts their uptake primarily to well-funded hospitals and specialized urology centers.

Key Market Opportunity: Expansion of Personalized Medicine & Digital Urology Solutions

The integration of personalized medicine approaches and digital health technologies presents a major growth opportunity in the North America bladder disorders market. AI-driven diagnostic tools, remote patient monitoring systems, and data-enabled treatment planning are improving precision in disease management and patient outcomes. Pharmaceutical companies and medtech firms are increasingly focusing on biomarker-based therapies and individualized treatment protocols to enhance efficacy. For instance, the adoption of remote bladder health monitoring applications in post-treatment care is improving long-term disease tracking and reducing hospital readmissions.

North America Bladder Disorders Market Scope

The North America bladder disorders market is segmented on the basis of type, treatment type, diagnosis, end user, and distribution channel.

- By Type

On the basis of type, the North America bladder disorders market is segmented into cystitis, urinary incontinence, overactive bladder, interstitial cystitis, and bladder cancer. The Overactive Bladder (OAB) segment dominated the market with a share of 36.8% in 2025, owing to its high prevalence among aging populations and increasing diagnosis rates across the United States. This condition is widely recognized due to its significant impact on quality of life, leading to frequent clinical consultations. Strong availability of pharmacological therapies and neuromodulation treatments further strengthens its dominance. Rising awareness programs and improved diagnostic access are increasing patient identification rates. Continuous innovation in long-term management therapies is also supporting sustained demand. For instance, growing use of antimuscarinic and beta-3 agonist drugs highlights strong treatment adoption in clinical practice.

The Bladder Cancer segment is projected to register the fastest growth at a CAGR of 6.2% from 2026 to 2033, driven by rising incidence rates and advancements in early detection technologies. Increasing adoption of immunotherapy and targeted therapy is improving survival outcomes and treatment effectiveness. Enhanced screening programs and biomarker-based diagnostics are enabling earlier intervention. Growing investment in oncology research is also supporting pipeline development. Rising awareness about hematuria and urinary symptoms is encouraging timely diagnosis. For instance, increased use of cystoscopy-based screening in high-risk populations is accelerating early-stage detection.

- By Treatment Type

On the basis of treatment type, the market is segmented into surgery, medication, and non-surgical approaches. The Medication segment led the market with a share of 48.3% in 2025, driven by its role as the first-line treatment for most bladder disorders such as overactive bladder and urinary incontinence. Pharmacological therapies are widely prescribed due to ease of administration and strong clinical efficacy. Increasing availability of beta-3 adrenergic agonists and anticholinergic drugs is supporting market dominance. High patient preference for non-invasive treatment options further strengthens adoption. Continuous drug innovation is improving symptom control and reducing side effects. For instance, widespread prescription of mirabegron-based therapies reflects strong pharmaceutical penetration.

The Non-surgical treatment segment is expected to witness the fastest growth at a CAGR of 6.5% from 2026 to 2033, driven by increasing demand for minimally invasive and outpatient-based procedures. Technologies such as sacral neuromodulation and bladder Botox injections are gaining traction. Patients increasingly prefer treatments with shorter recovery times and reduced hospitalization. Advancements in device-based therapies are improving clinical outcomes. Expanding outpatient urology centers are supporting adoption. For instance, rising use of percutaneous tibial nerve stimulation highlights growing preference for non-invasive neuromodulation techniques.

- By Diagnosis

On the basis of diagnosis, the market is segmented into urinalysis, cystoscopy, urodynamic testing, bladder ultrasound, imaging tests, and others. The Cystoscopy segment dominated the market with a share of 31.5% in 2025, owing to its high diagnostic accuracy and widespread use in evaluating bladder abnormalities. It is considered the gold standard for detecting bladder cancer and structural abnormalities. Increasing hospital-based diagnostic procedures are supporting demand. Technological improvements in flexible cystoscopes are enhancing patient comfort. Strong physician preference further reinforces its dominance. For instance, routine use of cystoscopy in hematuria evaluation demonstrates its critical clinical role.

The Urodynamic Testing segment is projected to register the fastest growth at a CAGR of 6.3% from 2026 to 2033, driven by increasing demand for functional assessment of bladder performance. It helps in diagnosing complex urinary disorders such as incontinence and neurogenic bladder. Rising prevalence of neurological conditions is boosting its clinical relevance. Expanding awareness among urologists is supporting adoption. Technological advancements are improving testing accuracy and efficiency. For instance, increasing use of multichannel urodynamic systems in specialized urology clinics is driving procedural growth.

- By End User

On the basis of end user, the market is segmented into hospitals, clinics, ambulatory surgery centers, and others. The Hospitals segment dominated the market with a share of 54.7% in 2025, driven by high patient inflow and availability of advanced diagnostic and therapeutic infrastructure. Hospitals serve as primary centers for complex bladder disorder management and surgical procedures. Strong presence of specialized urology departments supports dominance. Availability of skilled healthcare professionals enhances treatment quality. Integrated care pathways improve patient outcomes. For instance, large hospital networks in the United States handle a significant proportion of neuromodulation implant procedures.

The Ambulatory Surgery Centers (ASCs) segment is expected to witness the fastest growth at a CAGR of 6.6% from 2026 to 2033, driven by increasing shift toward outpatient-based minimally invasive procedures. ASCs offer cost-effective treatment options with shorter recovery times. Rising preference for same-day discharge procedures is boosting adoption. Technological advancements are enabling complex urology procedures in outpatient settings. Insurance coverage expansion is further supporting growth. For instance, increasing ASC-based Botox bladder injection procedures highlights this transition.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct and retail channels. The Direct channel dominated the market with a share of 61.2% in 2025, driven by strong hospital procurement systems and direct contracts with pharmaceutical and medical device companies. Hospitals and specialty clinics prefer direct sourcing for better pricing and supply reliability. Strong relationships between manufacturers and healthcare providers support this dominance. Large-scale institutional purchasing further strengthens this channel. Regulatory compliance requirements also favor direct procurement. For instance, direct supply agreements for neuromodulation devices are widely adopted across U.S. hospitals.

The Retail channel is projected to register the fastest growth at a CAGR of 6.1% from 2026 to 2033, driven by increasing availability of prescription drugs through retail pharmacies and online platforms. Growing patient preference for convenient access to medications is supporting expansion. Expansion of pharmacy chains is improving distribution reach. Digital pharmacy adoption is further accelerating growth. Rising self-management of chronic bladder conditions is boosting demand. For instance, increased retail dispensing of overactive bladder medications highlights growing outpatient care trends.

North America Bladder Disorders Market Regional Analysis

The United States dominated the North America bladder disorders market with the largest revenue share of 82.4% in 2025, supported by a high prevalence of urinary disorders, advanced healthcare infrastructure, strong reimbursement coverage, and early adoption of innovative treatment technologies. The country benefits from widespread adoption of innovative therapies such as neuromodulation devices, botulinum toxin injections, and advanced pharmacological treatments for overactive bladder and urinary incontinence. The presence of leading pharmaceutical and medical device companies further strengthens treatment availability and innovation. Increasing awareness of bladder health, rising geriatric population, and early diagnosis practices are also contributing to market expansion. Strong hospital networks and specialized urology centers enhance access to advanced care. Continuous clinical research and product approvals are further reinforcing the United States’ dominance in the regional market.

U.S. Bladder Disorders Market Insight

The U.S. bladder disorders market is witnessing strong growth due to rising prevalence of urinary incontinence, overactive bladder, and interstitial cystitis, along with a rapidly aging population and high awareness of urological health. The country’s advanced healthcare infrastructure and strong reimbursement framework are supporting widespread adoption of pharmacological therapies, neuromodulation devices, and minimally invasive procedures. Increasing utilization of AI-assisted diagnostics and digital health platforms is improving early detection and long-term disease management. In addition, strong presence of leading pharmaceutical and medical device companies is accelerating innovation and treatment availability across hospitals and specialty clinics. Growing focus on outpatient care and patient-friendly therapies is further boosting market expansion across the United States.

Canada Bladder Disorders Market Insight

The Canada bladder disorders market is experiencing steady growth, supported by increasing healthcare investments, expanding urology care access, and rising awareness of bladder-related conditions among the aging population. The country’s universal healthcare system is facilitating improved diagnosis and treatment adoption, particularly for overactive bladder and urinary incontinence. Growing use of minimally invasive therapies and prescription medications is supporting patient care efficiency and outcomes. Additionally, increasing integration of advanced diagnostic tools such as cystoscopy and urodynamic testing is enhancing clinical accuracy. Expanding specialty clinics and hospital infrastructure are further strengthening treatment accessibility across urban and semi-urban regions in Canada.

Mexico Bladder Disorders Market Insight

The Mexico bladder disorders market is gradually expanding due to improving healthcare infrastructure, rising awareness of urinary tract conditions, and increasing access to diagnostic and treatment services. Growing prevalence of untreated bladder disorders and increasing adoption of basic pharmacological therapies are driving market demand. Public and private healthcare initiatives are enhancing availability of urology services in urban hospitals. However, limited access to advanced neuromodulation and high-cost therapies remains a constraint in rural areas. Increasing medical tourism and gradual adoption of minimally invasive procedures are expected to support future market growth in Mexico.

North America Bladder Disorders Market Share

The North America bladder disorders industry is primarily led by well-established companies, including:

- Astellas Pharma Inc. (Japan)

- Pfizer Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Bayer AG (Germany)

- Johnson & Johnson Services, Inc. (U.S.)

- Boston Scientific Corporation (U.S.)

- Medtronic (Ireland)

- Coloplast A/S (Denmark)

- Teleflex Incorporated (U.S.)

- BD (U.S.)

- Hollister Incorporated (U.S.)

- Cook (U.S.)

- Laborie Medical Technologies Corp. (Canada)

- UroMems SAS (France)

- Olympus Corporation (Japan)

- Karl Storz SE & Co. KG (Germany)

- Ferring Pharmaceuticals (Switzerland)

- Ipsen (France)

- Recordati S.p.A. (Italy)

- Pierre Fabre Médicament (France)

Latest Developments in North America Bladder Disorders Market

- In January 2025, Medtronic, a global healthcare technology leader, announced continued expansion of its sacral neuromodulation portfolio used for overactive bladder and urinary retention management in the U.S. market, strengthening its InterStim-based treatment ecosystem through enhanced clinical adoption and long-term patient management solutions. The development highlights growing demand for implantable neuromodulation therapies in chronic bladder disorder care, supported by increasing physician adoption across specialized urology centers in North America. This expansion reinforces Medtronic’s leadership in advanced bladder control therapies and reflects ongoing innovation in minimally invasive treatment options for refractory urinary conditions

- In September 2024, AbbVie, a leading biopharmaceutical company, highlighted continued clinical and real-world evidence development for its onabotulinumtoxinA (Botox) therapy used in overactive bladder treatment across the United States, supporting broader physician confidence in long-term symptom management outcomes. The update emphasized improved patient-reported outcomes and sustained efficacy in reducing urinary incontinence episodes among adults with neurogenic and idiopathic bladder conditions. This development reflects increasing reliance on biologic therapies in chronic urology care

- In June 2023, Axonics, a medical technology company specializing in sacral neuromodulation systems, announced expanded commercialization efforts in the United States following its acquisition of Contura, strengthening its position in the treatment of urinary incontinence using Bulkamid hydrogel therapy. The integration enhanced Axonics’ portfolio of minimally invasive solutions for stress urinary incontinence, enabling broader access across urology practices. This development reflects increasing adoption of injectable bulking agents as an alternative to surgical interventions

- In March 2022, Sumitomo Pharma America (formerly Urovant Sciences) continued expansion of its vibegron-based therapy (Gemtesa) commercialization efforts in the U.S. overactive bladder market, strengthening its presence in oral pharmacological treatment options for urinary urgency and frequency. The development supported broader physician adoption of beta-3 adrenergic agonists as alternatives to anticholinergic drugs, improving tolerability profiles for patients. This reflects increasing preference for newer oral therapies in bladder disorder management

- In November 2021, Medtronic reported continued clinical adoption and procedural growth of its sacral neuromodulation technologies across North America, driven by increasing utilization in patients with overactive bladder and non-obstructive urinary retention. The development highlighted expanding awareness among physicians regarding implantable neuromodulation as an effective long-term treatment option. This trend reflects rising preference for device-based therapies over chronic pharmacological management in refractory cases

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.