North America Collaborative Robot Market

Market Size in USD Billion

USD

1.80 Billion

USD

18.94 Billion

2024

2032

USD

1.80 Billion

USD

18.94 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.80 Billion | |

| USD 18.94 Billion | |

| % | |

|

Collaborative Robot Market Size

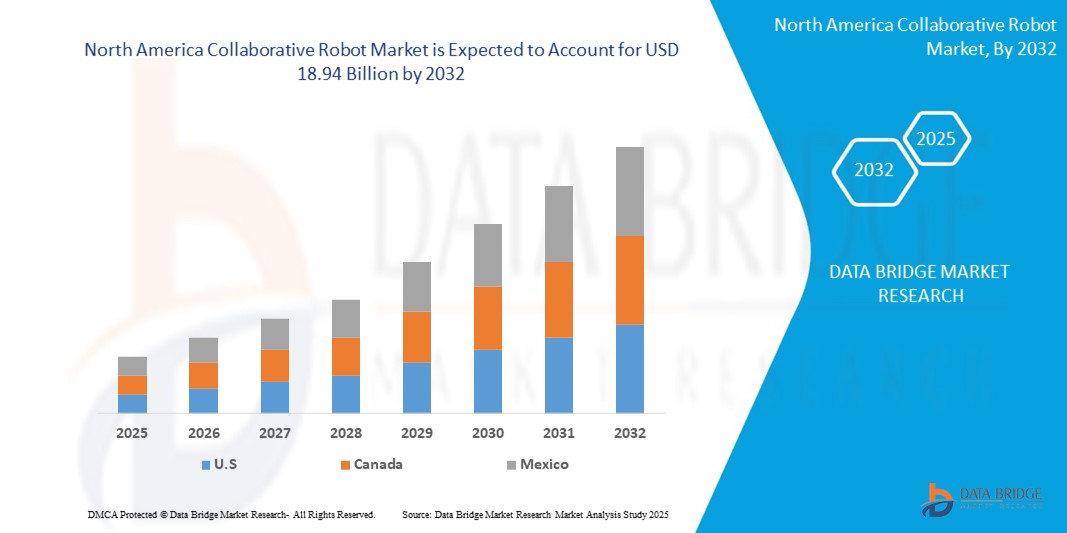

- The North America Collaborative Robot market size was valued at USD 1.80 billion in 2024 and is expected to reach USD 18.94 billion by 2032, at a CAGR of 34.20% during the forecast period

- Market expansion is being driven by increased automation across industries such as automotive, electronics, healthcare, and logistics, where collaborative robots (cobots) enhance productivity and flexibility while ensuring worker safety.

- Additionally, the affordability, ease of programming, and scalability of cobots make them ideal for small and medium-sized enterprises (SMEs), further fueling adoption. These trends, combined with advancements in AI and sensor technology, are accelerating the deployment of collaborative robots throughout North America.

Collaborative Robot Market Analysis

- Collaborative robots, or cobots, designed to work safely alongside humans, are increasingly being integrated into industrial and non-industrial workflows across North America due to their flexibility, ease of deployment, and enhanced safety features. These robots are becoming critical tools in manufacturing, logistics, and healthcare sectors, where they streamline operations and improve productivity.

- The rapid adoption of Industry 4.0 practices, labor shortages, and rising demand for automation in SMEs are key drivers propelling the demand for collaborative robots. Their ability to handle repetitive tasks with high precision while being cost-effective is positioning them as a preferred automation solution across diverse industries.

- The U.S. dominates the North America collaborative robot market with a revenue share of over 70.0% in 2024, supported by early automation adoption, strong manufacturing base, and significant investments in robotics R&D. Major U.S. firms are leveraging cobots to optimize production lines, especially in automotive and electronics sectors.

- Canada is emerging as a high-growth region for collaborative robots, driven by expanding industrial automation, supportive government policies, and increased focus on smart manufacturing solutions among SMEs.

- The up to 5 kg payload segment holds the largest market share of 42.7% in 2024, as these lightweight cobots are ideal for high-precision, low-payload tasks such as pick-and-place, quality inspection, and assembly in electronics and small parts manufacturing.

Report Scope and Collaborative Robot Market Segmentation

|

Attributes |

Collaborative Robot Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Collaborative Robot Market Trends

“AI Integration and Human-Robot Collaboration for Enhanced Productivity”

- A prominent trend in the North America Collaborative Robot market is the integration of artificial intelligence (AI) and advanced sensor technologies, enabling more intuitive and safe human-robot collaboration. This development is reshaping factory floors by allowing cobots to perform complex tasks while adapting to human input in real-time.

- For example, in March 2024, Universal Robots launched a new AI-enabled cobot software enhancement designed to optimize pick-and-place operations using machine learning algorithms that adapt to variable object shapes and positions. This development enables greater efficiency and flexibility in industries such as electronics and packaging.

- The growing use of computer vision and AI allows cobots to perform tasks like defect detection, precision assembly, and dynamic path planning with greater autonomy and minimal human oversight. Companies such as ABB and FANUC are increasingly incorporating AI to enhance the contextual understanding of cobots and improve their responsiveness in unstructured environments.

- Voice-assisted operation and gesture-based control are also gaining momentum, contributing to safer and more interactive workspaces. For instance, in 2024, READY Robotics introduced Forge/OS updates that support voice-command-enabled robotic programming, making cobots even more accessible to non-technical users.

- The trend towards intelligent, adaptive, and user-friendly cobots is transforming collaborative robotics into indispensable tools across North American industries. Their deployment is expanding from automotive and heavy manufacturing into areas such as logistics, healthcare, food processing, and small-scale manufacturing.

Collaborative Robot Market Dynamics

Driver

“Rising Automation in SMEs and Industry 4.0 Adoption”

- The growing need for flexible, cost-effective automation solutions among small and medium-sized enterprises (SMEs), coupled with the broader push toward Industry 4.0, is a major driver of the collaborative robot market in North America.

- For instance, in January 2024, Canada-based Robotiq introduced a line of plug-and-play cobot grippers aimed at SMEs, allowing small manufacturers to automate assembly and pick-and-place operations with minimal integration effort.

- As traditional industrial robots often require complex programming and significant infrastructure, cobots offer a scalable, safe, and easily programmable alternative ideal for small operations. This is especially appealing in sectors such as metal fabrication, electronics, and consumer goods.

- Additionally, workforce shortages and the need to increase operational efficiency are prompting companies to adopt cobots for repetitive or ergonomically challenging tasks. According to a 2024 report by the Association for Advancing Automation (A3), cobot deployments in North America grew by 22% year-over-year, with strong uptake in logistics and healthcare.

- The simplicity, safety compliance, and return on investment offered by collaborative robots make them well-suited for businesses aiming to modernize production processes without overhauling existing systems.

Restraint/Challenge

“High Integration Costs and Technical Complexity in Multi-Process Environments”

- Despite their advantages, the adoption of collaborative robots is restrained by the high upfront costs of advanced hardware and the complexity involved in integrating cobots into multi-process workflows.

- For instance, while lightweight cobots are relatively affordable, the cost increases significantly when outfitted with advanced AI modules, high-resolution vision systems, and precision grippers. This can be a barrier for small companies without significant automation budgets.

- Technical challenges also arise when deploying cobots in environments where they must interact with multiple machines, sensors, and software systems. This requires robust interoperability standards and skilled labor, which are often lacking in SMEs.

- In a 2024 survey conducted by Deloitte, over 40% of manufacturers in North America cited system integration and programming complexity as major obstacles to cobot adoption.

- Moreover, safety concerns—especially in environments involving heavy or sharp objects—necessitate additional investment in sensors and compliance measures to meet regulatory standards.

- Addressing these issues through modular hardware, standardized software interfaces, and improved training resources will be essential for unlocking the full potential of collaborative robotics across the region.

Collaborative Robot Market Scope

The market is segmented on the basis of payload, component, application, and end-user.

- By Payload

On the basis of payload, the North America collaborative robot market is segmented into up to 5 kg, 5–10 kg, and above 10 kg. The up to 5 kg segment dominated the market with the largest revenue share of 42.7% in 2024, owing to its suitability for high-precision, low-payload tasks such as electronics assembly, quality inspection, and small parts handling. These cobots are favored by SMEs and industries with limited floor space due to their compact design and cost-effectiveness.

The 5–10 kg payload segment is expected to witness the fastest CAGR from 2025 to 2032, driven by increasing deployment in applications requiring higher strength without compromising on flexibility. These cobots are gaining traction in the automotive and metalworking sectors for tasks such as machine tending, light welding, and more robust material handling operations.

• By Component

On the basis of component, the market is segmented into hardware and software. The hardware segment held the largest market share in 2024, attributed to consistent demand for robotic arms, sensors, grippers, and control systems that form the physical foundation of collaborative robots. Hardware innovations, including lightweight materials and precision actuators, are enhancing cobot performance across sectors.

The software segment is expected to record the highest growth rate from 2025 to 2032, supported by advancements in AI, machine learning, and intuitive programming platforms. Solutions such as drag-and-drop programming, simulation tools, and real-time monitoring are enabling rapid cobot deployment and driving increased adoption, especially among non-technical users.

• By Application

On the basis of application, the market is segmented into material handling, assembly, pick & place, welding & soldering, quality testing, and others. The material handling segment led the market in 2024, driven by the widespread use of cobots for loading/unloading, palletizing, and packaging tasks in manufacturing and logistics. These applications significantly improve operational efficiency and reduce workplace injuries caused by repetitive lifting.

The pick & place segment is anticipated to register the highest CAGR from 2025 to 2032, fueled by strong demand in the electronics, food & beverage, and e-commerce sectors. Cobots equipped with advanced vision systems are being widely adopted for their speed, accuracy, and adaptability in high-throughput pick-and-place environments.

• By End-User

On the basis of end-user, the North America collaborative robot market is segmented into automotive, electronics & semiconductors, manufacturing, healthcare, logistics, and others. The automotive sector accounted for the largest revenue share in 2024, with cobots being deployed for repetitive tasks like welding, component assembly, and painting, helping automakers reduce production time and labor costs.

The healthcare sector is projected to experience the fastest growth from 2025 to 2032, driven by rising adoption of cobots for laboratory automation, pharmaceutical production, and surgical assistance. For instance, in 2024, several hospitals in the U.S. began piloting collaborative robots for handling sterile equipment and supporting diagnostic procedures, underscoring the growing role of robotics in clinical settings.

Collaborative Robot Market Regional Analysis

- North America dominates the collaborative robot (cobot) market with the largest revenue share of 38.5% in 2024, fueled by the region’s strong focus on industrial automation, labor efficiency, and technological advancements.

- The adoption of collaborative robots is driven by the need for flexible automation solutions that can work safely alongside human workers in diverse industries including automotive, electronics, and healthcare.

- A robust manufacturing base, favorable government support for automation, and a growing trend among small and medium-sized enterprises (SMEs) to implement cost-effective robotics have significantly bolstered market growth across the region.

U.S. Collaborative Robot Market Insight

The U.S. collaborative robot market held the largest revenue share of 70.0% in North America in 2024, owing to the rapid advancement of smart manufacturing initiatives and rising labor shortages in key industrial sectors. Major investments in cobot deployment across automotive assembly lines, electronics manufacturing, and medical device production are contributing to widespread adoption.

In March 2024, Universal Robots announced a strategic collaboration with Denali Advanced Integration to expand cobot deployment across American manufacturing plants, highlighting the growing demand for human-robot collaboration to improve productivity and safety. In addition, the U.S. is a hub for robotics R&D and software innovation, further driving the adoption of high-performance, AI-integrated cobots.

Canada Collaborative Robot Market Insight

Canada is expected to be the fastest-growing market for collaborative robots in North America during the forecast period, supported by growing automation in the manufacturing and logistics sectors. The country’s strategic focus on boosting industrial efficiency, coupled with incentives for digital transformation in SMEs, is fueling cobot adoption.

For example, in 2024, the Canadian government expanded its support for the Advanced Manufacturing Supercluster, encouraging businesses to integrate robotics and AI into their operations. This initiative has led to increased deployments of collaborative robots in areas such as warehouse automation, electronics assembly, and precision machining, positioning Canada as a rising hub for intelligent automation.

Collaborative Robot Market Share

The Collaborative Robot industry is primarily led by well-established companies, including:

- Universal Robots A/S (Denmark)

- FANUC Corporation (Japan)

- ABB Ltd. (Switzerland)

- KUKA AG (Germany)

- Doosan Robotics Inc. (South Korea)

- Yaskawa America, Inc. (Japan)

- Kawasaki Heavy Industries, Ltd. (Japan)

- Aubo Robotics USA, Inc. (U.S.)

- Techman Robot Inc. (Taiwan)

- Precise Automation, Inc. (U.S.)

Latest Developments in North America Collaborative Robot Market

- In April 2023, Universal Robots introduced the UR20 collaborative robot, designed for high payload operations with enhanced joint performance and faster cycle times. With over 30% improved reach compared to previous models and a 25% reduction in joint wear, this launch aimed to address heavier material handling and palletizing applications in automotive and logistics sectors

- In January 2023, ABB expanded its GoFa series with upgraded safety features and ease-of-programming modules. These new models experienced a 33% uptick in adoption in the electronics and assembly sectors within six months. The launch was targeted to simplify use cases for smaller manufacturers and reduce deployment time by 40%

- In September 2024, Rethink Robotics unveiled its Rethink Reacher (RE) line of collaborative robots at IMTS, marking its return to the market. The Reacher cobot line includes seven new models handling payloads ranging from 7 to 30 kg, featuring improved design, increased precision, speed, and durability, and supported by an IP65 rating for use in wet and dusty environments

- In March 2024, Schneider Electric released two new Lexium collaborative robots, the RL 3 and RL 12, with the RL 18 model set to be released later that year. The comprehensive Lexium line enables high-speed motion and control of up to 130 axes from one processor, helping manufacturers address production, flexibility, and sustainability challenges

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

North America Collaborative Robot Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its North America Collaborative Robot Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as North America Collaborative Robot Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.