North America Heart Failure Software Market

Market Size in USD Billion

USD

1.96 Billion

USD

3.03 Billion

2025

2033

USD

1.96 Billion

USD

3.03 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.96 Billion | |

| USD 3.03 Billion | |

| % | |

|

North America Heart Failure Software Market Size

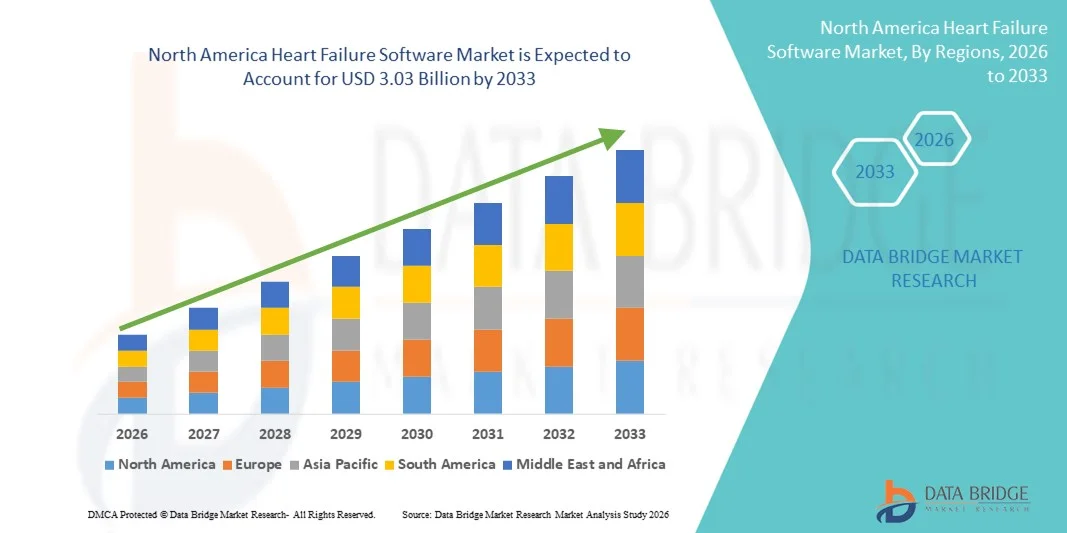

- The North America Heart Failure Software market size was valued at USD 1.96 Billion in 2025 and is expected to reach USD 3.03 Billion by 2033, at a CAGR of 5.60% during the forecast period

- The market growth is largely fueled by the increasing prevalence of heart failure and the rapid adoption of digital health technologies, including clinical decision support systems, remote patient monitoring, and AI-enabled analytics, leading to improved disease management across hospitals and outpatient care settings

- Furthermore, rising demand for data-driven, user-friendly, and interoperable healthcare IT solutions that support early diagnosis, treatment optimization, and continuous patient monitoring is establishing heart failure software as a critical tool in modern cardiovascular care. These converging factors are accelerating the uptake of Heart Failure Software solutions, thereby significantly boosting the industry’s growth

North America Heart Failure Software Market Analysis

- Heart failure software, including clinical decision support systems, remote patient monitoring platforms, and AI-enabled analytics tools, is becoming a critical component of cardiovascular care across hospitals and outpatient settings, enabling improved disease management, early intervention, and reduced hospital readmissions

- The growing demand for heart failure software is primarily driven by the rising prevalence of cardiovascular diseases, increasing adoption of digital health solutions, and government-led healthcare digitization initiatives, particularly across Middle Eastern healthcare systems focusing on value-based and outcome-driven care

- U.S. dominated the heart failure software market with the largest revenue share of approximately 42.8% in 2025, supported by strong government investments, rapid digital transformation of hospitals, high adoption of electronic health records, and growing deployment of remote patient monitoring and AI-driven clinical platforms across public and private healthcare facilities

- Canada is expected to be the fastest-growing country in the heart failure software market during the forecast period, driven by advanced healthcare infrastructure, aggressive adoption of telehealth and AI-based healthcare technologies, rising cardiovascular disease burden, and strong regulatory support for digital health innovation

- The integrated segment dominated the market with a revenue share of approximately 61.2% in 2025, supported by its ability to seamlessly connect with hospital information systems, EHRs, laboratory systems, and diagnostic imaging platforms

Report Scope and Heart Failure Software Market Segmentation

|

Attributes |

Heart Failure Software Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

North America Heart Failure Software Market Trends

Advanced Analytics and AI-Driven Clinical Decision Support

- A significant and accelerating trend in the global failure software market is the increasing integration of artificial intelligence (AI), machine learning, and advanced analytics to support early diagnosis, risk stratification, and personalized treatment planning for heart failure patients. These technologies are enabling healthcare providers to move toward more proactive and data-driven disease management approaches

- For instance, AI-enabled heart failure management platforms are being deployed across hospitals and specialty cardiac centers to analyze large volumes of patient data, including electronic health records (EHRs), imaging results, and remote monitoring data, to predict disease progression and reduce unplanned hospitalizations

- AI integration in heart failure software allows for features such as predictive modeling, automated alerts for clinical deterioration, and individualized therapy recommendations. Some platforms leverage machine learning algorithms to identify high-risk patients earlier and assist clinicians in optimizing medication regimens and follow-up schedules

- The growing adoption of remote patient monitoring (RPM) tools, including wearable devices and connected sensors, is further enhancing heart failure software capabilities by enabling continuous tracking of vital signs such as heart rate, blood pressure, and fluid status, supporting timely clinical interventions

- This trend toward intelligent, data-driven, and interoperable heart failure software solutions is reshaping clinical workflows and improving care coordination across hospitals, outpatient clinics, and home-based care settings. Consequently, software developers and healthcare IT providers are increasingly focusing on scalable, cloud-based platforms tailored to regional healthcare infrastructure

- The demand for advanced heart failure software solutions is growing steadily across the region as healthcare systems prioritize improved patient outcomes, reduced readmission rates, and more efficient utilization of limited clinical resources

North America Heart Failure Software Market Dynamics

Driver

Rising Burden of Cardiovascular Diseases and Healthcare Digitalization

- The rising prevalence of cardiovascular diseases, including heart failure, driven by aging populations, lifestyle changes, and increasing rates of hypertension and diabetes, is a major driver of demand for heart failure software solutions

- For instance, several countries across the region are investing in national digital health initiatives and hospital information system upgrades to improve chronic disease management, creating a favorable environment for the adoption of heart failure management software

- As healthcare providers face increasing patient volumes and resource constraints, heart failure software offers critical capabilities such as centralized patient data management, clinical decision support, and care pathway standardization, helping improve efficiency and quality of care

- Furthermore, the growing emphasis on value-based care and outcome-driven healthcare models is encouraging providers to adopt software solutions that support long-term disease monitoring, medication adherence, and reduced hospital readmissions

- The increasing use of telehealth services and remote monitoring programs across urban and semi-urban regions is further accelerating the adoption of heart failure software in both public and private healthcare settings

Restraint/Challenge

High Implementation Costs and Data Privacy Concerns

- High initial implementation costs associated with advanced heart failure software systems, including licensing, system integration, staff training, and infrastructure upgrades, present a significant challenge to widespread adoption, particularly in resource-constrained healthcare facilities across

- For instance, smaller hospitals and clinics may face budgetary limitations that restrict their ability to invest in comprehensive digital health platforms, slowing market penetration in certain regions

- Concerns related to data privacy, cybersecurity, and regulatory compliance also act as restraints, as heart failure software relies heavily on sensitive patient health data. Inconsistent data protection frameworks across countries can complicate cross-border deployments and cloud-based implementations

- Addressing these challenges through cost-effective deployment models, stronger cybersecurity measures, and compliance with regional health data regulations is essential for building trust among healthcare providers and patients

- Overcoming these barriers through government support, public-private partnerships, and scalable software solutions will be critical for sustained growth of the Heart Failure Software market

North America Heart Failure Software Market Scope

The market is segmented on the basis of type, delivery mode, platform, supportive devices, features, and end-user.

- By Type

On the basis of type, the Heart Failure Software market is segmented into Knowledge-Based and Non-Knowledge-Based systems. The knowledge-based segment dominated the largest market revenue share of approximately 58.4% in 2025, primarily due to its ability to incorporate clinical guidelines, standardized treatment protocols, and evidence-based decision-making tools into heart failure management workflows. These systems assist clinicians by providing alerts, recommendations, and predictive insights based on patient-specific clinical data. Hospitals increasingly rely on knowledge-based software to reduce diagnostic errors and improve clinical outcomes for chronic heart failure patients. The rising burden of cardiovascular diseases and growing emphasis on guideline-adherent care further support adoption. Integration with electronic health records enhances clinical efficiency and continuity of care. Strong regulatory support for clinical decision support systems also boosts demand. In addition, increasing adoption in tertiary care hospitals and academic medical centers contributes significantly to market dominance.

The non-knowledge-based segment is expected to witness the fastest CAGR of approximately 9.6% from 2026 to 2033, driven by growing demand for flexible, data-driven platforms that focus on visualization and trend analysis rather than predefined clinical rules. These systems are widely adopted in outpatient clinics and ambulatory settings due to lower implementation and maintenance costs. The increasing use of wearable devices and remote monitoring tools generates large volumes of patient data that are efficiently managed by non-knowledge-based software. Healthcare providers prefer these solutions for population health monitoring and reporting. Rising adoption in developing healthcare systems and expanding telehealth services further accelerate growth.

- By Delivery Mode

On the basis of delivery mode, the Heart Failure Software market is segmented into On-Premises, Cloud-Based Systems, and Web-Based solutions. The cloud-based systems segment accounted for the largest market revenue share of approximately 46.9% in 2025, owing to its scalability, cost efficiency, and remote accessibility. Cloud-based platforms enable real-time monitoring of heart failure patients across multiple care settings, supporting telemedicine and home healthcare models. Healthcare providers benefit from reduced infrastructure investments and automated software updates. Increasing adoption of remote patient monitoring programs significantly drives demand. Enhanced data security, regulatory compliance, and interoperability with EHRs further strengthen market penetration. Cloud platforms also facilitate integration with wearable and mobile health devices. The shift toward value-based care models reinforces widespread adoption.

The web-based segment is projected to grow at the fastest CAGR of around 10.3% from 2026 to 2033, driven by ease of deployment and browser-based accessibility. These solutions are particularly attractive for multi-location healthcare providers and specialty clinics. Web-based platforms support rapid implementation without extensive IT infrastructure. Increasing internet penetration and growing digital health literacy support adoption. Expanding use in outpatient care and remote consultations further accelerates growth during the forecast period.

- By Platform

On the basis of platform, the Heart Failure Software market is segmented into Standalone and Integrated systems. The integrated segment dominated the market with a revenue share of approximately 61.2% in 2025, supported by its ability to seamlessly connect with hospital information systems, EHRs, laboratory systems, and diagnostic imaging platforms. Integrated solutions enable comprehensive patient management by consolidating clinical, diagnostic, and therapeutic data into a single interface. Hospitals prefer integrated platforms to improve care coordination among multidisciplinary teams. These systems reduce data duplication and enhance clinical decision-making. Regulatory requirements for interoperability further drive adoption. The increasing complexity of heart failure management supports demand for integrated solutions.

The standalone segment is anticipated to register the fastest CAGR of nearly 8.8% from 2026 to 2033, driven by adoption among small hospitals, specialty clinics, and ambulatory care centers. Standalone software offers focused functionality with faster deployment timelines. Lower upfront costs and minimal system integration requirements attract resource-constrained healthcare facilities. Growing use in outpatient and remote care settings further supports rapid growth. Technological improvements in user interfaces enhance adoption.

- By Supportive Devices

On the basis of supportive devices, the Heart Failure Software market is segmented into Desktops, Tablets, and Others. The desktop segment held the largest market revenue share of approximately 49.5% in 2025, due to widespread usage in hospitals and diagnostic centers. Desktop systems provide high processing power and large display interfaces suitable for detailed data analysis. Clinicians prefer desktops for reviewing imaging data, lab results, and longitudinal patient records. Integration with hospital networks ensures secure data storage. Desktops also support advanced analytics and reporting tools. Their reliability and compatibility with enterprise systems drive continued dominance.

The tablet segment is expected to grow at the fastest CAGR of about 11.1% during the forecast period, supported by increasing mobility needs in clinical environments. Tablets facilitate point-of-care decision-making and bedside patient monitoring. Growing adoption in home healthcare and telecardiology programs accelerates growth. Lightweight design and improved battery performance enhance usability. Secure mobile applications further support expanding adoption. Furthermore, tablets offer seamless integration with EHR systems, enabling faster access to patient data. Rising investment in mobile health infrastructure is also driving the adoption of tablet-based heart failure software solutions.

- By Features

On the basis of features, the Heart Failure Software market is segmented into Heart Monitoring Activity, Tracking Periodic Tests, Review Progress, Diagnosis and Therapy Monitoring, Diary Management Tool, and Others. The diagnosis and therapy monitoring segment dominated the market with a revenue share of approximately 34.7% in 2025, driven by its critical role in managing chronic and advanced heart failure cases. These features enable clinicians to assess treatment effectiveness and disease progression. Integration with remote monitoring devices allows early detection of clinical deterioration. Hospitals prioritize these tools to reduce readmissions and improve outcomes. Personalized therapy planning further supports adoption. Regulatory emphasis on outcome-based care strengthens market leadership.

The heart monitoring activity segment is expected to register the fastest CAGR of nearly 12.4% from 2026 to 2033, driven by the increasing adoption of wearable cardiac monitoring devices. Continuous tracking supports proactive disease management and early intervention. Rising demand for home-based care significantly accelerates growth. Integration with mobile applications enhances patient engagement. Growing awareness of preventive cardiology further supports expansion. Moreover, advancements in AI-powered analytics improve accuracy and early detection of anomalies. Increasing partnerships between software providers and device manufacturers are further strengthening the segment’s growth.

- By End-User

On the basis of end-user, the Heart Failure Software market is segmented into Hospitals, Specialty Clinics, Ambulatory Surgical Centers, and Others. The hospitals segment accounted for the largest market revenue share of approximately 52.8% in 2025, due to high patient volumes and advanced care requirements. Hospitals manage complex heart failure cases requiring continuous monitoring and data integration. Availability of specialized cardiology departments supports adoption. Strong IT infrastructure enables seamless implementation. Government funding and digital health initiatives further reinforce dominance.

The specialty clinics segment is projected to grow at the fastest CAGR of around 10.7% during the forecast period, driven by increasing specialization in cardiovascular care. Rising outpatient management of heart failure supports demand. Clinics adopt digital tools for personalized treatment planning. Expanding referral networks further accelerate growth. Improved affordability and usability strengthen adoption. In addition, specialty clinics benefit from faster software implementation cycles and lower infrastructure requirements compared to large hospitals. The growing preference for focused, cost-effective cardiac care centers among patients is further boosting segment growth.

North America Heart Failure Software Market Regional Analysis

- The North America heart failure software market is anticipated to expand significantly during the forecast period, supported by rapid digital transformation in the healthcare sector and strong government initiatives promoting smart healthcare

- The region is witnessing increased investments in telemedicine, electronic health records, and remote patient monitoring systems, which are driving the adoption of heart failure software solutions

- Rising prevalence of cardiovascular diseases and growing healthcare infrastructure upgrades are further fueling market growth

U.S. Heart Failure Software Market

The U.S. heart failure software market dominated the Heart Failure Software market with the largest revenue share of approximately 42.8% in 2025, supported by strong government investments, rapid digital transformation of hospitals, high adoption of electronic health records, and growing deployment of remote patient monitoring and AI-driven clinical platforms across public and private healthcare facilities. The country’s focus on improving healthcare accessibility and patient outcomes is also encouraging hospitals and clinics to adopt advanced heart failure management software.

Canada Heart Failure Software Market

The Canada heart failure software market is expected to be the fastest-growing country in the Heart Failure Software market during the forecast period, driven by advanced healthcare infrastructure, aggressive adoption of telehealth and AI-based healthcare technologies, rising cardiovascular disease burden, and strong regulatory support for digital health innovation. The presence of global healthcare technology providers and ongoing smart hospital projects are also accelerating software adoption in Canada.

North America Heart Failure Software Market Share

The Heart Failure Software industry is primarily led by well-established companies, including:

• Philips Healthcare (Netherlands)

• GE HealthCare (U.S.)

• Siemens Healthineers (Germany)

• Medtronic (Ireland)

• Boston Scientific (U.S.)

• Abbott (U.S.)

• Novartis (Switzerland)

• Roche Diagnostics (Switzerland)

• B.D. (U.S.)

• Allscripts (U.S.)

• Epic Systems (U.S.)

• Cerner (U.S.)

• IBM Watson Health (U.S.)

• Oracle Health Sciences (U.S.)

• ResMed (U.S.)

Latest Developments in North America Heart Failure Software Market

- In September 2024, Astellas Pharma Inc. announced that its DIGITIVA™ digital health solution for heart failure management was listed with the U.S. Food and Drug Administration (FDA) as a Class I Software as a Medical Device (SaMD). DIGITIVA integrates a smartphone app, a digital stethoscope, and clinician review components to support at-home monitoring and personalized care for heart failure patients

- In May 2025, Cardiosense launched the nationwide SEISMIC-HF II study to validate its AI-based algorithm for non-invasive heart failure management, following promising results from SEISMIC-HF I, which demonstrated the AI’s ability to estimate intracardiac pressures—critical for early detection and proactive intervention

- In April 2025, Eko Health Inc. received FDA clearance for its CORE500 Digital Stethoscope with integrated heart failure detection features, aimed at assisting clinicians in identifying early signs of heart failure during routine exams; Eko also secured USD 41 Billion in Series D funding to expand its Sensora platform’s reach

- In April 2025, the PrediHealth Project, a Europe-based research initiative, launched an advanced AI-driven telemedicine platform that combines wearable device data with predictive analytics to manage chronic heart failure more effectively, showing promising results in reducing readmissions and enhancing patient engagement

- In March 2025, researchers introduced TRisk, a transformer-based AI model trained on large-scale UK health records to predict 36-month mortality in heart failure patients, significantly outperforming traditional risk prediction models and highlighting the integration of advanced deep learning tools in heart failure decision support applications

- In April 2025, the FDA granted clearance to HeartFocus, an AI-enabled cardiac imaging software developed by DESKi, enabling healthcare professionals—including non-specialists—to perform diagnostic-grade echocardiography using compatible devices, thereby broadening access to early cardiac care

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.