North America Gene Synthesis Market

Market Size in USD Billion

USD

1.66 Billion

USD

8.92 Billion

2025

2033

USD

1.66 Billion

USD

8.92 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.66 Billion | |

| USD 8.92 Billion | |

| % | |

|

North America Gene Synthesis Market Overview

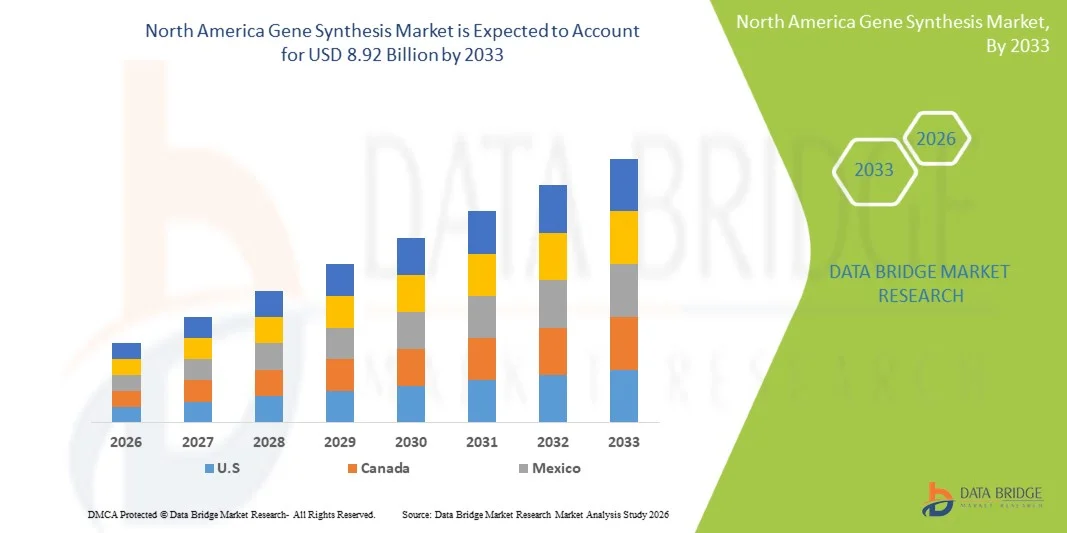

The North America gene synthesis market was valued at USD 1.66 billion in 2025 and is projected to reach USD 8.92 billion by 2033, growing at a CAGR of 23.40% from 2026 to 2033. The market is witnessing steady expansion driven by increasing demand for synthetic biology applications, rapid advancements in DNA synthesis technologies, and growing investments in genomics research across pharmaceutical and biotechnology sectors.

The rising adoption of gene synthesis in drug discovery, personalized medicine, and vaccine development, coupled with strong research infrastructure and funding support in the U.S. and Canada, is accelerating market growth. In addition, improvements in high-throughput and automated gene synthesis platforms are enabling faster, more accurate, and cost-efficient production of custom DNA sequences, supporting applications in healthcare, agriculture, and industrial biotechnology.

Key Market Trends & Insights

- The United States dominated the North America gene synthesis market with the largest revenue share of 87.12% in 2025, supported by strong biotechnology ecosystems, advanced genomics infrastructure, and high R&D investments from leading pharmaceutical and life sciences companies.

- The Consumables segment led the market with a 48.62% share in 2025, driven by continuous and recurring demand for nucleotides, enzymes, reagents, and oligonucleotide building blocks used in DNA assembly workflows.

- Canada is expected to be the fastest-growing country at a CAGR of 10.6% from 2026 to 2033, fueled by rising government funding for genomics research, expanding biotech startups, and growing academic–industry collaborations.

- Software & Services are the fastest-growing component type, projected to register a CAGR of 12.4%, reflecting the surge in adoption of AI-based gene design platforms and cloud-enabled bioinformatics tools.

- The Standard Gene segment dominated the gene type category with a 44.18% revenue share in 2025, led by widespread use in routine research, cloning applications, and basic molecular biology studies.

- Custom Gene Synthesis accounted for 61.35% of the market, preferred by strong demand for tailored DNA sequences for therapeutic research, protein engineering, and vaccine development.

- The Gene Library Synthesis segment is the fastest-growing gene synthesis type category, with a CAGR of 11.8%, driven by increasing use in high-throughput screening, functional genomics, and synthetic biology research.

Market Size & Forecast

- Global Market Value (2025): USD 1.66 Billion

- Expected Market Value (2033): USD 8.92 Billion

- Forecast CAGR (2026–2033): 23.40%

- Leading Country in 2025: United States

- Fastest Growing Country: Canada

Report Scope and North America Gene Synthesis Market Segmentation

|

Attributes |

North America Gene Synthesis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico |

|

Key Market Players |

· Twist Bioscience (U.S.) · Integrated DNA Technologies (U.S.) · Thermo Fisher Scientific, Inc. (U.S.) · Ginkgo Bioworks (U.S.) · Synthego (U.S.) · ATUM (U.S.) · Codex DNA (U.S.) · Azenta Life Sciences (U.S.) · OriGene Technologies (U.S.) · Synbio Technologies (U.S.) · Eton Bioscience (U.S.) · Blue Heron Biotechnology (U.S.) · GenScript Biotech Corporation (China) · Bio Basic Inc. (Canada) · Biomatik Corporation (Canada) · Eurofins Genomics (Luxembourg) · Creative Biogene (U.S.) · Plasmidsaurus (U.S.) · DNA Script (France) · Benchling (U.S.) |

|

Market Opportunities |

· Expansion of personalized medicine programs · Increasing use of gene synthesis in next-generation vaccine development · Growing adoption of synthetic biology in industrial biotechnology |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

North America Gene Synthesis Market Trends

Trend: Rising Adoption of Gene Synthesis in Synthetic Biology & Drug Discovery

Biotechnology firms and pharmaceutical companies are increasingly utilizing gene synthesis to design and construct custom DNA sequences for drug discovery, metabolic engineering, and precision medicine development. The integration of high-throughput automated synthesis platforms enables rapid generation of optimized gene constructs for therapeutic research and industrial applications. Researchers are also leveraging AI-driven design tools to improve sequence accuracy, reduce synthesis errors, and accelerate experimental workflows, while cloud-based platforms support global collaboration in genomics projects. For instance, Twist Bioscience and Ginkgo Bioworks are expanding large-scale synthetic DNA production to support next-generation therapeutic and industrial biotechnology applications.

North America Gene Synthesis Market Dynamics

Key Market Driver: Expanding Applications in Gene and Cell Therapy Development

The rapid growth of gene and cell therapy pipelines has significantly increased demand for high-quality synthesized DNA sequences used in vector construction, therapeutic gene design, and functional genomics research. Pharmaceutical companies and biotech startups are integrating gene synthesis into early-stage drug development to accelerate target identification and optimize therapeutic candidates. Continuous advancements in enzymatic synthesis technologies are further improving scalability, accuracy, and cost efficiency of DNA production. For instance, companies such as Moderna and CRISPR Therapeutics are increasingly relying on custom gene constructs for developing advanced gene-editing and mRNA-based therapeutic solutions.

Key Restraint/Challenge: High Cost and Technical Complexity of Scalable Gene Synthesis

A major restraint in the North America gene synthesis market is the high cost associated with large-scale, high-fidelity DNA synthesis platforms, along with technical limitations in synthesizing long or highly repetitive sequences. The requirement for specialized infrastructure, skilled personnel, and stringent quality control increases operational expenses for research institutions and smaller biotech firms. In addition, error correction processes and synthesis bottlenecks further limit throughput in complex genomic applications.

For instance, academic laboratories and early-stage biotech startups often face delays in scaling synthetic gene workflows due to dependency on expensive commercial synthesis service providers such as Integrated DNA Technologies.

Key Market Opportunity: Expansion of AI-Driven Design and High-Throughput Synthetic Biology Platforms

The increasing integration of artificial intelligence and machine learning in gene design is creating significant opportunities for automated sequence optimization, error reduction, and predictive genetic modeling in synthetic biology workflows. High-throughput gene synthesis platforms combined with cloud-based bioinformatics are enabling faster, more cost-efficient development of complex DNA constructs for drug discovery, diagnostics, and engineered biological systems. Growing adoption across pharmaceutical, agricultural, and industrial biotechnology sectors is further expanding commercial potential. For instance, companies such as Benchling and GenScript are advancing AI-enabled gene design and scalable DNA synthesis platforms to accelerate research and therapeutic development pipelines.

North America Gene Synthesis Market Scope

The North America gene synthesis market is segmented on the basis of component, gene type, gene synthesis type, application, method, end user, and distribution channel.

- By Component

On the basis of component, the North America gene synthesis market is segmented into synthesizer, consumables, and software & services. The Consumables segment dominated the market with a 48.62% share in 2025, owing to continuous and recurring demand for nucleotides, enzymes, reagents, and oligonucleotide building blocks used in DNA assembly workflows. These materials are essential for every synthesis cycle, making them a stable revenue-generating category for suppliers. Strong adoption across pharmaceutical and biotech research labs further strengthens its dominance. Increasing gene editing and synthetic biology experiments are boosting consumables consumption at scale. High repeat purchase frequency ensures sustained market contribution. The segment also benefits from expanding automated synthesis systems that require standardized reagent inputs.

The Software & Services segment is expected to witness the fastest growth at a CAGR of 12.4% from 2026 to 2033, driven by increasing adoption of AI-based gene design platforms and cloud-enabled bioinformatics tools. These solutions support sequence optimization, error correction, and predictive modeling for complex gene constructs. Growing demand for outsourced gene synthesis services among biotech startups is also fueling expansion. Integration of machine learning algorithms enhances efficiency and reduces design time. Rising collaboration between research institutions and service providers is further accelerating adoption. Increasing shift toward digitalized and automated synthetic biology workflows is strengthening this segment’s growth trajectory.

- By Gene Type

On the basis of gene type, the market is segmented into standard gene, express gene, complex gene, and others. The Standard Gene segment dominated the market with a 44.18% share in 2025, driven by widespread use in routine research, cloning applications, and basic molecular biology studies. These genes are easier and faster to synthesize, making them highly cost-effective for academic and industrial laboratories. High demand from pharmaceutical companies for early-stage drug screening supports segment dominance. Standard genes are also widely used in diagnostic assay development. Their relatively low error rate and established synthesis protocols further enhance adoption. Continuous demand from educational and research institutions sustains market leadership.

The Complex Gene segment is expected to witness the fastest growth at a CAGR of 13.1% from 2026 to 2033, driven by increasing need for long, modified, and high-GC content sequences used in advanced therapeutic and synthetic biology applications. These genes are essential for gene therapy, vaccine development, and engineered biological systems. Advances in enzymatic synthesis and error-correction technologies are improving feasibility. Rising demand for multi-domain protein engineering is further supporting growth. Pharmaceutical companies are increasingly investing in complex gene constructs for precision medicine development. Expanding applications in cell and gene therapy pipelines are accelerating segment expansion.

- By Gene Synthesis Type

On the basis of gene synthesis type, the market is segmented into gene library synthesis and custom gene synthesis. The Custom Gene Synthesis segment dominated the market with a 61.35% share in 2025, driven by strong demand for tailored DNA sequences for therapeutic research, protein engineering, and vaccine development. Researchers require highly specific gene constructs that cannot be fulfilled by standardized libraries. Pharmaceutical companies heavily rely on custom synthesis for drug discovery pipelines. Increasing adoption in CRISPR-based gene editing further strengthens demand. The segment benefits from flexibility, high accuracy, and compatibility with advanced research applications. Continuous innovation in automated synthesis platforms supports scalability of custom solutions.

The Gene Library Synthesis segment is expected to witness the fastest growth at a CAGR of 11.8% from 2026 to 2033, driven by increasing use in high-throughput screening, functional genomics, and synthetic biology research. Gene libraries enable rapid testing of multiple genetic variants in parallel, improving research efficiency. Growing demand for protein engineering and pathway optimization is accelerating adoption. Expanding use in AI-driven drug discovery platforms is further enhancing relevance. Declining costs of library construction are supporting broader accessibility. Rising integration with cloud-based bioinformatics tools is strengthening large-scale genomic research capabilities.

- By Application

On the basis of application, the market is segmented into synthetic biology, genetic engineering, vaccine design, therapeutics antibodies, and others. The Synthetic Biology segment dominated the market with a 39.74% share in 2025, driven by extensive use of engineered DNA sequences for designing new biological systems and metabolic pathways. Companies are leveraging gene synthesis to produce bio-based chemicals, enzymes, and industrial proteins. Strong investment in bio-manufacturing and sustainable production methods supports dominance. Increasing use of automation and AI in synthetic biology workflows is enhancing productivity. Academic and industrial collaboration is further accelerating innovation. The segment benefits from broad cross-industry applications including healthcare, agriculture, and energy.

The Vaccine Design segment is expected to witness the fastest growth at a CAGR of 13.6% from 2026 to 2033, driven by rising demand for rapid vaccine development platforms, especially for mRNA and recombinant DNA-based vaccines. Gene synthesis enables quick design and modification of antigen sequences. Increasing preparedness for emerging infectious diseases is fueling adoption. Pharmaceutical companies are investing heavily in rapid-response vaccine technologies. Advances in synthetic DNA manufacturing are reducing development timelines. Growing government funding for pandemic preparedness is further accelerating segment growth.

- By Method

On the basis of method, the market is segmented into solid phase synthesis, chip-based DNA synthesis, and PCR-based enzyme synthesis. The Solid Phase Synthesis segment dominated the market with a 52.08% share in 2025, owing to its high accuracy, scalability, and established use in oligonucleotide and gene assembly workflows. It is widely adopted in commercial gene synthesis services due to reliable output quality. Strong compatibility with automation systems enhances efficiency. Pharmaceutical and biotech companies prefer this method for standardized production. Continuous optimization of chemical synthesis protocols improves yield and reduces errors. Its maturity and global availability support sustained dominance.

The PCR-Based Enzyme Synthesis segment is expected to witness the fastest growth at a CAGR of 14.2% from 2026 to 2033, driven by increasing demand for enzymatic, error-reduced, and environmentally friendly DNA synthesis techniques. This method enables higher fidelity and longer sequence assembly compared to traditional approaches. Growing focus on sustainable and green biotechnology practices supports adoption. Advances in polymerase engineering are improving performance. Rising use in complex gene construction and synthetic biology applications is further accelerating growth. Continuous innovation is positioning enzymatic synthesis as a next-generation technology.

- By End User

On the basis of end user, the market is segmented into academic & research institutes, diagnostics laboratories, biotech & pharmaceutical companies, and others. The Biotech & Pharmaceutical Companies segment dominated the market with a 46.28% share in 2025, driven by extensive use of gene synthesis in drug discovery, biologics development, and gene therapy programs. These companies invest heavily in synthetic biology platforms to accelerate innovation pipelines. Increasing demand for personalized medicine and targeted therapies further strengthens adoption. Integration of gene synthesis into R&D workflows improves efficiency and reduces development timelines. Strong financial capacity enables large-scale outsourcing and in-house synthesis adoption. Continuous expansion of biologics and gene editing pipelines sustains dominance.

The Academic & Research Institutes segment is expected to witness the fastest growth at a CAGR of 11.9% from 2026 to 2033, driven by rising funding for genomics research and synthetic biology education programs. Universities are increasingly adopting gene synthesis for experimental biology and innovation projects. Government grants supporting life sciences research are boosting adoption. Growing collaboration with biotech companies is accelerating technology transfer. Increasing access to cloud-based gene design tools is enhancing research capabilities. Expanding focus on molecular biology and genetic engineering studies is further supporting segment growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, online distributions, and third-party distributions. The Direct Tender segment dominated the market with a 58.41% share in 2025, driven by large-scale procurement contracts from pharmaceutical companies, research institutes, and government-funded projects. Direct agreements ensure customized gene synthesis solutions with better quality control and pricing advantages. Strong supplier–client relationships enhance reliability and long-term collaboration. Bulk purchasing requirements in clinical and research applications further strengthen this channel. High dependency on trusted vendors supports dominance. Regulatory compliance requirements also favor direct procurement models.

The Online Distributions segment is expected to witness the fastest growth at a CAGR of 13.3% from 2026 to 2033, driven by increasing adoption of digital procurement platforms and cloud-based ordering systems. These platforms offer faster turnaround times and simplified ordering processes for researchers. Expanding presence of biotech e-commerce portals is improving accessibility. Small and mid-sized labs increasingly prefer online channels due to cost efficiency. Integration with AI-based sequence design tools is further streamlining purchasing workflows. Rising digitalization of life science procurement is accelerating segment expansion.

North America Gene Synthesis Market Regional Analysis

The United States dominated the North America gene synthesis market with the largest revenue share of 87.12% in 2025, supported by strong biotechnology ecosystems, advanced genomics infrastructure, and high R&D investments from leading pharmaceutical and life sciences companies. The country benefits from rapid adoption of automated DNA synthesis platforms, extensive use of synthetic biology in drug discovery, and strong integration of AI and bioinformatics in genomic workflows. Increasing applications in gene therapy, vaccine development, and precision medicine continue to reinforce the United States’ leadership position in the regional market.

U.S. Gene Synthesis Market Insight

The U.S. gene synthesis market is witnessing strong growth due to rising investments in genomics research, gene therapy development, and precision medicine programs. The country’s highly advanced biotechnology ecosystem, along with the presence of leading pharmaceutical and synthetic biology companies, is driving demand across drug discovery, vaccine design, and genetic engineering applications. In addition, increasing adoption of AI-driven gene design platforms and high-throughput DNA synthesis technologies is accelerating research efficiency and reducing development timelines across life sciences sectors.

Canada Gene Synthesis Market Insight

The Canada gene synthesis market is witnessing steady growth due to increasing government funding for genomics research, rising adoption of synthetic biology in healthcare and agriculture, and expanding collaboration between academic institutes and biotechnology companies. The country’s strong life sciences ecosystem, along with growing presence of contract research organizations and biotech startups, is driving demand across drug discovery, vaccine development, and genetic engineering applications. In addition, increasing use of AI-driven gene design platforms, cloud-based bioinformatics tools, and automated DNA synthesis technologies is improving research efficiency and supporting advanced biomedical innovation across Canada.

Mexico Gene Synthesis Market Insight

The Mexico gene synthesis market is experiencing gradual growth, supported by rising investments in biotechnology infrastructure, increasing focus on healthcare innovation, and growing adoption of molecular biology tools in academic and clinical research. The country is witnessing expanding use of gene synthesis in diagnostics, agricultural biotechnology, and pharmaceutical research applications. In addition, increasing collaboration with North American biotech firms, along with gradual adoption of synthetic biology and genetic engineering technologies, is helping improve research capabilities and driving market development in Mexico.

North America Gene Synthesis Market Share

The North America Gene Synthesis industry is primarily led by well-established companies, including:

- Twist Bioscience (U.S.)

- Integrated DNA Technologies (U.S.)

- Thermo Fisher Scientific, Inc. (U.S.)

- Ginkgo Bioworks (U.S.)

- Synthego (U.S.)

- ATUM (U.S.)

- Codex DNA (U.S.)

- Azenta Life Sciences (U.S.)

- OriGene Technologies (U.S.)

- Synbio Technologies (U.S.)

- Eton Bioscience (U.S.)

- Blue Heron Biotechnology (U.S.)

- GenScript Biotech Corporation (China)

- Bio Basic Inc. (Canada)

- Biomatik Corporation (Canada)

- Eurofins Genomics (Luxembourg)

- Creative Biogene (U.S.)

- Plasmidsaurus (U.S.)

- DNA Script (France)

- Benchling (U.S.)

Latest Developments in North America Gene Synthesis Market

- In May 2025, Twist Bioscience and Ginkgo Bioworks revised their long-term collaboration agreement, shifting to a more flexible model that allows on-demand ordering of synthetic DNA while strengthening Twist’s intellectual property position in long DNA technologies, reflecting growing demand for scalable gene synthesis solutions in synthetic biology and therapeutics development

- In June 2024, GenScript Biotech Corporation launched its FLASH Gene service in North America, enabling ultra-fast gene synthesis with turnaround times as short as four business days, significantly accelerating workflows in drug discovery, vaccine development, and antibody engineering applications

- In May 2024, GenScript expanded its RNA capabilities by introducing a self-amplifying RNA (saRNA) synthesis service, supporting advanced applications in vaccines, gene therapy, and cancer immunotherapy, and enhancing efficiency in protein expression and therapeutic development pipelines

- In January 2024, Twist Bioscience expanded its Express Genes platform in North America, offering faster turnaround times and larger-scale DNA preparation to support high-throughput research in synthetic biology, pharmaceutical development, and genetic engineering applications

- In November 2023, Twist Bioscience launched its Express Genes rapid synthesis service, enabling delivery of synthetic DNA in as little as 5–7 business days using its silicon-based DNA synthesis platform, significantly improving speed and efficiency in biotechnology and pharmaceutical R&D workflows

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.