North America Diagnostic Electrocardiograph Ecg Market

Market Size in USD Billion

USD

123.40 Billion

USD

254.87 Billion

2024

2032

USD

123.40 Billion

USD

254.87 Billion

2024

2032

| 2025 - 2032 | |

| USD 123.40 Billion | |

| USD 254.87 Billion | |

| % | |

|

Diagnostic Electrocardiograph (ECG) Market Size

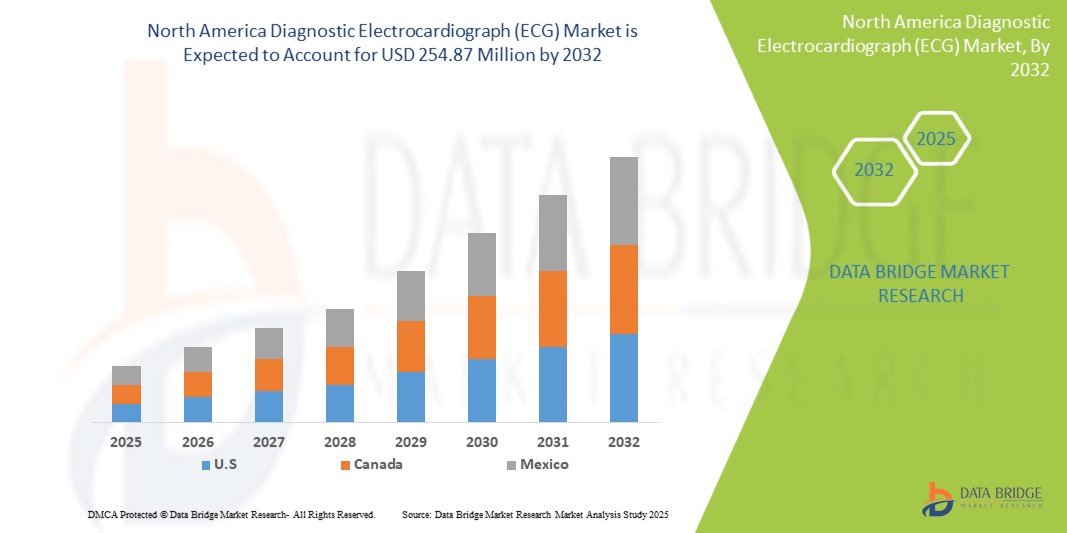

- The North America Diagnostic Electrocardiograph (ECG) Market size was valued at USD 123.40 million in 2024 and is expected to reach USD 254.87 million by 2032, at a CAGR of 9.5% during the forecast period.

- The market growth is largely fueled by the increasing prevalence of cardiovascular diseases, a rising geriatric population, and the growing demand for early and accurate diagnosis of cardiac conditions.

- Furthermore, technological advancements in ECG devices, such as portability, wireless connectivity, and integration with digital health platforms, are broadening their applications and enhancing patient monitoring, thereby significantly boosting the industry's growth.

Diagnostic Electrocardiograph (ECG) Market Analysis

- Diagnostic Electrocardiograph (ECG) devices, which record the electrical activity of the heart, are increasingly vital tools in modern cardiology and general healthcare settings due to their non-invasive nature, cost-effectiveness, and ability to provide crucial insights into cardiac function.

- The escalating demand for ECG devices is primarily fueled by the growing burden of cardiovascular diseases, increased awareness about heart health, and a rising preference for point-of-care diagnostics.

- U.S. dominates the Diagnostic Electrocardiograph (ECG) Market with the largest revenue share of 36.01% in 2025, characterized by a well-developed healthcare infrastructure, high healthcare expenditure, and strong adoption of advanced medical technologies. The U.S. is experiencing substantial growth in ECG device installations, particularly in hospitals and diagnostic centers, driven by innovations from both established medical device companies and startups focusing on AI-powered analysis and remote monitoring features.

- Canada is expected to be the fastest-growing region in the Diagnostic Electrocardiograph (ECG) Market during the forecast period due to increasing healthcare expenditure, rising awareness about cardiovascular diseases, and a growing geriatric population.

- The Resting ECG segment is expected to dominate the Diagnostic Electrocardiograph (ECG) Market with a market share of 43.2% in 2025, driven by its widespread use in routine check-ups and initial cardiac assessments.

Report Scope and Diagnostic Electrocardiograph (ECG) Market Segmentation

|

Attributes |

Diagnostic Electrocardiograph (ECG) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Diagnostic Electrocardiograph (ECG) Market Trends

“Integration of AI and Telemedicine for Enhanced Diagnostics”

- A significant and accelerating trend in the North America Diagnostic Electrocardiograph (ECG) Market is the deepening integration of artificial intelligence (AI) and telemedicine platforms. This fusion of technologies is significantly enhancing the efficiency, accuracy, and accessibility of cardiac diagnostics.

- For instance, AI algorithms are being developed and implemented to analyze ECG waveforms for automated detection of arrhythmias, myocardial ischemia, and other cardiac abnormalities, reducing the burden on clinicians and improving diagnostic speed. Similarly, portable and wearable ECG devices are seamlessly integrating with telemedicine platforms, allowing for remote monitoring of patients with cardiovascular conditions.

- This enables healthcare providers to remotely review ECG data, provide timely interventions, and manage chronic cardiac diseases more effectively, especially for patients in remote areas or those with limited mobility. The demand for ECG solutions that offer seamless AI-powered analysis and remote monitoring capabilities is growing rapidly across hospitals, diagnostic centers, and homecare settings, as healthcare systems increasingly prioritize convenience, cost-effectiveness, and comprehensive patient management.

Diagnostic Electrocardiograph (ECG) Market Dynamics

Driver

“Rising Prevalence of Cardiovascular Diseases and Aging Population”

- The increasing prevalence of cardiovascular diseases (CVDs) such as coronary artery disease, arrhythmias, and heart failure, coupled with a rapidly aging population in North America, is a significant driver for the heightened demand for Diagnostic Electrocardiograph (ECG) devices.

- CVDs remain a leading cause of morbidity and mortality, necessitating early and accurate diagnosis for effective management and improved patient outcomes. As the geriatric population grows, so does the incidence of age-related cardiac conditions, further increasing the need for routine cardiac monitoring and diagnostic procedures.

- For instance, According to the Centers for Disease Control and Prevention (CDC), heart disease is the leading cause of death for men, women, and most racial and ethnic groups in the United States. In 2021, about 695,000 people in the U.S. died from heart disease. This high burden directly translates to an increased need for diagnostic tools like ECG.

- ECG is a fundamental and non-invasive tool for initial cardiac assessment, screening, and monitoring, making it indispensable in clinical practice. The growing awareness among both healthcare professionals and the general public about the importance of early detection of heart conditions is propelling the adoption of ECG devices across various healthcare settings, from hospitals and clinics to homecare.

Restraint/Challenge

“High Cost of Advanced ECG Systems and Data Management Challenges”

- The relatively high initial cost of some advanced Diagnostic Electrocardiograph (ECG) systems, particularly those with sophisticated features like wireless connectivity, real-time data transmission, and integrated AI analysis, can be a significant barrier to broader market penetration, especially for smaller clinics or healthcare facilities with budget constraints.

- While basic ECG machines are affordable, the premium features that enhance diagnostic capabilities and workflow efficiency often come with a higher price tag. This can limit access to cutting-edge technology for some patient populations.

- Additionally, managing the vast amount of ECG data generated, especially from continuous monitoring devices like Holter monitors and event recorders, poses significant data management and cybersecurity challenges. Ensuring data security, privacy, and seamless integration with electronic health records (EHR) systems requires robust IT infrastructure and adherence to stringent regulations, which can be complex and costly for healthcare providers. Overcoming these challenges through cost-effective innovations and secure, interoperable data solutions will be vital for sustained market growth.

Diagnostic Electrocardiograph (ECG) Market Scope

The market is segmented on the basis of type, communication protocol, unlocking mechanism, and application.

- By Type

On the basis of type, the North America Diagnostic Electrocardiograph (ECG) Market is segmented into Resting ECG, Stress ECG, Holter Monitors, Event Recorders, and Others.

The Resting ECG segment dominates the largest market revenue share of 43.2% in 2025, driven by its widespread use as a primary diagnostic tool for initial cardiac assessment in routine check-ups, emergency settings, and general practitioners' offices due to its non-invasive nature and rapid results. The Holter Monitors segment is anticipated to witness the fastest growth rate of 7.7% from 2025 to 2032, fueled by the increasing prevalence of transient arrhythmias and the growing need for continuous, long-term cardiac monitoring outside of a clinical setting to detect intermittent cardiac events.

- By lead type

On the basis of lead type, the North America Diagnostic Electrocardiograph (ECG) Market is segmented into 3-Lead, 6-Lead, 12-Lead, and Others. The 12-Lead segment held the largest market revenue share in 2025, driven by its comprehensive view of the heart's electrical activity, making it the gold standard for diagnosing a wide range of cardiac conditions, including myocardial infarction and complex arrhythmias, in hospital and clinical settings.

The 3-Lead segment is expected to witness the fastest CAGR from 2025 to 2032, driven by its increasing adoption in portable and wearable ECG devices for basic rhythm monitoring in homecare and remote patient monitoring scenarios, offering simplicity and convenience.

- By End User

On the basis of end user, the North America Diagnostic Electrocardiograph (ECG) Market is segmented into Hospitals & Clinics, Diagnostic Centers, Ambulatory Surgical Centers, Homecare Settings, and Others. The Hospitals & Clinics segment accounted for the largest market revenue share in 2024, driven by the high volume of cardiac patients, the need for comprehensive diagnostic capabilities, and the routine use of ECGs for various medical procedures and patient admissions.

The Homecare Settings segment is expected to witness the fastest CAGR from 2025 to 2032, driven by the growing emphasis on remote patient monitoring, the rise of chronic cardiovascular conditions requiring continuous oversight, and the increasing availability of user-friendly, portable ECG devices for self-monitoring.

Diagnostic Electrocardiograph (ECG) Market Regional Analysis

- U.S. dominates the Diagnostic Electrocardiograph (ECG) Market with the largest revenue share of 36.01% in 2025. This dominance is primarily driven by a high prevalence of cardiovascular diseases, robust healthcare expenditure, advanced healthcare infrastructure, and a strong focus on early disease diagnosis.

- Consumers and healthcare providers in the region highly value the diagnostic accuracy, non-invasiveness, and efficiency offered by ECG devices for various cardiac conditions.

- This widespread adoption is further supported by a technologically advanced population, significant investments in medical research and development, and the growing preference for remote patient monitoring and telehealth solutions that integrate ECG capabilities, establishing ECG as an indispensable tool in both clinical and homecare settings.

U.S. Diagnostic Electrocardiograph (ECG) Market Insight

The U.S. Diagnostic Electrocardiograph (ECG) Market captured the largest revenue share of 36.01% within North America in 2025. This is fueled by the significant burden of cardiovascular diseases, a large geriatric population, and extensive healthcare spending. Healthcare providers are increasingly prioritizing the enhancement of cardiac care through advanced diagnostic tools and remote monitoring systems. The growing preference for non-invasive diagnostic procedures, combined with robust demand for technologically advanced ECG devices and integration with electronic health records, further propels the Diagnostic Electrocardiograph (ECG) industry. Moreover, the increasing integration of telemedicine platforms and wearable ECG devices is significantly contributing to the market's expansion, enabling remote cardiac monitoring and timely interventions.

Canada Diagnostic Electrocardiograph (ECG) Market Insight

The Canada Diagnostic Electrocardiograph (ECG) Market is projected to expand at a substantial CAGR throughout the forecast period. This is primarily driven by a rising aging population, increasing awareness of cardiovascular health, and government initiatives aimed at improving chronic disease management. The focus on accessible healthcare, coupled with the demand for cost-effective and accurate cardiac diagnostics, is fostering the adoption of ECG devices across various clinical settings and for home use. Canadian consumers are also drawn to the benefits of early diagnosis and personalized cardiac care. The region is experiencing significant growth across hospital, clinic, and community healthcare applications, with ECG devices being incorporated into both established medical practices and new patient care models.

Mexico Diagnostic Electrocardiograph (ECG) Market Insight

The Mexico Diagnostic Electrocardiograph (ECG) Market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by improving healthcare infrastructure, increasing healthcare expenditure, and a rising prevalence of cardiovascular risk factors. Additionally, growing awareness regarding heart health and the importance of preventive diagnostics are encouraging both healthcare providers and individuals to utilize ECG solutions. Mexico’s improving access to medical technologies, alongside its expanding healthcare services, is expected to continue to stimulate market growth.

Diagnostic Electrocardiograph (ECG) Market Share

The Diagnostic Electrocardiograph (ECG) industry is primarily led by well-established companies, including:

- Philips (Netherlands)

- GE Healthcare (U.S.)

- NIHON KOHDEN (Japan)

- Fukuda Denshi (Japan)

- Mortara Instrument (U.S.)

- Spacelabs Healthcare (U.S.)

- Schiller AG (Switzerland)

- BioTelemetry (U.S.)

- Welch Allyn (U.S.)

- Suzuken (Japan)

- EDAN Instruments (China)

- Mindray Medical (China)

- Innomed (Hungary)

- Ambu A/S (Denmark)

Latest Developments in North America Diagnostic Electrocardiograph (ECG) Market

- In March 2025, GE HealthCare announced the U.S. launch of its MAC IQ ECG system at the American College of Cardiology (ACC) 2025 conference. The system features advanced AI-driven analysis tools for early detection of subtle cardiac abnormalities and integrates cloud connectivity for seamless data sharing. This underscores the company's dedication to delivering innovative, reliable diagnostic solutions tailored to the evolving needs of the healthcare market.

- In February 2025, Philips advanced its remote cardiac monitoring solutions through its BioTel Heart division, enhancing Mobile Cardiac Telemetry (MCOT) devices with improved algorithms for arrhythmia detection and treatment. This advancement highlights Philips' commitment to developing cutting-edge technologies that safeguard vulnerable spaces and offer greater protection and peace of mind for patients and healthcare providers.

- In November 2024, Hill-Rom's Welch Allyn CP 300 ECG system was updated with a new user interface and better data management capabilities. It also offers EMR connectivity and an intuitive touchscreen for primary care clinics and emergency departments. This project highlights the increasing significance of smart technology in urban safety, contributing to the development of safer, smarter communities.

- In October 2024, BPL Medical Technologies launched the Cardiart GenX3, a 3-channel ECG machine featuring the Glasgow ECG Interpretation algorithm. It's designed for use in clinics and hospitals, offering real-time data transfer capabilities. This collaboration is designed to enhance diagnostic efficiency and streamline accessibility for healthcare professionals, facilitating more efficient and accurate cardiac assessments.

- In January 2021, BioTelemetry, Inc., a prominent provider of remote cardiac diagnosis and monitoring systems in the United States, was acquired by Koninklijke Philips N.V. This strategic acquisition enhances Philips' portfolio of patient care management solutions, offering healthcare providers enhanced convenience and control while ensuring robust diagnostic capabilities.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.