North America Copper Market

Market Size in USD Billion

USD

44.04 Billion

USD

68.39 Billion

2025

2033

USD

44.04 Billion

USD

68.39 Billion

2025

2033

| 2026 - 2033 | |

| USD 44.04 Billion | |

| USD 68.39 Billion | |

| % | |

|

North America Copper Market Size

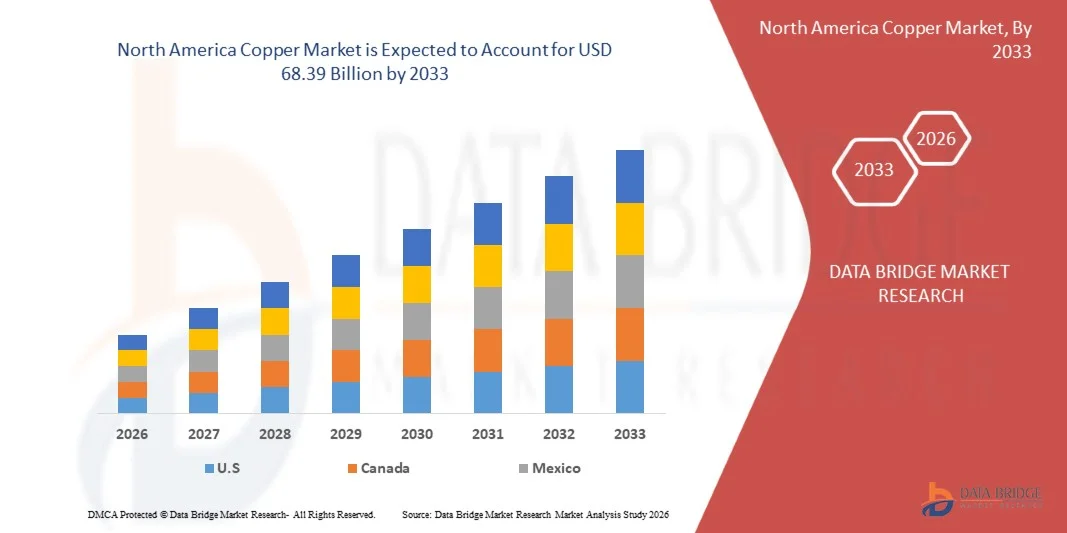

- The North America Copper Market size was valued at USD 44.04 billion in 2025 and is expected to reach USD 68.39 billion by 2033, at a CAGR of 5.8% during the forecast period

- Copper is a highly conductive, ductile, and corrosion-resistant base metal widely used for electrical, thermal, and industrial applications. It is available in various product forms including copper cathodes, rods (alambrón), bars, bus bars, strips, wires, tubes, and copper alloys such as brass and bronze. Its superior electrical conductivity, recyclability, and antimicrobial properties make it essential across power transmission, construction, transportation, electronics, and renewable energy industries.

- Manufacturing processes typically involve mining, concentration, smelting, electrorefining (for cathode production), followed by continuous casting, rolling, extrusion, and drawing to produce semi-finished and finished copper products. These processes ensure high purity levels (up to 99.99% for cathodes), excellent conductivity, and mechanical performance required for industrial and infrastructure applications.

North America Copper Market Analysis

- Copper is primarily produced through mining of sulfide and oxide ores, followed by flotation, smelting, converting, and electrorefining to produce high-purity cathodes. Downstream processing includes continuous casting and rolling to manufacture rods, strips, sheets, tubes, and specialty copper alloys for diversified industrial use

- The market is driven by accelerating electrification, rapid expansion of renewable energy installations such as solar and wind, grid modernization projects, and rising EV adoption. However, challenges include volatile copper prices, declining ore grades, supply chain disruptions, high energy costs in smelting operations, and environmental regulations surrounding mining activities

- Government initiatives promoting renewable energy targets, domestic critical mineral supply chain security, and infrastructure modernization are strengthening the North America copper production ecosystem. Significant opportunities exist in recycled copper utilization, green copper production technologies, expansion of copper usage in battery systems, and infrastructure growth across emerging economies such as India, Indonesia, Vietnam, and Brazil as industrialization accelerates

- In 2026, U.S. is expected to dominate as well as highest growing country in the North America Copper Market, supported by large-scale construction activities, strong electrical equipment manufacturing, rapid EV production, and extensive renewable energy capacity additions in countries such as China, Japan, and India. The region benefits from integrated supply chains, large smelting capacities, and strong downstream fabrication industries

- In 2025, the copper cathodes segment is dominate the North America Copper Market with an estimated market share of 31.33%, owing to its role as the primary refined form of copper used for manufacturing rods, wires, strips, and other downstream products. High purity levels, strong demand from electrical infrastructure, and growing consumption in renewable and EV applications reinforce its leading position within the overall North America Copper Market landscape

Report Scope and North America Copper Market Segmentation

|

Attributes |

copper Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

North America Copper Market Trends

“Accelerating Electrification and Renewable Energy Expansion Driving North America copper Demand”

- The rapid expansion of electrification initiatives worldwide is creating significant growth opportunities for the North America Copper Market. Increasing investments in renewable energy projects, electric vehicle (EV) infrastructure, grid modernization, and energy storage systems are substantially boosting copper consumption. Governments across major economies are implementing decarbonization targets, clean energy policies, and infrastructure stimulus programs, accelerating the transition toward electricity-driven transportation and power systems

- copper plays a critical role in EVs due to its superior electrical conductivity and thermal performance. Electric vehicles require significantly higher copper content compared to internal combustion engine vehicles, as copper is extensively used in motors, inverters, wiring harnesses, charging systems, and battery interconnections. The rapid scale-up of EV production in North America is therefore directly contributing to rising copper demand

- Additionally, copper is indispensable in renewable energy systems such as solar photovoltaic installations and wind turbines. It is widely used in generators, transformers, inverters, and power transmission cables, ensuring efficient electricity generation and distribution. Expansion of smart grids and high-voltage transmission networks further strengthens consumption of copper rods, strips, and bus bars

- Beyond energy and mobility, copper demand is increasing across construction, data centers, telecommunications infrastructure, and industrial automation. Urbanization and digitalization trends are driving the need for reliable wiring, connectivity systems, and advanced electrical equipment, where copper remains the preferred material due to its durability and conductivity advantages

- Therefore, as North America economies accelerate electrification, renewable capacity additions, and digital infrastructure development, copper is positioned as a foundational material of the energy transition, making electrification-led demand growth a defining long-term trend in the North America Copper Market.

North America Copper Market Dynamics

Driver

“Accelerating Electrification and Renewable Energy Deployment Worldwide”

- Rising North America electrification is a major driver of the North America Copper Market, particularly due to expanding renewable energy installations, electric vehicle (EV) adoption, and grid modernization projects.

- Governments and utilities are increasingly investing in solar, wind, hydro, and energy storage systems to meet decarbonization targets and rising electricity demand. copper plays a fundamental role in power generation, transmission, and distribution infrastructure because of its superior electrical conductivity and thermal efficiency.

- Electric vehicles require significantly higher copper content compared to conventional internal combustion engine vehicles, as copper is extensively used in electric motors, battery connections, inverters, wiring harnesses, and charging infrastructure. As EV production scales in North America, copper consumption per vehicle continues to increase, directly supporting market growth.

- In addition, expansion of smart grids, high-voltage transmission networks, and data centers is driving sustained demand for copper rods, bus bars, strips, and cables. Rapid urbanization and infrastructure development across emerging economies further amplify the need for reliable electrical wiring and connectivity solutions.

- As countries accelerate their transition toward low-carbon and electricity-driven economies, copper remains an essential material underpinning long-term energy and industrial transformation

Restraint/Challenge

“Environmental Concerns and Supply-Side Constraints in copper Mining and Processing”

- Environmental and regulatory pressures associated with copper mining and refining present key challenges to the North America Copper Market. copper extraction often involves large-scale open-pit mining, which can result in land degradation, water usage concerns, tailings management risks, and ecosystem disruption. Increasing scrutiny from regulators and local communities is raising compliance requirements and extending permitting timelines for new mining projects

- Additionally, declining ore grades in several major copper-producing regions are increasing operational costs and energy consumption, thereby raising the carbon footprint of mining and smelting activities.

- As governments implement stricter environmental standards and carbon reduction policies, producers face growing pressure to adopt cleaner technologies and improve sustainability practices

- Price volatility driven by supply-demand imbalances, geopolitical risks, and trade policies further adds uncertainty for manufacturers and downstream users. Infrastructure bottlenecks and limited new project development may constrain future supply growth.

- Collectively, environmental challenges, regulatory tightening, and supply-side limitations could increase production costs and pose risks to stable long-term market expansion.

North America Copper Market Scope

The market is segmented on the basis of product form, temper, copper grade, application, and end-use.

• By Product Form

On the basis of product form, the market is segmented into copper Cathodes, copper Strips (>0.15mm and <0.15mm) (specifically Alambrón, >6mm), copper Bars & Shapes, copper Bus Bars, copper Strips (>0.15mm and <0.15mm), copper Alloys.

The copper Cathodes segment is expected to dominated the largest market revenue share of 33.40% in 2026, driven by its exceptional high-temperature oxidation resistance and mechanical stability, making it indispensable for critical applications in gas turbines, nuclear reactors, and petrochemical processing, where materials face extreme thermal cycling and corrosive environments.

The copper Rods (specifically Alambrón, >6mm segment is anticipated to witness the fastest CAGR of 6.0% from 2026 to 2033, fueled by escalating demand for superior corrosion resistance in harsh acidic environments, particularly within chemical processing plants, offshore oil & gas extraction, and flue gas desulfurization systems, where Hastelloy-type alloys excel against pitting and stress-corrosion cracking.

• By Temper

On the basis of temper, the market is segmented into soft, half-hard, hard-spring and extra-spring.

The Soft segment is expected to held the largest market revenue share of 46.52% in 2026, driven by its versatility in forging critical components like turbine shafts, valve stems, and fasteners that demand uniform strength and machinability in high-stress aerospace, power generation, and marine propulsion systems.

The Soft segment is expected to witness the fastest CAGR of 6.1% from 2026 to 2033, driven by surging infrastructure investments in oil & gas pipelines, power plant cooling systems, and chemical transport networks that require seamless, corrosion-resistant conduits capable of withstanding high-pressure, acidic, and high-temperature conditions.

• By copper Grade

On the basis of copper grade, the market is segmented into pure coppers, oxygen free coppers, electrolytic coppers, free-machining coppers.

The Pure coppers segment is expected to dominated the market with a revenue share of 43.44% in 2026, fueled by escalating demand across oil & gas, chemical processing, and marine sectors where exposure to aggressive acids, seawater, and high-chloride environments necessitates materials like Hastelloy and Inconel to prevent pitting, crevice corrosion, and stress cracking.

The Pure coppers segment in the North America Copper Market is projected to register the fastest CAGR of 6.1% from 2026 to 2033, driven by expanding applications in medical devices such as stents and orthopedic implants, aerospace actuators for adaptive structures, and automotive sensors that exploit super elasticity and two-way shape recovery under stress or temperature changes. Rising demand for high-performance, corrosion-resistant, and durable materials in advanced electronics, precision engineering, and other high-tech industries is further accelerating the adoption of nickel-based shape-memory alloys.

• By Application

On the basis of application, the market is segmented into electrical wiring, power transmission lines, cables and busbars, heat exchangers, electric vehicles, motor parts, industrial machinery, plumbing, roofing, solar panels, pipes, architectural applications, refrigeration tubing, high conductivity copper Cathodes, electrodes, cooking utensils, water-cooled copper crucibles, spark plugs, optical fibers and others.

The Electrical Wiring segment is expected to dominated the market with a revenue share of 15.49% in 2026, driven by surging demand for high-performance coppers in gas turbines, nuclear reactors, and renewable infrastructure like wind turbine gearboxes and solar thermal components that require exceptional heat resistance, creep strength, and fatigue endurance under continuous high-temperature operation.

The Electric Vehicles segment in the North America Copper Market is anticipated to witness the fastest CAGR of 10.2% from 2026 to 2033, driven by growing applications in medical devices such as stents and orthopedic implants, aerospace actuators for adaptive structures, and automotive sensors that utilize super elasticity and two-way shape recovery under stress or temperature variations. Increasing demand for high-performance, corrosion-resistant, and durable materials in advanced electronic and precision engineering applications is further accelerating the adoption of coppers in these sectors.•

• By End-Use

On the basis of end-use, the market is segmented into construction, electricals and electronics, power and energy, automotive, consumer products, telecommunications, medical, aerospace and defense, others.

The Construction segment is expected to dominated the market with a revenue share of 33.53% in 2026, driven by surging demand for high-performance coppers in gas turbines, nuclear reactors, and renewable infrastructure like wind turbine gearboxes and solar thermal components that require exceptional heat resistance, creep strength, and fatigue endurance under continuous high-temperature operation.

The Automotive segment in the North America Copper Market is anticipated to witness the fastest CAGR of 7.4% from 2026 to 2033, driven by growing applications in medical devices such as stents and orthopedic implants, aerospace actuators for adaptive structures, and automotive sensors that utilize super elasticity and two-way shape recovery under stress or temperature variations. Increasing demand for high-performance, corrosion-resistant, and durable materials in advanced electronic and precision engineering applications is further accelerating the adoption of coppers in these sectors

North America Copper Market Regional Analysis

U.S. North America Copper Market Insight

U.S. is one of the fastest-growing market, with a projected CAGR of approximately 6.0% during 2026–2033. Growth is supported by strong investments in infrastructure modernization, renewable energy expansion, EV manufacturing, and data center development. High demand for copper in power transmission cables, charging infrastructure, and advanced electronics—alongside domestic mining and refining capabilities—continues to strengthen the U.S. market position.

Canada North America Copper Market Insight

Canada is expected to witness steady growth in the North American North America Copper Market, with a projected CAGR of 5.5% during 2026–2033. Growth is driven by investments in clean energy projects, mining expansion, and electrification initiatives. Rising demand for copper in power grids, industrial equipment, and EV charging infrastructure supports market expansion, alongside Canada’s role as an important copper resource producer.

Mexico North America Copper Market Insight

Mexico is one of the moderately-growing markets in North America, with a projected CAGR of approximately 4.9% during 2026–2033. Growth is fueled by rapid urbanization, large-scale renewable energy capacity additions, strong EV production, and expansion of construction and manufacturing sectors. China’s extensive smelting and refining capacity, combined with government support for electrification and infrastructure development, continues to accelerate copper consumption.

North America Copper Market Share

The North America Copper Market is primarily led by well-established companies, including:

- Jiangxi copper Corporation (China)

- BHP (Australia)

- Codelco (Chile)

- Glencore (Switzerland)

- Anglo American (U.K.)

- Mitsubishi Materials Corporation (Japan)

- Grupo México (Mexico)

- First Quantum Minerals Ltd (Canada)

- Freeport-McMoRan (U.S.)

- Aurubis AG (Germany)

- KGHM (Poland)

- Chinalco (China)

- Teck Resources Limited (Canada)

- Antofagasta plc (U.K.)

- Rio Tinto (U.K.)

- Sumitomo Metal Mining Co., Ltd. (Japan)

- Norilsk Nickel (Russia)

- Siemens (Germany)

- thyssenkrupp Materials NA, Inc. (U.S.)

- Southwire Company, LLC (U.S.)

- Poongsan Corporation (South Korea)

Latest Developments in the Europe North America Copper Market

- In March 2025, Jiangxi copper Corporation Limited (JCL) completed the equity acquisition of Dingshengxin Mining, with AnJie Broad Law Firm providing full legal support. The deal strengthened JCL’s industrial chain layout and boosted its resource integration capabilities. By applying advanced technologies and management expertise, JCL aimed to improve the production efficiency and resource utilization of the Zhugongtang Lead-Zinc Mine. The acquisition positioned JCL for stronger operational performance and expanded growth opportunities.

- In April 2025, Aurubis AG ramped up its new copper recycling smelter in the U.S., after investing USD 800 million over four years. The facility was set to process 180,000 metric tons of complex copper scrap annually. It aimed to produce 70,000 tons of refined copper each year. The project marked Aurubis' expansion into the U.S. recycling market. This move boosted its North America footprint and supported long-term metal supply security.

- In March 2025, Codelco reclaimed its position as the world’s top copper producer, reporting 2024 output of 1.44 million tonnes, slightly surpassing BHP’s 1.43 million. The Chilean state miner is advancing ore-rich projects, exploring Saudi investment, and adopting I-Pulse’s electric rock-shattering tech. Codelco and BHP are both modernizing aging Chilean operations amid declining ore grades.

- In April 2025, Glencore’s DRC operations, Kamoto copper Company and Mutanda Mining, received The copper Mark after completing a rigorous assurance process. The certification confirmed their alignment with 33 ESG criteria under the new RRA 3.0 standard. Independent third-party assessments included interviews with over 200 workers and stakeholders. These were the first African mines certified under the updated standard. The recognition strengthened Glencore’s reputation in responsible mining and supported investor confidence and market access.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 MULTIVARIATE MODELING

2.7 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.8 DBMR MARKET POSITION GRID

2.9 MARKET APPLICATION COVERAGE GRID

2.1 DBMR VENDOR SHARE ANALYSIS

2.11 SECONDARY SOURCES

2.12 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PESTLE ANALYSIS

4.2 PORTERS FIVE FORCES

4.3 PRODUCTION CONSUMPTION ANALYSIS

4.4 IMPORT-EXPORT SCENARIO

4.5 TECHNOLOGICAL ADVANCEMENT BY MANUFACTURERS

4.6 VENDOR SELECTION CRITERIA

4.7 COMPETITOR KEY PRICING ANALYSIS

4.8 DIVE INTO DISTRIBUTORS AND OEMS TO UNDERSTAND PONTENTIAL OR EXISTING CUSTOMERS NEEDS TO UNDERSTAND PONTENTIAL OR EXISTING CUSTOMERS NEEDS & SUPPLY CHAIN ANALYSIS

4.8.1 LOGISTICS COST SCENARIO

4.8.2 IMPORTANCE OF LOGISTICS SERVICE PROVIDERS

4.9 CLIMATE CHANGE SCENARIO

4.9.1 ENVIRONMENTAL CONCERNS

4.9.2 INDUSTRY RESPONSE

4.9.3 GOVERNMENT’S ROLE

4.1 BUYERS INSIGHTS, BY APPLICATION

4.11 PRODUCTION CAPACITY FOR TOP COMPANIES

4.12 IMPORT-EXPORT SCENARIO

4.13 TARIFFS & IMPACT ON THE MARKET

4.13.1 CURRENT COPPER TARIFF RATE (S) IN TOP-5 FIVE MAJOR MARKETS

4.13.2 OUTLOOK: LOCAL PRODUCTION V/S IMPORT RELIANCE

4.13.3 VENDOR SELECTION CRITERIA DYNAMICS

4.13.4 IMPACT ON SUPPLY CHAIN

4.13.4.1 RAW MATERIAL PROCUREMENT

4.13.4.2 MANUFACTURING AND PRODUCTION

4.13.5 IMPACT ON PRICES

4.13.6 REGULATORY INCLINATION

4.13.6.1 GEOPOLITICAL SITUATION

4.14 RAW MATERIAL COVERAGE

4.15 MAIN COMPETITORS

4.15.1 JIANGXI COPPER CORPORATION

4.15.2 SWOT ANALYSIS

4.15.3 SWOT ANALYSIS

4.15.4 SWOT ANALYSIS

4.16 COPPER SUBSTITUTES: RELEVANCE AND ADOPTION BY INDUSTRY–NORTH AMERICA COPPER MARKET

4.16.1 INTRODUCTION

4.16.2 POWER TRANSMISSION AND DISTRIBUTION INDUSTRY

4.16.3 TELECOMMUNICATIONS AND DATA INFRASTRUCTURE

4.16.4 AUTOMOTIVE INDUSTRY

4.16.5 CONSTRUCTION AND PLUMBING INDUSTRY

4.16.6 ELECTRONICS AND ELECTRICAL EQUIPMENT MANUFACTURING

4.16.7 RENEWABLE ENERGY AND ENERGY STORAGE

4.16.8 INDUSTRIAL MACHINERY AND MANUFACTURING EQUIPMENT

4.16.9 CONCLUSION

4.17 GROWTH OPPORTUNITIES AND RESTRAINS

4.17.1 ASIA-PACIFIC

4.17.1.1 CHINA

4.17.1.1.1 OPPORTUNITY -. INFRASTRUCTURE & CLEAN ENERGY TRANSITION

4.17.1.1.2 RESTRAINT -. SLOWING GROWTH & PRICE SENSITIVITY

4.17.1.2 INDIA

4.17.1.2.1 OPPORTUNITY -. RAPID GROWTH ACROSS INFRASTRUCTURE & EV TRANSITION

4.17.1.2.2 RESTRAINT -. IMPORT DEPENDENCE & SUPPLY GAPS

4.17.1.3 JAPAN

4.17.1.3.1 OPPORTUNITY - STABLE HIGH-VALUE INDUSTRIAL DEMAND

4.17.1.3.2 RESTRAINT - MATURE MARKET WITH LIMITED EXPANSION

4.17.1.4 SOUTH KOREA

4.17.1.4.1 OPPORTUNITY - ELECTRONICS & SEMICONDUCTOR FABRICATION

4.17.1.4.2 RESTRAINT - EXPORT CYCLE SENSITIVITY & INPUT COSTS

4.17.1.5 INDONESIA

4.17.1.5.1 OPPORTUNITY - INDUSTRIALIZATION & URBAN ELECTRIFICATION

4.17.1.5.2 RESTRAINT - LIMITED LOCAL REFINING & PROCESSING CAPACITY

4.17.1.6 THAILAND

4.17.1.6.1 OPPORTUNITY - ELECTRONICS & AUTOMOTIVE COMPONENTS

4.17.1.6.2 RESTRAINT - PRICE SENSITIVITY & DEPENDENCY ON IMPORTS

4.17.1.7 AUSTRALIA

4.17.1.7.1 OPPORTUNITY - STRATEGIC RAW MATERIAL SUPPLY

4.17.1.7.2 RESTRAINT - LIMITED DOMESTIC VALUE-ADDED MANUFACTURING

4.17.2 NORTH AMERICA

4.17.2.1 U.S.

4.17.2.1.1 OPPORTUNITY - INFRASTRUCTURE MODERNIZATION & ELECTRIFICATION

4.17.2.1.2 RESTRAINT - IMPORT DEPENDENCE & TRADE POLICY UNCERTAINTY

4.17.2.2 CANADA

4.17.2.2.1 OPPORTUNITY - MINING BASE & CLEAN ENERGY TRANSITION

4.17.2.2.2 RESTRAINT - EXPORT AND VALUE-ADDED LIMITATIONS

4.17.2.3 MEXICO

4.17.2.3.1 OPPORTUNITY - AUTOMOTIVE ELECTRIFICATION & MANUFACTURING INTEGRATION

4.17.2.3.2 RESTRAINT - SUPPLY CHAIN & PROCESSING CHALLENGES

4.17.3 EUROPE

4.17.3.1 GERMANY

4.17.3.1.1 OPPORTUNITY - INDUSTRIAL & ENERGY TRANSITION DEMAND

4.17.3.1.2 RESTRAINT - HIGH COSTS & COMPETITIVE PRESSURES

4.17.3.2 U.K.

4.17.3.2.1 OPPORTUNITY - GRID MODERNIZATION & RENEWABLES

4.17.3.2.2 RESTRAINT - IMPORT DEPENDENCE & COST VOLATILITY

4.17.3.3 FRANCE

4.17.3.3.1 OPPORTUNITY - TRANSPORT ELECTRIFICATION & ENERGY PROJECTS

4.17.3.3.2 RESTRAINT - REGULATORY COSTS & MODEST VOLUMES

4.17.3.4 ITALY

4.17.3.4.1 OPPORTUNITY - RENEWABLES & BUILDING RETROFIT DEMAND

4.17.3.4.2 RESTRAINT - IMPORT RELIANCE & COMPETITION

4.17.3.5 SPAIN

4.17.3.5.1 OPPORTUNITY - SOLAR & RAIL ELECTRIFICATION

4.17.3.5.2 RESTRAINT - MACRO AND COST PRESSURES

4.17.3.6 RUSSIA

4.17.3.6.1 OPPORTUNITY - ENERGY & INDUSTRIAL BASE

4.17.3.6.2 RESTRAINT - GEOPOLITICAL RISKS & SANCTIONS

4.17.3.7 SWEDEN

4.17.3.7.1 OPPORTUNITY - HIGH PER CAPITA COPPER USE & TECH DEMAND

4.17.3.7.2 RESTRAINT - MARKET SIZE LIMITS VOLUME GROWTH

4.17.3.8 SWITZERLAND

4.17.3.8.1 OPPORTUNITY - PRECISION ENGINEERING & HIGH‑VALUE METALS

4.17.3.8.2 RESTRAINT - NO UPSTREAM CAPACITY

4.17.3.9 DENMARK

4.17.3.9.1 OPPORTUNITY - WIND ENERGY & GRID MODERNIZATION

4.17.3.9.2 RESTRAINT - SMALL MARKET SCALE

4.17.3.10 NETHERLANDS

4.17.3.10.1 OPPORTUNITY - LOGISTICS & DISTRIBUTION HUB

4.17.3.10.2 RESTRAINT - IMPORT DEPENDENCE

4.17.3.11 BELGIUM

4.17.3.11.1 OPPORTUNITY - PORT NETWORK & TRANSIT DEMAND

4.17.3.11.2 RESTRAINT - LIMITED DOMESTIC VALUE‑ADDED

4.17.3.12 TURKEY

4.17.3.12.1 OPPORTUNITY - INFRASTRUCTURE & INDUSTRIAL GROWTH

4.17.3.12.2 RESTRAINT - EXCHANGE RATE & IMPORT COSTS

4.17.3.13 NORWAY

4.17.3.13.1 OPPORTUNITY - RENEWABLES & ENERGY SYSTEMS

4.17.3.13.2 RESTRAINT - LIMITED DOMESTIC MARKET

4.17.3.14 FINLAND

4.17.3.14.1 OPPORTUNITY - EXPORT & ENERGY MODERNIZATION

4.17.3.14.2 RESTRAINT - MODEST MARKET EXPANSION

4.17.4 MIDDLE EAST & AFRICA

4.17.4.1 SAUDI ARABIA

4.17.4.1.1 OPPORTUNITY – INFRASTRUCTURE & ENERGY TRANSITION

4.17.4.1.2 RESTRAINT – IMPORT DEPENDENCY & PRICE VOLATILITY

4.17.4.2 UAE

4.17.4.2.1 OPPORTUNITY – TRADE HUB & INDUSTRIAL ELECTRIFICATION

4.17.4.2.2 RESTRAINT – RELIANCE ON IMPORTS & MARKET SIZE LIMITATIONS

4.17.4.3 SOUTH AFRICA

4.17.4.3.1 OPPORTUNITY – MINING & INDUSTRIAL BASE

4.17.4.3.2 RESTRAINT – ENERGY COSTS & SUPPLY DISRUPTIONS

4.17.4.4 EGYPT

4.17.4.4.1 OPPORTUNITY – INFRASTRUCTURE MODERNIZATION & POWER DISTRIBUTION

4.17.4.4.2 RESTRAINT – IMPORT DEPENDENCE & LIMITED LOCAL REFINING

4.17.4.5 ISRAEL

4.17.4.5.1 OPPORTUNITY – HIGH-TECH & DATA CENTERS

4.17.4.5.2 RESTRAINT – SMALL MARKET SIZE & IMPORT DEPENDENCY

4.17.4.6 QATAR

4.17.4.6.1 OPPORTUNITY – INFRASTRUCTURE & ENERGY PROJECTS

4.17.4.6.2 RESTRAINT – HIGH IMPORT DEPENDENCE

4.17.4.7 KUWAIT

4.17.4.7.1 OPPORTUNITY – URBAN INFRASTRUCTURE & POWER DISTRIBUTION

4.17.4.7.2 RESTRAINT – LIMITED DOMESTIC REFINING

4.17.4.8 OMAN

4.17.4.8.1 OPPORTUNITY – INDUSTRIAL & ENERGY SECTORS

4.17.4.8.2 RESTRAINT – LIMITED LOCAL PRODUCTION

4.17.4.9 BAHRAIN

4.17.4.9.1 OPPORTUNITY – CONSTRUCTION & ENERGY PROJECTS

4.17.4.9.2 RESTRAINT – HIGH IMPORT DEPENDENCE

4.17.5 SOUTH AMERICA

4.17.5.1 BRAZIL

4.17.5.1.1 OPPORTUNITY – DIVERSIFIED INDUSTRIAL BASE & IMPORTED DEMAND

4.17.5.1.2 RESTRAINT – RELIANCE ON IMPORTED REFINED COPPER

4.17.5.2 ARGENTINA

4.17.5.2.1 OPPORTUNITY – EMERGING MINING PROJECTS & EXPORT POTENTIAL

4.17.5.2.2 RESTRAINT – REGULATORY & ENVIRONMENTAL CONCERNS

4.17.5.3 COLOMBIA

4.17.5.4 OPPORTUNITY – INFRASTRUCTURE & ELECTRIFICATION PUSH

4.17.5.4.1 RESTRAINT – LIMITED DOMESTIC PRODUCTION

4.17.5.5 CHILE

4.17.5.5.1 OPPORTUNITY – NORTH AMERICA LEADERSHIP IN COPPER PRODUCTION

4.17.5.5.2 RESTRAINT – PERMITTING & INFRASTRUCTURE BOTTLENECKS

4.17.5.6 PERU

4.17.5.6.1 OPPORTUNITY – LARGE SCALE MINING INVESTMENTS

4.17.5.6.2 RESTRAINT – SOCIAL & ENVIRONMENTAL CHALLENGES

4.18 KEY INDUSTRIES AND FUTURE TRENDS

4.18.1 KEY INDUSTRIES DRIVING COPPER DEMAND

4.18.1.1 ENERGY TRANSITION & CLEAN POWER INFRASTRUCTURE

4.18.1.2 ELECTRIC VEHICLES (EVS) & TRANSPORT ELECTRIFICATION

4.18.1.3 CONSTRUCTION & URBAN INFRASTRUCTURE

4.18.1.4 ELECTRICALS, ELECTRONICS & DIGITAL HARDWARE

4.18.1.5 INDUSTRIAL & MANUFACTURING MACHINERY

4.18.1.6 CONSUMER GOODS, TELECOMMUNICATIONS & OTHERS

4.18.1.7 CONSUMER GOODS, TELECOMMUNICATIONS & OTHERS

4.18.2 FUTURE MARKET TRENDS:

4.18.2.1 LONG-TERM DEMAND GROWTH LINKED TO ELECTRIFICATION

4.18.2.2 SUPPLY CONSTRAINTS & STRUCTURAL DEFICITS

4.18.2.3 PRICE DYNAMICS & MARKET SENSITIVITIES

4.18.2.4 CIRCULAR ECONOMY & RECYCLING

4.18.2.5 SUBSTITUTION RISKS & MATERIAL INNOVATION

4.18.2.6 GEOPOLITICAL AND STRATEGIC FORCES

4.18.2.7 TECHNOLOGY & DIGITALIZATION TRENDS

4.19 NEW APPLICATIONS OF COPPER

4.19.1 ELECTRIC VEHICLES (EVS) AND HYBRID SYSTEMS:

4.19.1.1 RENEWABLE ENERGY & GRID TECHNOLOGIES

4.19.1.2 DATA CENTERS, AI, AND DIGITAL INFRASTRUCTURE

4.19.1.3 AEROSPACE AND DEFENCE

4.19.1.4 ADDITIVE MANUFACTURING (3D PRINTING)

4.19.1.5 INTERNET OF THINGS (IOT) AND SMART DEVICES

4.19.1.6 THERMAL MANAGEMENT & ADVANCED ELECTRONICS

4.2 PRODUCT DEMAND AND FUTURE DEMAND BY INDUSTRY

4.21 MOST PROFITABLE SEGMENTS AND END-USED BY COUNTRY/REGION

4.22 SUSTAINABILITY TRENDS (RECYCLING, GREEN ENERGY, ETC)

4.22.1 NORTH AMERICA

4.22.1.1 RECYCLING & CIRCULAR ECONOMY:

4.22.1.2 GREEN ENERGY ADOPTION

4.22.2 EUROPE

4.22.2.1 RECYCLING & CIRCULAR ECONOMY

4.22.2.2 GREEN ENERGY DEPLOYMENT:

4.22.3 ASIA PACIFIC

4.22.3.1 RECYCLING & CIRCULAR ECONOMY

4.22.3.2 GREEN ENERGY DEPLOYMENT

4.22.4 MIDDLE EAST & AFRICA

4.22.4.1 RECYCLING & CIRCULAR ECONOMY

4.22.4.2 GREEN ENERGY DEPLOYMENT:

4.22.5 SOUTH AMERICA

4.22.5.1 RECYCLING & CIRCULAR ECONOMY

4.22.5.2 GREEN ENERGY DEPLOYMENT

4.22.6 CONCLUSION

5 TARIFFS & IMPACT– NORTH AMERICA COPPER MARKET

5.1 CURRENT TARIFF RATE(S) IN TOP-5 COUNTRY MARKETS

5.2 OUTLOOK: LOCAL PRODUCTION V/S IMPORT RELIANCE

5.3 VENDOR SELECTION CRITERIA DYNAMICS

5.4 IMPACT ON SUPPLY CHAIN

5.4.1 RAW MATERIAL PROCUREMENT

5.4.2 MANUFACTURING AND PRODUCTION

5.4.3 LOGISTICS AND DISTRIBUTION

5.4.4 PRICE PITCHING AND POSITION OF MARKET

5.5 INDUSTRY PARTICIPANTS: PROACTIVE MOVES

5.5.1 SUPPLY CHAIN OPTIMIZATION

5.5.2 JOINT VENTURE ESTABLISHMENTS

5.6 IMPACT ON PRICES

5.7 REGULATORY INCLINATION

5.7.1 GEOPOLITICAL SITUATION

5.7.2 TRADE PARTNERSHIPS BETWEEN THE COUNTRIES

5.7.2.1 FREE TRADE AGREEMENTS

5.7.2.2 ALLIANCE ESTABLISHMENTS

5.7.3 STATUS ACCREDITATION (INCLUDING MFN)

5.7.4 11.7.4 DOMESTIC COURSE OF CORRECTION

5.7.4.1 INCENTIVE SCHEMES TO BOOST PRODUCTION OUTPUTS

5.8 PRICE INDEX

6 IMPACT OF TECHNOLOGY INNOVATIONS ON COPPER DEMAND

6.1 NORTH AMERICA

6.2 EUROPE

6.3 ASIA-PACIFIC

6.4 MIDDLE EAST & AFRICA

6.5 SOUTH AMERICA

7 REGULATION COVERAGE – NORTH AMERICA COPPER MARKET

7.1 INTRODUCTION

7.2 ADVANCED ORE PROCESSING AND BENEFICIATION TECHNOLOGIES

7.3 HYDROMETALLURGICAL INNOVATIONS AND LOW-EMISSION EXTRACTION

7.4 SMELTING AND REFINING PROCESS OPTIMIZATION

7.5 RECYCLING-DRIVEN MANUFACTURING AND SECONDARY COPPER PROCESSING

7.6 DIGITALIZATION AND AUTOMATION IN PROCESSING OPERATIONS

7.7 PRECISION MANUFACTURING AND APPLICATION-SPECIFIC COPPER PRODUCTS

7.8 REGIONAL ANALYSIS OF INNOVATIONS IN COPPER PROCESSING AND MANUFACTURING

8 MARKET OVERVIEW

8.1 DRIVERS

8.1.1 SURGE IN NORTH AMERICA RENEWABLE ENERGY PROJECTS INCREASING COPPER CONSUMPTION

8.1.2 RISING INTEGRATION OF COPPER IN EMERGING RENEWABLE INDUSTRIES

8.1.3 RAPID ADOPTION OF ELECTRIC VEHICLES (EVS) BOOSTING DEMAND FOR COPPER-INTENSIVE COMPONENTS

8.1.4 PROLIFERATION OF CONSUMER ELECTRONICS AND DATA CENTERS INCREASING COPPER DEMAND

8.2 RESTRAINTS

8.2.1 VOLATILITY IN COPPER PRICES HAMPERS LONG-TERM INVESTMENT PLANNING

8.2.2 ENVIRONMENTAL CONCERNS AND REGULATORY RESTRICTIONS DELAY MINING OPERATIONS

8.3 OPPORTUNITIES

8.3.1 EXPANSION OF 5G INFRASTRUCTURE FUELS DEMAND FOR HIGH-CONDUCTIVITY COPPER IN TELECOMMUNICATIONS INDUSTRIES

8.3.2 STRATEGIC PARTNERSHIPS BETWEEN MINING FIRMS AND TECH COMPANIES ENSURE SUSTAINABLE COPPER SOURCING

8.3.3 INNOVATIONS IN COPPER ALLOYS ENHANCE PERFORMANCE IN AEROSPACE AND DEFENSE APPLICATIONS

8.3.4 RISING INVESTMENTS IN INFRASTRUCTURE AND SMART GRID DEVELOPMENT ACROSS EMERGING ECONOMIES

8.4 CHALLENGES

8.4.1 LABOR SHORTAGES AND SKILL GAPS IN MINING SECTORS HINDER OPERATIONAL PRODUCTIVITY

8.4.2 GEOPOLITICAL INSTABILITY IN COPPER-PRODUCING NATIONS DISRUPTS SUPPLY CHAIN RELIABILITY

9 NORTH AMERICA COPPER MARKET, BY PRODUCT FORM

9.1 OVERVIEW

9.2 NORTH AMERICA COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

9.2.1 COPPER CATHODES

9.2.2 COPPER RODS (SPECIFICALLY ALAMBRÓN, >6MM

9.2.3 COPPER BARS & SHAPES

9.2.4 COPPER BUS BARS

9.2.5 COPPER STRIPS (>0.15MM AND <0.15MM)

9.2.6 COPPER ALLOYS

9.3 NORTH AMERICA COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

9.3.1 COPPER CATHODES

9.3.2 COPPER RODS (SPECIFICALLY ALAMBRÓN, >6MM

9.3.3 COPPER BARS & SHAPES

9.3.4 COPPER BUS BARS

9.3.5 COPPER STRIPS (>0.15MM AND <0.15MM)

9.3.6 COPPER ALLOYS

9.4 NORTH AMERICA COPPER CATHODES IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

9.4.1 ASIA-PACIFIC

9.4.2 NORTH AMERICA

9.4.3 EUROPE

9.4.4 SOUTH AMERICA

9.4.5 MIDDLE EAST AND AFRICA

9.5 NORTH AMERICA COPPER RODS (SPECIFICALLY ALAMBRÓN, >6MM IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

9.5.1 ASIA-PACIFIC

9.5.2 NORTH AMERICA

9.5.3 EUROPE

9.5.4 SOUTH AMERICA

9.5.5 MIDDLE EAST AND AFRICA

9.6 NORTH AMERICA COPPER BARS & SHAPES IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

9.6.1 ASIA-PACIFIC

9.6.2 NORTH AMERICA

9.6.3 EUROPE

9.6.4 SOUTH AMERICA

9.6.5 MIDDLE EAST AND AFRICA

9.7 NORTH AMERICA COPPER BUS BARS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

9.7.1 ASIA-PACIFIC

9.7.2 NORTH AMERICA

9.7.3 EUROPE

9.7.4 SOUTH AMERICA

9.7.5 MIDDLE EAST AND AFRICA

9.8 NORTH AMERICA COPPER STRIPS (>0.15MM AND <0.15MM) IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

9.8.1 ASIA-PACIFIC

9.8.2 NORTH AMERICA

9.8.3 EUROPE

9.8.4 SOUTH AMERICA

9.8.5 MIDDLE EAST AND AFRICA

9.9 NORTH AMERICA COPPER ALLOYS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

9.9.1 ASIA-PACIFIC

9.9.2 NORTH AMERICA

9.9.3 EUROPE

9.9.4 SOUTH AMERICA

9.9.5 MIDDLE EAST AND AFRICA

10 NORTH AMERICA COPPER MARKET, BY TEMPER

10.1 OVERVIEW

10.2 NORTH AMERICA COPPER MARKET, BY TEMPER, 2018-2033 (USD MILLION)

10.2.1 SOFT

10.2.2 HALF-HARD

10.2.3 HARD-SPRING

10.2.4 EXTRA-SPRING

10.3 NORTH AMERICA COPPER MARKET, BY TEMPER, 2018-2033 (THOUSAND TONS)

10.3.1 SOFT

10.3.2 HALF-HARD

10.3.3 HARD-SPRING

10.3.4 EXTRA-SPRING

10.4 NORTH AMERICA SOFT IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

10.4.1 ASIA-PACIFIC

10.4.2 NORTH AMERICA

10.4.3 EUROPE

10.4.4 SOUTH AMERICA

10.4.5 MIDDLE EAST AND AFRICA

10.5 NORTH AMERICA HALF-HARD IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

10.5.1 ASIA-PACIFIC

10.5.2 NORTH AMERICA

10.5.3 EUROPE

10.5.4 SOUTH AMERICA

10.5.5 MIDDLE EAST AND AFRICA

10.6 NORTH AMERICA HARD-SPRING IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

10.6.1 ASIA-PACIFIC

10.6.2 NORTH AMERICA

10.6.3 EUROPE

10.6.4 SOUTH AMERICA

10.6.5 MIDDLE EAST AND AFRICA

10.7 NORTH AMERICA EXTRA-SPRING IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

10.7.1 ASIA-PACIFIC

10.7.2 NORTH AMERICA

10.7.3 EUROPE

10.7.4 SOUTH AMERICA

10.7.5 MIDDLE EAST AND AFRICA

11 NORTH AMERICA COPPER MARKET, BY COPPER GRADE

11.1 OVERVIEW

11.2 NORTH AMERICA COPPER MARKET, BY COPPRER GRADE, 2018-2033 (USD MILLION)

11.2.1 PURE COPPERS

11.2.2 OXYGEN FREE COPPERS

11.2.3 ELECTROLYTIC COPPERS

11.2.4 FREE-MACHINING COPPERS

11.3 NORTH AMERICA COPPER MARKET, BY COPPRER GRADE, 2018-2033 (THOUSAND TONS)

11.3.1 PURE COPPERS

11.3.2 OXYGEN FREE COPPERS

11.3.3 ELECTROLYTIC COPPERS

11.3.4 FREE-MACHINING COPPERS

11.4 NORTH AMERICA PURE COPPERS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

11.4.1 ASIA-PACIFIC

11.4.2 NORTH AMERICA

11.4.3 EUROPE

11.4.4 SOUTH AMERICA

11.4.5 MIDDLE EAST AND AFRICA

11.5 NORTH AMERICA OXYGEN FREE COPPERS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

11.5.1 ASIA-PACIFIC

11.5.2 NORTH AMERICA

11.5.3 EUROPE

11.5.4 SOUTH AMERICA

11.5.5 MIDDLE EAST AND AFRICA

11.6 NORTH AMERICA ELECTROLYTIC COPPERS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

11.6.1 ASIA-PACIFIC

11.6.2 NORTH AMERICA

11.6.3 EUROPE

11.6.4 SOUTH AMERICA

11.6.5 MIDDLE EAST AND AFRICA

11.7 NORTH AMERICA FREE-MACHINING COPPERS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

11.7.1 ASIA-PACIFIC

11.7.2 NORTH AMERICA

11.7.3 EUROPE

11.7.4 SOUTH AMERICA

11.7.5 MIDDLE EAST AND AFRICA

12 NORTH AMERICA COPPER MARKET, BY APPLICATION

12.1 OVERVIEW

12.2 NORTH AMERICA COPPER MARKET, BY APPLICATION, 2018-2033 (USD MILLION)

12.2.1 ELECTRICAL WIRING

12.2.2 POWER TRANSMISSION LINES

12.2.3 CABLES AND BUSBARS

12.2.4 HEAT EXCHANGERS

12.2.5 ELECTRIC VEHICLES

12.2.6 MOTOR PARTS

12.2.7 INDUSTRIAL MACHINERY

12.2.8 PLUMBING

12.2.9 ROOFING

12.2.10 SOLAR PANELS

12.2.11 PIPES

12.2.12 ARCHITECTURAL APPLICATIONS

12.2.13 REFRIGERATION TUBING

12.2.14 HIGH CONDUCTIVITY WIRES

12.2.15 ELECTRODES

12.2.16 COOKING UTENSILS

12.2.17 WATER-COOLED COPPER CRUCIBLES

12.2.18 SPARK PLUGS

12.2.19 OPTICAL FIBERS

12.2.20 OTHERS

12.3 NORTH AMERICA COPPER MARKET, BY APPLICATION, 2018-2033 (THOUSAND TONS)

12.3.1 ELECTRICAL WIRING

12.3.2 POWER TRANSMISSION LINES

12.3.3 CABLES AND BUSBARS

12.3.4 HEAT EXCHANGERS

12.3.5 ELECTRIC VEHICLES

12.3.6 MOTOR PARTS

12.3.7 INDUSTRIAL MACHINERY

12.3.8 PLUMBING

12.3.9 ROOFING

12.3.10 SOLAR PANELS

12.3.11 PIPES

12.3.12 ARCHITECTURAL REGIONS

12.3.13 REFRIGERATION TUBING

12.3.14 HIGH CONDUCTIVITY WIRES

12.3.15 ELECTRODES

12.3.16 COOKING UTENSILS

12.3.17 WATER-COOLED COPPER CRUCIBLES

12.3.18 SPARK PLUGS

12.3.19 OPTICAL FIBERS

12.3.20 OTHERS

12.4 NORTH AMERICA ELECTRICAL WIRING IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

12.4.1 ASIA-PACIFIC

12.4.2 NORTH AMERICA

12.4.3 EUROPE

12.4.4 SOUTH AMERICA

12.4.5 MIDDLE EAST AND AFRICA

12.5 NORTH AMERICA POWER TRANSMISSION LINES IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

12.5.1 ASIA-PACIFIC

12.5.2 NORTH AMERICA

12.5.3 EUROPE

12.5.4 SOUTH AMERICA

12.5.5 MIDDLE EAST AND AFRICA

12.6 NORTH AMERICA CABLES AND BUSBARS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

12.6.1 ASIA-PACIFIC

12.6.2 NORTH AMERICA

12.6.3 EUROPE

12.6.4 SOUTH AMERICA

12.6.5 MIDDLE EAST AND AFRICA

12.7 NORTH AMERICA HEAT EXCHANGERS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

12.7.1 ASIA-PACIFIC

12.7.2 NORTH AMERICA

12.7.3 EUROPE

12.7.4 SOUTH AMERICA

12.7.5 MIDDLE EAST AND AFRICA

12.8 NORTH AMERICA ELECTRIC VEHICLES IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

12.8.1 ASIA-PACIFIC

12.8.2 NORTH AMERICA

12.8.3 EUROPE

12.8.4 SOUTH AMERICA

12.8.5 MIDDLE EAST AND AFRICA

12.9 NORTH AMERICA MOTOR PARTS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

12.9.1 ASIA-PACIFIC

12.9.2 NORTH AMERICA

12.9.3 EUROPE

12.9.4 SOUTH AMERICA

12.9.5 MIDDLE EAST AND AFRICA

12.1 NORTH AMERICA INDUSTRIAL MACHINERY IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

12.10.1 ASIA-PACIFIC

12.10.2 NORTH AMERICA

12.10.3 EUROPE

12.10.4 SOUTH AMERICA

12.10.5 MIDDLE EAST AND AFRICA

12.11 NORTH AMERICA PLUMBING IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

12.11.1 ASIA-PACIFIC

12.11.2 NORTH AMERICA

12.11.3 EUROPE

12.11.4 SOUTH AMERICA

12.11.5 MIDDLE EAST AND AFRICA

12.12 NORTH AMERICA ROOFING IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

12.12.1 ASIA-PACIFIC

12.12.2 NORTH AMERICA

12.12.3 EUROPE

12.12.4 SOUTH AMERICA

12.12.5 MIDDLE EAST AND AFRICA

12.13 NORTH AMERICA SOLAR PANELS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

12.13.1 ASIA-PACIFIC

12.13.2 NORTH AMERICA

12.13.3 EUROPE

12.13.4 SOUTH AMERICA

12.13.5 MIDDLE EAST AND AFRICA

12.14 NORTH AMERICA PIPES IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

12.14.1 ASIA-PACIFIC

12.14.2 NORTH AMERICA

12.14.3 EUROPE

12.14.4 SOUTH AMERICA

12.14.5 MIDDLE EAST AND AFRICA

12.15 NORTH AMERICA ARCHITECTURAL REGIONS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

12.15.1 ASIA-PACIFIC

12.15.2 NORTH AMERICA

12.15.3 EUROPE

12.15.4 SOUTH AMERICA

12.15.5 MIDDLE EAST AND AFRICA

12.16 NORTH AMERICA REFRIGERATION TUBING IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

12.16.1 ASIA-PACIFIC

12.16.2 NORTH AMERICA

12.16.3 EUROPE

12.16.4 SOUTH AMERICA

12.16.5 MIDDLE EAST AND AFRICA

12.17 NORTH AMERICA HIGH CONDUCTIVITY WIRES IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

12.17.1 ASIA-PACIFIC

12.17.2 NORTH AMERICA

12.17.3 EUROPE

12.17.4 SOUTH AMERICA

12.17.5 MIDDLE EAST AND AFRICA

12.18 NORTH AMERICA ELECTRODES IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

12.18.1 ASIA-PACIFIC

12.18.2 NORTH AMERICA

12.18.3 EUROPE

12.18.4 SOUTH AMERICA

12.18.5 MIDDLE EAST AND AFRICA

12.19 NORTH AMERICA COOKING UTENSILS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

12.19.1 ASIA-PACIFIC

12.19.2 NORTH AMERICA

12.19.3 EUROPE

12.19.4 SOUTH AMERICA

12.19.5 MIDDLE EAST AND AFRICA

12.2 NORTH AMERICA WATER-COOLED COPPER CRUCIBLES IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

12.20.1 ASIA-PACIFIC

12.20.2 NORTH AMERICA

12.20.3 EUROPE

12.20.4 SOUTH AMERICA

12.20.5 MIDDLE EAST AND AFRICA

12.21 NORTH AMERICA SPARK PLUGS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

12.21.1 ASIA-PACIFIC

12.21.2 NORTH AMERICA

12.21.3 EUROPE

12.21.4 SOUTH AMERICA

12.21.5 MIDDLE EAST AND AFRICA

12.22 NORTH AMERICA OPTICAL FIBERS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

12.22.1 ASIA-PACIFIC

12.22.2 NORTH AMERICA

12.22.3 EUROPE

12.22.4 SOUTH AMERICA

12.22.5 MIDDLE EAST AND AFRICA

12.23 NORTH AMERICA OTHERS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

12.23.1 ASIA-PACIFIC

12.23.2 NORTH AMERICA

12.23.3 EUROPE

12.23.4 SOUTH AMERICA

12.23.5 MIDDLE EAST AND AFRICA

13 NORTH AMERICA COPPER MARKET, BY END-USE

13.1 OVERVIEW

13.2 NORTH AMERICA COPPER MARKET, BY END-USE, 2018-2033 (USD MILLION)

13.2.1 CONSTRUCTION

13.2.2 ELECTRICALS AND ELECTRONICS

13.2.3 POWER AND ENERGY

13.2.4 AUTOMOTIVE

13.2.5 CONSUMER PRODUCTS

13.2.6 TELECOMMUNICATIONS

13.2.7 MEDICAL

13.2.8 AEROSPACE AND DEFENCE

13.2.9 OTHERS

13.3 NORTH AMERICA COPPER MARKET, BY END-USE, 2018-2033 (THOUSAND TONS)

13.3.1 CONSTRUCTION

13.3.2 ELECTRICALS AND ELECTRONICS

13.3.3 POWER AND ENERGY

13.3.4 AUTOMOTIVE

13.3.5 CONSUMER PRODUCTS

13.3.6 TELECOMMUNICATIONS

13.3.7 MEDICAL

13.3.8 AEROSPACE AND DEFENCE

13.3.9 OTHERS

13.4 NORTH AMERICA CONSTRUCTION IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

13.4.1 ASIA-PACIFIC

13.4.2 NORTH AMERICA

13.4.3 EUROPE

13.4.4 SOUTH AMERICA

13.4.5 MIDDLE EAST AND AFRICA

13.5 NORTH AMERICA ELECTRICALS AND ELECTRONICS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

13.5.1 ASIA-PACIFIC

13.5.2 NORTH AMERICA

13.5.3 EUROPE

13.5.4 SOUTH AMERICA

13.5.5 MIDDLE EAST AND AFRICA

13.6 NORTH AMERICA POWER AND ENERGY IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

13.6.1 ASIA-PACIFIC

13.6.2 NORTH AMERICA

13.6.3 EUROPE

13.6.4 SOUTH AMERICA

13.6.5 MIDDLE EAST AND AFRICA

13.7 NORTH AMERICA AUTOMOTIVE IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

13.7.1 ASIA-PACIFIC

13.7.2 NORTH AMERICA

13.7.3 EUROPE

13.7.4 SOUTH AMERICA

13.7.5 MIDDLE EAST AND AFRICA

13.8 NORTH AMERICA CONSUMER PRODUCTS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

13.8.1 ASIA-PACIFIC

13.8.2 NORTH AMERICA

13.8.3 EUROPE

13.8.4 SOUTH AMERICA

13.8.5 MIDDLE EAST AND AFRICA

13.9 NORTH AMERICA TELECOMMUNICATIONS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

13.9.1 ASIA-PACIFIC

13.9.2 NORTH AMERICA

13.9.3 EUROPE

13.9.4 SOUTH AMERICA

13.9.5 MIDDLE EAST AND AFRICA

13.1 NORTH AMERICA MEDICAL IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

13.10.1 ASIA-PACIFIC

13.10.2 NORTH AMERICA

13.10.3 EUROPE

13.10.4 SOUTH AMERICA

13.10.5 MIDDLE EAST AND AFRICA

13.11 NORTH AMERICA AEROSPACE AND DEFENCE IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

13.11.1 ASIA-PACIFIC

13.11.2 NORTH AMERICA

13.11.3 EUROPE

13.11.4 SOUTH AMERICA

13.11.5 MIDDLE EAST AND AFRICA

13.12 NORTH AMERICA OTHERS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

13.12.1 ASIA-PACIFIC

13.12.2 NORTH AMERICA

13.12.3 EUROPE

13.12.4 SOUTH AMERICA

13.12.5 MIDDLE EAST AND AFRICA

13.13 NORTH AMERICA CONSTRUCTION IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

13.13.1 COPPER CATHODES

13.13.2 COPPER BARS & SHAPES

13.13.3 COPPER RODS (SPECIFICALLY ALAMBRÓN, >6MM

13.13.4 COPPER BUS BARS

13.13.5 COPPER STRIPS (>0.15MM AND <0.15MM)

13.13.6 COPPER ALLOYS

13.14 NORTH AMERICA CONSTRUCTION IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

13.14.1 COPPER CATHODES

13.14.2 COPPER BARS & SHAPES

13.14.3 COPPER RODS (SPECIFICALLY ALAMBRÓN, >6MM

13.14.4 COPPER BUS BARS

13.14.5 COPPER STRIPS (>0.15MM AND <0.15MM)

13.14.6 COPPER ALLOYS

13.15 NORTH AMERICA ELECTRICALS AND ELECTRONICS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

13.15.1 COPPER CATHODES

13.15.2 COPPER RODS (SPECIFICALLY ALAMBRÓN, >6MM

13.15.3 COPPER BUS BARS

13.15.4 COPPER BARS & SHAPES

13.15.5 COPPER STRIPS (>0.15MM AND <0.15MM)

13.15.6 COPPER ALLOYS

13.16 NORTH AMERICA ELECTRICALS AND ELECTRONICS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

13.16.1 COPPER CATHODES

13.16.2 COPPER RODS (SPECIFICALLY ALAMBRÓN, >6MM

13.16.3 COPPER BUS BARS

13.16.4 COPPER BARS & SHAPES

13.16.5 COPPER STRIPS (>0.15MM AND <0.15MM)

13.16.6 COPPER ALLOYS

13.17 NORTH AMERICA POWER AND ENERGY IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

13.17.1 COPPER CATHODES

13.17.2 COPPER BUS BARS

13.17.3 COPPER RODS (SPECIFICALLY ALAMBRÓN, >6MM

13.17.4 COPPER BARS & SHAPES

13.17.5 COPPER STRIPS (>0.15MM AND <0.15MM)

13.17.6 COPPER ALLOYS

13.18 NORTH AMERICA POWER AND ENERGY IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

13.18.1 COPPER CATHODES

13.18.2 COPPER BUS BARS

13.18.3 COPPER RODS (SPECIFICALLY ALAMBRÓN, >6MM

13.18.4 COPPER BARS & SHAPES

13.18.5 COPPER STRIPS (>0.15MM AND <0.15MM)

13.18.6 COPPER ALLOYS

13.19 NORTH AMERICA AUTOMOTIVE IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

13.19.1 COPPER RODS (SPECIFICALLY ALAMBRÓN, >6MM

13.19.2 COPPER CATHODES

13.19.3 COPPER BUS BARS

13.19.4 COPPER STRIPS (>0.15MM AND <0.15MM)

13.19.5 COPPER BARS & SHAPES

13.19.6 COPPER ALLOYS

13.2 NORTH AMERICA AUTOMOTIVE IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

13.20.1 COPPER RODS (SPECIFICALLY ALAMBRÓN, >6MM

13.20.2 COPPER CATHODES

13.20.3 COPPER BUS BARS

13.20.4 COPPER STRIPS (>0.15MM AND <0.15MM)

13.20.5 COPPER BARS & SHAPES

13.20.6 COPPER ALLOYS

13.21 NORTH AMERICA CONSUMER PRODUCTS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

13.21.1 COPPER CATHODES

13.21.2 COPPER STRIPS (>0.15MM AND <0.15MM)

13.21.3 COPPER RODS (SPECIFICALLY ALAMBRÓN, >6MM

13.21.4 COPPER ALLOYS

13.21.5 COPPER BARS & SHAPES

13.21.6 COPPER BUS BARS

13.22 NORTH AMERICA CONSUMER PRODUCTS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

13.22.1 COPPER CATHODES

13.22.2 COPPER STRIPS (>0.15MM AND <0.15MM)

13.22.3 COPPER RODS (SPECIFICALLY ALAMBRÓN, >6MM

13.22.4 COPPER ALLOYS

13.22.5 COPPER BARS & SHAPES

13.22.6 COPPER BUS BARS

13.23 NORTH AMERICA TELECOMMUNICATIONS PRODUCTS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

13.23.1 COPPER STRIPS (>0.15MM AND <0.15MM)

13.23.2 COPPER CATHODES

13.23.3 COPPER RODS (SPECIFICALLY ALAMBRÓN, >6MM

13.23.4 COPPER BUS BARS

13.23.5 COPPER BARS & SHAPES

13.23.6 COPPER ALLOYS

13.24 NORTH AMERICA TELECOMMUNICATIONS PRODUCTS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

13.24.1 COPPER STRIPS (>0.15MM AND <0.15MM)

13.24.2 COPPER CATHODES

13.24.3 COPPER RODS (SPECIFICALLY ALAMBRÓN, >6MM

13.24.4 COPPER BUS BARS

13.24.5 COPPER BARS & SHAPES

13.24.6 COPPER ALLOYS

13.25 NORTH AMERICA MEDICAL IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

13.25.1 COPPER CATHODES

13.25.2 COPPER ALLOYS

13.25.3 COPPER STRIPS (>0.15MM AND <0.15MM)

13.25.4 COPPER RODS (SPECIFICALLY ALAMBRÓN, >6MM

13.25.5 COPPER BARS & SHAPES

13.25.6 COPPER BUS BARS

13.26 NORTH AMERICA MEDICAL IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

13.26.1 COPPER CATHODES

13.26.2 COPPER ALLOYS

13.26.3 COPPER STRIPS (>0.15MM AND <0.15MM)

13.26.4 COPPER RODS (SPECIFICALLY ALAMBRÓN, >6MM

13.26.5 COPPER BARS & SHAPES

13.26.6 COPPER BUS BARS

13.27 NORTH AMERICA AEROSPACE AND DEFENCE IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

13.27.1 COPPER ALLOYS

13.27.2 COPPER CATHODES

13.27.3 COPPER STRIPS (>0.15MM AND <0.15MM)

13.27.4 COPPER RODS (SPECIFICALLY ALAMBRÓN, >6MM

13.27.5 COPPER BARS & SHAPES

13.27.6 COPPER BUS BARS

13.28 NORTH AMERICA AEROSPACE AND DEFENCE IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

13.28.1 COPPER ALLOYS

13.28.2 COPPER CATHODES

13.28.3 COPPER STRIPS (>0.15MM AND <0.15MM)

13.28.4 COPPER RODS (SPECIFICALLY ALAMBRÓN, >6MM

13.28.5 COPPER BARS & SHAPES

13.28.6 COPPER BUS BARS

13.29 NORTH AMERICA OTHERS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

13.29.1 COPPER ALLOYS

13.29.2 COPPER CATHODES

13.29.3 COPPER STRIPS (>0.15MM AND <0.15MM)

13.29.4 COPPER RODS (SPECIFICALLY ALAMBRÓN, >6MM

13.29.5 COPPER BARS & SHAPES

13.29.6 COPPER BUS BARS

13.3 NORTH AMERICA OTHERS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

13.30.1 COPPER ALLOYS

13.30.2 COPPER CATHODES

13.30.3 COPPER STRIPS (>0.15MM AND <0.15MM)

13.30.4 COPPER RODS (SPECIFICALLY ALAMBRÓN, >6MM

13.30.5 COPPER BARS & SHAPES

13.30.6 COPPER BUS BARS

14 NORTH AMERICA COPPER MARKET, BY REGION

14.1 NORTH AMERICA

14.1.1 U.S.

14.1.2 CANADA

14.1.3 MEXICO

15 NORTH AMERICA COPPER MARKET, COMPANY LANDSCAPE

15.1 COMPANY SHARE ANALYSIS: GLOBAL

16 SWOT ANALYSIS

17 COMPANY PROFILES (MANUFACTURERS)

17.1 JIANGXI COPPER GROUP CO., LTD.

17.1.1 COMPANY SNAPSHOT

17.1.2 REVENUE ANALYSIS

17.1.3 COMPANY SHARE ANALYSIS

17.1.4 PRODUCT PORTFOLIO

17.1.5 RECENT DEVELOPMENT

17.2 AURUBIS AG

17.2.1 COMPANY SNAPSHOT

17.2.2 REVENUE ANALYSIS

17.2.3 COMPANY SHARE ANALYSIS

17.2.4 PRODUCT PORTFOLIO

17.2.5 RECENT DEVELOPMENTS/NEWS

17.3 CODELCO

17.3.1 COMPANY SNAPSHOT

17.3.2 COMPANY SHARE ANALYSIS

17.3.3 PRODUCT PORTFOLIO

17.3.4 RECENT DEVELOPMENT

17.4 GLENCORE

17.4.1 COMPANY SNAPSHOT

17.4.2 REVENUE ANALYSIS

17.4.3 COMPANY SHARE ANALYSIS

17.4.4 PRODUCT PORTFOLIO

17.4.5 RECENT DEVELOPMENTS/NEWS

17.5 BHP

17.5.1 COMPANY SNAPSHOT

17.5.2 REVENUE ANALYSIS

17.5.3 COMPANY SHARE ANALYSIS

17.5.4 PRODUCT PORTFOLIO

17.5.5 RECENT DEVELOPMENT

17.6 ALUMINIUM CORP

17.6.1 COMPANY SNAPSHOT

17.6.2 PRODUCT PORTFOLIO

17.6.3 RECENT DEVELOPMENTS/NEWS

17.7 ANGLO AMERICAN PLC

17.7.1 COMPANY SNAPSHOT

17.7.2 REVENUE ANALYSIS

17.7.3 PRODUCT PORTFOLIO

17.7.4 RECENT DEVELOPMENT/NEWS

17.8 ANTOFAGASTA PLC

17.8.1 COMPANY SNAPSHOT

17.8.2 REVENUE ANALYSIS

17.8.3 PRODUCT PORTFOLIO

17.8.4 RECENT DEVELOPMENT

17.9 AVIVA METALS

17.9.1 COMPANY SNAPSHOT

17.9.2 PRODUCT PORTFOLIO

17.9.3 RECENT DEVELOPMENT

17.1 CECIL

17.10.1 COMPANY SNAPSHOT

17.10.2 PRODUCT PORTFOLIO

17.10.3 RECENT DEVELOPMENTS/NEWS

17.11 CUNEXT GROUP INDUSTRIES

17.11.1 COMPANY SNAPSHOT

17.11.2 PRODUCT PORTFOLIO

17.11.3 RECENT DEVELOPMENTS/NEWS

17.12 FIRST QUANTUM MINERALS LTD.

17.12.1 COMPANY SNAPSHOT

17.12.2 REVENUE ANALYSIS

17.12.3 PRODUCT PORTFOLIO

17.12.4 RECENT DEVELOPMENT/NEWS

17.13 FREEPORT-MCMORAN

17.13.1 COMPANY SNAPSHOT

17.13.2 REVENUE ANALYSIS

17.13.3 PRODUCT PORTFOLIO

17.13.4 RECENT DEVELOPMENTS/NEWS

17.14 GINDRE

17.14.1 COMPANY SNAPSHOT

17.14.2 PRODUCT PORTFOLIO

17.14.3 RECENT DEVELOPMENT

17.15 GOLDEN DRAGON PRECISE COPPER TUBE INC,

17.15.1 COMPANY SNAPSHOT

17.15.2 PRODUCT PORTFOLIO

17.15.3 RECENT DEVELOPMENTS

17.16 GRUPO MÉXICO

17.16.1 COMPANY SNAPSHOT

17.16.2 REVENUE ANALYSIS

17.16.3 PRODUCT PORTFOLIO

17.16.4 RECENT DEVELOPMENT

17.17 HUSSEY COPPER

17.17.1 COMPANY SNAPSHOT

17.17.2 PRODUCT PORTFOLIO

17.17.3 RECENT DEVELOPMENTS/NEWS

17.18 IMC

17.18.1 COMPANY SNAPSHOT

17.18.2 PRODUCT PORTFOLIO

17.18.3 RECENT DEVELOPMENTS/NEWS

17.19 IUSA WIRE, INC

17.19.1 COMPANY SNAPSHOT

17.19.2 PRODUCT PORTFOLIO

17.19.3 RECENT DEVELOPMENTS/NEWS

17.2 JX ADVANCED METALS CORPORATION (SUBSIDIARY OF ENEOS HOLDINGS)

17.20.1 COMPANY SNAPSHOT

17.20.2 REVENUE ANALYSIS

17.20.3 PRODUCT PORTFOLIO

17.20.4 RECENT DEVELOPMENT

17.21 KGHM

17.21.1 COMPANY SNAPSHOT

17.21.2 REVENUE ANALYSIS

17.21.3 PRODUCT PORTFOLIO

17.21.4 RECENT DEVELOPMENT

17.22 KME GERMANY GMBH

17.22.1 COMPANY SNAPSHOT

17.22.2 PRODUCT PORTFOLIO

17.22.3 RECENT DEVELOPMENT

17.23 LUVATA

17.23.1 COMPANY SNAPSHOT

17.23.2 PRODUCT PORTFOLIO

17.23.3 RECENT DEVELOPMENT

17.24 MITSUBISHI MATERIALS CORPORATION

17.24.1 COMPANY SNAPSHOT

17.24.2 REVENUE ANALYSIS

17.24.3 PRODUCT PORTFOLIO

17.24.4 RECENT DEVELOPMENT/NEWS

17.25 MITSUI MINING & SMELTING CO.,LTD

17.25.1 COMPANY SNAPSHOT

17.25.2 REVENUE ANALYSIS

17.25.3 PRODUCT PORTFOLIO

17.25.4 RECENT DEVELOPMENT

17.26 NACOBRE USA

17.26.1 COMPANY SNAPSHOT

17.26.2 PRODUCT PORTFOLIO

17.26.3 RECENT DEVELOPMENTS/NEWS

17.27 NORILSK NICKEL

17.27.1 COMPANY SNAPSHOT

17.27.2 REVENUE ANALYSIS

17.27.3 PRODUCT PORTFOLIO

17.27.4 RECENT DEVELOPMENTS/NEWS

17.28 ORIENTAL COPPER CO., LTD.

17.28.1 COMPANY SNAPSHOT

17.28.2 PRODUCT PORTFOLIO

17.28.3 RECENT DEVELOPMENTS/NEWS

17.29 PARANAPANEMA INSTITUCIONAL

17.29.1 COMPANY SNAPSHOT

17.29.2 REVENUE ANALYSIS

17.29.3 PRODUCT PORTFOLIO

17.29.4 RECENT DEVELOPMENT

17.3 POONGSAN CORPORATION

17.30.1 COMPANY SNAPSHOT

17.30.2 REVENUE ANALYSIS

17.30.3 PRODUCT PORTFOLIO

17.30.4 RECENT DEVELOPMENT

17.31 REVERE COPPER PRODUCTS INC.

17.31.1 COMPANY SNAPSHOT

17.31.2 PRODUCT PORTFOLIO

17.31.3 RECENT DEVELOPMENTS/NEWS

17.32 RIO TINTO

17.32.1 COMPANY SNAPSHOT

17.32.2 REVENUE ANALYSIS

17.32.3 PRODUCT PORTFOLIO

17.32.4 RECENT DEVELOPMENTS/NEWS

17.33 SAM DONG CO, LTD.

17.33.1 COMPANY SNAPSHOT

17.33.2 PRODUCT PORTFOLIO

17.33.3 RECENT DEVELOPMENTS/NEWS

17.34 SARKUYSAN BILGI SISTEMLERI

17.34.1 COMPANY SNAPSHOT

17.34.2 REVENUE ANALYSIS

17.34.3 PRODUCT PORTFOLIO

17.34.4 RECENT DEVELOPMENTS/NEWS

17.35 SOFIA MED

17.35.1 COMPANY SNAPSHOT

17.35.2 PRODUCT PORTFOLIO

17.35.3 RECENT DEVELOPMENT/NEWS

17.36 SOUTHWIRE COMPANY, LLC

17.36.1 COMPANY SNAPSHOT

17.36.2 PRODUCT PORTFOLIO

17.36.3 RECENT DEVELOPMENT

17.37 SUMITOMO METAL MINING CO., LTD.

17.37.1 COMPANY SNAPSHOT

17.37.2 REVENUE ANALYSIS

17.37.3 PRODUCT PORTFOLIO

17.37.4 RECENT DEVELOPMENTS/NEWS

17.38 TECK RESOURCES LIMITED

17.38.1 COMPANY SNAPSHOT

17.38.2 REVENUE ANALYSIS

17.38.3 PRODUCT PORTFOLIO

17.38.4 RECENT DEVELOPMENTS/NEWS

17.39 TECNOFIL

17.39.1 COMPANY SNAPSHOT

17.39.2 PRODUCT PORTFOLIO

17.39.3 RECENT DEVELOPMENTS/NEWS

17.4 TERMOMECANICA - SÃO PAULO S.A.

17.40.1 COMPANY SNAPSHOT

17.40.2 PRODUCT PORTFOLIO

17.40.3 RECENT DEVELOPMENTS/NEWS

17.41 THYSSENKRUPP MATERIALS NA, INC.

17.41.1 COMPANY SNAPSHOT

17.41.2 PRODUCT PORTFOLIO

17.41.3 RECENT DEVELOPMENTS

17.42 UNIVERTICAL

17.42.1 COMPANY SNAPSHOT

17.42.2 PRODUCT PORTFOLIO

17.42.3 RECENT DEVELOPMENTS/NEWS

17.43 VALE

17.43.1 COMPANY SNAPSHOT

17.43.2 REVENUE ANALYSIS

17.43.3 PRODUCT PORTFOLIO

17.43.4 RECENT DEVELOPMENTS/NEWS

17.44 WIELAND

17.44.1 COMPANY SNAPSHOT

17.44.2 PRODUCT PORTFOLIO

17.44.3 RECENT DEVELOPMENT

18 COMPANY PROFILES (OEMS)

18.1 ABB

18.1.1 COMPANY SNAPSHOT

18.1.2 REVENUE ANALYSIS

18.1.3 PRODUCT PORTFOLIO

18.1.4 RECENT DEVELOPMENT

18.2 EATON

18.2.1 COMPANY SNAPSHOT

18.2.2 REVENUE ANALYSIS

18.2.3 PRODUCT PORTFOLIO

18.2.4 RECENT DEVELOPMENT/NEWS

18.3 SCHNEIDER ELECTRIC

18.3.1 COMPANY SNAPSHOT

18.3.2 REVENUE ANALYSIS

18.3.3 PRODUCT PORTFOLIO

18.3.4 RECENT DEVELOPMENT/NEWS

18.4 SIEMENS

18.4.1 COMPANY SNAPSHOT

18.4.2 REVENUE ANALYSIS

18.4.3 PRODUCT PORTFOLIO

18.4.4 RECENT DEVELOPMENTS

19 QUESTIONNAIRE

20 RELATED REPORTS

List of Table

TABLE 1 PRODUCTION CAPACITY FOR TOP COMPANIES

TABLE 2 U.S. COPPER DEMAND, PRODUCTION, AND IMPORTS

TABLE 3 COMPANY WISE MARKET ANALYSIS

TABLE 4 COMPANY WISE REVENUE BY PRODUCT

TABLE 5 INDUSTRY-WISE ADOPTION LOGIC OF COPPER SUBSTITUTES AND APPLICATION CONSTRAINTS

TABLE 6 INDUSTRY WISE COPPER PRODUCT USAGE AND PROJECT DEMAND

TABLE 7 MOST PROFITABLE COPPER PRODUCT SEGMENT AND KEY END-USE INDUSTRIES BY REION/COUNTRY

TABLE 8 HEAT MAP ANALYSIS OF COPPER CONCENTRATES TARIFF INTENSITY ACROSS MAJOR MARKETS

TABLE 9 TARIFF DIFFERENTIATION ACROSS COPPER PRODUCT CATEGORIES

TABLE 10 NORTH AMERICA COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 11 NORTH AMERICA COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 12 NORTH AMERICA COPPER CATHODES IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 13 NORTH AMERICA COPPER RODS (SPECIFICALLY ALAMBRÓN, >6MM IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 14 NORTH AMERICA COPPER BARS & SHAPES IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 15 NORTH AMERICA COPPER BUS BARS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 16 NORTH AMERICA COPPER STRIPS (>0.15MM AND <0.15MM) IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 17 NORTH AMERICA COPPER ALLOYS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 18 NORTH AMERICA COPPER MARKET, BY TEMPER, 2018-2033 (USD MILLION)

TABLE 19 NORTH AMERICA COPPER MARKET, BY TEMPER, 2018-2033 (THOUSAND TONS)

TABLE 20 NORTH AMERICA SOFT IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 21 NORTH AMERICA HALF-HARD IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 22 NORTH AMERICA HARD-SPRING IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 23 NORTH AMERICA EXTRA-SPRING IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 24 NORTH AMERICA COPPER MARKET, BY COPPRER GRADE, 2018-2033 (USD MILLION)

TABLE 25 NORTH AMERICA COPPER MARKET, BY COPPRER GRADE, 2018-2033 (THOUSAND TONS)

TABLE 26 NORTH AMERICA PURE COPPERS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 27 NORTH AMERICA OXYGEN FREE COPPERS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 28 NORTH AMERICA ELECTROLYTIC COPPERS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 29 NORTH AMERICA FREE-MACHINING COPPERS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 30 NORTH AMERICA COPPER MARKET, BY APPLICATION, 2018-2033 (USD MILLION)

TABLE 31 NORTH AMERICA COPPER MARKET, BY APPLICATION, 2018-2033 (THOUSAND TONS)

TABLE 32 NORTH AMERICA ELECTRICAL WIRING IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 33 NORTH AMERICA POWER TRANSMISSION LINES IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 34 NORTH AMERICA CABLES AND BUSBARS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 35 NORTH AMERICA HEAT EXCHANGERS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 36 NORTH AMERICA ELECTRIC VEHICLES IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 37 NORTH AMERICA MOTOR PARTS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 38 NORTH AMERICA INDUSTRIAL MACHINERY IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 39 NORTH AMERICA PLUMBING IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 40 NORTH AMERICA ROOFING IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 41 NORTH AMERICA SOLAR PANELS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 42 NORTH AMERICA PIPES IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 43 NORTH AMERICA ARCHITECTURAL REGIONS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 44 NORTH AMERICA REFRIGERATION TUBING IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 45 NORTH AMERICA HIGH CONDUCTIVITY WIRES IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 46 NORTH AMERICA ELECTRODES IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 47 NORTH AMERICA COOKING UTENSILS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 48 NORTH AMERICA WATER-COOLED COPPER CRUCIBLES IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 49 NORTH AMERICA SPARK PLUGS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 50 NORTH AMERICA OPTICAL FIBERS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 51 NORTH AMERICA OTHERS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 52 NORTH AMERICA COPPER MARKET, BY END-USE, 2018-2033 (USD MILLION)

TABLE 53 NORTH AMERICA COPPER MARKET, BY END-USE, 2018-2033 (THOUSAND TONS)

TABLE 54 NORTH AMERICA CONSTRUCTION IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 55 NORTH AMERICA ELECTRICALS AND ELECTRONICS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 56 NORTH AMERICA POWER AND ENERGY IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 57 NORTH AMERICA AUTOMOTIVE IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 58 NORTH AMERICA CONSUMER PRODUCTS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 59 NORTH AMERICA TELECOMMUNICATIONS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 60 NORTH AMERICA MEDICAL IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 61 NORTH AMERICA AEROSPACE AND DEFENCE IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 62 NORTH AMERICA OTHERS IN COPPER MARKET, BY REGION, 2018-2033 (USD MILLION)

TABLE 63 NORTH AMERICA CONSTRUCTION IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 64 NORTH AMERICA CONSTRUCTION IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 65 NORTH AMERICA ELECTRICALS AND ELECTRONICS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 66 NORTH AMERICA ELECTRICALS AND ELECTRONICS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 67 NORTH AMERICA POWER AND ENERGY IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 68 NORTH AMERICA POWER AND ENERGY IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 69 NORTH AMERICA AUTOMOTIVE IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 70 NORTH AMERICA AUTOMOTIVE IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 71 NORTH AMERICA CONSUMER PRODUCTS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 72 NORTH AMERICA CONSUMER PRODUCTS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 73 NORTH AMERICA TELECOMMUNICATIONS PRODUCTS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 74 NORTH AMERICA TELECOMMUNICATIONS PRODUCTS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 75 NORTH AMERICA MEDICAL IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 76 NORTH AMERICA MEDICAL IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 77 NORTH AMERICA AEROSPACE AND DEFENCE IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 78 NORTH AMERICA AEROSPACE AND DEFENCE IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 79 NORTH AMERICA OTHERS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 80 NORTH AMERICA OTHERS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 81 REGION

TABLE 82 NORTH AMERICA COPPER MARKET, BY COUNTRY, 2018-2033 (USD MILLION)

TABLE 83 NORTH AMERICA COPPER MARKET, BY COUNTRY, 2018-2033 (THOUSAND TONS)

TABLE 84 NORTH AMERICA

TABLE 85 NORTH AMERICA COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 86 NORTH AMERICA COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 87 NORTH AMERICA COPPER MARKET, BY TEMPER, 2018-2033 (USD MILLION)

TABLE 88 NORTH AMERICA COPPER MARKET, BY TEMPER, 2018-2033 (THOUSAND TONS)

TABLE 89 NORTH AMERICA COPPER MARKET, BY COPPRER GRADE, 2018-2033 (USD MILLION)

TABLE 90 NORTH AMERICA COPPER MARKET, BY COPPRER GRADE, 2018-2033 (THOUSAND TONS)

TABLE 91 NORTH AMERICA COPPER MARKET, BY APPLICATION, 2018-2033 (USD MILLION)

TABLE 92 NORTH AMERICA COPPER MARKET, BY APPLICATION, 2018-2033 (THOUSAND TONS)

TABLE 93 NORTH AMERICA COPPER MARKET, BY END-USE, 2018-2033 (USD MILLION)

TABLE 94 NORTH AMERICA COPPER MARKET, BY END-USE, 2018-2033 (THOUSAND TONS)

TABLE 95 NORTH AMERICA CONSTRUCTION IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 96 NORTH AMERICA CONSTRUCTION IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 97 NORTH AMERICA ELECTRICALS AND ELECTRONICS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 98 NORTH AMERICA ELECTRICALS AND ELECTRONICS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 99 NORTH AMERICA POWER AND ENERGY IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 100 NORTH AMERICA POWER AND ENERGY IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 101 NORTH AMERICA AUTOMOTIVE IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 102 NORTH AMERICA AUTOMOTIVE IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 103 NORTH AMERICA CONSUMER PRODUCTS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 104 NORTH AMERICA CONSUMER PRODUCTS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 105 NORTH AMERICA TELECOMMUNICATIONS PRODUCTS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 106 NORTH AMERICA TELECOMMUNICATIONS PRODUCTS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 107 NORTH AMERICA MEDICAL IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 108 NORTH AMERICA MEDICAL IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 109 NORTH AMERICA AEROSPACE AND DEFENCE IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 110 NORTH AMERICA AEROSPACE AND DEFENCE IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 111 NORTH AMERICA OTHERS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 112 NORTH AMERICA OTHERS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 113 U.S. COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 114 U.S. COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 115 U.S. COPPER MARKET, BY TEMPER, 2018-2033 (USD MILLION)

TABLE 116 U.S. COPPER MARKET, BY TEMPER, 2018-2033 (THOUSAND TONS)

TABLE 117 U.S. COPPER MARKET, BY COPPRER GRADE, 2018-2033 (USD MILLION)

TABLE 118 U.S. COPPER MARKET, BY COPPRER GRADE, 2018-2033 (THOUSAND TONS)

TABLE 119 U.S. COPPER MARKET, BY APPLICATION, 2018-2033 (USD MILLION)

TABLE 120 U.S. COPPER MARKET, BY APPLICATION, 2018-2033 (THOUSAND TONS)

TABLE 121 U.S. COPPER MARKET, BY END-USE, 2018-2033 (USD MILLION)

TABLE 122 U.S. COPPER MARKET, BY END-USE, 2018-2033 (THOUSAND TONS)

TABLE 123 U.S. CONSTRUCTION IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 124 U.S. CONSTRUCTION IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 125 U.S. ELECTRICALS AND ELECTRONICS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 126 U.S. ELECTRICALS AND ELECTRONICS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 127 U.S. POWER AND ENERGY IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 128 U.S. POWER AND ENERGY IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 129 U.S. AUTOMOTIVE IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 130 U.S. AUTOMOTIVE IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 131 U.S. CONSUMER PRODUCTS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 132 U.S. CONSUMER PRODUCTS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 133 U.S. TELECOMMUNICATIONS PRODUCTS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 134 U.S. TELECOMMUNICATIONS PRODUCTS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 135 U.S. MEDICAL IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 136 U.S. MEDICAL IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 137 U.S. AEROSPACE AND DEFENCE IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 138 U.S. AEROSPACE AND DEFENCE IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 139 U.S. OTHERS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 140 U.S. OTHERS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 141 CANADA COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 142 CANADA COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 143 CANADA COPPER MARKET, BY TEMPER, 2018-2033 (USD MILLION)

TABLE 144 CANADA COPPER MARKET, BY TEMPER, 2018-2033 (THOUSAND TONS)

TABLE 145 CANADA COPPER MARKET, BY COPPRER GRADE, 2018-2033 (USD MILLION)

TABLE 146 CANADA COPPER MARKET, BY COPPRER GRADE, 2018-2033 (THOUSAND TONS)

TABLE 147 CANADA COPPER MARKET, BY APPLICATION, 2018-2033 (USD MILLION)

TABLE 148 CANADA COPPER MARKET, BY APPLICATION, 2018-2033 (THOUSAND TONS)

TABLE 149 CANADA COPPER MARKET, BY END-USE, 2018-2033 (USD MILLION)

TABLE 150 CANADA COPPER MARKET, BY END-USE, 2018-2033 (THOUSAND TONS)

TABLE 151 CANADA CONSTRUCTION IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 152 CANADA CONSTRUCTION IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 153 CANADA ELECTRICALS AND ELECTRONICS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 154 CANADA ELECTRICALS AND ELECTRONICS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 155 CANADA POWER AND ENERGY IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 156 CANADA POWER AND ENERGY IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 157 CANADA AUTOMOTIVE IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 158 CANADA AUTOMOTIVE IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 159 CANADA CONSUMER PRODUCTS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 160 CANADA CONSUMER PRODUCTS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 161 CANADA TELECOMMUNICATIONS PRODUCTS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 162 CANADA TELECOMMUNICATIONS PRODUCTS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 163 CANADA MEDICAL IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 164 CANADA MEDICAL IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 165 CANADA AEROSPACE AND DEFENCE IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 166 CANADA AEROSPACE AND DEFENCE IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 167 CANADA OTHERS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 168 CANADA OTHERS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 169 MEXICO COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 170 MEXICO COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 171 MEXICO COPPER MARKET, BY TEMPER, 2018-2033 (USD MILLION)

TABLE 172 MEXICO COPPER MARKET, BY TEMPER, 2018-2033 (THOUSAND TONS)

TABLE 173 MEXICO COPPER MARKET, BY COPPRER GRADE, 2018-2033 (USD MILLION)

TABLE 174 MEXICO COPPER MARKET, BY COPPRER GRADE, 2018-2033 (THOUSAND TONS)

TABLE 175 MEXICO COPPER MARKET, BY APPLICATION, 2018-2033 (USD MILLION)

TABLE 176 MEXICO COPPER MARKET, BY APPLICATION, 2018-2033 (THOUSAND TONS)

TABLE 177 MEXICO COPPER MARKET, BY END-USE, 2018-2033 (USD MILLION)

TABLE 178 MEXICO COPPER MARKET, BY END-USE, 2018-2033 (THOUSAND TONS)

TABLE 179 MEXICO CONSTRUCTION IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 180 MEXICO CONSTRUCTION IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 181 MEXICO ELECTRICALS AND ELECTRONICS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 182 MEXICO ELECTRICALS AND ELECTRONICS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 183 MEXICO POWER AND ENERGY IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 184 MEXICO POWER AND ENERGY IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 185 MEXICO AUTOMOTIVE IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 186 MEXICO AUTOMOTIVE IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 187 MEXICO CONSUMER PRODUCTS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 188 MEXICO CONSUMER PRODUCTS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 189 MEXICO TELECOMMUNICATIONS PRODUCTS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 190 MEXICO TELECOMMUNICATIONS PRODUCTS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 191 MEXICO MEDICAL IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 192 MEXICO MEDICAL IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 193 MEXICO AEROSPACE AND DEFENCE IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)

TABLE 194 MEXICO AEROSPACE AND DEFENCE IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (THOUSAND TONS)

TABLE 195 MEXICO OTHERS IN COPPER MARKET, BY PRODUCT FORM, 2018-2033 (USD MILLION)