North America Electronic Drug Delivery Systems Market

Market Size in USD Billion

USD

4.52 Billion

USD

8.94 Billion

2024

2032

USD

4.52 Billion

USD

8.94 Billion

2024

2032

| 2025 - 2032 | |

| USD 4.52 Billion | |

| USD 8.94 Billion | |

| % | |

|

North America Electronic Drug Delivery Systems Market Size

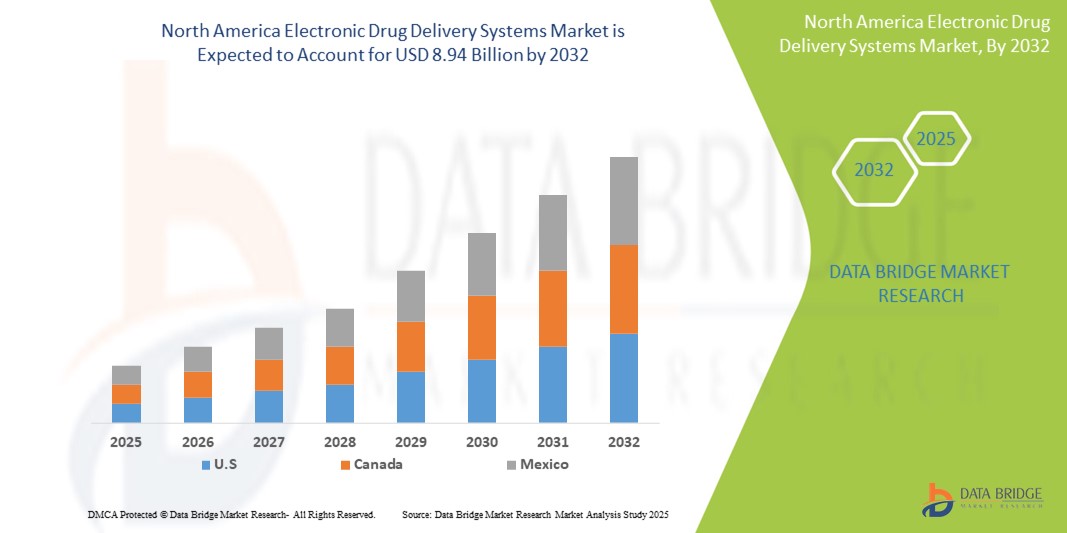

- The North America electronic drug delivery systems market size was valued at USD 4.52 billion in 2024 and is expected to reach USD 8.94 billion by 2032, at a CAGR of 8.90% during the forecast period

- The market growth is largely fueled by the increasing prevalence of chronic diseases and the rising shift toward self-administration of drugs, supported by advancements in digital health technologies and connected medical devices

- Furthermore, growing patient demand for convenient, precise, and technology-enabled drug delivery options is positioning electronic drug delivery systems as a critical component of modern healthcare. These converging factors are accelerating adoption across hospitals, homecare, and specialty clinics, thereby significantly boosting the industry’s growth

North America Electronic Drug Delivery Systems Market Analysis

- Electronic drug delivery systems, encompassing connected inhalers, auto-injectors, infusion pumps, and wearable devices, are increasingly integral to modern healthcare for precise dosing, enhanced patient adherence, and seamless integration with digital health platforms across hospital and homecare settings

- The escalating demand for electronic drug delivery systems is primarily driven by the rising prevalence of chronic diseases, growing preference for self-administration, and technological advancements in connected and smart drug delivery solutions

- U.S. dominated the North American electronic drug delivery systems market with the largest revenue share of 82.6% in 2024, supported by advanced healthcare infrastructure, strong adoption of innovative therapies, and the presence of leading medical device manufacturers

- Canada is expected to be the fastest-growing country in the North American electronic drug delivery systems market during the forecast period due to increased healthcare digitalization and growing adoption of home-based self-administration therapies

- The wearable infusion pumps segment dominated the North American electronic drug delivery systems market with a market share of 40.84% in 2024, attributed to their widespread use in diabetes management and other chronic conditions. These pumps offer continuous drug delivery, enhancing patient compliance and treatment efficacy

Report Scope and North America Electronic Drug Delivery Systems Market Segmentation

|

Attributes |

North America Electronic Drug Delivery Systems Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

North America Electronic Drug Delivery Systems Market Trends

Integration with Digital Health and Connected Platforms

- A significant and accelerating trend in the North America electronic drug delivery systems market is the deepening integration with digital health platforms, mobile apps, and cloud-based monitoring tools, enhancing patient adherence and remote treatment oversight

- For Instance, connected inhalers such as Propeller Health and digital auto-injectors such as Enable Injections integrate with apps to track dosing schedules and provide real-time adherence feedback to patients and healthcare providers

- Smart connectivity in these devices enables features such as automated dose reminders, adherence analytics, and predictive alerts for missed doses, helping optimize treatment plans and reduce errors in chronic disease management

- The seamless integration of electronic drug delivery systems with telehealth platforms and electronic health records allows healthcare providers to monitor multiple patients remotely, adjust therapies based on real-time data, and provide personalized interventions efficiently

- This trend towards more connected, data-driven, and patient-centric drug delivery solutions is fundamentally reshaping patient expectations and engagement in chronic disease management. Consequently, companies such as BD and Ypsomed are developing connected devices with real-time monitoring and app-based reporting features

- The demand for electronic drug delivery systems with integrated digital health solutions is growing rapidly across hospitals, homecare, and specialty clinics, as patients increasingly prioritize convenience, precision, and real-time feedback in their treatment plans

North America Electronic Drug Delivery Systems Market Dynamics

Driver

Rising Prevalence of Chronic Diseases and Self-Administration Preference

- The increasing prevalence of chronic diseases such as diabetes, asthma, and autoimmune disorders, coupled with a growing preference for self-administered therapies, is a major driver for the heightened adoption of electronic drug delivery systems

- For Instance, in March 2024, Enable Injections launched an IoT-enabled auto-injector platform designed for at-home biologic therapy, supporting remote monitoring and adherence tracking, reinforcing market growth in the U.S.

- As patients seek more convenient and reliable treatment options outside hospitals, electronic drug delivery systems provide precise dosing, real-time alerts, and remote monitoring, offering a compelling advantage over traditional drug administration methods

- Furthermore, the rising adoption of connected healthcare devices and telehealth services is increasing the demand for electronic drug delivery systems that integrate seamlessly into broader patient management ecosystems

- The convenience of wearable infusion pumps, smart inhalers, and connected auto-injectors, combined with real-time monitoring apps, is propelling adoption in hospitals, homecare, and specialty clinics. Trends toward patient-centered care models and the availability of user-friendly devices further drive market growth

Restraint/Challenge

Device Cost and Regulatory Compliance Hurdles

- High development costs, complex regulatory requirements, and cybersecurity concerns related to connected drug delivery systems pose significant challenges to broader adoption in North America

- For Instance, reports of vulnerabilities in IoT-enabled auto-injectors and smart inhalers have made some healthcare providers and patients hesitant to adopt fully connected systems due to data privacy and safety concerns

- Addressing these concerns through secure authentication, encrypted data transmission, and regulatory compliance is crucial for building trust among patients and healthcare institutions. Companies such as BD and Ypsomed emphasize cybersecurity features and FDA compliance in their marketing

- In addition, the relatively high price of advanced electronic drug delivery systems compared to conventional devices can limit adoption among price-sensitive patients and smaller clinics, even though basic connected devices are gradually becoming more affordable

- While costs are decreasing over time, the perceived premium for connected and smart drug delivery solutions can still hinder adoption, particularly among patients with less awareness of the benefits

- Overcoming these challenges through enhanced device security, regulatory alignment, patient education, and cost-effective solutions will be vital for sustained market growth in North America

North America Electronic Drug Delivery Systems Market Scope

The market is segmented on the basis of type, component, connectivity, system type, application, and end user.

- By Type

On the basis of type, the North America electronic drug delivery systems market is segmented into electronic infusion pumps, wearable infusion pumps, electronic injection pens, inhalers, electronic auto-injectors, electronic inhalers, electronic capsules, and others. The wearable infusion pumps segment dominated the market with the largest revenue share of 40.84% in 2024, driven by their widespread adoption in diabetes management and other chronic disease therapies. Patients and caregivers prioritize wearable pumps for continuous and precise drug delivery, which enhances treatment adherence and quality of life. These devices are favored due to their portability, discreet design, and integration with mobile apps for remote monitoring. The segment benefits from increasing awareness of self-administered therapies and growing healthcare digitalization across homecare settings. In addition, wearable pumps are compatible with advanced drug formulations, such as insulin analogs and biologics, which further fuels adoption. Their integration with telehealth systems and cloud-based monitoring platforms also provides healthcare providers with actionable real-time data to optimize patient care.

The electronic auto-injectors segment is anticipated to witness the fastest growth rate of 22.1% from 2025 to 2032, driven by rising demand for biologic therapies and self-administration in chronic diseases such as rheumatoid arthritis, multiple sclerosis, and immunodeficiency disorders. Auto-injectors are appreciated for their ease of use, reducing dosing errors and enhancing patient confidence. Their compact design and pre-filled dosing capabilities make them suitable for homecare, outpatient, and hospital settings. Increasing collaborations between pharmaceutical companies and medtech innovators are expanding the availability of connected auto-injectors with smart features such as dose reminders and Bluetooth monitoring. Furthermore, growing regulatory approvals for patient-friendly auto-injectors in North America are accelerating adoption. The segment also benefits from advancements in ergonomics, safety mechanisms, and integration with smartphone apps for adherence tracking, enhancing overall patient engagement.

- By Component

On the basis of component, the market is segmented into sensors, wireless communicators and antennas, micro pumps and flow regulators, drug reservoirs, microcontrollers, and others. The sensors segment dominated the market with a share of 36.5% in 2024, owing to their critical role in ensuring accurate dosing, flow monitoring, and patient safety. Sensors provide real-time feedback on drug delivery performance and allow automatic adjustment in infusion or injection rates. Their integration with connected platforms facilitates remote monitoring, early detection of malfunctions, and enhanced treatment efficacy. Healthcare providers and patients increasingly rely on sensors for adherence tracking, automated alerts, and preventive interventions. Advanced sensors are being developed to support complex drug formulations, including biologics and high-viscosity solutions. Continuous improvements in miniaturization and reliability of sensors further strengthen their dominance in electronic drug delivery devices.

The wireless communicator and antenna segment is expected to witness the fastest CAGR of 21.8% from 2025 to 2032, fueled by the increasing demand for connected drug delivery systems. Wireless communication enables seamless data transfer to mobile apps, cloud servers, and healthcare provider dashboards. Devices with BLE, Wi-Fi, or NB-IoT capabilities allow remote monitoring, patient adherence tracking, and personalized dosing notifications. Growing telehealth adoption and remote patient management in North America significantly drive the integration of wireless modules in modern drug delivery systems. The segment also benefits from technological advancements in low-power communication and secure data transmission protocols. Pharmaceutical companies are increasingly collaborating with medtech providers to embed wireless communication for connected therapy solutions, further accelerating growth.

- By Connectivity

On the basis of connectivity, the market is segmented into Bluetooth Low Energy (BLE), Wi-Fi, Ethernet, NB-IoT, and others. The BLE segment dominated the market with a share of 38.2% in 2024, due to its low power consumption, reliable short-range connectivity, and seamless smartphone integration. BLE-enabled devices allow patients to track dosing, receive adherence alerts, and sync with mobile health applications without frequent recharging. Healthcare providers use BLE connectivity for remote monitoring and real-time adherence management. Its compatibility with wearable devices, auto-injectors, and smart infusion pumps makes it the preferred choice for portable drug delivery systems. BLE also ensures secure peer-to-peer communication and minimizes interference, which is critical for clinical applications. The segment is further supported by the growing adoption of mobile-based digital health solutions and patient-centric therapy approaches.

The Wi-Fi segment is expected to witness the fastest growth rate of 23.5% from 2025 to 2032, driven by its capability to support continuous real-time data transfer and integration with cloud-based telehealth platforms. Wi-Fi-enabled devices provide automatic updates, remote diagnostics, and enhanced device management for healthcare providers and caregivers. This connectivity facilitates predictive analytics, adherence monitoring, and improved patient engagement. Growth in hospital-based connected therapy solutions, combined with increasing homecare adoption, fuels Wi-Fi connectivity integration. The segment benefits from higher bandwidth requirements for complex therapies and multi-parameter monitoring. In addition, Wi-Fi allows seamless interoperability with other digital health platforms, contributing to enhanced patient outcomes and treatment optimization.

- By System Type

On the basis of system type, the market is segmented into battery-powered systems and rechargeable systems. The battery-powered systems segment dominated with a market share of 42.1% in 2024, due to ease of use, minimal maintenance, and widespread availability in wearable infusion pumps and auto-injectors. Battery-powered systems provide uninterrupted therapy delivery and are convenient for homecare patients who may not have access to frequent recharging. Their reliability and portability make them highly suitable for chronic disease management. The segment is further strengthened by the growing adoption of disposable and pre-filled devices that rely on battery power for single or short-term use. Healthcare providers prefer battery-powered systems for their simplicity, lower operational complexity, and consistent performance in hospital and homecare settings. Continuous innovations in battery efficiency and longevity also reinforce their market dominance.

The rechargeable systems segment is expected to witness the fastest growth rate of 20.6% from 2025 to 2032, fueled by adoption in wearable infusion pumps, connected auto-injectors, and advanced drug delivery devices requiring higher energy capacity. Rechargeable systems support devices with integrated sensors, wireless communication modules, and continuous infusion functionality. The segment benefits from patient demand for sustainable and eco-friendly therapy solutions. Technological advances in fast-charging batteries and energy-efficient electronics drive adoption. Hospitals and specialty clinics increasingly adopt rechargeable systems to reduce long-term operational costs. Rechargeable systems also enable multi-functional devices with enhanced features such as real-time monitoring and adherence tracking, boosting market growth.

- By Application

On the basis of application, the market is segmented into diabetes, asthma and COPD, multiple sclerosis, growth hormone therapy, immunodeficiency disease, cardiovascular disease, thalassemia, and others. The diabetes segment dominated the market with a share of 44.3% in 2024, driven by high prevalence rates in the U.S. and Canada and growing adoption of insulin pumps and connected glucose monitoring systems. Patients and caregivers prioritize electronic drug delivery systems for precise insulin dosing, improved glycemic control, and reduced risk of complications. Integration with mobile apps and cloud-based monitoring enhances adherence and remote therapy management. Rising awareness of patient-centered care and home-based diabetes management strengthens the dominance of this segment. Technological advancements in insulin pumps and wearable infusion systems provide continuous, personalized drug delivery. Diabetes-focused device manufacturers continue to innovate, offering devices with connectivity, AI-based dosing, and alerts to optimize therapy outcomes.

The asthma and COPD segment is expected to witness the fastest CAGR of 21.4% from 2025 to 2032, driven by the increasing use of smart inhalers with connected monitoring features. These devices allow patients to track inhaler usage, improve adherence, and transmit real-time data to healthcare providers. Rising prevalence of respiratory diseases and growing awareness of digital therapy solutions support rapid adoption. Integration with telehealth platforms enables remote disease management and personalized therapy adjustment. Technological advancements in sensors, connectivity, and drug formulation compatibility drive the segment growth. Patient preference for self-administration, convenience, and adherence optimization fuels adoption in homecare and outpatient settings.

- By End User

On the basis of end user, the market is segmented into home healthcare, hospitals, clinics, ambulatory centers, and others. The home healthcare segment dominated the market with a revenue share of 39.7% in 2024, due to increasing preference for self-administration of therapies in chronic disease management. Patients benefit from wearable infusion pumps, auto-injectors, and connected inhalers that provide real-time adherence feedback and remote monitoring by healthcare providers. The segment is strengthened by rising chronic disease prevalence, telehealth integration, and government initiatives promoting home-based care. Homecare adoption reduces hospital visits, enhances patient comfort, and lowers healthcare costs. Connected devices ensure continuous data collection for caregivers and clinicians, supporting better treatment outcomes. Home healthcare continues to be favored for convenience, patient independence, and accessibility of digital therapy solutions.

The hospitals segment is expected to witness the fastest CAGR of 22.0% from 2025 to 2032, driven by high adoption of electronic infusion pumps, connected auto-injectors, and wearable devices for in-patient and outpatient therapy administration. Hospitals benefit from integrated digital drug delivery systems for remote monitoring, automated dosing, and workflow optimization. Growing investments in hospital infrastructure, chronic disease management programs, and adoption of connected healthcare technologies support rapid growth. The segment also benefits from increasing use of high-value therapies requiring precise and programmable drug delivery. Hospitals prioritize devices with advanced safety features, sensor integration, and connectivity, enhancing treatment efficiency and patient outcomes.

North America Electronic Drug Delivery Systems Market Regional Analysis

- U.S. dominated the North American electronic drug delivery systems market with the largest revenue share of 82.6% in 2024, supported by advanced healthcare infrastructure, strong adoption of innovative therapies, and the presence of leading medical device manufacturers

- Patients and healthcare providers in the region highly value the convenience, accuracy, and remote monitoring capabilities offered by electronic drug delivery systems, including wearable infusion pumps, auto-injectors, and smart inhalers

- This widespread adoption is further supported by advanced healthcare infrastructure, strong presence of leading medical device manufacturers, and growing integration of digital health platforms, establishing electronic drug delivery systems as a preferred solution across homecare, hospitals, and specialty clinics

U.S. Electronic Drug Delivery Systems Market Insight

The U.S. electronic drug delivery systems market captured the largest revenue share in 2024 within North America, driven by the rising prevalence of chronic diseases such as diabetes, asthma, and autoimmune disorders. Patients and healthcare providers are increasingly prioritizing self-administered, connected therapy solutions that enhance dosing accuracy, adherence, and remote monitoring. The growing adoption of wearable infusion pumps, smart inhalers, and auto-injectors, combined with integration into mobile health apps and cloud-based platforms, further propels market growth. In addition, initiatives supporting homecare, telehealth integration, and patient-centric care models are significantly contributing to the expansion of the U.S. market.

Canada Electronic Drug Delivery Systems Market Insight

The Canada electronic drug delivery systems market is projected to expand at a substantial CAGR during the forecast period, primarily driven by rising chronic disease prevalence and government initiatives promoting digital health adoption. Increased awareness among patients and healthcare providers regarding the benefits of connected drug delivery devices is fostering market penetration. Home-based care solutions and remote monitoring platforms are supporting adoption in residential and outpatient settings. Moreover, Canada’s well-established healthcare infrastructure and emphasis on patient-centered therapy are encouraging uptake across hospitals, clinics, and homecare programs.

Mexico Electronic Drug Delivery Systems Market Insight

The Mexico electronic drug delivery systems market is expected to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of chronic disease management, expanding healthcare infrastructure, and growing adoption of connected therapy solutions. Patients are increasingly seeking self-administered drug delivery options such as wearable infusion pumps, auto-injectors, and smart inhalers. Government initiatives to improve healthcare accessibility and telehealth integration are supporting market growth. In addition, rising private healthcare investments and partnerships with international device manufacturers are enhancing the availability of advanced drug delivery systems. The growing urban population and increasing disposable income in Mexico further propel adoption in both homecare and hospital settings.

North America Electronic Drug Delivery Systems Market Share

The North America electronic drug delivery systems industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Insulet Corporation (U.S.)

- BD (U.S.)

- AbbVie Inc. (U.S.)

- Eisai Co., Ltd. (U.S.)

- Dexcom, Inc. (U.S.)

- Novo Nordisk A/S (U.S.)

- Sanofi (U.S.)

- Johnson & Johnson and its affiliates (U.S.)

- F. Hoffmann-La Roche Ltd (U.S.)

- Abbott (U.S.)

- Bayer (U.S.)

- GSK plc (U.S.)

- Merck & Co., Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Lilly USA, LLC (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- AstraZeneca (U.S.)

- Gilead Sciences, Inc. (U.S.)

- Amgen Inc. (U.S.)

What are the Recent Developments in North America Electronic Drug Delivery Systems Market?

- In July 2025, Becton Dickinson (BD) announced its first pharma-sponsored clinical trial using the BD Libertas Wearable Injector. This innovative, prefilled, patient-ready-to-use drug delivery system is designed to enable the delivery of complex biologics via subcutaneous injection. The trial aims to evaluate the device's performance in real-world settings

- In May 2025, Medtronic announced plans to spin off its diabetes division into a standalone company. The new entity, which will be headquartered in Northridge, California, is expected to employ around 8,000 people. This move is part of Medtronic's long-term restructuring efforts to focus on its more lucrative businesses, especially heart devices

- In April 2025, Dexcom announced that its G7 15-Day continuous glucose monitoring (CGM) system received FDA clearance. This device is designed for individuals aged 18 and older with diabetes and is expected to launch in the U.S. in the second half of 2025. It is the company's most accurate and longest-lasting wearable CGM system

- In April 2025, Medtronic announced the submission of a 510(k) application to the U.S. Food and Drug Administration (FDA) for an interoperable insulin pump designed to work seamlessly with Abbott's continuous glucose monitoring (CGM) system. This collaboration aims to enhance diabetes management by integrating Abbott's CGM sensor with Medtronic's insulin delivery devices, enabling automatic insulin adjustments to maintain glucose levels within the target range.

- In August 2024, Insulet announced that its Omnipod 5 Automated Insulin Delivery System received FDA clearance for use in individuals aged 18 and older with type 2 diabetes. This made Omnipod 5 the first and only automated insulin delivery system FDA-cleared for both type 1 and type 2 diabetes management

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.