North America Cast Films Market

Market Size in USD Billion

USD

2.95 Billion

USD

4.30 Billion

2025

2033

USD

2.95 Billion

USD

4.30 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.95 Billion | |

| USD 4.30 Billion | |

| % | |

|

North America Cast Films Market Size

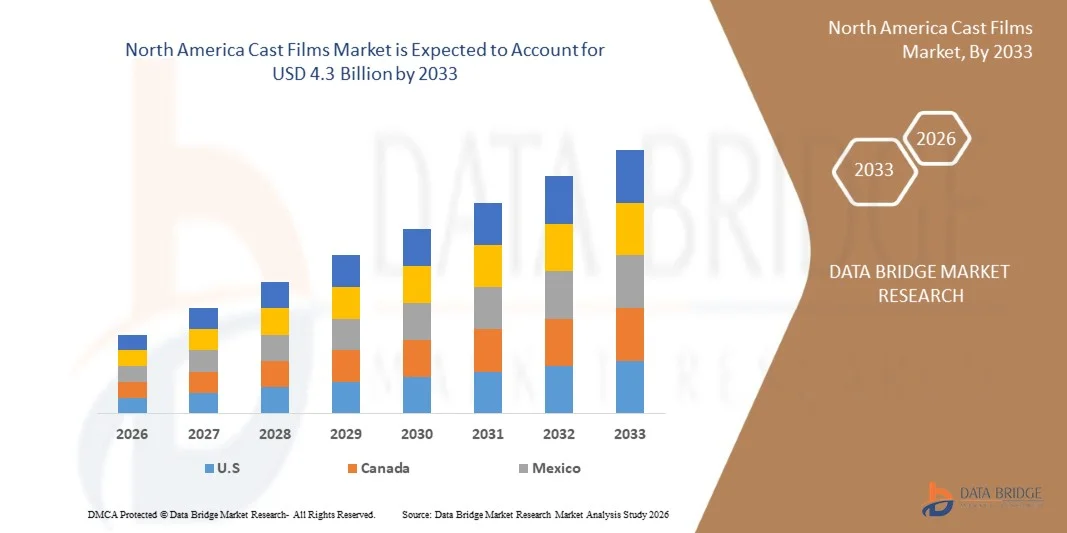

- The North America Cast Films Market size was valued at USD 2.95 Billion in 2025 and is expected to reach USD 4.3 Billion by 2033, at a CAGR of 4.9% during the forecast period

- Cast film is a type of plastic film produced by melting polymer resins and extruding them through a flat die onto a chilled casting roll, resulting in a smooth, uniform film. Cast films are commonly made from materials such as polypropylene (CPP) and polyethylene (PE). The North America Cast Films Market refers to the production and consumption of flat, extruded plastic films manufactured using the cast film extrusion process, primarily utilizing materials such as polypropylene (PP), polyethylene (PE), and specialty polymers.

North America Cast Films Market Analysis

- The North America Cast Films Market represents a critical segment within the North America flexible packaging and industrial materials landscape, supporting applications across food & beverages, pharmaceuticals, personal care, agriculture, and industrial packaging. Cast films are characterized by their superior clarity, uniform thickness, excellent sealing properties, and high production efficiency compared to blown films.

- Market growth is driven by rising demand for flexible packaging, lightweight materials, and sustainable packaging solutions. Increasing consumption of packaged food, ready-to-eat meals, and pharmaceutical products, along with a shift toward recyclable and downgauged materials, is accelerating adoption of cast films across both consumer and industrial sectors.

- U.S. is projected to lead the North America Cast Films Market share 81.30%. Growth in the region is supported by rapid urbanization, expanding food processing industries, rising consumer goods production, and strong manufacturing bases in North America.

- U.S. is projected to be the fastest-growing region CAGR 5.0% in 2025. driven by strong demand for high-performance packaging, advanced manufacturing technologies, and growth in food, healthcare, and consumer goods sectors. Sustainability trends, increasing use of recyclable materials, and innovation in barrier films further accelerate market growth.

- The Polyethylene (PE) cast films segment is anticipated to hold the largest market share 64.97% in 2026, driven by its cost-effectiveness, flexibility, excellent sealability, and recyclability. PE cast films are widely used in food packaging, shrink films, stretch wraps, and agricultural films, making them highly versatile across applications.

Report Scope and North America Cast Films Market Segmentation

|

Attributes |

North America Cast Films Market Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework.. |

North America Cast Films Market Trends

“Rowing Adoption of Recyclable Mono-Material Cast Films”

- The increasing adoption of recyclable mono-material cast films represents a significant growth opportunity for the North America cast film market. Regulatory pressures, sustainability goals, and consumer awareness are driving demand for packaging solutions that align with circular economy principles. Mono-material cast films, designed to be fully recyclable, address both performance and environmental requirements, offering a viable alternative to multilayer and composite films that face recycling challenges.

- Italian pasta brand Garofalo introduced pasta packaging made from mono‑polypropylene (PP) films created by GT Polifilm using SABIC’s certified circular polypropylene. The resulting mono‑material PP bags can be recycled within existing polypropylene waste streams, demonstrating practical application of mono‑material film in food packaging

- SÜDPACK launched recyclable mono material polypropylene and polyethylene films under its Pure Line product family for coffee packaging. The films offer a recyclable alternative to conventional composite structures while maintaining packaging functionality.

North America Cast Films Market Dynamics

Driver

Rising Demand for High-Performance Flexible Packaging Solutions

- The North America Cast Films Market has been significantly propelled by the rising demand for high-performance flexible packaging solutions across key end-use sectors such as food & beverage, personal care, pharmaceuticals, and consumer goods. Flexible packaging formats including pouches, sachets, overwraps, and laminated structures are increasingly preferred over rigid counterparts due to their superior combination of lightweight properties, mechanical strength, clarity, and barrier performance, all of which are hallmarks of cast films such as cast polypropylene (CPP) and related structures. This shift stems from evolving consumer preferences toward convenience, extended shelf life, attractive product presentation, and cost efficiencies in transportation and material usage, which rigid packaging often cannot match.

- In 2025, Jindal Poly Films announced a major USD 84 Million investment to expand its Nashik facility with new BOPP, PET, and CPP film production lines. This strategic capital expenditure is explicitly aimed at augmenting capacity for flexible packaging films to meet surging market demand, particularly in food, personal care, and pharmaceutical applications, underscoring industry recognition of flexible packaging as a key growth driver.

- UFlex commissioned an advanced 6.5-meter-wide CPP film line with 18,000 tonnes per annum capacity at its Russia facility in 2024, directly responding to customer requirements for high-performance flexible films used in packaging solutions worldwide. This expansion not only enhances production capability but also reflects strategic alignment with increasing demand for flexible film substrates that deliver enhanced clarity, sealability, and durability.

Restraint/Challenge

Recycling Limitations of Multilayer Cast Film Structure

- Recycling limitations associated with multilayer cast film structures present a significant restraint on the growth of the North America cast film market. Multilayer films are widely used due to their superior barrier performance, mechanical strength, and functional versatility across food, pharmaceutical, and consumer packaging applications. However, these structures typically combine multiple polymer layers with different chemical compositions, which complicates separation and recycling processes within existing waste management systems..

- Most recycling infrastructures across regions are designed to process mono-material plastics. Multilayer cast films require advanced separation technologies that remain limited in availability and commercial viability. This structural complexity reduces recyclability efficiency, increases processing costs, and limits the acceptance of such materials within circular economy frameworks. As sustainability regulations continue to evolve, materials that face recycling challenges encounter growing scrutiny from regulatory authorities and environmental agencies .

- According to analyses from recycling coalitions in North America, recycling of plastic films including multilayer packaging films is heavily dependent on specialized drop‑off systems rather than curbside collection, limiting the ability of companies to achieve broader recycled content and circularity targets. This systemic constraint influences company efforts to scale sustainable packaging programs

North America Cast Films Market Scope

The North America Cast Films Market is segmented into five segments based on material, thickness, packaging format, layer structure, and application

- By Material

On the basis of material, the North America Cast Films Market is segmented into polyethylene, polypropylene, polyamide, PVC, others. Polyethylene is further segmented into linear low-density polyethylene (LLDPE), low-density polyethylene (LDPE), high-density polyethylene (HDPE). Polypropylene is further segmented into cast polypropylene (CPP), biaxially oriented polypropylene (BOPP). In 2026 the polyethylene segment is expected to dominate the market with a 64.97% market share. Polyethylene dominates the North America Cast Films Market due to its cost-effectiveness, excellent sealability, flexibility, and recyclability. Rising demand for lightweight, durable, and moisture-resistant packaging in food, consumer goods, and agriculture is driving adoption. Its compatibility with high-speed processing further supports widespread industrial usage.

Polyamide it is anticipated to show the fastest growing 5.4% during the forecast period. Polyamide cast films are gaining traction owing to their superior mechanical strength, puncture resistance, and high barrier properties against oxygen and aromas. Growing demand for premium food and pharmaceutical packaging requiring extended shelf life and product integrity is significantly accelerating the adoption of polyamide-based cast films.

- By Thickness

On the basis of thickness, the North America Cast Films Market is segmented into 31–50 microns, up to 30 microns, 51–70 microns, above 70 microns. In 2026, the 31–50 microns segment is expected to dominate the market with a 38.25% market share and it is anticipated to show the fastest growth during the forecast period. The 31–50 microns thickness segment is driven by rising demand for downgauged, lightweight packaging that balances material efficiency with mechanical strength. This range offers optimal durability, flexibility, and cost control, making it highly preferred in food packaging, pouches, and multilayer laminates across consumer and industrial sectors.

- By Packaging Format

On the basis of packaging format, the North America Cast Films Market is segmented into pouches, bags, laminates, wraps, labels. In 2026, the pouches segment is expected to dominate the market with a 38.93% market share and it is anticipated to show the fastest growth during the forecast period. The growing popularity of pouches is fueled by demand for convenient, portable, and resealable packaging formats. Cast films enable superior clarity, printability, and barrier performance in pouches, supporting applications in food, beverages, and pharmaceuticals. Their lightweight nature also reduces transportation and material costs significantly.

- By Layer Structure

On the basis of layer structure, the North America Cast Films Market is segmented into multilayer, monolayer. In 2026, the multilayer segment is expected to dominate the market with a 63.84%market share and it is anticipated to show the fastest growth during the forecast period. Multilayer cast films are driven by increasing need for enhanced barrier protection, mechanical strength, and shelf-life extension. Combining different polymers improves performance against moisture, oxygen, and light, making multilayer structures essential for premium food, pharmaceutical, and industrial packaging requiring superior product preservation.

- By Application

On the basis of application, the North America Cast Films Market is segmented into food & beverages, industrial, personal care, pharmaceuticals, electricals & electronics, textile, others. In 2026, the food & beverages segment is expected to dominate the market with a 33.85% market share. The food and beverages segment drives cast films demand through rising consumption of packaged, processed, and ready-to-eat products. Cast films provide excellent moisture resistance, seal integrity, and visual appeal, helping extend shelf life and ensure food safety while meeting growing consumer preference for convenient packaging formats.

Pharmaceuticals it is anticipated to show the fastest growing 5.6% during the forecast period. Pharmaceutical packaging demand is boosting cast films adoption due to the need for high barrier protection, chemical resistance, and contamination prevention. Cast films ensure product stability, dosage safety, and regulatory compliance, making them essential for blister packs, sachets, and medical packaging in a rapidly expanding healthcare sector.

North America Cast Films Market Regional Analysis

- U.S. dominates the North America Cast Films Market with the largest revenue share of 81.30% in 2026

- The strong demand across food packaging, pharmaceuticals, electronics, and automotive sectors. The region benefits from a robust manufacturing base, low-cost production, rapid urbanization, and high adoption of flexible packaging solutions in China, India, Japan, and Southeast Asia.

Canada North America Cast Films Market Insight

The Canada North America Cast Films Market captured the largest share of North America revenue in 2026, fueled by extensive use in consumer electronics packaging, food processing, and pharmaceutical applications. Major domestic players continue to expand capacity and invest in advanced multilayer and recyclable cast film technologies to meet rising quality and sustainability requirements.

Mexico North America Cast Films Market Insight

The Mexico North America Cast Films Market is projected to grow steadily, driven by increasing adoption in food packaging, pharmaceutical blister packaging, and industrial laminates. Strong regulatory support for sustainable materials, recyclability, and reduced plastic waste is encouraging the development of bio-based and downgauged cast films.

North America Cast Films Market Share

The North America Cast Films Market is primarily led by well-established companies, including:

- Amcor plc (BERRY GLOBAL) (Switzerland)

- UFlex Limited (India)

- Inteplast Group (U.S.)

- Jindal Films Limited (India)

- OBEN GROUP S.A.C. (Ecuador)

- Bischof + Klein SE & CO. KG (Germany)

- MITSUI CHEMICALS AMERICA, INC. (U.S.)

- Polifilm GmbH (Germany)

- PROFOL GmbH (Germany)

- FUTAMURA CHEMICAL CO, LTD. (Japan)

- Polyplex (India)

- Thai Film Industries Public Limited Company (Thailand)

- SCIENTEX BERHAD (Malaysia)

- Polibak Plastik Film Sanayi Ve Ticaret Aş (Turkey)

- Copol International Ltd (India)

- 3B FILMS LIMITED (India)

- Alpha Marathon Film Extrusion Technologies (U.S.)

- Cloudfilm Packaging Materials Co., Ltd. (China)

- IPG (Canada)

- Kingchuan Packaging (CPP Film) (China)

- PANVERTA CAKRAKENCANA (Indonesia)

- Plastchim-T (Russia)

- Pt. Bhineka Tatamulya Industri. (Indonesia)

- TAKIGAWA CORPORATION (Japan)

Latest Developments in North America Cast Films Market

- In July, 2025, Inteplast Group has acquired Perga, a plastics film manufacturer based in Walldürn, south-western Germany. The decision marks Inteplast’s first move into Europe and brings Perga into the company’s engineered films division. This development help the company to ear revenue in the company year.

- In June 2025, Amcor has launched a first-of-its-kind, more sustainable Perflex shrink bag with an integrated handle for Butterball’s turkey breast packaging, replacing the traditional net wrap. The new design reduces packaging material and improves production efficiency, eliminating the need for manual netting. Compared with the incumbent packaging, the Perflex bag achieves a 22% reduction in carbon footprint and 22% lower water consumption. This innovation enhances Amcor’s sustainability portfolio by offering a lower-impact packaging solution that meets growing customer and regulatory demand for eco-friendly materials.

- In, August, 2024 Jindal Poly Films to add a new BOPP film production line in India. The expansion is intended to increase output capacity and cater to growing demand in flexible packaging. It strengthens the company’s position in the packaging films market..

- In September 2025, UFlex announced a strategic partnership between Morris Packaging LLC and UFlex Packaging Inc. to deliver an innovative and sustainable woven bag series. The collaboration strengthens UFlex’s presence in the North American packaging market and expands its sustainable product offerings. This move underscores the company’s focus on innovation and North America expansion in packaging solutions.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF NORTH AMERICA CAST FILMS MARKET

1.4 CURRENCY AND PRICING

1.5 LIMITATIONS

1.6 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 DBMR TRIPOD DATA VALIDATION MODEL

2.5 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.6 DBMR MARKET POSITION GRID

2.7 VENDOR SHARE ANALYSIS

2.8 MULTIVARIATE MODELING

2.9 MATERIAL TYPE TIMELINE CURVE

2.1 MARKET APPLICATION COVERAGE GRID

2.11 SECONDARY SOURCES

2.12 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PESTAL ANALYSIS

4.2 PORTERS FIVE FORCES ANALYSIS

4.3 RAW MATERIAL COVERAGE — NORTH AMERICA CAST FILMS MARKET

4.3.1 POLYOLEFINS

4.3.1.1 Polyethylene (PE)

4.3.2 POLYPROPYLENE (PP)

4.3.3 FUNCTIONAL POLYMERS AND COPOLYMERS

4.3.4 ADDITIVES AND PROCESSING AIDS

4.3.5 FILLERS, REINFORCEMENTS, AND MODIFIERS

4.4 TECHNOLOGICAL ADVANCEMENTS BY MANUFACTURERS OF NORTH AMERICA CAST FILMS MARKET

4.4.1 ADVANCED MULTI-LAYER CO-EXTRUSION TECHNOLOGIES

4.4.2 HIGH-PRECISION DIE AND COOLING SYSTEM INNOVATIONS

4.4.3 INTEGRATION OF AUTOMATION AND DIGITAL PROCESS CONTROL

4.4.4 DEVELOPMENT OF HIGH-PERFORMANCE AND SPECIALTY CAST FILMS

4.4.5 SUSTAINABILITY-ORIENTED MATERIAL AND PROCESS INNOVATIONS

4.4.6 ENHANCED COMPATIBILITY WITH FLEXIBLE PACKAGING CONVERTING PROCESSES

4.4.7 ENERGY-EFFICIENT AND HIGH-OUTPUT PRODUCTION LINES

4.4.8 CONCLUSION

4.5 VENDOR SELECTION CRITERIA FOR NORTH AMERICA CAST FILMS MARKET

4.5.1 PRODUCT QUALITY, FILM PERFORMANCE, AND CONSISTENCY

4.5.2 MANUFACTURING CAPABILITY AND TECHNOLOGICAL SOPHISTICATION

4.5.3 PRODUCT PORTFOLIO BREADTH AND CUSTOMIZATION CAPABILITY

4.5.4 SUPPLY RELIABILITY AND OPERATIONAL SCALABILITY

4.5.5 SUSTAINABILITY CREDENTIALS AND REGULATORY COMPLIANCE

4.5.6 COST COMPETITIVENESS AND TOTAL VALUE PROPOSITION

4.5.7 TECHNICAL SUPPORT AND CUSTOMER SERVICE CAPABILITY

4.5.8 CONCLUSION

4.6 SUPPLY CHAIN ANALYSIS

4.6.1 OVERVIEW

4.6.2 LOGISTIC COST SCENARIO

4.6.3 IMPORTANCE OF LOGISTICS SERVICE PROVIDERS

4.7 CLIMATE CHANGE SCENARIO

4.7.1 ENVIRONMENTAL CONCERNS

4.7.2 INDUSTRY RESPONSE

4.7.3 GOVERNMENT’S ROLE

4.7.4 ANALYST RECOMMENDATIONS

4.8 PRICING ANALYSIS

5 REGULATION COVERAGE

5.1 PRODUCT CODES

5.2 CERTIFIED STANDARDS

5.3 SAFETY STANDARDS

5.3.1 MATERIAL HANDLING & STORAGE

5.3.2 TRANSPORT & PRECAUTIONS

5.3.3 HARAD IDENTIFICATION

6 MARKET OVERVIEW

6.1 DRIVERS

6.1.1 RISING DEMAND FOR HIGH-PERFORMANCE FLEXIBLE PACKAGING SOLUTIONS

6.1.2 STRONG GROWTH IN PACKAGED AND CONVENIENCE FOOD SECTOR

6.1.3 TECHNOLOGICAL ADVANCEMENTS IN CAST FILM EXTRUSION

6.2 RESTRAINTS

6.2.1 STRINGENT ENVIRONMENTAL REGULATIONS ON PLASTIC USAGE AND DISPOSAL

6.2.2 RECYCLING LIMITATIONS OF MULTILAYER CAST FILM STRUCTURES

6.3 OPPORTUNITIES

6.3.1 GROWING ADOPTION OF RECYCLABLE MONO-MATERIAL CAST FILMS

6.3.2 EXPANDING DEMAND FROM PHARMACEUTICAL AND HEALTHCARE PACKAGING SECTORS

6.4 CHALLENGES

6.4.1 FLUCTUATING IN RAW MATERIAL PRICES

6.4.2 INTENSIFYING COMPETITION FROM ALTERNATIVE PACKAGING SOLUTIONS

7 NORTH AMERICA CAST FILMS MARKET, BY MATERIAL.

7.1 OVERVIEW

7.2 NORTH AMERICA CAST FILMS MARKET, BY MATERIAL, 2018-2033 (USD THOUSAND)

7.2.1 POLYETHYLENE

7.2.2 POLYPROPYLENE

7.2.3 POLYAMIDE

7.2.4 PVC

7.2.5 OTHERS

7.3 NORTH AMERICA POLYETHYLENE IN CAST FILMS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

7.3.1 LINEAR LOW-DENSITY POLYETHYLENE (LLDPE)

7.3.2 LOW-DENSITY POLYETHYLENE (LDPE)

7.3.3 HIGH-DENSITY POLYETHYLENE (HDPE)

7.4 NORTH AMERICA POLYETHYLENE IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

7.4.1 ASIA-PACIFIC

7.4.2 NORTH AMERICA

7.4.3 EUROPE

7.4.4 SOUTH AMERICA

7.4.5 MIDDLE EAST & AFRICA

7.5 NORTH AMERICA POLYPROPYLENE IN CAST FILMS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

7.5.1 CAST POLYPROPYLENE (CPP)

7.5.2 BIAXIALLY ORIENTED POLYPROPYLENE (BOPP)

7.6 NORTH AMERICA POLYPROPYLENE IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

7.6.1 ASIA-PACIFIC

7.6.2 NORTH AMERICA

7.6.3 EUROPE

7.6.4 SOUTH AMERICA

7.6.5 MIDDLE EAST & AFRICA

7.7 NORTH AMERICA POLYAMIDE IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

7.7.1 ASIA-PACIFIC

7.7.2 NORTH AMERICA

7.7.3 EUROPE

7.7.4 SOUTH AMERICA

7.7.5 MIDDLE EAST & AFRICA

7.8 NORTH AMERICA PVC IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

7.8.1 ASIA-PACIFIC

7.8.2 NORTH AMERICA

7.8.3 EUROPE

7.8.4 SOUTH AMERICA

7.8.5 MIDDLE EAST & AFRICA

7.9 NORTH AMERICA OTHERS IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

7.9.1 ASIA-PACIFIC

7.9.2 NORTH AMERICA

7.9.3 EUROPE

7.9.4 SOUTH AMERICA

7.9.5 MIDDLE EAST & AFRICA

8 NORTH AMERICA CAST FILMS MARKET, BY THICKNESS

8.1 OVERVIEW

8.2 NORTH AMERICA CAST FILMS MARKET, BY THICKNESS, 2018-2033 (USD THOUSAND)

8.2.1 31–50 MICRONS

8.2.2 UP TO 30 MICRONS

8.2.3 51–70 MICRONS

8.2.4 ABOVE 70 MICRONS

8.3 NORTH AMERICA 31–50 MICRONS IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.3.1 ASIA-PACIFIC

8.3.2 NORTH AMERICA

8.3.3 EUROPE

8.3.4 SOUTH AMERICA

8.3.5 MIDDLE EAST & AFRICA

8.4 NORTH AMERICA UP TO 30 MICRONS IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.4.1 ASIA-PACIFIC

8.4.2 NORTH AMERICA

8.4.3 EUROPE

8.4.4 SOUTH AMERICA

8.4.5 MIDDLE EAST & AFRICA

8.5 NORTH AMERICA 51–70 MICRONS IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.5.1 ASIA-PACIFIC

8.5.2 NORTH AMERICA

8.5.3 EUROPE

8.5.4 SOUTH AMERICA

8.5.5 MIDDLE EAST & AFRICA

8.6 NORTH AMERICA ABOVE 70 MICRONS IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.6.1 ASIA-PACIFIC

8.6.2 NORTH AMERICA

8.6.3 EUROPE

8.6.4 SOUTH AMERICA

8.6.5 MIDDLE EAST & AFRICA

8.7 NORTH AMERICA CAST FILMS MARKET, BY PACKAGING FORMAT, 2018-2033 (USD THOUSAND)

9 NORTH AMERICA CAST FILMS MARKET, BY PACKAGING FORMAT

9.1 OVERVIEW

9.1.1 POUCHES

9.1.2 BAGS

9.1.3 LAMINATES

9.1.4 WRAPS

9.1.5 LABELS

9.2 NORTH AMERICA POUCHES IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.2.1 ASIA-PACIFIC

9.2.2 NORTH AMERICA

9.2.3 EUROPE

9.2.4 SOUTH AMERICA

9.2.5 MIDDLE EAST & AFRICA

9.3 NORTH AMERICA BAGS IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.3.1 ASIA-PACIFIC

9.3.2 NORTH AMERICA

9.3.3 EUROPE

9.3.4 SOUTH AMERICA

9.3.5 MIDDLE EAST & AFRICA

9.4 NORTH AMERICA LAMINATES IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.4.1 ASIA-PACIFIC

9.4.2 NORTH AMERICA

9.4.3 EUROPE

9.4.4 SOUTH AMERICA

9.4.5 MIDDLE EAST & AFRICA

9.5 NORTH AMERICA WRAPS IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.5.1 ASIA-PACIFIC

9.5.2 NORTH AMERICA

9.5.3 EUROPE

9.5.4 SOUTH AMERICA

9.5.5 MIDDLE EAST & AFRICA

9.6 NORTH AMERICA LABELS IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.6.1 ASIA-PACIFIC

9.6.2 NORTH AMERICA

9.6.3 EUROPE

9.6.4 SOUTH AMERICA

9.6.5 MIDDLE EAST & AFRICA

10 NORTH AMERICA CAST FILMS MARKET, BY LAYER STRUCTURE.

10.1 OVERVIEW

10.2 NORTH AMERICA CAST FILMS MARKET, BY LAYER STRUCTURE, 2018-2033 (USD THOUSAND)

10.2.1 MULTILAYER

10.2.2 MONOLAYER

10.3 NORTH AMERICA MULTILAYER IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.3.1 ASIA-PACIFIC

10.3.2 NORTH AMERICA

10.3.3 EUROPE

10.3.4 SOUTH AMERICA

10.3.5 MIDDLE EAST & AFRICA

10.4 NORTH AMERICA MONOLAYER IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.4.1 ASIA-PACIFIC

10.4.2 NORTH AMERICA

10.4.3 EUROPE

10.4.4 SOUTH AMERICA

10.4.5 MIDDLE EAST & AFRICA

11 NORTH AMERICA CAST FILMS MARKET, BY APPLICATION.

11.1 OVERVIEW

11.2 NORTH AMERICA CAST FILMS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

11.2.1 FOOD & BEVERAGES

11.2.2 INDUSTRIAL

11.2.3 PERSONAL CARE

11.2.4 PHARMACEUTICALS

11.2.5 ELECTRICALS & ELECTRONICS

11.2.6 TEXTILE

11.2.7 OTHERS

11.3 NORTH AMERICA FOOD & BEVERAGES IN CAST FILMS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

11.3.1 PROCESSED MEAT & POULTRY

11.3.2 FROZEN PRODUCTS

11.3.3 FRUITS & VEGETABLES

11.3.4 FRESH MEAT & POULTRY

11.3.5 CONFECTIONERY PRODUCTS

11.3.6 DAIRY PRODUCTS

11.3.7 DRY FRUITS

11.3.8 OTHERS

11.4 NORTH AMERICA FOOD & BEVERAGES IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.4.1 ASIA-PACIFIC

11.4.2 NORTH AMERICA

11.4.3 EUROPE

11.4.4 SOUTH AMERICA

11.4.5 MIDDLE EAST & AFRICA

11.5 NORTH AMERICA INDUSTRIAL IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.5.1 ASIA-PACIFIC

11.5.2 NORTH AMERICA

11.5.3 EUROPE

11.5.4 SOUTH AMERICA

11.5.5 MIDDLE EAST & AFRICA

11.6 NORTH AMERICA PERSONAL CARE IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.6.1 ASIA-PACIFIC

11.6.2 NORTH AMERICA

11.6.3 EUROPE

11.6.4 SOUTH AMERICA

11.6.5 MIDDLE EAST & AFRICA

11.7 NORTH AMERICA PHARMACEUTICALS IN CAST FILMS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

11.7.1 DRUG PACKAGING

11.7.2 VACCINE PACKAGING

11.7.3 OTHERS

11.8 NORTH AMERICA PHARMACEUTICALS IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.8.1 ASIA-PACIFIC

11.8.2 NORTH AMERICA

11.8.3 EUROPE

11.8.4 SOUTH AMERICA

11.8.5 MIDDLE EAST & AFRICA

11.9 NORTH AMERICA ELECTRICALS & ELECTRONICS IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.9.1 ASIA-PACIFIC

11.9.2 NORTH AMERICA

11.9.3 EUROPE

11.9.4 SOUTH AMERICA

11.9.5 MIDDLE EAST & AFRICA

11.1 NORTH AMERICA TEXTILE IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.10.1 ASIA-PACIFIC

11.10.2 NORTH AMERICA

11.10.3 EUROPE

11.10.4 SOUTH AMERICA

11.10.5 MIDDLE EAST & AFRICA

11.11 NORTH AMERICA OTHERS IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.11.1 ASIA-PACIFIC

11.11.2 NORTH AMERICA

11.11.3 EUROPE

11.11.4 SOUTH AMERICA

11.11.5 MIDDLE EAST & AFRICA

12 NORTH AMERICA CAST FILMS MARKET, BY REGION

12.1 NORTH AMERICA

12.1.1 U.S.

12.1.2 CANADA

12.1.3 MEXICO

13 NORTH AMERICA CAST FILMSMARKET

13.1 COMPANY SHARE ANALYSIS: GLOBAL

14 SWOT ANALYSIS

15 COMPANY PROFILES

15.1 AMCOR INC.(BERRY GLOBAL)

15.1.1 COMPANY SNAPSHOT

15.1.2 REVENUE ANALYSIS

15.1.3 COMPANY SHARE ANALYSIS

15.1.4 PRODUCT PORTFOLIO

15.1.5 RECENT DEVELOPMENT

15.2 UFLEX LTD

15.2.1 COMPANY SNAPSHOT

15.2.2 REVENUE ANALYSIS

15.2.3 COMPANY SHARE ANALYSIS

15.2.4 PRODUCT/SERVICE PORTFOLIO

15.2.5 RECENT DEVELOPMENT

15.3 INTEPLAST GROUP

15.3.1 COMPANY SNAPSHOT

15.3.2 COMPANY SHARE ANALYSIS

15.3.3 PRODUCT PORTFOLIO

15.3.4 RECENT DEVELOPMENT

15.4 JINDAL POLY FILMS LIMITED.

15.4.1 COMPANY SNAPSHOT

15.4.2 REVENUE ANALYSIS

15.4.3 COMPANY SHARE ANALYSIS

15.4.4 PRODUCT/SERVICE PORTFOLIO

15.4.5 RECENT DEVELOPMENT

15.5 OBEN HOLDING GROUP S.A.C.

15.5.1 COMPANY SNAPSHOT

15.5.2 COMPANY SHARE ANALYSIS

15.5.3 PRODUCT/SERVICE PORTFOLIO

15.5.4 RECENT DEVELOPMENT

15.6 3B FILMS LIMITED

15.6.1 COMPANY SNAPSHOT

15.6.2 REVENUE ANALYSIS

15.6.3 PRODUCT PORTFOLIO

15.6.4 RECENT DEVELOPMENT

15.7 ALPHA MARATHON FILM EXTRUSION TECHNOLOGIES

15.7.1 COMPANY SNAPSHOT

15.7.2 PRODUCT PORTFOLIO

15.7.3 RECENT DEVELOPMENT

15.8 BISCHOF + KLEIN SE & CO. KG

15.8.1 COMPANY SNAPSHOT

15.8.2 PRODUCT PORTFOLIO

15.8.3 RECENT DEVELOPMENT

15.9 CLOUD FILM PACKAGING MATERIALS CO., LTD.

15.9.1 COMPANY SNAPSHOT

15.9.2 PRODUCT PORTFOLIO

15.9.3 RECENT DEVELOPMENT

15.1 COPOL INTERNATIONAL LTD

15.10.1 COMPANY SNAPSHOT

15.10.2 PRODUCT/SERVICE PORTFOLIO

15.10.3 RECENT DEVELOPMENT

15.11 FUTAMORA CHEMICAL CO. LTD.

15.11.1 COMPANY SNAPSHOT

15.11.2 PRODUCT/SERVICE PORTFOLIO

15.11.3 RECENT DEVELOPMENT

15.12 IPG

15.12.1 COMPANY SNAPSHOT

15.12.2 PRODUCT PORTFOLIO

15.12.3 RECENT DEVELOPMENT

15.13 KINGCHUAN PACKAGING (CPP FILM)

15.13.1 COMPANY SNAPSHOT

15.13.2 PRODUCT/SERVICE PORTFOLIO

15.13.3 RECENT DEVELOPMENT

15.14 MITSUI CHEMICALS AMERICA, INC.

15.14.1 COMPANY SNAPSHOT

15.14.2 REVENUE ANALYSIS

15.14.3 PRODUCT/SERVICE PORTFOLIO

15.14.4 RECENT DEVELOPMENT

15.15 PANVERTA CAKRAKENCANA

15.15.1 COMPANY SNAPSHOT

15.15.2 PRODUCT PORTFOLIO

15.15.3 RECENT DEVELOPMENT

15.16 PLASTCHIM-T

15.16.1 COMPANY SNAPSHOT

15.16.2 PRODUCT/SERVICE PORTFOLIO

15.16.3 RECENT DEVELOPMENT

15.17 POLİBAK PLASTİK FİLM SANAYİ VE TİCARET AŞ

15.17.1 COMPANY SNAPSHOT

15.17.2 PRODUCT PORTFOLIO

15.17.3 RECENT DEVELOPMENT

15.18 POLIFILM GMBH

15.18.1 COMPANY SNAPSHOT

15.18.2 PRODUCT PORTFOLIO

15.18.3 RECENT DEVELOPMENT

15.19 POLYPLEX

15.19.1 COMPANY SNAPSHOT

15.19.2 REVENUE ANALYSIS

15.19.3 PRODUCT PORTFOLIO

15.19.4 RECENT DEVELOPMENT

15.2 PROFOL GMBH

15.20.1 COMPANY SNAPSHOT

15.20.2 PRODUCT PORTFOLIO

15.20.3 RECENT DEVELOPMENT

15.21 PT. BHINEKA TATAMULYA INDUSTRY

15.21.1 COMPANY SNAPSHOT

15.21.2 PRODUCT/SERVICE PORTFOLIO

15.21.3 RECENT DEVELOPMENT

15.22 SCIENTEX BERHAD

15.22.1 COMPANY SNAPSHOT

15.22.2 REVENUE ANALYSIS

15.22.3 PRODUCT PORTFOLIO

15.22.4 RECENT DEVELOPMENT

15.23 TAKIGAWA CORPORATION

15.23.1 COMPANY SNAPSHOT

15.23.2 PRODUCT PORTFOLIO

15.23.3 RECENT DEVELOPMENT

15.24 THAI FILM INDUSTRIES PUBLIC COMPANY LTD.

15.24.1 COMPANY SNAPSHOT

15.24.2 REVENUE ANALYSIS

15.24.3 PRODUCT/SERVICE PORTFOLIO

15.24.4 RECENT DEVELOPMENT

16 QUESTIONNAIRE

17 RELATED REPORTS

List of Table

TABLE 1 NORTH AMERICA CAST FILMS MARKET, BY MATERIAL, 2018-2033 (USD THOUSAND)

TABLE 2 NORTH AMERICA POLYETHYLENE IN CAST FILMS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 3 NORTH AMERICA POLYETHYLENE IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 4 NORTH AMERICA POLYPROPYLENE IN CAST FILMS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 5 NORTH AMERICA POLYPROPYLENE IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 6 NORTH AMERICA POLYAMIDE IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 7 NORTH AMERICA PVC IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 8 NORTH AMERICA OTHERS IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 9 NORTH AMERICA CAST FILMS MARKET, BY THICKNESS, 2018-2033 (USD THOUSAND)

TABLE 10 NORTH AMERICA 31–50 MICRONS IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 11 NORTH AMERICA UP TO 30 MICRONS IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 12 NORTH AMERICA 51–70 MICRONS IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 13 NORTH AMERICA ABOVE 70 MICRONS IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 14 NORTH AMERICA CAST FILMS MARKET, BY PACKAGING FORMAT, 2018-2033 (USD THOUSAND)

TABLE 15 NORTH AMERICA POUCHES IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 16 NORTH AMERICA BAGS IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 17 NORTH AMERICA LAMINATES IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 18 NORTH AMERICA WRAPS IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 19 NORTH AMERICA LABELS IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 20 NORTH AMERICA CAST FILMS MARKET, BY LAYER STRUCTURE, 2018-2033 (USD THOUSAND)

TABLE 21 NORTH AMERICA MULTILAYER IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 22 NORTH AMERICA MONOLAYER IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 23 NORTH AMERICA CAST FILMS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 24 NORTH AMERICA FOOD & BEVERAGES IN CAST FILMS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 25 NORTH AMERICA FOOD & BEVERAGES IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 26 NORTH AMERICA INDUSTRIAL IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 27 NORTH AMERICA PERSONAL CARE IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 28 NORTH AMERICA PHARMACEUTICALS IN CAST FILMS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 29 NORTH AMERICA PHARMACEUTICALS IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 30 NORTH AMERICA ELECTRICALS & ELECTRONICS IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 31 NORTH AMERICA TEXTILE IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 32 NORTH AMERICA OTHERS IN CAST FILMS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 33 REGION

TABLE 34 NORTH AMERICA CAST FILMS MARKET, BY COUNTRY, 2018-2033 (USD THOUSAND)

TABLE 35 USD THOUSAND

TABLE 36 NORTH AMERICA CAST FILMS MARKET, BY MATERIAL, 2018-2033 (USD THOUSAND)

TABLE 37 NORTH AMERICA POLYETHYLENE IN CAST FILMS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 38 NORTH AMERICA POLYPROPYLENE IN CAST FILMS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 39 NORTH AMERICA CAST FILMS MARKET, BY THICKNESS, 2018-2033 (USD THOUSAND)

TABLE 40 NORTH AMERICA CAST FILMS MARKET, BY PACKAGING FORMAT, 2018-2033 (USD THOUSAND)

TABLE 41 NORTH AMERICA CAST FILMS MARKET, BY LAYER STRUCTURE, 2018-2033 (USD THOUSAND)

TABLE 42 NORTH AMERICA CAST FILMS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 43 NORTH AMERICA FOOD & BEVERAGES IN CAST FILMS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 44 NORTH AMERICA PHARMACEUTICALS IN CAST FILMS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 45 USD THOUSAND

TABLE 46 U.S. CAST FILMS MARKET, BY MATERIAL, 2018-2033 (USD THOUSAND)

TABLE 47 U.S. POLYETHYLENE IN CAST FILMS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 48 U.S. POLYPROPYLENE IN CAST FILMS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 49 U.S. CAST FILMS MARKET, BY THICKNESS, 2018-2033 (USD THOUSAND)

TABLE 50 U.S. CAST FILMS MARKET, BY PACKAGING FORMAT, 2018-2033 (USD THOUSAND)

TABLE 51 U.S. CAST FILMS MARKET, BY LAYER STRUCTURE, 2018-2033 (USD THOUSAND)

TABLE 52 U.S. CAST FILMS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 53 U.S. FOOD & BEVERAGES IN CAST FILMS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 54 U.S. PHARMACEUTICALS IN CAST FILMS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 55 USD THOUSAND

TABLE 56 CANADA CAST FILMS MARKET, BY MATERIAL, 2018-2033 (USD THOUSAND)

TABLE 57 CANADA POLYETHYLENE IN CAST FILMS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 58 CANADA POLYPROPYLENE IN CAST FILMS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 59 CANADA CAST FILMS MARKET, BY THICKNESS, 2018-2033 (USD THOUSAND)

TABLE 60 CANADA CAST FILMS MARKET, BY PACKAGING FORMAT, 2018-2033 (USD THOUSAND)

TABLE 61 CANADA CAST FILMS MARKET, BY LAYER STRUCTURE, 2018-2033 (USD THOUSAND)

TABLE 62 CANADA CAST FILMS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 63 CANADA FOOD & BEVERAGES IN CAST FILMS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 64 CANADA PHARMACEUTICALS IN CAST FILMS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 65 USD THOUSAND

TABLE 66 MEXICO CAST FILMS MARKET, BY MATERIAL, 2018-2033 (USD THOUSAND)

TABLE 67 MEXICO POLYETHYLENE IN CAST FILMS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 68 MEXICO POLYPROPYLENE IN CAST FILMS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 69 MEXICO CAST FILMS MARKET, BY THICKNESS, 2018-2033 (USD THOUSAND)

TABLE 70 MEXICO CAST FILMS MARKET, BY PACKAGING FORMAT, 2018-2033 (USD THOUSAND)

TABLE 71 MEXICO CAST FILMS MARKET, BY LAYER STRUCTURE, 2018-2033 (USD THOUSAND)

TABLE 72 MEXICO CAST FILMS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 73 MEXICO FOOD & BEVERAGES IN CAST FILMS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 74 MEXICO PHARMACEUTICALS IN CAST FILMS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

List of Figure

FIGURE 1 NORTH AMERICA CAST FILMS MARKET: SEGMENTATION

FIGURE 2 NORTH AMERICA CAST FILMS MARKET: DATA TRIANGULATION

FIGURE 3 NORTH AMERICA CAST FILMS MARKET: DROC ANALYSIS

FIGURE 4 NORTH AMERICA CAST FILMS MARKET: NORTH AMERICA VS REGIONAL MARKET ANALYSIS

FIGURE 5 NORTH AMERICA CAST FILMS MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 NORTH AMERICA CAST FILMS MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 NORTH AMERICA CAST FILMS MARKET: DBMR MARKET POSITION GRID

FIGURE 8 NORTH AMERICA CAST FILMS MARKET: VENDOR SHARE ANALYSIS

FIGURE 9 NORTH AMERICA CAST FILMS MARKET: MULTIVARIVATE MODELING

FIGURE 10 NORTH AMERICA CAST FILMS MARKET: MATERIAL TYPE TIMELINE CURVE

FIGURE 11 NORTH AMERICA CAST FILMS MARKET: APPLICATION COVERAGE GRID

FIGURE 12 NORTH AMERICA CAST FILMS MARKET: SEGMENTATION

FIGURE 13 FIVE SEGMENTS COMPRISE THE NORTH AMERICA CAST FILMS MARKET, BY MATERIAL (2025)

FIGURE 14 NORTH AMERICA CAST FILMS MARKET: EXECUTIVE SUMMARY

FIGURE 15 STRATEGIC DECISIONS

FIGURE 16 RISING DEMAND FOR HIGH-PERFORMANCE FLEXIBLE PACKAGING SOLUTIONS IS EXPECTED TO DRIVE THE NORTH AMERICA CAST FILMS MARKET DURING THE FORECAST PERIOD OF 2026 TO 2033

FIGURE 17 POLYETHYLENE PRESSES SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE NORTH AMERICA CAST FILMS MARKET IN 2025 & 2033

FIGURE 18 DROC ANALYSIS

FIGURE 19 NORTH AMERICA CAST FILMS MARKET, BY MATERIAL, 2025

FIGURE 20 NORTH AMERICA CAST FILMS MARKET, BY THICKNESS, 2025

FIGURE 21 NORTH AMERICA CAST FILMS MARKET, BY PACKAGING FORMAT

FIGURE 22 NORTH AMERICA CAST FILMS MARKET, BY LAYER STRUCTURE, 2025

FIGURE 23 NORTH AMERICA CAST FILMS MARKET, BY APPLICATION, 2025

FIGURE 24 NORTH AMERICA CAST FILMS MARKET: SNAPSHOT (2026)

FIGURE 25 NORTH AMERICA CAST FILMSMARKET: COMPANY SHARE 2025 (%)

North America Cast Films Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its North America Cast Films Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as North America Cast Films Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.