North America Dexa Equipment Market

Market Size in USD Million

USD

352.47 Million

USD

652.39 Million

2025

2033

USD

352.47 Million

USD

652.39 Million

2025

2033

| 2026 - 2033 | |

| USD 352.47 Million | |

| USD 652.39 Million | |

| % | |

|

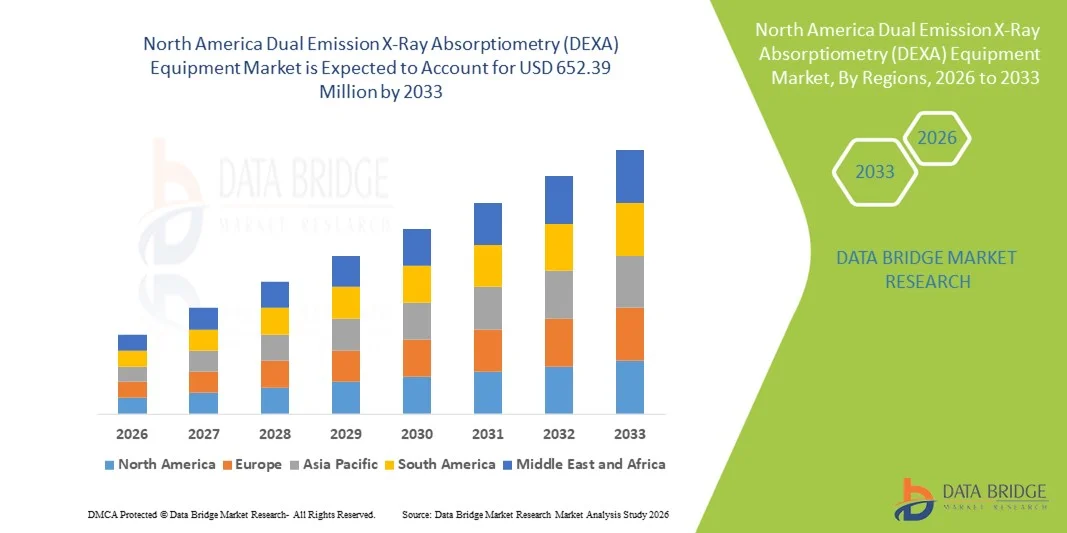

North America Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market Size

- The North America Dual Emission X-Ray Absorptiometry (DEXA) equipment market size was valued at USD 352.47 million in 2025 and is expected to reach USD 652.39 million by 2033, at a CAGR of 8.00% during the forecast period

- The market growth is largely fueled by the increasing prevalence of osteoporosis and other bone-related disorders in aging populations, coupled with the rising focus on early diagnosis and preventive healthcare. Advancements in imaging technologies and integration with healthcare IT systems are further enhancing the efficiency and accuracy of DEXA scan

- Furthermore, growing awareness among clinicians and patients about bone health, along with rising adoption of non-invasive and low-radiation diagnostic tools in hospitals, clinics, and diagnostic centers, is positioning DEXA as the preferred solution for bone density assessment. These converging factors are accelerating the adoption of DEXA equipment, thereby significantly boosting the industry's growth

North America Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market Analysis

- DEXA equipment, providing precise measurement of bone mineral density and body composition, is increasingly critical in healthcare for early osteoporosis diagnosis, fracture risk assessment, and preventive care, due to its non-invasive nature, low radiation exposure, and clinical accuracy

- The escalating demand for DEXA equipment is primarily fueled by the rising prevalence of osteoporosis, growing aging population, and increasing awareness of preventive healthcare in the United States. Technological advancements such as faster scan times, higher-resolution imaging, and integration with electronic health records (EHRs) are further driving adoption in hospitals, clinics, and mobile health centers

- The United States dominated the North America DEXA equipment market with the largest revenue share of 78.35% in 2025, characterized by advanced healthcare infrastructure, high per capita healthcare expenditure, and a strong presence of key manufacturers, with substantial adoption in hospitals and diagnostic centers driven by demand for routine bone health monitoring and fracture risk assessment

- Canada is expected to be the fastest-growing country in the North America DEXA equipment market during the forecast period due to increasing healthcare investments, rising awareness about bone health, and government initiatives promoting early osteoporosis screening and preventive care programs

- Bone densitometry and fracture risk assessment segment dominated the North America DEXA equipment market in 2025 with a share of 50.9%, owing to their critical role in osteoporosis detection, treatment planning, and preventive healthcare

Report Scope and North America Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market Segmentation

|

Attributes |

North America Dual Emission X-Ray Absorptiometry (DEXA) Equipment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

North America Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market Trends

Enhanced Diagnostic Accuracy Through Advanced Imaging and AI Integration

- A significant and accelerating trend in the North America DEXA equipment market is the incorporation of advanced imaging technologies and AI-driven analysis software, enhancing diagnostic accuracy and patient monitoring capabilities

- For instance, newer DEXA systems such as GE Lunar iDXA and Hologic Horizon integrate AI algorithms to automatically detect and highlight regions of low bone density, streamlining the workflow for clinicians and improving early diagnosis of osteoporosis and fracture risk

- AI integration in DEXA equipment enables predictive analytics for fracture risk, automated reporting, and longitudinal patient monitoring, helping clinicians provide personalized care plans. Some systems can learn patient-specific trends over time, offering smarter alerts and actionable insights

- The integration with hospital IT systems and electronic health records (EHRs) allows centralized control of imaging data, facilitating seamless coordination across departments, research studies, and preventive healthcare programs

- This trend toward more intelligent, precise, and interconnected DEXA systems is reshaping clinical expectations for bone health diagnostics. Consequently, manufacturers such as Hologic and GE Healthcare are developing AI-enabled DEXA scanners with enhanced analysis, faster scan times, and improved patient workflow

- The demand for DEXA equipment with AI-assisted imaging and advanced analytical capabilities is growing rapidly across hospitals, clinics, and mobile health centers, as healthcare providers increasingly prioritize accuracy, efficiency, and preventive care

- The growing use of DEXA in personalized medicine, such as monitoring bone health during osteoporosis treatment or evaluating body composition in metabolic and sports medicine, is opening new applications and revenue streams

North America Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market Dynamics

Driver

Rising Osteoporosis Prevalence and Preventive Healthcare Awareness

- The increasing prevalence of osteoporosis and age-related bone disorders, coupled with rising awareness of preventive healthcare and early diagnosis, is a key driver for the adoption of DEXA equipment in North America

- For instance, in 2025, Hologic launched an updated AI-enabled Horizon scanner targeting enhanced fracture risk assessment, reflecting the focus on technological advancements to meet growing clinical demand

- As clinicians and patients increasingly prioritize bone health monitoring, DEXA provides precise measurements of bone mineral density, body composition, and fracture risk, offering a clear advantage over traditional assessment methods

- Furthermore, the growing adoption of routine health screenings, preventive care initiatives, and integration of DEXA into research studies makes it a vital diagnostic tool in hospitals, clinics, and mobile health centers

- Features such as automated reporting, fast scan times, and non-invasive imaging with minimal radiation exposure further propel the adoption of DEXA equipment across healthcare settings

- Expansion of mobile DEXA services and community health programs is driving adoption in underserved regions, creating new opportunities for portable and compact systems

- Partnerships between equipment manufacturers and healthcare providers for bundled preventive care packages are increasing market penetration and driving recurring service-based revenue

Restraint/Challenge

High Cost and Regulatory Compliance Hurdles

- The relatively high acquisition and maintenance cost of advanced DEXA systems can pose a barrier to adoption, particularly for smaller clinics or mobile health programs with limited budgets

- In addition, regulatory compliance requirements for medical imaging devices, including FDA approvals and adherence to safety standards, add complexity and time to the introduction of new systems

- Addressing these challenges through cost-effective product development, leasing models, and ensuring timely regulatory approvals is crucial for broader market penetration. Manufacturers such as GE Healthcare and Hologic emphasize reliability, compliance, and service support to build trust among healthcare providers

- While technological advancements improve clinical utility, smaller or budget-conscious healthcare facilities may delay adoption until more affordable options are available

- Overcoming these barriers through financing solutions, regulatory support, and user-friendly, low-maintenance DEXA systems will be vital for sustaining market growth in North America

- Cybersecurity concerns related to AI-enabled DEXA software and patient data management are emerging as a challenge, requiring robust encryption and secure data protocols

- Limited awareness among some clinicians about advanced DEXA capabilities and AI integration can slow adoption, highlighting the need for targeted training and educational initiatives

North America Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market Scope

The market is segmented on the basis of product type, application, and end users.

- By Product Type

On the basis of product type, the North America DEXA equipment market is segmented into central DEXA and peripheral DEXA. The Central DEXA segment dominated the market with the largest revenue share of 65% in 2025, driven by its ability to perform full-body bone densitometry and comprehensive fracture risk assessment. Central systems are widely adopted in hospitals and large diagnostic centers due to their precision, reliability, and advanced imaging capabilities. They often integrate with AI-powered analytics software, enabling automated detection of low bone density and improving workflow efficiency. Hospitals and research facilities prefer central DEXA systems for multi-region assessment and longitudinal patient monitoring. The high accuracy, versatility, and compatibility with EHR systems make them indispensable in preventive healthcare programs.

The Peripheral DEXA segment is expected to witness the fastest growth rate of 20% from 2026 to 2033, fueled by rising demand for targeted and portable bone density screening solutions. Peripheral systems are ideal for specific body sites such as wrists, heels, or forearms, allowing clinics and mobile health centers to conduct cost-effective assessments without large infrastructure. Their compact size and ease of transport make them suitable for remote or community-based health programs. Peripheral DEXA devices are increasingly used in preventive healthcare initiatives, fitness centers, and research applications. The segment’s growth is further supported by technological enhancements improving scan speed, accuracy, and AI-assisted analysis. With rising awareness of osteoporosis screening and preventive care, peripheral DEXA adoption is gaining strong traction.

- By Application

On the basis of application, the market is segmented into bone densitometry and fracture risk assessment, fracture diagnosis, and body composition analysis. The Bone Densitometry and Fracture Risk Assessment segment dominated the market with a 50.9% share in 2025, driven by the high prevalence of osteoporosis and the need for early detection among aging populations. DEXA systems in this segment allow clinicians to monitor bone health, evaluate fracture risk, and develop personalized treatment plans. Integration with AI predictive tools further enhances clinical decision-making. The non-invasive nature and low radiation exposure of DEXA make it highly suitable for repeated patient monitoring. Hospitals, clinics, and research institutions rely heavily on this application for preventive care and longitudinal studies. Its dominance reflects both the clinical importance and high adoption rate across North American healthcare facilities.

The Body Composition Analysis segment is expected to witness the fastest growth rate of 18% during the forecast period, driven by increasing use in metabolic health management, sports medicine, and wellness programs. DEXA provides precise measurement of fat mass, lean mass, and visceral fat, making it superior to traditional body composition methods. Fitness centers, research labs, and clinical programs are adopting DEXA for personalized health and nutrition plans. The growth is fueled by rising consumer awareness of metabolic health and demand for non-invasive, accurate assessments. AI-assisted analysis and portable systems are expanding applications beyond hospitals into clinics and preventive care centers. As healthcare moves toward personalized medicine, body composition analysis with DEXA is emerging as a critical tool for both diagnostics and performance monitoring

- By End Users

On the basis of end users, the market is segmented into hospitals, clinics, mobile health centers, and others. The Hospitals segment dominated the market with a 55% share in 2025, driven by the need for high-precision diagnostic tools for bone health and fracture risk assessment. Hospitals utilize central DEXA systems for comprehensive patient evaluation and integration with electronic health records. This segment benefits from AI-assisted automated reporting and longitudinal patient tracking. Hospitals are also the primary buyers due to their capacity to invest in advanced technology and provide preventive care programs. The combination of accuracy, reliability, and workflow efficiency makes hospitals the largest and most critical end-user segment.

The Mobile Health Centers segment is expected to witness the fastest growth rate of 20% during the forecast period, fueled by the need to provide bone health diagnostics in remote and underserved areas. Portable and peripheral DEXA systems allow mobile units to conduct screenings without permanent infrastructure. Public health programs and preventive care campaigns are increasingly using mobile centers to reach populations with limited access to hospitals. The growth is supported by government initiatives promoting early osteoporosis detection and community health awareness. Mobile health centers also benefit from AI-assisted analytics and cloud-based reporting, improving accessibility and efficiency of care.

North America Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market Regional Analysis

- The United States dominated the North America DEXA equipment market with the largest revenue share of 78.35% in 2025, characterized by advanced healthcare infrastructure, high per capita healthcare expenditure, and a strong presence of key manufacturers, with substantial adoption in hospitals and diagnostic centers driven by demand for routine bone health monitoring and fracture risk assessment

- Healthcare providers in the region highly value the precision, low radiation exposure, and AI-assisted analysis offered by DEXA systems, enabling accurate bone mineral density measurement, fracture risk assessment, and body composition analysis

- This widespread adoption is further supported by advanced healthcare infrastructure, high per capita healthcare expenditure, and the presence of key market players, establishing DEXA as the preferred diagnostic solution for both clinical and preventive healthcare applications

U.S. Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market Insight

The U.S. DEXA equipment market captured the largest revenue share of 78.35% in 2025 within North America, fueled by the increasing prevalence of osteoporosis and rising awareness of preventive healthcare. Healthcare providers are prioritizing accurate bone mineral density measurement, fracture risk assessment, and body composition analysis using advanced DEXA systems. The adoption of AI-enabled scanners, faster imaging, and integration with electronic health records (EHRs) further propels the market. Moreover, the expanding use of DEXA in research institutions, hospitals, and mobile health centers is driving growth. The demand for portable and peripheral DEXA systems is also increasing to support community screening and preventive care initiatives.

Canada Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market Insight

The Canada DEXA equipment market is expected to grow at the fastest CAGR during the forecast period, driven by government-led preventive healthcare programs, rising osteoporosis awareness, and increasing investments in diagnostic infrastructure. Healthcare providers are adopting AI-assisted and portable DEXA systems for improved patient care, while mobile screening initiatives are enhancing access in remote regions. The growth of private clinics and research centers is also contributing to market expansion. Advanced imaging capabilities and non-invasive, low-radiation scans make DEXA systems a preferred choice across hospitals and community health programs.

Mexico Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market Insight

The Mexico DEXA equipment market is witnessing steady growth, fueled by increasing awareness of bone health, preventive screenings, and government initiatives targeting osteoporosis diagnosis. Hospitals and diagnostic centers are gradually upgrading to modern DEXA systems with higher resolution imaging and AI-assisted analysis. Adoption is also supported by the expansion of healthcare insurance coverage and the rise of private clinics. Growing investments in mobile health programs are enabling DEXA accessibility in underserved areas. Moreover, the trend toward body composition analysis in metabolic health and research applications is contributing to market demand.

North America Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market Share

The North America Dual Emission X-Ray Absorptiometry (DEXA) Equipment industry is primarily led by well-established companies, including:

- Hologic, Inc. (U.S.)

- GE HealthCare (U.S.)

- Swissray International, Inc. (U.S.)

- Mindways Software, Inc. (U.S.)

- Siemens Healthineers AG (Germany)

- Konica Minolta Healthcare Americas, Inc. (U.S.)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- FUJIFILM Healthcare (Japan)

- Analogic Corporation (U.S.)

- Carestream Health (U.S.)

- Ziehm Imaging (Germany)

- Mindray Medical International (China)

- Medtronic (Ireland)

- Orthoscan, Inc. (U.S.)

- Positron Corporation (U.S.)

- ICRco, LLC (U.S.)

- Whale Imaging, Inc. (U.S.)

- Norland at Swissray (U.S.)

What are the Recent Developments in North America Dual Emission X-Ray Absorptiometry (DEXA) Equipment Market?

- In January 2026, the U.S. Food and Drug Administration (FDA) cleared the use of bone scan measurements (including DEXA‑derived endpoints) as valid surrogate endpoints in osteoporosis clinical trials, enabling drug developers to evaluate new osteoporosis treatments more efficiently based on changes in bone mineral density rather than waiting for actual fracture outcomes

- In May 2025, SimonMed Imaging rolled out an advanced DEXA bone density scan combining bone density and bone quality analysis, expanding early osteoporosis detection capabilities at over 80 imaging locations. This enhanced DEXA service uses trabecular bone scoring (TBS) software cleared by the FDA, enabling clinicians to identify a higher number of patients at risk of fracture even when traditional bone mineral density appears normal, strengthening preventive care programs

- In April 2025, Johns Hopkins Medical Imaging announced the use of a new DEXA scanner at its Columbia center, featuring improved image quality and faster results for bone health exams. The upgrade signifies investment by a leading U.S. healthcare provider in enhanced densitometry technology, improving diagnostic accuracy for osteoporosis and fracture risk assessment

- In October 2024, Siemens Healthineers launched strategic efforts to integrate advanced AI‑enhanced imaging capabilities (including partnerships and collaborations) that support next‑generation imaging systems, signaling broader innovation trends relevant to diagnostic modalities such as DEXA. Though focused on imaging broadly, Siemens’ expansion of AI imaging technologies underscores the industry’s shift toward smarter diagnostics and integrated radiology platforms that can enhance DEXA workflows and analytics

- In May 2023, Shriners Children’s Portland installed a dedicated DEXA scan calibrated for pediatric use the first such system in the Pacific Northwest, improving bone health monitoring for children with conditions such as osteogenesis imperfecta and enhancing clinical decision‑making for treatment. This installation enables specialists to measure bone density and tailor bone‑strengthening therapies directly within the children’s hospital setting, eliminating the need to send pediatric patients to adult imaging facilities

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.