North America Fluid Management Systems Market

Market Size in USD Billion

USD

4.03 Billion

USD

9.22 Billion

2024

2032

USD

4.03 Billion

USD

9.22 Billion

2024

2032

| 2025 - 2032 | |

| USD 4.03 Billion | |

| USD 9.22 Billion | |

| % | |

|

Fluid Management Systems Market Size

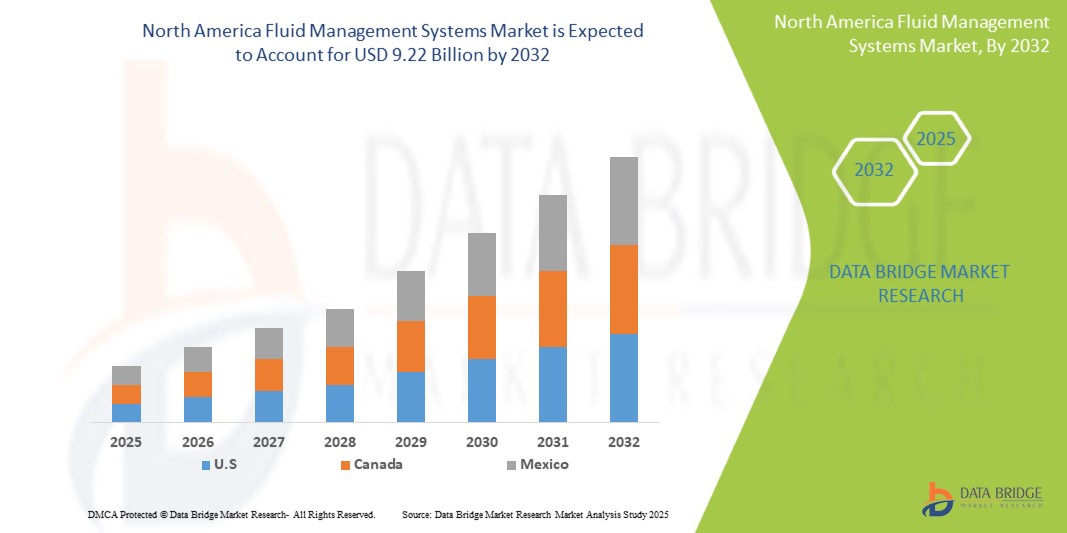

- The North America Fluid Management Systems market size was valued at USD 4.03 billion in 2024 and is expected to reach USD 9.22 billion by 2032, at a CAGR of 10.9% during the forecast period

- The market growth is largely fueled by the rising incidence of chronic illnesses, such as kidney failure, cardiovascular diseases, and gastrointestinal disorders, which necessitate ongoing surgical or interventional procedures involving fluid management.

- Furthermore, the increasing aging population in North America contributes to a higher patient volume requiring medical interventions. Technological advancements in fluid management systems, including improved precision, automation, and the development of disposable components, are driving market expansion. These converging factors are accelerating the uptake of fluid management solutions, thereby significantly boosting the industry's growth.

Fluid Management Systems Market Analysis

- Fluid Management Systems market encompasses a diverse range of medical devices and consumables designed to regulate and control fluids within the human body or at surgical sites. These systems are crucial for maintaining fluid balance, facilitating irrigation and suction during procedures, and managing fluid waste. Key components include dialyzers, insufflators, suction/evacuation and irrigation systems, and various consumables like tubing sets and catheters. Their application spans across numerous medical specialties, including urology, cardiology, gastroenterology, and in procedures like dialysis and minimally invasive surgeries. The market is driven by the increasing prevalence of chronic diseases, the growing adoption of minimally invasive techniques, and continuous technological advancements that enhance patient care and procedural efficiency.

- The escalating demand for fluid management systems is primarily fueled by the increasing number of minimally invasive surgical procedures, the rising focus on stringent infection control protocols in healthcare facilities, and the growing preference for safer and more efficient fluid handling during medical attention.

- The U.S. dominates the Fluid Management Systems market in North America with the largest revenue share of 81.45% in 2025, attributed to a well-developed healthcare infrastructure, rising number of surgical procedures, and early adoption of advanced fluid management technologies. High awareness regarding fluid balance in critical care and operating rooms, coupled with significant healthcare spending, reinforces the country’s leading position.

- The U.S. is expected to be the fastest-growing country in the North America Fluid Management Systems market during the forecast period, driven by the increasing incidence of chronic diseases such as kidney failure and cardiovascular conditions, along with the rising demand for minimally invasive surgeries where fluid regulation is critical. The presence of key players like Baxter, Stryker, and Fresenius also fuels innovation and accessibility.

- Standalone Fluid Management Systems are expected to dominate the North America Fluid Management Systems market with a market share of 46.9% in 2025, owing to their enhanced precision, integration capabilities with imaging systems, and strong utility across endoscopic, orthopedic, and gynecological procedures. Their widespread adoption in hospitals and ambulatory surgery centers is further bolstered by user-friendly interfaces and real-time fluid monitoring features.

Report Scope and Fluid Management Systems Market Segmentation

|

Attributes |

Fluid Management Systems Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Fluid Management Systems Market Trends

“Increasing adoption of minimally invasive surgical procedures”

- Growing Adoption of Minimally Invasive Surgeries and Disposable Components: A significant and accelerating trend in the North America fluid management systems market is the increasing adoption of minimally invasive surgical (MIS) procedures, which are highly dependent on precise fluid control. This trend is coupled with a notable shift towards the increased usage of disposable fluid management devices and components.

- For instance, MIS procedures, often performed with advanced robotic systems, require sophisticated fluid management systems for precise irrigation, suction, and clear visibility at surgical sites. The growing popularity of MIS, driven by benefits like quicker recovery and shorter hospital stays, directly fuels the demand for these systems.

- Simultaneously, there is a rising demand for disposable fluid management devices such as tubing sets, suction canisters, and catheters. This shift is primarily driven by increasing concerns about cross-contamination, the need to reduce sterilization costs, and stringent infection control requirements in healthcare facilities.

- Technological advancements are also a key trend, with companies innovating in areas like jetting highly viscous fluids to improve precision and versatility. The integration of IoT, machine learning, and cloud computing is enabling the development of predictive models for enhanced treatment outcomes.

- This trend towards more efficient, safer, and technologically integrated fluid management solutions is fundamentally reshaping surgical and patient care practices across North America.

Fluid Management Systems Market Dynamics

Driver

“Rising Incidence of Chronic Diseases and Minimally Invasive Procedures”

- The increasing prevalence of chronic illnesses, such as kidney failure, cardiovascular diseases, gastrointestinal diseases, and urological conditions, is a significant driver for the heightened demand for fluid management systems in North America. These conditions often necessitate ongoing surgical or interventional procedures that rely heavily on precise fluid control.

- For instance, the rising rate of urological diseases, including benign prostatic hyperplasia (BPH) and kidney stones, requires increased use of endoscopy in procedures like cystoscopy and transurethral resection, which in turn boosts the need for advanced fluid management systems.

- The growing number of minimally invasive surgical procedures being performed is a primary catalyst, as these techniques require specialized fluid management for optimal visibility and reduced blood loss.

- The increasing geriatric population in North America is more susceptible to these chronic conditions, further accelerating the demand for fluid management solutions.

- Additionally, stringent infection control protocols mandated by regulatory bodies encourage the adoption of advanced fluid management systems, including closed-loop systems and disposable components, to minimize cross-contamination risks monitoring

Restraint/Challenge

“High Costs and Supply Chain Disruptions”

- The high initial investment costs associated with advanced fluid management systems, coupled with potential disruptions in global supply chains, present significant challenges to widespread market adoption, particularly for smaller healthcare facilities and those with budget constraints.

- For instance, the capital expenditure for sophisticated fluid management equipment can be substantial. Healthcare providers may face increased costs if manufacturers pass on higher production expenses due to tariffs or trade conflicts, impacting purchasing decisions.

- Trade conflicts and tariffs can disrupt global supply chains, leading to delays in production, longer lead times, and scarcity of essential components (e.g., OEM parts, electronics), which can affect the upgrade or maintenance of existing equipment.

- Additionally, the need for skilled technicians for installation, operation, and maintenance of these complex systems adds to the operational burden. The temporary reduction in elective surgeries during events like the COVID-19 pandemic also highlighted vulnerabilities in market growth.

Fluid Management Systems Market Scope

The market is segmented on the basis product type, disposables and Accessories and Application and end user.

- By Product

On the basis of Product, the Fluid Management Systems market is into Integrated Fluid Management Systems and Standalone Fluid Management Systems. Standalone Fluid Management Systems dominate the market with the largest revenue share of 46.9% in 2025, driven by their adaptability across a wide range of minimally invasive surgical procedures such as endoscopy, urology, and gynecology. These systems are favored for their precision control, ease of integration with existing surgical equipment, and growing use in ambulatory surgical centers. Technological advancements such as digital flow regulation and user-friendly touchscreen interfaces are contributing to widespread adoption.

The Integrated Fluid Management Systems segment is anticipated to witness the fastest growth rate of 5.8% from 2025 to 2032, due to the increasing demand for unified platforms that combine irrigation, suction, and visualization functions. These systems streamline procedural workflow, reduce clutter in operating rooms, and enhance surgical safety—making them highly desirable in high-volume hospitals and tertiary care centers.

- By Disposables and Accessories

On the basis of application, the Fluid Management Systems market is segmented into Visualization Systems, Pressure Transducers, Valves, Connectors and Fittings, Catheters, Bloodlines, Tubing Sets, Pressure Monitoring Lines, Suction Canisters, Cannulas, and Others. The Tubing Sets held the largest market revenue share in 2025, owing to their indispensable role in maintaining fluid pathways during diagnostic and surgical procedures. These sets are vital for safe and sterile fluid delivery and drainage, and their use spans across multiple specialties including gastroenterology, urology, and cardiology. The segment benefits from high replacement rates and widespread use in single-use sterile applications.

The Visualization Systems is expected to witness the fastest CAGR from 2025 to 2032, driven by the increasing reliance on high-definition endoscopic visualization during fluid-intensive surgeries. Innovations in HD imaging, light management, and integration with fluid control modules are boosting demand across both inpatient and outpatient settings.

- By Applications

On the basis of application, the Fluid Management Systems market is segmented into Urology, Bronchoscopy, Arthroscopy, Cardiology, Neurology, Gastroenterology, Laparoscopy, Gynecology/Obstetrics, Otoscopy, Dentistry, Anesthesiology, and Others. The Urology segment driven by the high prevalence of kidney stones, prostate disorders, and bladder conditions requiring procedures like TURP and cystoscopy. Demand for advanced irrigation and suction systems in endourological surgeries is contributing to segment dominance.

The Laparoscopy segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by the growing adoption of minimally invasive surgeries for bariatric, gynecological, and gastrointestinal conditions. The need for precise fluid regulation and clear visualization in closed-body cavity procedures supports rising demand for laparoscopy-specific fluid management solutions.

- By End User

On the basis of end user, the Fluid Management Systems market is segmented into Hospitals, Ambulatory Surgical Centers (ASCs), Cosmetic Surgical Centers, and Others. The Hospitals segment is projected to dominate the market with the largest revenue share in 2025, driven by the high volume of complex surgical procedures requiring precise fluid control, such as urology, laparoscopy, and cardiology. Hospitals benefit from comprehensive infrastructure, integrated operating rooms, and higher budgets for advanced fluid management systems—both standalone and integrated. Additionally, hospitals are the primary settings for procedures involving critically ill patients and emergency cases where effective fluid balance is vital to clinical outcomes.

The Ambulatory Surgical Centers (ASCs) segment is expected to register the fastest CAGR from 2025 to 2032, owing to the rising demand for same-day surgeries and cost-effective healthcare delivery. ASCs are increasingly adopting compact, portable, and easy-to-operate fluid management systems to support minimally invasive procedures across specialties like arthroscopy, gynecology, and gastroenterology. The segment's growth is further supported by favorable reimbursement structures and the shift of elective procedures from hospitals to outpatient settings.

Fluid Management Systems Market Regional Analysis

- U.S. dominates the Fluid Management Systems market with the largest revenue share of 81.45% in 2025, driven by the increasing number of minimally invasive surgical procedures, advancements in surgical visualization, and a strong clinical preference for integrated and automated fluid control systems.

- The presence of a highly advanced healthcare infrastructure, along with the growing demand for precision and safety in surgeries such as urology, laparoscopy, and endoscopy, supports rapid adoption of fluid management technologies.

- Favorable reimbursement policies, coupled with rising investments in ambulatory surgical centers and outpatient facilities, contribute to expanded usage across a broad range of specialties. Major U.S.-based players such as Stryker, Baxter, and Zimmer Biomet continue to innovate and launch advanced fluid irrigation and suction systems integrated with high-definition imaging platforms.

- Furthermore, the increasing implementation of digital ORs (operating rooms) and growing preference for disposable fluid management accessories to reduce infection risk are supporting long-term market growth.

Canada Fluid Management Systems Market Insight

The Canada Fluid Management Systems market is projected to expand steadily throughout the forecast period, fueled by the increasing adoption of minimally invasive surgeries, national investments in digital health infrastructure, and the modernization of surgical environments in both public and private healthcare facilities. The Canadian healthcare system’s strong emphasis on infection control and patient safety is driving demand for high-quality fluid management accessories such as suction canisters, tubing sets, and disposable valves. Growing procedural volumes in urology, gynecology, and orthopedics, supported by improved hospital funding and surgical training programs, are boosting adoption. Additionally, collaborations with U.S.-based medical device companies help ensure access to cutting-edge systems. Health Canada’s robust regulatory framework ensures only highly effective and safe devices enter the market, which builds confidence among surgeons and procurement decision-makers alike.

Mexico Fluid Management Systems Market Insight

The Mexico Fluid Management Systems market is expected to grow at a notable CAGR during 2025–2032, supported by ongoing healthcare reforms, infrastructure development, and the increasing penetration of minimally invasive surgical procedures in both public and private hospitals. Government-led health campaigns, medical tourism growth, and rising surgical volumes—particularly in laparoscopy, endoscopy, and gynecology—are key factors driving market expansion. While access to advanced systems remains more concentrated in urban and private healthcare centers, public-private partnerships and foreign direct investments in the medical device sector are helping improve availability across broader regions. Training initiatives for healthcare professionals, especially in fluid-controlled procedures and infection prevention protocols, are further accelerating demand. Adoption of cost-effective standalone systems and reusable accessories is common, though disposable product usage is gradually increasing with enhanced awareness of patient safety standards.

Fluid Management Systems Market Share

The Fluid Management Systems industry is primarily led by well-established companies, including:

- Cardinal Health Inc. (U.S.)

- Johnson & Johnson Services Inc. (U.S.)

- Medtronic plc (Ireland)

- Fresenius Medical Care AG & Co. KGaA (Germany

- Becton Dickinson and Company (U.S.)

- Stryker Corporation (U.S.)

- Baxter International Inc. (U.S.)

- Ecolab Inc. (U.S.)

- B. Braun Melsungen AG (Germany)

- Zimmer Biomet Holdings Inc. (U.S.)

- Olympus Corporation (Japan)

- Hologic Inc. (U.S.)

- Arthrex Inc. (U.S.)

- Merit Medical Systems Inc. (U.S.)

- CONMED Corporation (U.S.)

- Richard Wolf GmbH (Germany)

- AngioDynamics Inc. (U.S.)

- Smith & Nephew (U.K.)

- Smiths Medical Inc. (U.S.)

- Teleflex Incorporated (U.S.)

- C.R. Bard (U.S.)

- 3M Company (U.S)

Latest Developments in North America Fluid Management Systems Market

- In November 2024, Megnajet Ltd. launched the OmniFlo fluid management system, designed to handle challenges of jetting highly viscous fluids, ensuring reliable fluid conditioning across various applications.

- In August 2023, the U.S. Food and Drug Administration approved Fresenius dialysis software to guide patients and caregivers through at-home sessions, enhancing fluid management in home dialysis.

- In December 2020, Cantel Medical Corp and Censis Technologies announced a new long-term partnership to combine Cantel's infection prevention endoscope reprocessing workflow portfolio with surgical asset management and instrument tracking solutions from Censis.

- In November 2018, the CrystalView Pro Irrigation System received approval for marketing the product by the FDA.

- In October 2018, the ENDOMAT SELECT hysteroscopic fluid management pump was approved by the US FDA.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.