North America Flare Monitoring Market

Market Size in USD Million

USD

450.17 Million

USD

871.00 Million

2025

2033

USD

450.17 Million

USD

871.00 Million

2025

2033

| 2026 - 2033 | |

| USD 450.17 Million | |

| USD 871.00 Million | |

| % | |

|

North America Flare Monitoring Market Size

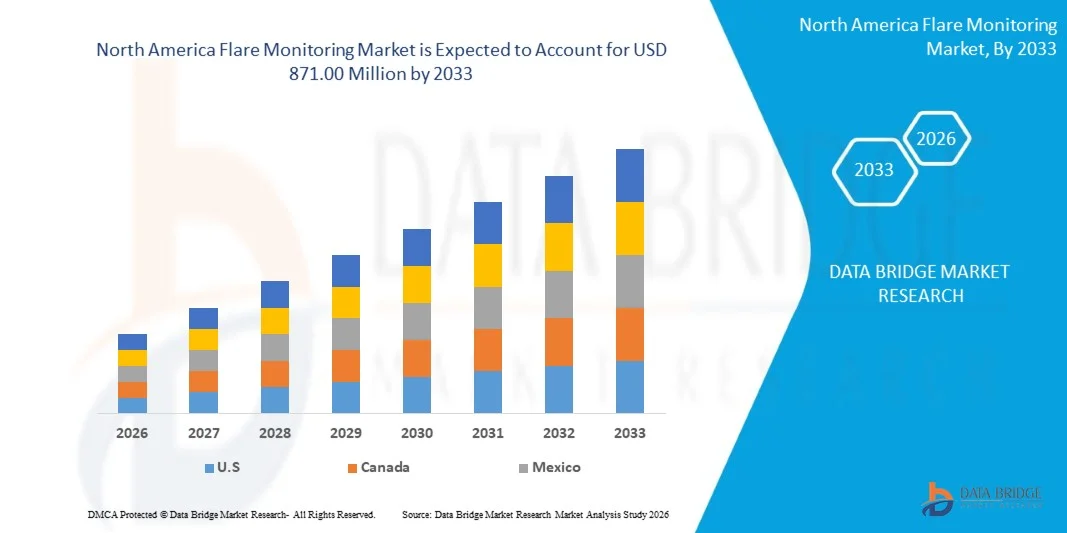

- The North America flare monitoring market size was valued at USD 450.17 million in 2025 and is expected to reach USD 871.00 million by 2033, at a CAGR of 8.60% during the forecast period

- The market growth is largely fuelled by the increasing enforcement of environmental regulations and emission control standards across oil & gas operations

- Rising adoption of advanced monitoring technologies such as infrared cameras and real-time data analytics is further supporting market expansion

North America Flare Monitoring Market Analysis

- Growing focus on reducing greenhouse gas emissions and improving operational efficiency in upstream and downstream facilities

- Increasing investments in digital monitoring solutions and automation across refineries and petrochemical plants

- U.S. dominated the North America flare monitoring market with the largest revenue share in 2025, driven by stringent environmental regulations and strong demand for emission monitoring across oil and gas operations

- Canada is expected to witness the highest compound annual growth rate (CAGR) in the North America flare monitoring market due to increasing investments in emission control technologies, rising focus on sustainability, and expanding adoption of advanced flare monitoring systems across oil sands and offshore operations

- The gas analyzer segment held the largest market revenue share in 2025 driven by its widespread use in real-time emission measurement and continuous monitoring across oil and gas facilities. Gas analyzers provide accurate detection of flared gases and are widely adopted due to their reliability, efficiency, and ability to support regulatory compliance

Report Scope and North America Flare Monitoring Market Segmentation

|

Attributes |

North America Flare Monitoring Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

• Teledyne Technologies Incorporated (U.S.) |

|

Market Opportunities |

• Increasing Adoption Of Real Time Emission Monitoring Technologies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

North America Flare Monitoring Market Trends

“Increasing Focus on Emission Reduction and Regulatory Compliance”

• The growing emphasis on environmental protection and emission control is significantly shaping the North America flare monitoring market, as regulatory authorities enforce stringent standards on industrial emissions. Flare monitoring systems are gaining traction due to their ability to provide real-time data, ensure compliance, and improve operational transparency across oil and gas facilities. This trend is encouraging companies to adopt advanced monitoring technologies to minimize environmental impact and avoid regulatory penalties

• Rising awareness regarding greenhouse gas emissions and their environmental impact has accelerated the adoption of flare monitoring systems across upstream, midstream, and downstream operations. Energy companies are increasingly investing in advanced infrared cameras, gas analyzers, and automated monitoring solutions to enhance efficiency and ensure accurate emission tracking. This is further driving demand for integrated and intelligent flare monitoring platforms

• Technological advancements are influencing purchasing decisions, with companies focusing on AI-based analytics, IoT integration, and cloud-enabled monitoring systems. These technologies help improve predictive maintenance, optimize flare performance, and reduce operational downtime. Manufacturers are also emphasizing system reliability and scalability to meet evolving industrial requirements

• For instance, in 2024, major oil and gas operators in the U.S. and Canada expanded the deployment of real-time flare monitoring systems across refineries and production sites. These implementations were aimed at improving emission visibility, ensuring regulatory compliance, and enhancing operational efficiency through automated data collection and reporting systems

• While demand for flare monitoring systems is rising, sustained market growth depends on continuous technological innovation, cost optimization, and the ability to integrate monitoring solutions with existing industrial infrastructure. Companies are focusing on enhancing system accuracy, scalability, and data analytics capabilities to support long-term adoption

North America Flare Monitoring Market Dynamics

Driver

“Stringent Environmental Regulations and Increasing Emission Monitoring Requirements”

• Increasing regulatory pressure to control industrial emissions is a major driver for the flare monitoring market in North America. Governments and environmental agencies are mandating the use of advanced monitoring systems to ensure compliance with emission standards, pushing industries to adopt reliable and accurate flare monitoring solutions

• Expanding oil and gas exploration and production activities are further influencing market growth. Flare monitoring systems play a critical role in ensuring safe operations, reducing gas flaring, and improving efficiency across production and refining processes. This is driving their adoption across both existing and new facilities

• Energy companies are actively investing in advanced monitoring technologies and digital solutions to enhance operational efficiency and meet sustainability goals. These investments are supported by increasing focus on reducing carbon footprint and improving environmental performance, leading to wider adoption of smart monitoring systems

• For instance, in 2023, leading energy companies in the U.S. and Canada increased investments in infrared-based flare monitoring and automated reporting systems to comply with stricter emission regulations. These initiatives helped improve transparency, reduce environmental impact, and strengthen regulatory compliance across operations

• Although regulatory support is driving growth, continued expansion depends on technological advancements, cost-effective solutions, and efficient integration with legacy systems to ensure widespread adoption across industries

Restraint/Challenge

“High Implementation Costs and Technical Complexity”

• The high initial cost of installing advanced flare monitoring systems remains a significant challenge, limiting adoption among smaller operators. Investment in specialized equipment, sensors, and integration systems increases overall project costs, making it difficult for cost-sensitive companies to adopt these solutions

• Technical complexity associated with system integration and maintenance also poses a barrier to market growth. Flare monitoring systems require skilled personnel for installation, calibration, and operation, which can increase operational challenges and costs

• Data management and cybersecurity concerns further impact adoption, as real-time monitoring systems generate large volumes of sensitive operational data. Ensuring secure data transmission and storage is critical for maintaining system integrity and regulatory compliance

• For instance, in 2024, several mid-sized oil and gas operators in North America reported delays in adopting advanced flare monitoring technologies due to high costs and challenges in integrating new systems with existing infrastructure. These factors also affected scalability and limited widespread deployment across facilities

• Addressing these challenges will require cost optimization, development of user-friendly solutions, and increased focus on training and technical support. Strengthening cybersecurity measures and improving system integration capabilities will be essential for long-term market growth and adoption

North America Flare Monitoring Market Scope

The market is segmented on the basis of mounting method and industry.

• By Mounting Method

On the basis of mounting method, the flare monitoring market is segmented into in process-mass spectrometers, gas chromatographs, gas analyzer, remote-IR imagers, and MSIR imagers. The gas analyzer segment held the largest market revenue share in 2025 driven by its widespread use in real-time emission measurement and continuous monitoring across oil and gas facilities. Gas analyzers provide accurate detection of flared gases and are widely adopted due to their reliability, efficiency, and ability to support regulatory compliance.

The remote-IR imagers segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for non-contact monitoring solutions and advanced infrared imaging capabilities. These systems enable real-time visualization of flare emissions and are gaining popularity for their ability to enhance safety, reduce manual intervention, and improve monitoring accuracy.

• By Industry

On the basis of industry, the flare monitoring market is segmented into onshore oil and gas production sites, refineries, petrochemical, landfills, offshore, and metal and steel production. The onshore oil and gas production sites segment held the largest market revenue share in 2025 driven by the extensive deployment of flare monitoring systems across upstream operations to ensure emission control and operational safety. These sites require continuous monitoring solutions to comply with environmental regulations and optimize production efficiency.

The offshore segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing offshore exploration activities and rising need for advanced monitoring systems in remote and complex environments. Offshore facilities are adopting sophisticated flare monitoring technologies to enhance safety, ensure compliance, and maintain efficient operations under challenging conditions.

North America Flare Monitoring Market Regional Analysis

• The U.S. dominated the North America flare monitoring market with the largest revenue share in 2025, driven by stringent environmental regulations and strong demand for emission monitoring across oil and gas operations

• Industries in the country highly prioritize real-time monitoring, regulatory compliance, and operational safety, leading to increased adoption of advanced flare monitoring systems such as infrared imaging and gas analyzers

• This widespread adoption is further supported by a well-established oil and gas infrastructure, high technological adoption, and increasing focus on reducing greenhouse gas emissions, making flare monitoring a critical component across upstream and downstream facilities

Canada Flare Monitoring Market Insight

The Canada flare monitoring market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing focus on environmental sustainability and rising investments in advanced emission monitoring technologies. The country is rapidly adopting flare monitoring systems across oil sands, refineries, and offshore facilities to improve operational efficiency and ensure compliance with evolving environmental standards. Growing deployment of infrared imaging systems and automated monitoring solutions, along with government initiatives promoting emission reduction, is further accelerating market growth. Moreover, the integration of smart monitoring technologies and expansion of energy infrastructure are significantly contributing to the country’s rapid market development.

North America Flare Monitoring Market Share

The North America flare monitoring industry is primarily led by well-established companies, including:

• Teledyne Technologies Incorporated (U.S.)

• FLIR Systems (U.S.)

• Emerson Electric Co. (U.S.)

• Honeywell International Inc. (U.S.)

• General Electric (U.S.)

• Ametek Inc. (U.S.)

• Thermo Fisher Scientific (U.S.)

• Sierra Instruments (U.S.)

• MKS Instruments (U.S.)

• Envent Engineering Ltd. (Canada)

• ABB Measurement & Analytics (U.S.)

• Baker Hughes (U.S.)

• Rockwell Automation (U.S.)

• Perma-Pipe International Holdings (U.S.)

• Photon Control Inc. (Canada)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

North America Flare Monitoring Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its North America Flare Monitoring Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as North America Flare Monitoring Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.