North America Cocoa Market

Market Size in USD Billion

USD

9.68 Billion

USD

13.55 Billion

2024

2032

USD

9.68 Billion

USD

13.55 Billion

2024

2032

| 2025 - 2032 | |

| USD 9.68 Billion | |

| USD 13.55 Billion | |

| % | |

|

North America Cocoa Market Size

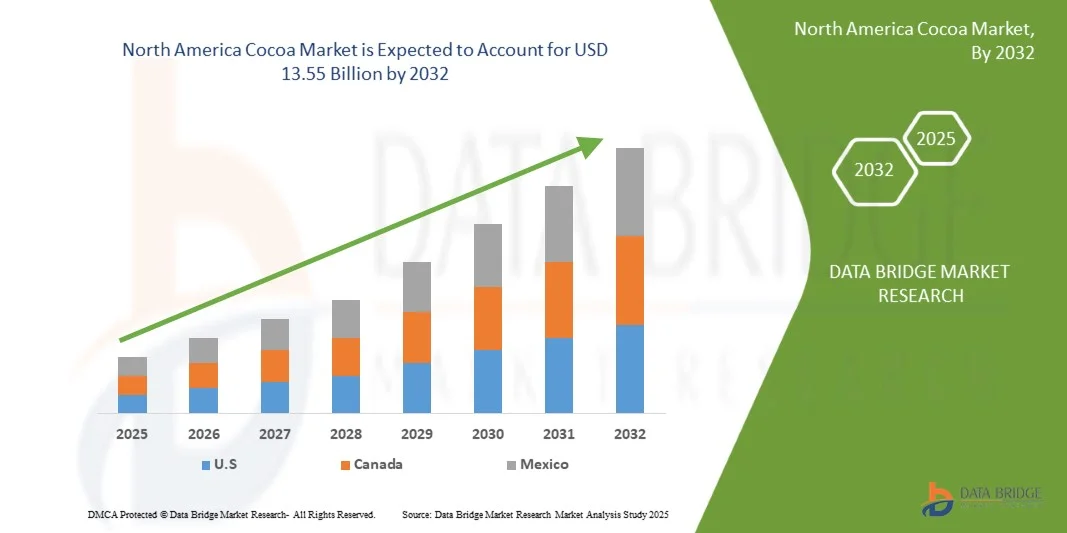

- The North America Cocoa Market was valued at USD 9.68 billion in 2024 and is expected to reach USD 13.55 billion by 2032, at a CAGR of 4.4% during the forecast period

- The market growth is largely fueled by the rising consumer demand for premium, organic, and sustainably sourced cocoa products, driven by increasing awareness of health benefits associated with dark chocolate and flavonoid-rich cocoa. The growing preference for clean-label and ethically produced ingredients is encouraging manufacturers to adopt transparent and traceable supply chains, thereby enhancing consumer trust and brand value

- Furthermore, expanding applications of cocoa across confectionery, beverages, cosmetics, and nutraceuticals, coupled with ongoing innovations in product formulations such as plant-based and low-sugar chocolate variants, are accelerating market adoption. These converging factors are significantly boosting the cocoa industry's growth and positioning it as a key segment within the food and beverage domain.

North America Cocoa Market Analysis

- The North America Cocoa Market is significantly driven by the rising demand for chocolate and confectionery products across diverse consumer segments. Chocolate remains one of the most popular indulgence products worldwide, with consumption steadily increasing in both developed and emerging economies. Cocoa, being the primary raw material for chocolate production, experiences a direct surge in demand in line with the growing chocolate industry. Factors such as evolving consumer lifestyles, increasing disposable incomes, and the expansion of premium and artisanal chocolate segments are further fueling this trend.

- Emerging trends include the rising demand for vegan and plant-based cocoa-based products, innovation in cocoa-based functional and fortified food products, and increasing popularity of single-origin and specialty cocoa varieties.

- U.S. is expected to dominate the North America Cocoa Market, holding the largest revenue share of 77.54% in 2025, attributed to increasing demand for vegan and plant-based cocoa-based products presents.

- U.S. is projected to be the fastest-growing country in the market during the forecast period with a CAGR of 4.5%, driven by its rising popularity of cocoa-based beverages and wide range of beverage products, including traditional hot chocolate, ready-to-drink cocoa beverages, flavored milk, protein shakes, and functional wellness drinks.

- The cocoa powder & cake segment is expected to dominate the North America Cocoa Market, with a market share of 37.40% in 2025, owing to the expanding application of cocoa in cosmetics and personal care products.

Report Scope and North America Cocoa Market Segmentation

|

Attributes |

North America Cocoa Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

North America Cocoa Market Trends

“Rising Demand for Chocolate and Confectionery Products”

- One prominent trend in the North America Cocoa Market is significantly driven by the rising demand for chocolate and confectionery products across diverse consumer segments.

- Cocoa, being the primary raw material for chocolate production, experiences a direct surge in demand in line with the growing chocolate industry. Factors such as evolving consumer lifestyles, increasing disposable incomes, and the expansion of premium and artisanal chocolate segments are further fueling this trend.

- For instance, in May 2024, Ferrero officially opened its chocolate processing facility in U.S., a 70,000-square-foot expansion, to service key brands such as Kinder, Ferrero Rocher, Butterfinger, and CRUNCH

- Product innovation by confectionery manufacturers, including the introduction of exotic flavors, functional chocolates with health benefits, and sustainable sourcing claims, has broadened consumer appeal.

North America Cocoa Market Dynamics

Driver

“Growing Awareness of Cocoa’s Health and Antioxidant Benefits”

- One of the key trends propelling the North America Cocoa Market is the increasing awareness of cocoa’s health-promoting properties has emerged as a strong driver for the market

- Cocoa is naturally rich in flavonoids, polyphenols, and other antioxidants that are linked to various health benefits, including improved cardiovascular health, better blood circulation, and reduced risk of chronic diseases.

- For instance, in November 2024, University of Birmingham researchers revealed that consuming high-flavanol cocoa after a high-fat meal greatly enhanced blood flow and vascular performance for up to 90 minutes, even during mental stress, suggesting a protective role for cardiovascular health in challenging dietary conditions

- The wellness trend, coupled with the rise of preventive healthcare, is expanding cocoa’s applications into categories such as cocoa-based beverages, protein powders, and beauty-from-within products. As consumers become more informed about the nutritional value of cocoa, the market is expected to benefit from sustained demand, creating new growth avenues across multiple industries beyond traditional chocolate manufacturing.

- Manufacturers are capitalizing on this awareness by promoting “dark chocolate” and “high cocoa content” products, which contain higher levels of beneficial compounds compared to milk chocolate

Opportunities

“Rising Demand for Vegan and Plant-Based Cocoa-Based Products”

- Growing adoption of vegan and plant-based lifestyles, driven by ethical, environmental, and health factors, is boosting demand for dairy-free cocoa-based products.

- Cocoa, being naturally plant-derived, aligns well with vegan trends in confectionery, bakery, and beverage industries.

- Product innovations such as dairy-free dark chocolates, plant-based cocoa beverages, and vegan-friendly cocoa spreads are gaining popularity.

- The rise of plant-based milk alternatives (almond, oat, and soy milk) supports the development of creamy, indulgent cocoa-based drinks without dairy.

- In 2023, Barry Callebaut reported strong traction for vegan chocolate brands using cocoa butter and plant milks, appealing to health- and sustainability-conscious consumers.

- Premium brands are offering ethically sourced, organic, and sustainably packaged vegan cocoa products, particularly thriving North America.

Restraint/Challenge

“Growing Competition from Alternative Ingredients in Confectionery Production”

- One of the key restraints impacting the North America Cocoa Market is the growing competition from alternative ingredients used in confectionery production. Rising cocoa prices, coupled with supply uncertainties caused by climate change and crop diseases, have encouraged manufacturers to explore cost-effective substitutes.

- Ingredients such as carob, synthetic cocoa flavors, and other plant-based alternatives are increasingly being adopted to partially or completely replace cocoa in chocolate, bakery, and beverage applications.

- Advanced food technology has enabled the development of cocoa flavor mimetics and blends that use less cocoa while maintaining taste and texture. This shift is particularly noticeable among mass-market confectionery brands seeking to maintain competitive pricing without compromising consumer appeal.

- While these alternatives may not fully replicate the premium qualities of cocoa, their increasing acceptance in certain consumer segments poses a challenge for cocoa demand.

North America Cocoa Market Scope

The North America Cocoa Market is segmented into product type, nature, types of cocoa, distribution channel, and application.

- Product Type

On the basis of product type, the market is segmented into cocoa powder & cake, cocoa butter, cocoa beans, cocoa liquor & paste, cocoa nibs, others. In 2025, the cocoa powder & cake segment is expected to dominate the market with a market share of 37.40%. The dominance of the cocoa powder & cake segment can be attributed to its widespread use in chocolate manufacturing, bakery applications, and beverage formulations. Its ease of storage, long shelf life, and compatibility with large-scale production processes make it highly preferred among food processors.

The cocoa beans segment is projected to grow with the highest CAGR of 5.2% during the forecast period due to rising demand for premium and single-origin chocolates, increasing use of raw cocoa in artisanal and craft applications, and growing consumer preference for minimally processed, natural ingredients.

- Nature

On the basis of nature, the market is segmented into conventional, organic. In 2025, the conventional segment is expected to dominate the market with a share of 92.82%. The dominance of the conventional segment is primarily driven by its cost efficiency, established supply chains, and large-scale production capabilities. Conventional cocoa offers consistent quality, making it ideal for manufacturers targeting mass-market applications.

The organic segment is anticipated to grow with the highest CAGR of 5.0% during the forecast period, owing to increasing consumer awareness of health and wellness.

- Type of Cocoa

On the basis of type of cocoa, the market is segmented into forastero cocoa, trinitario cocoa, criollo cocoa. In 2025, the forastero cocoa segment is expected to dominate with a market share of 83.53%. The dominance of the forastero cocoa segment can be attributed to its resilience, consistent quality, and suitability for mass production. Its regional cultivation footprint, supports economies of scale and meets the demands of large-scale chocolate producers. Its robustness also makes it less susceptible to disease, ensuring steady supply and affordability, driving their rapid adoption and consistent market growth

Forastero cocoa growing at the highest CAGR of 4.5% during the forecast period, due to its high yield, lower cost of production, and widespread cultivation.

- Distribution Channel

On the basis of distribution channel, the market is segmented into indirect, direct. In 2025, the Indirect segment is expected to dominate with a market share of 77.35%. The dominance of the Indirect segment is supported by the presence of established retail, wholesale, and distribution networks that facilitate access to cocoa products across both developed and emerging markets. Indirect channels offer better logistics, wider geographic coverage, and economies of scale especially for manufacturers distributing through supermarkets, wholesalers, and foodservice providers, driving their rapid adoption and consistent market growth.

The indirect segment is forecasted to grow with the highest CAGR of 4.9% during the forecast period, driven by the rapid expansion of e-commerce platforms, growing popularity of online retail channels, and increasing consumer preference for convenient purchasing options.

- Application

On the basis of application, the market is segmented into dietary supplements, food and beverage, beverage, pharmaceuticals, personal care and cosmetics. In 2025, the dietary supplements segment is anticipated to dominate with a share of 39.78%. The dominance of the dietary supplements segment is attributed to the growing recognition of cocoa’s health benefits, including its antioxidant properties, mood-enhancing effects, and cardiovascular support. Cocoa-based supplements are increasingly integrated into health-conscious diets and functional nutrition products, particularly in developed markets where preventive wellness is a major trend, driving their rapid adoption and consistent market growth.

The food and beverage segment is expected to grow with the highest CAGR of 5.0% during the forecast period, driven by increasing demand for cocoa-based snacks, bakery products, and dairy alternatives.

North America Cocoa Market Regional Analysis

- U.S. is expected to dominate the North America Cocoa Market, holding the largest market share of 77.54% in 2025, attributed to increasing demand for vegan and plant-based cocoa-based products presents.

- U.S. is projected to be the fastest-growing country in the market during the forecast period with a CAGR of 4.5%, driven by its rising popularity of cocoa-based beverages and wide range of beverage products, including traditional hot chocolate, ready-to-drink cocoa beverages, flavored milk, protein shakes, and functional wellness drinks.

- The North America Cocoa Market in the North America region is experiencing steady growth due to several key factors. One of the primary drivers is the rising demand for cocoa-based products such as chocolate, confectionery, and bakery items, fueled by a growing urban population and increasing disposable incomes. As consumer preferences shift toward Western-style diets and indulgent foods, the consumption of chocolate and cocoa-infused products is becoming more widespread, particularly in urban centers across the region. Additionally, the expanding food and beverage industry, along with a growing interest in functional foods and dietary supplements, is further boosting cocoa usage in diverse applications. The region is also witnessing a rise in organic and ethically sourced cocoa, driven by growing health awareness and sustainability concerns among consumers. Moreover, advancements in supply chain infrastructure and increased investments in local cocoa processing facilities are supporting market growth by improving product availability and reducing dependency on imports.

North America Cocoa Market Insight

North America is expected to register the CAGR of 4.4% from 2025 to 2032, large-scale consumption of chocolate and cocoa-based products, particularly in the United States. North America has a well-established and highly diversified food and beverage industry, where cocoa is a key ingredient in a broad range of products including confectionery, baked goods, dairy products, snacks, and beverages.

U.S. North America Cocoa Market Insights

U.S. is the expected to be the fastest growing with CAGR 4.5% from 2025 to 2032, the high demand for packaged and branded chocolate products, particularly during seasonal peaks such as holidays and special occasions. The U.S. is one of the world’s largest chocolate consumers and has a mature market with leading companies such as Hershey, Mars, and Mondelez driving production and innovation.

Canada North America Cocoa Market Insights

Canada continues to emerge as a significant market in the cocoa industry, supported by rising chocolate consumption and a growing preference for premium and artisanal products. The country benefits from a strong retail infrastructure and increasing demand for organic and ethically sourced cocoa ingredients. Canada is expected to be the one of the fastest growing in North America with a CAGR of 4.1% from 2025 to 2032, driven by health-conscious consumers seeking clean-label, fair-trade, and low-sugar cocoa products. Canadian manufacturers are also innovating with plant-based and functional cocoa offerings, aligning with evolving dietary trends and sustainability values, driving their rapid adoption and consistent market growth.

North America Cocoa Market Share

The cocoa industry is primarily led by well-established companies, including:

- Neogric Limited (U.K.)

- Macofa Chocolate factory (India)

- Toutan S.A (France)

- Olam International Limited (Singapore)

- Blommer Chocolate Company (U.S.)

- Deprama Cocoa (Indonesia)

- PT GRAND KAKAO INDONESIA (Indonesia)

- Jaya Saliem Industri (Indonesia)

- INDCRE S.A (Spain)

- PT ANDOW NGENSOWIDJAJA (Indonesia)

- INDOCOCOA (PT KENDO AGRI NUSANTARA) (Indonesia)

- Guan Chong Berhad (Malaysia)

- ECUAKAO GROUP LTD (Ecuador)

- CocoaCraft (India)

- Sucden (France)

- Cargill, Incorporated (U.S.)

- Cocoa Processing Company Limited (CPC) (Ghana)

- Uncommon Cacao (U.S.)

- Puratos (Belgium)

- ECOM Agroindustrial Corp. Limited (Switzerland)

- Kokoa Kamili (Tanzania)

- Barry Callebaut (Switzerland)

- JB Cocoa (Malaysia)

- Cocoa Hub (U.K.)

- Duc d’O (Part of the Baronie.com group) (Belgium)

- Natra (Spain)

- MONER COCOA, S.A. (Spain)

- Pacari Chocolate (Ecuador)

- Icam Spa (Italy)

- ALTINMARKA (Turkey)

Latest Developments in North America Cocoa Market

- In October 2024, A new cocoa production line was launched by Cargill at its Gresik plant in Indonesia to address the growing Asian appetite for indulgent foods, especially in bakery, ice cream, chocolate confectionery, and café-style beverages. The line was designed to enhance customization, enabling production of specialty cocoa powders and liquors with differentiated flavor profiles tailored to regional preferences.

- In October 2024, ICAM Cioccolato has launched a redesigned e-shop built on Shopify, offering a mobile-friendly, intuitive, and secure shopping experience. The platform showcases ICAM, Vanini, and Otto products while emphasizing sustainability and inclusivity. Featuring customer profiling for personalized marketing, the project was developed with Ecommerce School and supported by promotional campaigns to boost visibility and online sales.

- In June 2025, Kokoa Kamili, operating in Tanzania's Kilombero Valley since 2013, reaffirmed its mission to position the country as a global leader in fine-flavor cocoa. Co-founder Siman Bindra emphasized that while Tanzania produces only about 14,000 tons annually-far below major producers like Ivory Coast and Ghana-the nation's strength lies in its genetics, climate, and quality. Kokoa Kamili partners with 1,500 organic-certified farmers, has distributed over 600,000 seedlings, and is developing grafting programs from top-yielding, high-flavor trees. The company has won the Cocoa of Excellence award three times and seeks International Cocoa Organization recognition for its fine-flavor status to secure higher prices for all Tanzanian cocoa. Facing climate change challenges, Kokoa Kamili explores solar-powered irrigation and calls for national irrigation strategies to include cocoa. Bindra also aims to break the misconception that Africa produces only bulk, low-quality cocoa, stressing Tanzania's proven excellence in premium markets.

- In March 2025, Natra Cacao S.L. launched a project, supported by the European Regional Development Fund (FEDER) and the Valencian Agency of Innovation, to develop fermented products analogous to cocoa for chocolate production. The initiative explores alternative plant-based raw materials with the same organoleptic profile and functionality as fermented cocoa, aiming to create value-added products with health benefits, shorter and more resilient supply chains, and reduced dependence on volatile North America Cocoa Markets. The project also seeks to lower carbon footprint, mitigate deforestation risks, and drive innovation across the Natra group's value chain.

- In June 2025, In June, Touton showcases how collaboration, operational intelligence, and targeted innovation have driven meaningful results in forest protection, sustainable production, and community engagement in the 2023-2024 crop year. The report highlights achievements such as the distribution of hundreds of thousands of improved cocoa and multi-purpose trees in Ghana and Côte d'Ivoire, and the training of over 112,000 farmers in climate-smart practices.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 MULTIVARIATE MODELING

2.7 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.8 DBMR MARKET POSITION GRID

2.9 DBMR VENDOR SHARE ANALYSIS

2.1 MARKET APPLICATION COVERAGE GRID

2.11 SECONDARY SOURCES

2.12 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PORTER'S FIVE FORCES

4.2 IMPORT EXPORT SCENARIO

4.3 PRICING ANALYSIS

4.4 PRODUCTION CONSUMPTION ANALYSIS

4.5 SUPPLY CHAIN ANALYSIS

4.6 VALUE CHAIN ANALYSIS

4.7 VENDOR SELECTION CRITERIA

4.7.1 SOURCE: DBMR ANALYSIS

4.7.2 PRODUCT QUALITY AND CERTIFICATION

4.7.3 SOURCING AND TRACEABILITY

4.7.4 PRICING AND COST COMPETITIVENESS

4.7.5 SUSTAINABILITY AND ETHICAL PRACTICES

4.7.6 PRODUCTION CAPACITY AND RELIABILITY

4.7.7 COMPLIANCE WITH REGULATIONS

4.7.8 LOGISTICS AND SUPPLY CHAIN EFFICIENCY

4.7.9 REPUTATION AND REFERENCES

4.8 BRAND OUTLOOK

4.8.1 MARKET ROLES & POSITIONING (WHO PLAYS WHICH ROLE?)

4.8.2 PRODUCT & PACKAGING DIFFERENCES

4.8.3 SUSTAINABILITY & FARMER PROGRAMS (CRITICAL FOR REPUTATION & SUPPLY SECURITY)

4.8.4 STRENGTHS, COMPETITIVE EDGES, AND CUSTOMER FIT

4.8.5 RISKS & MARKET PRESSURES (INDUSTRY-WIDE)

4.8.6 STRATEGIC TAKEAWAYS FOR REPORT READERS

4.8.7 WHY THIS LAYOUT?

4.8.8 BARRY CALLEBAUT — FULL-SPECTRUM CHOCOLATE LEADER

4.8.9 CARGILL — CUSTOM SOLUTIONS + INDUSTRY SCALE

4.8.10 OLAM — ORIGINATION & PROCESSING BACKBONE

4.8.11 GUAN CHONG (GCB) — EFFICIENT PROCESSOR

4.8.12 BLOMMER — NORTH AMERICA PROCESSOR & SERVICE

4.9 CONSUMER BUYING BEHAVIOUR

4.9.1 PROBLEM RECOGNITION AND AWARENESS

4.9.2 INFORMATION SEARCH

4.9.3 EVALUATION OF ALTERNATIVES

4.9.4 PURCHASE DECISION

4.9.5 POST-PURCHASE BEHAVIOUR

4.9.6 DEMOGRAPHIC INSIGHTS

4.9.7 CONCLUSION

4.1 COST ANALYSIS BREAKDOWN

4.10.1 INITIAL INVESTMENT AND CAPITAL EXPENDITURE (CAPEX)

4.10.2 INSTALLATION AND INFRASTRUCTURE ADAPTATION

4.10.3 ENERGY CONSUMPTION AND OPERATIONAL COST (OPEX)

4.10.4 MAINTENANCE AND SERVICING

4.10.5 OVERHEAD AND INDIRECT COSTS

4.10.6 STRATEGIC INVESTMENT CONSIDERATIONS

4.11 INNOVATION TRACKER AND STRATEGIC ANALYSIS

4.11.1 MAJOR DEALS AND STRATEGIC ALLIANCES ANALYSIS

4.11.1.1 JOINT VENTURES

4.11.1.2 MERGERS AND ACQUISITIONS

4.11.1.3 LICENSING AND PARTNERSHIP

4.11.1.4 TECHNOLOGY COLLABORATIONS

4.11.1.5 STRATEGIC DIVESTMENTS

4.11.2 NUMBER OF PRODUCTS IN DEVELOPMENT

4.11.3 STAGE OF DEVELOPMENT

4.11.4 TIMELINES AND MILESTONES

4.11.5 INNOVATION STRATEGIES AND METHODOLOGIES

4.11.6 RISK ASSESSMENT AND MITIGATION

4.11.7 FUTURE OUTLOOK

4.12 PROFIT MARGINS SCENARIO

4.12.1 FACTORS INFLUENCING PROFITABILITY

4.12.2 VALUE ADDITION:

4.12.3 QUALITY & CERTIFICATION:

4.12.4 MARKET DEMAND:

4.12.5 BUSINESS MODEL:

4.13 RAW MATERIAL COVERAGE

4.13.1 COCOA BEANS (PRIMARY RAW MATERIAL)

4.13.2 SUGAR (SWEETENING AGENT)

4.13.3 COCOA BUTTER (FAT COMPONENT)

4.13.4 MILK POWDER (DAIRY INGREDIENT)

4.13.5 LECITHIN (EMULSIFIER)

4.14 TECHNOLOGICAL ADVANCEMENTS BY MANUFACTURER

4.14.1 ADVANCED COCOA BEAN ROASTING TECHNOLOGIES

4.14.2 AUTOMATED COCOA PROCESSING AND PRODUCTION SYSTEMS

4.14.3 AI-DRIVEN QUALITY CONTROL AND DEFECT DETECTION

4.14.4 ENERGY-EFFICIENT GRINDING AND CONCHING EQUIPMENT

4.14.5 SMART PACKAGING AND SHELF-LIFE EXTENSION SOLUTIONS

4.14.6 DIGITAL SUPPLY CHAIN AND TRACEABILITY INTEGRATION

4.15 PATENT ANALYSIS –

4.15.1 PATENT QUALITY AND STRENGTH

4.15.2 PATENT FAMILIES

4.15.3 NUMBER OF INTERNATIONAL PATENT FAMILIES BY PUBLICATION YEAR

4.15.4 REGION PATENT LANDSCAPE

4.15.5 IP STRATEGY AND MANAGEMENT

4.15.6 PATENT ANALYSIS – TOP APPLICANTS

5 TARIFFS & IMPACT ON THE NORTH AMERICA COCOA MARKET

5.1 CURRENT TARIFF RATE(S) IN TOP-5 COUNTRY MARKETS

5.2 OUTLOOK: LOCAL PRODUCTION V/S IMPORT RELIANCE

5.3 VENDOR SELECTION CRITERIA DYNAMICS

5.4 IMPACT ON SUPPLY CHAIN

5.4.1 RAW MATERIAL PROCUREMENT

5.4.2 MANUFACTURING AND PRODUCTION

5.4.3 LOGISTICS AND DISTRIBUTION

5.4.4 PRICE PITCHING AND POSITION OF MARKET

5.5 INDUSTRY PARTICIPANTS: PROACTIVE MOVES

5.5.1 SUPPLY CHAIN OPTIMIZATION

5.5.2 JOINT VENTURE ESTABLISHMENTS

5.6 IMPACT ON PRICES

5.7 REGULATORY INCLINATION

5.7.1 GEOPOLITICAL SITUATION

5.7.2 TRADE PARTNERSHIPS BETWEEN THE COUNTRIES

5.7.2.1 FREE TRADE AGREEMENTS

5.7.2.2 ALLIANCE ESTABLISHMENTS

5.7.3 STATUS ACCREDITATION (INCLUDING MFN)

5.7.4 DOMESTIC COURSE OF CORRECTION

5.7.4.1 INCENTIVE SCHEMES TO BOOST PRODUCTION OUTPUTS

5.7.4.2 ESTABLISHMENT OF SPECIAL ECONOMIC ZONES / INDUSTRIAL PARKS

6 REGULATION COVERAGE

7 BEANS AND RATIOS FOR HISTORY AND FORECAST AND WITH CONCRETE DATA

8 MARKET OVERVIEW

8.1 DRIVERS

8.1.1 RISING DEMAND FOR CHOCOLATE AND CONFECTIONERY PRODUCTS

8.1.2 GROWING AWARENESS OF COCOA’S HEALTH AND ANTIOXIDANT BENEFITS

8.1.3 EXPANDING USE OF COCOA IN COSMETICS AND PERSONAL CARE

8.1.4 GROWTH IN COCOA-BASED BEVERAGES

8.2 RESTRAINTS

8.2.1 GROWING COMPETITION FROM ALTERNATIVE INGREDIENTS IN CONFECTIONERY PRODUCTION

8.2.2 STRINGENT REGULATORY STANDARDS FOR COCOA QUALITY AND SAFETY COMPLIANCE

8.3 OPPORTUNITIES

8.3.1 RISING DEMAND FOR VEGAN AND PLANT-BASED COCOA-BASED PRODUCTS

8.3.2 INNOVATION IN COCOA-BASED FUNCTIONAL AND FORTIFIED FOOD PRODUCTS

8.3.3 INCREASING POPULARITY OF SINGLE-ORIGIN AND SPECIALTY COCOA VARIETIES

8.4 CHALLENGE

8.5 CLIMATE CHANGE REDUCING COCOA YIELDS AND AFFECTING QUALITY

8.5.1 LIMITED FARMER ACCESS TO MODERN FARMING TOOLS AND TRAINING

9 NORTH AMERICA COCOA MARKET, BY PRODUCT TYPE

9.1 OVERVIEW

9.2 COCOA POWDER & CAKE

9.3 COCOA BUTTER

9.4 COCOA BEANS

9.5 COCOA LIQUOR & PASTE

9.6 COCOA NIBS

9.7 OTHERS

10 NORTH AMERICA COCOA MARKET, BY NATURE

10.1 OVERVIEW

10.2 CONVENTIONAL

10.3 ORGANIC

11 NORTH AMERICA COCOA MARKET, BY TYPE OF COCOA

11.1 OVERVIEW

11.2 FORASTERO COCOA

11.3 TRINITARIO COCOA

11.4 CRIOLLO COCOA

12 NORTH AMERICA COCOA MARKET, BY DISTRIBUTION CHANNEL

12.1 OVERVIEW

12.2 INDIRECT

12.3 DIRECT

13 NORTH AMERICA COCOA MARKET, BY APPLICATION

13.1 OVERVIEW

13.2 DIETARY SUPPLEMENTS

13.3 FOOD AND BEVERAGE

13.4 BEVERAGE

13.5 PHARMACEUTICALS

13.6 PERSONAL CARE AND COSMETICS

14 NORTH AMERICA COCOA MARKET, BY REGION

14.1 NORTH AMERICA

14.1.1 U.S.

14.1.2 CANADA

14.1.3 MEXICO

15 NORTH AMERICA COCOA MARKET, COMPANY LANDSCAPE

15.1 COMPANY SHARE ANALYSIS: NORTH AMERICA

16 SWOT ANALYSIS

17 COMPANY PROFILES

17.1 OLAM GROUP

17.1.1 COMPANY SNAPSHOT

17.1.2 RECENT FINANCIALS

17.1.3 COMPANY SHARE ANALYSIS

17.1.4 PRODUCT PORTFOLIO

17.1.5 RECENT UPDATES

17.2 BARRY CALLEBAUT

17.2.1 COMPANY SNAPSHOT

17.2.2 REVENUE ANALYSIS

17.2.3 COMPANY SHARE ANALYSIS

17.2.4 PRODUCT PORTFOLIO

17.2.5 RECENT DEVELOPMENT

17.3 ECOM AGROINDUSTRIAL CORP. LIMITED.

17.3.1 COMPANY SNAPSHOT

17.3.2 COMPANY SHARE ANALYSIS

17.3.3 PRODUCT PORTFOLIO

17.3.4 RECENT DEVELOPMENTS/NEWS

17.4 PURATOS

17.4.1 COMPANY SNAPSHOT

17.4.2 COMPANY SHARE ANALYSIS

17.4.3 PRODUCT PORTFOLIO

17.4.4 RECENT DEVELOPMENT

17.5 GUAN CHONG BERHAD (GCB)

17.5.1 COMPANY SNAPSHOT

17.5.2 COMPANY SHARE ANALYSIS

17.5.3 PRODUCT PORTFOLIO

17.5.4 RECENT DEVELOPMENTS/NEWS

17.6 JB COCOA

17.6.1 COMPANY SNAPSHOT

17.6.2 REVENUE ANALYSIS

17.6.3 RECENT DEVELOPMENT

17.7 ALTINMARKA

17.7.1 COMPANY SNAPSHOT

17.7.2 PRODUCT PORTFOLIO

17.7.3 RECENT UPDATES

17.8 BLOMMER CHOCOLATE COMPANY

17.8.1 COMPANY SNAPSHOT

17.8.2 PRODUCT PORTFOLIO

17.8.3 RECENT DEVELOPMENT

17.9 CARGILL, INCORPORATED.

17.9.1 COMPANY SNAPSHOT

17.9.2 PRODUCT PORTFOLIO

17.9.3 RECENT DEVELOPMENT

17.1 COCOA HUB

17.10.1 COMPANY SNAPSHOT

17.10.2 PRODUCT PORTFOLIO

17.10.3 RECENT DEVELOPMENTS/NEWS

17.11 COCOA PROCESSING COMPANY LIMITED (CPC)

17.11.1 COMPANY SNAPSHOT

17.11.2 RECENT FINANCIALS

17.11.3 PRODUCT PORTFOLIO

17.11.4 RECENT UPDATES

17.12 COCOACRAFT

17.12.1 COMPANY SNAPSHOT

17.12.2 PRODUCT PORTFOLIO

17.12.3 RECENT DEVELOPMENTS/NEWS

17.13 DEPRAMA COCOA

17.13.1 COMPANY SNAPSHOT

17.13.2 PRODUCT PORTFOLIO

17.13.3 RECENT UPDATES

17.14 DUC D’O

17.14.1 COMPANY SNAPSHOT

17.14.2 PRODUCT PORTFOLIO

17.14.3 RECENT DEVELOPMENTS/NEWS

17.15 ECUAKAO GROUP LTD

17.15.1 COMPANY SNAPSHOT

17.15.2 PRODUCT PORTFOLIO

17.15.3 RECENT DEVELOPMENTS/NEWS

17.16 ICAM SPA

17.16.1 COMPANY SNAPSHOT

17.16.2 PRODUCT PORTFOLIO

17.16.3 RECENT UPDATES

17.17 INDCRE S.A

17.17.1 COMPANY SNAPSHOT

17.17.2 PRODUCT PORTFOLIO

17.17.3 RECENT UPDATES

17.18 INDOCOCOA

17.18.1 COMPANY SNAPSHOT

17.18.2 PRODUCT PORTFOLIO

17.18.3 RECENT DEVELOPMENTS/NEWS

17.19 JAYA SALIEM INDUSTRI

17.19.1 COMPANY SNAPSHOT

17.19.2 PRODUCT PORTFOLIO

17.19.3 RECENT DEVELOPMENT

17.2 KOKOA KAMILI

17.20.1 COMPANY SNAPSHOT

17.20.2 PRODUCT PORTFOLIO

17.20.3 RECENT DEVELOPMENTS/NEWS

17.21 MACOFA CHOCOLATE FACTORY

17.21.1 COMPANY SNAPSHOT

17.21.2 PRODUCT PORTFOLIO

17.21.3 RECENT DEVELOPMENT

17.22 MONER COCOA, S.A.

17.22.1 COMPANY SNAPSHOT

17.22.2 PRODUCT PORTFOLIO

17.22.3 RECENT UPDATES

17.23 NATRA

17.23.1 COMPANY SNAPSHOT

17.23.2 PRODUCT PORTFOLIO

17.23.3 RECENT DEVELOPMENTS/NEWS

17.24 NEOGRIC LIMITED

17.24.1 COMPANY SNAPSHOT

17.24.2 PRODUCT PORTFOLIO

17.24.3 RECENT DEVELOPMENT

17.25 PACARI

17.25.1 COMPANY SNAPSHOT

17.25.2 PRODUCT PORTFOLIO

17.25.3 RECENT UPDATES

17.26 PT ANDOW NGENSOWIDJAJA

17.26.1 COMPANY SNAPSHOT

17.26.2 PRODUCT PORTFOLIO

17.26.3 RECENT DEVELOPMENTS/NEWS

17.27 PT GRAND KAKAO INDONESIA

17.27.1 COMPANY SNAPSHOT

17.27.2 PRODUCT PORTFOLIO

17.27.3 RECENT DEVELOPMENT

17.28 TOUTON S.A.

17.28.1 COMPANY SNAPSHOT

17.28.2 PRODUCT PORTFOLIO

17.28.3 RECENT DEVELOPMENT

17.29 UNCOMMON CACOA .

17.29.1 COMPANY SNAPSHOT

17.29.2 PRODUCT PORTFOLIO

17.29.3 RECENT UPDATES

18 QUESTIONNAIRE

19 RELATED REPORTS

List of Table

TABLE 1 BRAND COMPARATIVE ANALYSIS

TABLE 2 FIGURE 2. COMPANY VS BRAND OVERVIEW

TABLE 3 NUMBER OF PATENTS PER YEAR

TABLE 4 NUMBER OF PATENTS PER REGION/COUNTRY

TABLE 5 TOP PATENT APPLICANTS.

TABLE 6 REGULATORY COVERAGE

TABLE 7 NORTH AMERICA COCOA MARKET, BY PRODUCT TYPE, 2018-2032 (USD THOUSAND)

TABLE 8 NORTH AMERICA COCOA MARKET, BY PRODUCT TYPE, 2018-2032 (TONS)

TABLE 9 NORTH AMERICA COCOA MARKET, BY PRODUCT TYPE, 2018-2032 (PRICE USD/KG)

TABLE 10 NORTH AMERICA COCOA BUTTER IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 11 NORTH AMERICA COCOA MARKET, BY NATURE, 2025-2032 (USD THOUSAND)

TABLE 12 NORTH AMERICA COCOA MARKET, BY NATURE, 2025-2032 (TONS)

TABLE 13 NORTH AMERICA COCOA MARKET, BY NATURE, 2025-2032 (PRICE USD/KG)

TABLE 14 NORTH AMERICA COCOA MARKET, BY TYPE OF COCOA, 2025-2032 (USD THOUSAND)

TABLE 15 NORTH AMERICA COCOA MARKET, BY TYPE OF COCOA, 2025-2032 (TONS)

TABLE 16 NORTH AMERICA COCOA MARKET, BY TYPE OF COCOA, 2025-2032 (PRICE USD/KG)

TABLE 17 NORTH AMERICA COCOA MARKET, BY DISTRIBUTION CHANNEL, 2025-2032 (USD THOUSAND)

TABLE 18 NORTH AMERICA COCOA MARKET, BY DISTRIBUTION CHANNEL, 2025-2032 (TONS)

TABLE 19 NORTH AMERICA COCOA MARKET, BY DISTRIBUTION CHANNEL, 2025-2032 (PRICE USD/KG)

TABLE 20 NORTH AMERICA INDIRECT IN COCOA MARKET, BY TYPE, 2025-2032 (USD THOUSAND)

TABLE 21 NORTH AMERICA OFFLINE DISTRIBUTION CHANNEL IN COCOA MARKET, BY TYPE, 2025-2032 (USD THOUSAND)

TABLE 22 NORTH AMERICA COCOA MARKET, BY APPLICATION, 2025-2032 (USD THOUSAND)

TABLE 23 NORTH AMERICA FOOD AND BEVERAGE IN COCOA MARKET, BY TYPE, 2025-2032 (USD THOUSAND)

TABLE 24 NORTH AMERICA BAKERY IN COCOA MARKET, BY TYPE, 2025-2032 (USD THOUSAND)

TABLE 25 NORTH AMERICA CONFECTIONERY IN COCOA MARKET, BY TYPE, 2025-2032 (USD THOUSAND)

TABLE 26 NORTH AMERICA CHOCLATE IN COCOA MARKET, BY TYPE, 2025-2032 (USD THOUSAND)

TABLE 27 NORTH AMERICA CHOCOLATE IN COCOA MARKET, BY CATEGORY, 2025-2032 (USD THOUSAND)

TABLE 28 NORTH AMERICA WHITE CHOCOLATE IN COCOA MARKET, BY TYPE, 2025-2032 (USD THOUSAND)

TABLE 29 NORTH AMERICA DAIRY PRODUCTS IN COCOA MARKET, BY TYPE, 2025-2032 (USD THOUSAND)

TABLE 30 NORTH AMERICA PROCESSED FOOD IN COCOA MARKET, BY TYPE, 2025-2032 (USD THOUSAND)

TABLE 31 NORTH AMERICA BEVERAGES IN COCOA MARKET, BY TYPE, 2025-2032 (USD THOUSAND)

TABLE 32 NORTH AMERICA DAIRY-BASED DRINKS IN COCOA MARKET, BY TYPE, 2025-2032 (USD THOUSAND)

TABLE 33 NORTH AMERICA PERSONAL CARE AND COSMETICS IN COCOA MARKET, BY TYPE, 2025-2032 (USD THOUSAND)

TABLE 34 NORTH AMERICA COCOA MARKET, BY APPLICATION, 2025-2032 (TONS)

TABLE 35 NORTH AMERICA COCOA MARKET, BY APPLICATION, 2025-2032 (PRICE USD/KG)

TABLE 36 NORTH AMERICA COCOA MARKET, BY COUNTRY, 2018-2032 (USD THOUSAND)

TABLE 37 NORTH AMERICA COCOA MARKET, BY COUNTRY, 2018-2032 (TONS)

TABLE 38 NORTH AMERICA COCOA MARKET, BY PRODUCT TYPE, 2018-2032 (USD THOUSAND)

TABLE 39 NORTH AMERICA COCOA MARKET, BY PRODUCT TYPE, 2018-2032 (TONS)

TABLE 40 NORTH AMERICA COCOA MARKET, BY PRODUCT TYPE, 2018-2032 (PRICE USD/KG)

TABLE 41 NORTH AMERICA COCOA BUTTER IN COCOA MARKET, BY PRODUCT TYPE, 2018-2032 (USD THOUSAND)

TABLE 42 NORTH AMERICA COCOA MARKET, BY NATURE, 2018-2032 (USD THOUSAND)

TABLE 43 NORTH AMERICA COCOA MARKET, BY NATURE, 2018-2032 (TONS)

TABLE 44 NORTH AMERICA COCOA MARKET, BY NATURE, 2018-2032 (PRICE USD/KG)

TABLE 45 NORTH AMERICA COCOA MARKET, BY TYPE OF COCOA, 2018-2032 (USD THOUSAND)

TABLE 46 NORTH AMERICA COCOA MARKET, BY TYPE OF COCOA, 2018-2032 (TONS)

TABLE 47 NORTH AMERICA COCOA MARKET, BY TYPE OF COCOA, 2018-2032 (PRICE USD/KG)

TABLE 48 NORTH AMERICA COCOA MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD THOUSAND)

TABLE 49 NORTH AMERICA COCOA MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (TONS)

TABLE 50 NORTH AMERICA COCOA MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (PRICE USD/KG)

TABLE 51 NORTH AMERICA INDIRECT IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 52 NORTH AMERICA OFFLINE DISTRIBUTION CHANNEL IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 53 NORTH AMERICA COCOA MARKET, BY APPLICATION, 2018-2032 (USD THOUSAND)

TABLE 54 NORTH AMERICA COCOA MARKET, BY APPLICATION, 2018-2032 (TONS)

TABLE 55 NORTH AMERICA COCOA MARKET, BY APPLICATION, 2018-2032 (PRICE USD/KG)

TABLE 56 NORTH AMERICA FOOD AND BEVERAGE IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 57 NORTH AMERICA BAKERY IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 58 NORTH AMERICA CONFECTIONERY IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 59 NORTH AMERICA CHOCOLATE IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 60 NORTH AMERICA CHOCOLATE IN COCOA MARKET, BY CATEGORY, 2018-2032 (USD THOUSAND)

TABLE 61 NORTH AMERICA WHITE CHOCOLATE IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 62 NORTH AMERICA DAIRY PRODUCTS IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 63 NORTH AMERICA PROCESSED FOOD IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 64 NORTH AMERICA BEVERAGE IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 65 NORTH AMERICA DAIRY-BASED DRINKS IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 66 NORTH AMERICA PERSONAL CARE AND COSMETICS IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 67 U.S. COCOA MARKET, BY PRODUCT TYPE, 2018-2032 (USD THOUSAND)

TABLE 68 U.S. COCOA MARKET, BY PRODUCT TYPE, 2018-2032 (TONS)

TABLE 69 U.S. COCOA MARKET, BY PRODUCT TYPE, 2018-2032 (PRICE USD/KG)

TABLE 70 U.S. COCOA BUTTER IN COCOA MARKET, BY PRODUCT TYPE, 2018-2032 (USD THOUSAND)

TABLE 71 U.S. COCOA MARKET, BY NATURE, 2018-2032 (USD THOUSAND)

TABLE 72 U.S. COCOA MARKET, BY NATURE, 2018-2032 (TONS)

TABLE 73 U.S. COCOA MARKET, BY NATURE, 2018-2032 (PRICE USD/KG)

TABLE 74 U.S. COCOA MARKET, BY TYPE OF COCOA, 2018-2032 (USD THOUSAND)

TABLE 75 U.S. COCOA MARKET, BY TYPE OF COCOA, 2018-2032 (TONS)

TABLE 76 U.S. COCOA MARKET, BY TYPE OF COCOA, 2018-2032 (PRICE USD/KG)

TABLE 77 U.S. COCOA MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD THOUSAND)

TABLE 78 U.S. COCOA MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (TONS)

TABLE 79 U.S. COCOA MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (PRICE USD/KG)

TABLE 80 U.S. INDIRECT IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 81 U.S. OFFLINE DISTRIBUTION CHANNEL IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 82 U.S. COCOA MARKET, BY APPLICATION, 2018-2032 (USD THOUSAND)

TABLE 83 U.S. COCOA MARKET, BY APPLICATION, 2018-2032 (TONS)

TABLE 84 U.S. COCOA MARKET, BY APPLICATION, 2018-2032 (PRICE USD/KG)

TABLE 85 U.S. FOOD AND BEVERAGE IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 86 U.S. BAKERY IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 87 U.S. CONFECTIONERY IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 88 U.S. CHOCOLATE IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 89 U.S. CHOCOLATE IN COCOA MARKET, BY CATEGORY, 2018-2032 (USD THOUSAND)

TABLE 90 U.S. WHITE CHOCOLATE IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 91 U.S. DAIRY PRODUCTS IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 92 U.S. PROCESSED FOOD IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 93 U.S. BEVERAGE IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 94 U.S. DAIRY-BASED DRINKS IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 95 U.S. PERSONAL CARE AND COSMETICS IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 96 CANADA COCOA MARKET, BY PRODUCT TYPE, 2018-2032 (USD THOUSAND)

TABLE 97 CANADA COCOA MARKET, BY PRODUCT TYPE, 2018-2032 (TONS)

TABLE 98 CANADA COCOA MARKET, BY PRODUCT TYPE, 2018-2032 (PRICE USD/KG)

TABLE 99 CANADA COCOA BUTTER IN COCOA MARKET, BY PRODUCT TYPE, 2018-2032 (USD THOUSAND)

TABLE 100 CANADA COCOA MARKET, BY NATURE, 2018-2032 (USD THOUSAND)

TABLE 101 CANADA COCOA MARKET, BY NATURE, 2018-2032 (TONS)

TABLE 102 CANADA COCOA MARKET, BY NATURE, 2018-2032 (PRICE USD/KG)

TABLE 103 CANADA COCOA MARKET, BY TYPE OF COCOA, 2018-2032 (USD THOUSAND)

TABLE 104 CANADA COCOA MARKET, BY TYPE OF COCOA, 2018-2032 (TONS)

TABLE 105 CANADA COCOA MARKET, BY TYPE OF COCOA, 2018-2032 (PRICE USD/KG)

TABLE 106 CANADA COCOA MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD THOUSAND)

TABLE 107 CANADA COCOA MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (TONS)

TABLE 108 CANADA COCOA MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (PRICE USD/KG)

TABLE 109 CANADA INDIRECT IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 110 CANADA OFFLINE DISTRIBUTION CHANNEL IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 111 CANADA COCOA MARKET, BY APPLICATION, 2018-2032 (USD THOUSAND)

TABLE 112 CANADA COCOA MARKET, BY APPLICATION, 2018-2032 (TONS)

TABLE 113 CANADA COCOA MARKET, BY APPLICATION, 2018-2032 (PRICE USD/KG)

TABLE 114 CANADA FOOD AND BEVERAGE IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 115 CANADA BAKERY IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 116 CANADA CONFECTIONERY IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 117 CANADA CHOCOLATE IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 118 CANADA CHOCOLATE IN COCOA MARKET, BY CATEGORY, 2018-2032 (USD THOUSAND)

TABLE 119 CANADA WHITE CHOCOLATE IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 120 CANADA DAIRY PRODUCTS IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 121 CANADA PROCESSED FOOD IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 122 CANADA BEVERAGE IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 123 CANADA DAIRY-BASED DRINKS IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 124 CANADA PERSONAL CARE AND COSMETICS IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 125 MEXICO COCOA MARKET, BY PRODUCT TYPE, 2018-2032 (USD THOUSAND)

TABLE 126 MEXICO COCOA MARKET, BY PRODUCT TYPE, 2018-2032 (TONS)

TABLE 127 MEXICO COCOA MARKET, BY PRODUCT TYPE, 2018-2032 (PRICE USD/KG)

TABLE 128 MEXICO COCOA BUTTER IN COCOA MARKET, BY PRODUCT TYPE, 2018-2032 (USD THOUSAND)

TABLE 129 MEXICO COCOA MARKET, BY NATURE, 2018-2032 (USD THOUSAND)

TABLE 130 MEXICO COCOA MARKET, BY NATURE, 2018-2032 (TONS)

TABLE 131 MEXICO COCOA MARKET, BY NATURE, 2018-2032 (PRICE USD/KG)

TABLE 132 MEXICO COCOA MARKET, BY TYPE OF COCOA, 2018-2032 (USD THOUSAND)

TABLE 133 MEXICO COCOA MARKET, BY TYPE OF COCOA, 2018-2032 (TONS)

TABLE 134 MEXICO COCOA MARKET, BY TYPE OF COCOA, 2018-2032 (PRICE USD/KG)

TABLE 135 MEXICO COCOA MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD THOUSAND)

TABLE 136 MEXICO COCOA MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (TONS)

TABLE 137 MEXICO COCOA MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (PRICE USD/KG)

TABLE 138 MEXICO INDIRECT IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 139 MEXICO OFFLINE DISTRIBUTION CHANNEL IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 140 MEXICO COCOA MARKET, BY APPLICATION, 2018-2032 (USD THOUSAND)

TABLE 141 MEXICO COCOA MARKET, BY APPLICATION, 2018-2032 (TONS)

TABLE 142 MEXICO COCOA MARKET, BY APPLICATION, 2018-2032 (PRICE USD/KG)

TABLE 143 MEXICO FOOD AND BEVERAGE IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 144 MEXICO BAKERY IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 145 MEXICO CONFECTIONERY IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 146 MEXICO CHOCOLATE IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 147 MEXICO CHOCOLATE IN COCOA MARKET, BY CATEGORY, 2018-2032 (USD THOUSAND)

TABLE 148 MEXICO WHITE CHOCOLATE IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 149 MEXICO DAIRY PRODUCTS IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 150 MEXICO PROCESSED FOOD IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 151 MEXICO BEVERAGE IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 152 MEXICO DAIRY-BASED DRINKS IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 153 MEXICO PERSONAL CARE AND COSMETICS IN COCOA MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

List of Figure

FIGURE 1 NORTH AMERICA COCOA MARKET

FIGURE 2 NORTH AMERICA COCOA MARKET: DATA TRIANGULATION

FIGURE 3 NORTH AMERICA COCOA MARKET: DROC ANALYSIS

FIGURE 4 NORTH AMERICA COCOA MARKET: REGIONAL MARKET ANALYSIS

FIGURE 5 NORTH AMERICA COCOA MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 NORTH AMERICA COCOA MARKET: MULTIVARIATE MODELLING

FIGURE 7 NORTH AMERICA COCOA MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 8 NORTH AMERICA COCOA MARKET: DBMR MARKET POSITION GRID

FIGURE 9 NORTH AMERICA COCOA MARKET: VENDOR SHARE ANALYSIS

FIGURE 10 NORTH AMERICA COCOA MARKET: SEGMENTATION

FIGURE 11 EUROPE IS EXPECTED TO DOMINATE THE NORTH AMERICA COCOA MARKET AND IS EXPECTED TO GROW WITH THE HIGHEST CAGR IN THE FORECAST PERIOD

FIGURE 12 EXECUTIVE SUMMARY

FIGURE 13 SIX SEGMENTS COMPRISE THE NORTH AMERICA COCOA MARKET, BY PRODUCT TYPE (2024)

FIGURE 14 STRATEGIC DECISIONS

FIGURE 15 RISING DEMAND FOR CHOCOLATE AND CONFECTIONERY PRODUCTS IS EXPECTED TO DRIVE THE NORTH AMERICA COCOA MARKET IN THE FORECAST PERIOD (2025-2032)

FIGURE 16 THE COCOA POWDER & CAKE SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE NORTH AMERICA COCOA MARKET IN 2025 AND 2032

FIGURE 17 IMPORT EXPORT SCENARIO (USD THOUSAND)

FIGURE 18 NORTH AMERICA COCOA MARKET, 2022-2032, AVERAGE SELLING PRICE (USD/KG)

FIGURE 19 PRODUCTION CONSUMPTION ANALYSIS

FIGURE 20 VENDOR SELECTION CRITERIA

FIGURE 21 IPC CODE V/S NUMBER OF PATENTS

FIGURE 22 NUMBER OF PATENTS PER YEAR

FIGURE 23 NUMBER OF PATENTS PER REGION/COUNTRY

FIGURE 24 TOP PATENT APPLICANTS.

FIGURE 25 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES OF THE NORTH AMERICA COCOA MARKET

FIGURE 26 NORTH AMERICA COCOA MARKET: BY PRODUCT TYPE, 2024

FIGURE 27 NORTH AMERICA COCOA MARKET: BY NATURE, 2024

FIGURE 28 NORTH AMERICA COCOA MARKET: BY TYPE OF COCOA, 2024

FIGURE 29 NORTH AMERICA COCOA MARKET: BY DISTRIBUTION CHANNEL, 2024

FIGURE 30 NORTH AMERICA COCOA MARKET: BY APPLICATION, 2024

FIGURE 31 NORTH AMERICA COCOA MARKET: SNAPSHOT (2024)

FIGURE 32 NORTH AMERICA COCOA MARKET: COMPANY SHARE 2024 (%)

North America Cocoa Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its North America Cocoa Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as North America Cocoa Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.