North America Craniomaxilofacial Devices Market

Market Size in USD Billion

USD

2.03 Billion

USD

3.76 Billion

2024

2032

USD

2.03 Billion

USD

3.76 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.03 Billion | |

| USD 3.76 Billion | |

| % | |

|

North America Craniomaxillofacial Devices Market Size

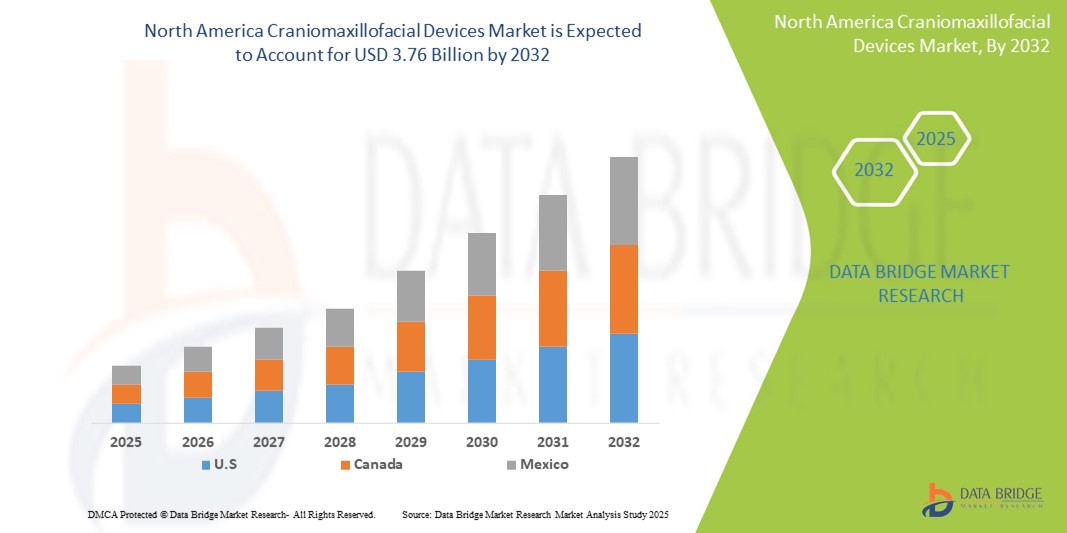

- The North America craniomaxillofacial devices market size was valued at USD 2.03 billion in 2024 and is expected to reach USD 3.76 billion by 2032, at a CAGR of 8.00% during the forecast period

- The market growth is largely fueled by the increasing prevalence of facial trauma, congenital deformities, and rising demand for reconstructive surgeries, coupled with advancements in biomaterials and 3D printing technologies for customized implants

- Furthermore, growing patient awareness regarding minimally invasive procedures, combined with the rising adoption of technologically advanced craniomaxillofacial devices by healthcare providers, is establishing these devices as a critical solution in modern surgical care. These converging factors are accelerating the uptake of craniomaxillofacial devices, thereby significantly boosting the industry's growth

North America Craniomaxillofacial Devices Market Analysis

- Craniomaxillofacial devices, offering advanced surgical solutions for the treatment of facial fractures, trauma, deformities, and reconstructive surgeries, are increasingly vital components of modern healthcare systems in both hospitals and specialty clinics due to their clinical effectiveness, improved patient outcomes, and seamless integration with advanced surgical techniques

- The escalating demand for craniomaxillofacial devices is primarily fueled by the rising prevalence of facial trauma cases, an increase in cosmetic and reconstructive surgical procedures, and a growing preference for minimally invasive surgical interventions

- U.S. dominated the craniomaxillofacial devices market with the largest revenue share of 76.3% in 2024, characterized by advanced healthcare infrastructure, high surgical volumes, and a strong presence of leading industry players. The country is experiencing substantial growth in craniomaxillofacial device adoption, particularly in trauma centers and specialized hospitals, driven by continuous innovations and favorable reimbursement policies

- Canada is expected to be the fastest growing country in the craniomaxillofacial devices market during the forecast period, supported by rising investments in healthcare modernization, growing access to specialized surgical care, and an increasing incidence of craniofacial conditions requiring surgical intervention

- The internal fixators segment dominated the market with a revenue share of 62.4% in 2024, owing to their ability to provide rigid, long-term stabilization while minimizing surgical trauma

Report Scope and Craniomaxillofacial Devices Market Segmentation

|

Attributes |

Craniomaxillofacial Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

North America Craniomaxillofacial Devices Market Trends

Enhanced Precision Through Technological Integration

- A significant and accelerating trend in the North America craniomaxillofacial devices market is the growing integration of advanced technologies such as computer-assisted surgical navigation, 3D printing, and robotic-assisted systems. These innovations are enhancing surgical precision, reducing procedure time, and improving patient outcomes in craniomaxillofacial procedures

- For instance, leading manufacturers are increasingly adopting patient-specific implants (PSIs) created through 3D printing technologies. These implants are tailored to match a patient’s unique anatomy, allowing for improved fit, faster recovery, and reduced complication rates compared to conventional implants

- The use of intraoperative imaging and surgical navigation systems is also expanding, providing real-time visualization that allows surgeons to operate with greater accuracy during complex reconstructive and trauma surgeries. These solutions support minimally invasive approaches and help reduce postoperative risks

- Furthermore, robotic-assisted platforms are being introduced in craniomaxillofacial surgeries to support delicate reconstructions and implant placements. These systems provide enhanced dexterity, stability, and precision, addressing challenges in highly complex anatomical regions

- The seamless integration of advanced visualization tools, surgical planning software, and customized implants is fundamentally reshaping expectations within the craniomaxillofacial field. Hospitals and specialty clinics in North America are increasingly investing in these solutions to provide safer, faster, and more reliable care

- As a result, the demand for craniomaxillofacial devices that offer precision, customization, and interoperability with digital surgical tools is growing rapidly across trauma, oncology, and reconstructive surgery applications, thereby fueling overall market expansion

North America Craniomaxillofacial Devices Market Dynamics

Driver

Growing Need Due to Rising Cases of Facial Trauma and Reconstructive Surgeries

- The increasing prevalence of facial injuries caused by accidents, sports-related trauma, and rising demand for reconstructive surgeries is a significant driver for the heightened demand for craniomaxillofacial devices

- For instance, in September 2024, Zimmer Biomet launched its CranioFix 3D Patient-Specific Implant System, designed to provide customized cranial and facial reconstruction solutions. The system enables precise anatomical fit, reduces operative time, and improves post-surgical outcomes for patients undergoing craniofacial trauma and reconstructive surgeries. Such developments by key players are expected to drive the Craniomaxillofacial Devices industry growth in the forecast period

- As patients and surgeons increasingly seek effective solutions for restoring facial form and function, craniomaxillofacial devices offer advanced features such as rigid fixation, biocompatibility, and minimally invasive application, providing a compelling upgrade over traditional surgical methods

- Furthermore, the growing popularity of cosmetic and reconstructive procedures, coupled with the expansion of specialized maxillofacial surgical centers, is making craniomaxillofacial devices an integral component of modern surgical care

- The convenience of advanced plating systems, distraction devices, and 3D-printed implants, along with their ability to reduce recovery times and improve aesthetic as well as functional outcomes, are key factors propelling adoption in both trauma and elective surgeries. The rising number of road traffic accidents and technological advancements in biomaterials further contribute to market growth

Restraint/Challenge

Concerns Regarding High Costs and Limited Access in Emerging Regions

- The high costs associated with craniomaxillofacial surgical procedures and devices pose a significant challenge to broader market penetration. Advanced fixation systems, custom implants, and navigation-assisted surgical tools are often expensive, limiting adoption among healthcare providers in cost-sensitive markets

- For instance, many hospitals in developing regions struggle with limited budgets and are unable to afford cutting-edge craniomaxillofacial devices, which restricts accessibility for patients in need of advanced trauma or reconstructive care

- Addressing these cost-related barriers through favorable reimbursement policies, local manufacturing, and affordable device portfolios will be crucial for increasing adoption. Companies such as Medtronic and Zimmer Biomet are focusing on developing cost-effective solutions and expanding training programs for surgeons in emerging economies

- Another challenge lies in the limited availability of highly skilled surgeons trained in craniomaxillofacial procedures, especially in low- and middle-income countries. This skills gap hampers widespread utilization of advanced devices

- While technological advancements and gradual cost reductions are improving accessibility, overcoming these barriers will require collaborative efforts between manufacturers, healthcare systems, and policymakers to ensure equitable patient access to advanced craniomaxillofacial treatments

North America Craniomaxillofacial Devices Market Scope

The market is segmented on the basis of product, material, location, application, and end-user.

- By Product

On the basis of product, the North America craniomaxillofacial devices market is segmented into bone graft substitute, MF plate and screw fixation, CMF distraction, cranial flap fixation, thoracic fixation, and temporomandibular joint replacement. The bone graft substitute segment dominated the market with the largest revenue share of 34.2% in 2024, owing to its crucial role in facilitating bone regeneration and providing structural support in reconstructive and trauma surgeries. Bone graft substitutes, including both synthetic and allogenic materials, are increasingly preferred for their versatility, high success rates, and compatibility with various surgical procedures. Their use across neurosurgery, orthognathic, plastic, and trauma surgeries reinforces their market dominance. Hospitals and surgical centers rely heavily on bone graft substitutes to restore structural integrity and optimize functional and aesthetic outcomes. The growing adoption of minimally invasive techniques and advanced surgical planning further strengthens demand. The segment benefits from continuous product innovations, clinical validation, and broad surgeon familiarity, ensuring its continued leading position in the market.

The MF plate and screw fixation segment is forecasted to grow at the fastest CAGR of 9.1% from 2025 to 2032, driven by technological advancements in implant design and materials. These systems provide enhanced stability and precise fixation in craniofacial surgeries, reducing operative times and improving patient outcomes. Increasing adoption in trauma cases, combined with integration into patient-specific surgical planning and computer-assisted navigation, supports rapid growth. Hospitals and specialty clinics are investing in these systems to enhance surgical efficiency and reliability. Rising awareness of postoperative complications and the need for predictable outcomes is further accelerating the uptake of MF plate and screw systems. Furthermore, improvements in biocompatible metals and modular plates allow customization for complex anatomical requirements. The segment’s growth is also propelled by expanding clinical applications in reconstructive, orthognathic, and tumor-related surgeries across North America.

- By Material

On the basis of material, the craniomaxillofacial devices market is segmented into ceramic, biological, metal, and polymers. The metal segment held the largest revenue share of 45.7% in 2024, primarily due to superior mechanical strength, biocompatibility, and long-term reliability of titanium alloys and stainless steel. Metals are widely preferred for load-bearing applications and structural reinforcement in complex craniofacial procedures. Titanium, in particular, supports osseointegration and minimizes rejection risk, making it the standard choice for reconstructive and trauma surgeries. The extensive clinical experience with metal implants, combined with high surgeon confidence and regulatory approval, reinforces its dominant position.

The polymers segment is expected to witness the fastest CAGR of 8.3% from 2025 to 2032, driven by the increasing use of bioresorbable and composite materials. These materials promote natural bone regeneration, reduce the need for secondary surgeries, and are especially valuable in pediatric and elective cases. Advances in material science, including enhanced strength and flexibility, enable broader clinical adoption. Expanding awareness among surgeons and improved regulatory acceptance are further contributing to growth. Moreover, ongoing R&D in innovative polymer coatings and composites is enhancing implant biocompatibility, further accelerating market adoption

- By Location

On the basis of location, the craniomaxillofacial devices market is segmented into external fixators and internal fixators. The internal fixators segment dominated the market with a revenue share of 62.4% in 2024, owing to their ability to provide rigid, long-term stabilization while minimizing surgical trauma. Internal fixators are highly preferred in trauma, reconstructive, and congenital surgeries as they ensure optimal bone healing and functional restoration. Their compatibility with minimally invasive surgical techniques enhances patient recovery times and reduces postoperative complications. Surgeons also favor internal fixators for their versatility across complex craniofacial procedures. The widespread clinical adoption and established trust among healthcare professionals further reinforce their dominance. Additionally, robust regulatory approvals and extensive availability in hospitals and specialized clinics contribute to the segment’s strong market position.

The external fixators segment is projected to grow at the fastest CAGR of 7.6% from 2025 to 2032, fueled by increasing demand for adjustable stabilization in complex trauma and severe deformity cases. Advances in lightweight materials, modular designs, and enhanced adjustability improve both surgical precision and patient comfort. External fixators are increasingly used in emergency interventions, pediatric trauma, and cases requiring rapid postoperative adjustments. The adoption of innovative designs that facilitate minimally invasive application and reduce operative time is further driving growth. Growing awareness among surgeons about their versatility and expanding use in specialized trauma centers contribute to the accelerating market share.

- By Application

On the basis of application, the craniomaxillofacial devices market is segmented into plastic surgery, neurosurgery and ENT, and orthognathic and dental surgery. The plastic surgery segment held the largest market share of 38.6% in 2024, driven by the increasing incidence of congenital deformities, tumor resections, and post-traumatic reconstruction needs. Advanced implants in this segment help restore structural integrity, facial symmetry, and overall aesthetics, making them indispensable for reconstructive procedures. The segment benefits from continuous innovations in biomaterials, patient-specific implants, and minimally invasive techniques, which enhance surgical outcomes. Surgeons and hospitals increasingly rely on these implants to meet high patient expectations for functionality and appearance. The established clinical expertise, broad availability of products, and high procedural volume contribute to the dominance of the plastic surgery application.

The orthognathic and dental surgery segment is expected to witness the fastest CAGR of 8.5% from 2025 to 2032, supported by growing awareness of corrective jaw surgeries, improved facial aesthetics, and advancements in computer-aided surgical planning. The adoption of patient-specific implants, 3D-printed surgical guides, and minimally invasive approaches further accelerates growth. Rising patient demand for cosmetic and functional improvements, combined with increased access to advanced surgical technologies, fuels segment expansion. Surgeons are increasingly integrating these implants for precise alignment, faster recovery, and improved postoperative outcomes. Market growth is also reinforced by expanding dental and craniofacial specialty clinics and educational initiatives highlighting benefits of corrective procedures.

- By End-User

On the basis of end-user, the craniomaxillofacial devices market is segmented into hospitals and ASCs. The hospitals segment dominated the market with a revenue share of 48.4% in 2024, primarily due to their advanced surgical infrastructure, availability of multidisciplinary care teams, and ability to handle high-volume craniofacial procedures. Hospitals are the central hubs for trauma management, reconstructive surgeries, and complex craniomaxillofacial cases that require specialized expertise and access to advanced imaging and robotic systems. Their strong reimbursement framework, comprehensive postoperative care, and wide adoption of innovative implants further strengthen their dominance. Additionally, the presence of experienced surgeons and access to cutting-edge technologies make hospitals the preferred choice for patients undergoing both emergency and elective craniofacial surgeries.

The ASCs segment is expected to witness the fastest CAGR of 9.3% from 2025 to 2032, driven by the growing preference for outpatient and same-day surgical procedures. Ambulatory surgical centers offer shorter waiting times, reduced costs, and more personalized care compared to hospitals, making them increasingly attractive to patients. The adoption of minimally invasive techniques and integration of 3D-printed patient-specific implants in ASCs are expanding their scope in craniofacial surgeries. Their ability to deliver high-quality care in a more focused, patient-centered environment, combined with the rising number of elective procedures, is expected to accelerate segment growth significantly over the forecast period.

North America Craniomaxillofacial Devices Market Regional Analysis

- North America dominated the craniomaxillofacial devices market with the largest revenue share in 2024, driven by advanced healthcare infrastructure, high surgical adoption rates, and the presence of globally leading manufacturers

- The region’s dominance is further supported by a rising incidence of craniofacial trauma cases, congenital deformities, and reconstructive surgeries, which are fueling the demand for innovative implants and fixation systems

- Strong reimbursement frameworks, growing awareness of patient-specific implants, and rapid integration of 3D printing technologies in surgical planning have also reinforced North America’s leadership position in this market

U.S. Craniomaxillofacial Devices Market Insight

The U.S. craniomaxillofacial devices market captured the largest revenue share of 76.3% in 2024 within North America, underpinned by well-established healthcare infrastructure, higher surgical volumes, and the widespread presence of leading medical device companies. Growth in the U.S. market is particularly strong in trauma centers, academic hospitals, and specialty clinics, where advanced surgical procedures are increasingly supported by cutting-edge technologies such as navigation-assisted surgery and customized implants. Favorable reimbursement policies, continuous product innovations, and a high level of surgeon expertise are accelerating the adoption of craniomaxillofacial devices in the country.

Canada Craniomaxillofacial Devices Market Insight

The Canada craniomaxillofacial devices market is expected to be the fastest-growing country in the Craniomaxillofacial Devices market during the forecast period, projected to register a strong CAGR, driven by rising healthcare modernization initiatives, growing government investments in surgical infrastructure, and improved access to specialized craniofacial care. Increasing awareness of minimally invasive approaches, adoption of 3D-printed patient-specific implants, and the expansion of specialty clinics are contributing significantly to market growth. The rising incidence of craniofacial trauma cases from accidents and sports-related injuries, along with growing demand for elective reconstructive surgeries, further supports Canada’s accelerating market trajectory.

North America Craniomaxillofacial Devices Market Share

The Craniomaxillofacial Devices industry is primarily led by well-established companies, including:

- Zimmer Biomet (U.S.)

- Stryker (U.S.)

- Johnson & Johnson and its affiliates (U.S.)

- Medtronic (U.S.)

- INTEGRA LIFESCIENCES CORPORATION (U.S.)

- KLS Martin Group (Germany)

- B. Braun SE (Germany)

- Renishaw plc (U.K.)

- 3D Systems, Inc. (U.S.)

- Acumed LLC (U.S.)

- Medartis AG (Switzerland)

- OsteoMed (U.S.)

- Calavera Surgical Design (U.S.)

- Bioplate Inc. (U.S.)

Latest Developments in North America Craniomaxillofacial Devices Market

- In June 2022, Ricoh USA, Inc. received FDA 510(k) clearance for its RICOH 3D for Healthcare solution, enabling the production of patient-specific 3D-printed anatomic models for craniomaxillofacial and orthopedic applications. This development is a significant step in advancing surgical planning by providing precise, personalized models that improve preoperative preparation and overall patient outcomes

- In May 2023, Ricoh secured an expanded FDA 510(k) clearance for its craniomaxillofacial and orthopedic 3D modeling service, which now includes soft-tissue anatomical models in addition to bone structures. This expansion broadens its clinical utility, allowing surgeons to gain deeper insights into complex anatomies, ultimately enhancing surgical precision and decision-making

- In April 2024, 3D Systems announced FDA 510(k) clearance for its VSP PEEK Cranial Implant, marking the world’s first patient-specific, additively manufactured PEEK implant designed for cranioplasty procedures. Developed with Evonik’s VESTAKEEP PEEK biomaterial and the EXT 220 MED 3D printer, this innovation represents a breakthrough in personalized cranial reconstruction, combining biocompatibility with advanced digital workflows

- In June 2024, MCRA, LLC supported 3D Systems in achieving FDA clearance for the VSP PEEK Cranial Implant, providing regulatory, biocompatibility, and scientific expertise throughout the approval process. This milestone highlights the growing collaboration between regulatory specialists and medical device innovators to accelerate the adoption of advanced, patient-specific craniomaxillofacial implants in North America

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.