North America Hereditary Cancer Testing Market

Market Size in USD Billion

USD

3.39 Billion

USD

9.20 Billion

2025

2033

USD

3.39 Billion

USD

9.20 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.39 Billion | |

| USD 9.20 Billion | |

| % | |

|

North America Hereditary Cancer Testing Market Size

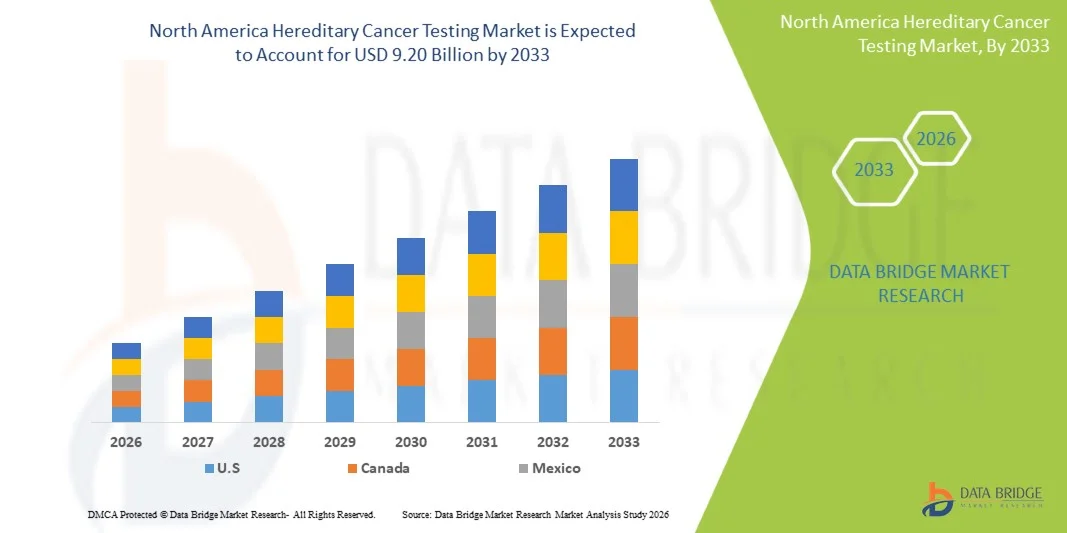

- The North America hereditary cancer testing market size was valued at USD 3.39 billion in 2025 and is expected to reach USD 9.20 billion by 2033, at a CAGR of 13.3% during the forecast period

- The market growth is largely fueled by the increasing prevalence of hereditary cancers and growing awareness regarding the benefits of early genetic screening and personalized medicine, leading to higher adoption across clinical and diagnostic settings

- Furthermore, advancements in next-generation sequencing technologies, supportive reimbursement frameworks, and the presence of key industry players are establishing hereditary cancer testing as a critical component of precision oncology. These converging factors are accelerating the uptake of testing solutions, thereby significantly boosting the region's market growth

North America Hereditary Cancer Testing Market Analysis

- Hereditary cancer testing, which involves genetic screening to identify inherited mutations associated with cancers such as breast, ovarian, and colorectal cancer, is becoming a critical component of modern healthcare systems across North America due to its role in early detection, risk assessment, and personalized treatment planning in both clinical and preventive care settings

- The escalating demand for hereditary cancer testing is primarily fueled by the rising incidence of genetic cancers, increasing awareness about early diagnosis, and a growing preference for precision medicine and targeted therapies among patients and healthcare providers

- The United States dominated the hereditary cancer testing market in North America with the largest revenue share of 82.4% in 2025, characterized by advanced healthcare infrastructure, strong reimbursement frameworks, and a high adoption of next-generation sequencing technologies, with the country experiencing substantial growth in genetic testing volumes, particularly through hospital networks and specialized diagnostic laboratories, driven by continuous innovations from leading biotechnology firms

- Canada is expected to be the fastest growing country in the hereditary cancer testing market during the forecast period driven by expanding access to genetic counseling services, increasing government initiatives for early cancer screening, and rising investments in precision medicine

- Multi-gene panel testing segment dominated the hereditary cancer testing market with a significant market share of 68.7% in 2025, driven by its ability to simultaneously analyze multiple cancer-related genes, offering comprehensive, cost-effective, and clinically actionable insights compared to single-gene testing methods

Report Scope and North America Hereditary Cancer Testing Market Segmentation

|

Attributes |

North America Hereditary Cancer Testing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

North America Hereditary Cancer Testing Market Trends

“Rising Adoption of AI-Driven Genomic Interpretation and Precision Oncology”

- A significant and accelerating trend in the North America hereditary cancer testing market is the deepening integration of artificial intelligence (AI) with genomic sequencing platforms and clinical decision-support systems. This convergence of technologies is significantly enhancing diagnostic accuracy and personalized risk assessment

- For instance, leading genetic testing providers are integrating AI-based algorithms with next-generation sequencing platforms to analyze complex genetic variants and deliver faster, more precise hereditary cancer risk reports. Similarly, clinical laboratories are leveraging cloud-based platforms to streamline genetic data interpretation and reporting workflows

- AI integration in hereditary cancer testing enables features such as automated variant classification, predictive risk modeling, and improved identification of rare mutations. For instance, some platforms utilize machine learning to continuously refine variant interpretation accuracy and provide more actionable insights for clinicians. Furthermore, digital tools offer healthcare providers the ability to access real-time decision support, improving patient outcomes

- The seamless integration of hereditary cancer testing with electronic health records and broader precision medicine platforms facilitates centralized management of patient genetic data. Through a unified system, clinicians can coordinate genetic insights with treatment planning, surveillance strategies, and family risk assessment, creating a more connected healthcare ecosystem

- This trend towards more intelligent, data-driven, and integrated genetic testing solutions is fundamentally reshaping clinical practices in oncology. Consequently, companies are developing advanced genomic testing solutions with features such as automated reporting, AI-based analytics, and enhanced compatibility with healthcare IT systems

- The demand for hereditary cancer testing solutions that offer advanced analytics and seamless integration is growing rapidly across hospitals, diagnostic laboratories, and research institutions, as healthcare providers increasingly prioritize precision medicine and early disease detection

- Growing emphasis on population-scale genetic screening initiatives and preventive healthcare programs is also contributing to higher adoption rates, as governments and healthcare organizations aim to reduce long-term cancer burden through early detection strategies

North America Hereditary Cancer Testing Market Dynamics

Driver

“Growing Demand Due to Rising Cancer Burden and Expansion of Precision Medicine”

- The increasing prevalence of hereditary cancers and the expanding adoption of precision medicine approaches among healthcare providers are significant drivers for the heightened demand for hereditary cancer testing

- For instance, in recent years, multiple healthcare institutions across the United States have expanded access to genetic screening programs, integrating hereditary cancer testing into routine oncology care pathways. Such initiatives by key stakeholders are expected to drive market growth in the forecast period

- As awareness regarding inherited cancer risks continues to rise, patients and clinicians are increasingly seeking early detection and preventive strategies, with hereditary cancer testing offering insights into mutation status and personalized risk management

- Furthermore, advancements in sequencing technologies and the growing availability of genetic counseling services are making hereditary cancer testing more accessible and clinically relevant, supporting its integration into mainstream healthcare

- The ability to guide targeted therapies, inform family screening decisions, and enable proactive healthcare planning are key factors propelling the adoption of hereditary cancer testing across clinical and research settings. The trend towards preventive healthcare and personalized treatment further contributes to market growth

- Increasing government initiatives and funding support for genomic research programs are further driving the expansion of hereditary cancer testing services across healthcare systems

- Rising partnerships between diagnostic laboratories and pharmaceutical companies are also boosting demand, as genetic testing plays a critical role in patient stratification for targeted drug development

Restraint/Challenge

“High Cost of Testing and Ethical Concerns Around Genetic Data Usage”

- Concerns surrounding the high cost of advanced genetic testing procedures and limited reimbursement in certain cases pose a significant challenge to broader market penetration. As hereditary cancer testing involves complex technologies, it can be financially burdensome for some patient groups

- For instance, disparities in insurance coverage and access to genetic counseling services across regions have made some individuals hesitant to undergo hereditary cancer testing despite potential benefits

- Addressing these cost-related barriers through expanded insurance coverage, government support programs, and cost-efficient testing solutions is crucial for improving accessibility. In addition, concerns regarding data privacy, ethical use of genetic information, and potential discrimination based on genetic results can create hesitation among patients

- While regulatory frameworks are evolving to protect genetic data, uncertainties around data security and usage policies may still hinder adoption, particularly among privacy-conscious individuals

- Overcoming these challenges through policy support, improved affordability, and enhanced data protection measures will be vital for sustained market growth in hereditary cancer testing across North America

- Limited availability of skilled genetic counselors and trained professionals in certain areas can also restrict the effective implementation and interpretation of hereditary cancer testing results

- Variability in regulatory guidelines and testing standards across regions may create inconsistencies in test quality and reporting, posing an additional barrier to widespread adoption

North America Hereditary Cancer Testing Market Scope

The market is segmented on the basis of test type, diagnosis type, technology, disease type, end user, and distribution channel.

- By Test Type

On the basis of test type, the North America hereditary cancer testing market is segmented into multi panel set and single site genetic test. The multi panel set segment dominated the market with the largest market revenue share of 68.7% in 2025, driven by its ability to analyze multiple cancer-associated genes simultaneously, offering comprehensive risk assessment. Healthcare providers increasingly prefer multi-gene panels due to their cost-effectiveness compared to conducting multiple single-gene tests separately. These panels also enhance diagnostic efficiency by identifying a broader spectrum of mutations in a single test. The growing adoption of precision medicine and advancements in sequencing technologies further support segment dominance. In addition, increasing clinical guidelines recommending panel testing for hereditary cancers are accelerating its widespread use across hospitals and laboratories.

The single site genetic test segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by its targeted approach in identifying specific known mutations within families. This method is particularly useful for follow-up testing when a pathogenic variant has already been identified in a family member. Its lower cost compared to multi-gene panels makes it more accessible for certain patient groups. Increasing awareness about familial cancer risks is also driving demand for targeted testing. Furthermore, advancements in rapid testing technologies are improving turnaround times for single-site tests. The growing emphasis on personalized and preventive healthcare strategies is further contributing to segment growth.

- By Diagnosis Type

On the basis of diagnosis type, the market is segmented into biopsy, imaging, and lab tests. The lab tests segment dominated the market with the largest revenue share in 2025, driven by its central role in genetic analysis and mutation identification. Laboratory-based testing enables precise detection of hereditary cancer markers using advanced molecular techniques. The increasing availability of high-throughput sequencing platforms is enhancing the efficiency of lab-based diagnostics. In addition, the integration of lab testing with genetic counseling services is improving patient outcomes. Strong infrastructure and established diagnostic laboratories in North America further support segment growth. Rising demand for early detection and preventive screening is also boosting the adoption of lab tests.

The imaging segment is expected to witness the fastest CAGR from 2026 to 2033, driven by its growing role in complementary diagnostics and early tumor detection. Imaging technologies such as MRI and CT scans are increasingly used alongside genetic testing to assess cancer progression and risk. Advances in imaging techniques are improving accuracy and enabling earlier detection of abnormalities. The integration of imaging data with genetic insights is enhancing clinical decision-making. Increasing investments in advanced diagnostic infrastructure are also supporting segment growth. Moreover, rising awareness of comprehensive cancer screening is fueling demand for imaging-based diagnostics.

- By Technology

On the basis of technology, the market is segmented into sequencing, polymerase chain reaction (PCR), and microarray. The sequencing segment dominated the market with the largest revenue share in 2025, driven by the widespread adoption of next-generation sequencing technologies. Sequencing enables comprehensive analysis of multiple genes, making it essential for hereditary cancer testing. Continuous technological advancements are reducing costs and improving accuracy, encouraging broader adoption. The ability to detect rare and complex mutations further strengthens its clinical value. In addition, increasing research and development activities in genomics are supporting segment growth. The growing demand for precision medicine is also accelerating the use of sequencing technologies.

The polymerase chain reaction (PCR) segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by its high sensitivity, speed, and cost-effectiveness for targeted genetic testing. PCR is widely used for detecting specific mutations and validating sequencing results. Its rapid turnaround time makes it suitable for clinical applications requiring quick results. Increasing adoption in diagnostic laboratories and research settings is driving segment growth. Technological improvements are enhancing PCR accuracy and expanding its applications. Furthermore, rising demand for affordable testing solutions is contributing to its increasing adoption.

- By Disease Type

On the basis of disease type, the market is segmented into hereditary breast & ovarian cancer syndrome, Cowden syndrome, Lynch syndrome, hereditary leukemia and hematologic malignancies syndromes, familial adenomatous polyposis (FAP), Li-Fraumeni syndrome, von Hippel-Lindau disease, and multiple endocrine neoplasias (MEN) syndromes. The hereditary breast & ovarian cancer syndrome segment dominated the market with the largest revenue share in 2025, driven by the high prevalence of BRCA1 and BRCA2 gene mutations. Increasing awareness campaigns and screening programs are encouraging early detection of these cancers. The availability of targeted therapies for BRCA mutations is further boosting testing demand. Strong clinical guidelines recommending genetic testing for high-risk individuals also support segment dominance. In addition, growing patient awareness and physician recommendations are driving adoption. Continuous research in breast and ovarian cancer genetics is further strengthening the segment.

The Lynch syndrome segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing awareness of hereditary colorectal cancer risks. Advances in genetic testing are improving the detection of mismatch repair gene mutations associated with Lynch syndrome. Rising adoption of preventive screening programs is also contributing to segment growth. Healthcare providers are increasingly recommending testing for patients with a family history of colorectal cancer. The growing focus on early diagnosis and personalized treatment is further boosting demand. In addition, increasing research and funding in colorectal cancer genetics are supporting segment expansion.

- By End User

On the basis of end user, the market is segmented into hospitals, clinics, laboratories, radiology centers, diagnostic centers, and others. The hospitals segment dominated the market with the largest revenue share in 2025, driven by the availability of advanced diagnostic infrastructure and integrated care services. Hospitals serve as primary centers for cancer diagnosis, treatment, and genetic counseling. The presence of multidisciplinary teams enhances the adoption of hereditary cancer testing. Increasing patient inflow and demand for comprehensive care further support segment dominance. In addition, strong reimbursement frameworks in North America are facilitating testing in hospital settings. Continuous investments in healthcare infrastructure are also contributing to growth.

The laboratories segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the rising demand for specialized genetic testing services. Independent and reference laboratories are increasingly adopting advanced genomic technologies to offer high-quality testing. The growing trend of outsourcing diagnostic services is driving demand for laboratory-based testing. Increasing partnerships between hospitals and laboratories are further supporting growth. Technological advancements are improving testing efficiency and scalability. Moreover, rising demand for cost-effective and accurate diagnostic solutions is boosting the segment.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender and retail sales. The direct tender segment dominated the market with the largest revenue share in 2025, driven by bulk procurement by hospitals, healthcare institutions, and government organizations. Direct tendering ensures cost efficiency and consistent supply of testing kits and services. Large healthcare networks prefer this channel for streamlined procurement processes. The presence of long-term contracts with diagnostic companies further supports segment dominance. In addition, increasing government initiatives for cancer screening programs are boosting demand through direct tenders. The growing focus on preventive healthcare is also contributing to segment growth.

The retail sales segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing availability of direct-to-consumer genetic testing kits. Consumers are becoming more proactive about understanding their genetic risks, leading to higher demand for retail testing options. The convenience of at-home testing and online purchasing is supporting segment expansion. Advancements in digital health platforms are further facilitating access to genetic testing services. Increasing awareness about hereditary cancer risks is also driving adoption. Furthermore, the growing trend of personalized healthcare is contributing to the rapid growth of retail sales channels.

North America Hereditary Cancer Testing Market Regional Analysis

- The United States dominated the hereditary cancer testing market in North America with the largest revenue share of 82.4% in 2025, characterized by advanced healthcare infrastructure, strong reimbursement frameworks, and a high adoption of next-generation sequencing technologies

- Consumers and healthcare providers in the region highly value the clinical benefits, accuracy, and personalized insights offered by hereditary cancer testing, along with its integration into advanced healthcare systems and digital health platforms

- This widespread adoption is further supported by advanced healthcare infrastructure, favorable reimbursement policies, and a strong presence of key industry players, along with a technologically advanced population and increasing focus on early diagnosis and risk assessment, establishing hereditary cancer testing as a preferred solution for both clinical and preventive oncology settings

U.S. Hereditary Cancer Testing Market Insight

The United States hereditary cancer testing market captured the largest revenue share in 2025 within North America, fueled by the strong adoption of precision medicine and the expanding use of genetic screening in oncology care. Patients and healthcare providers are increasingly prioritizing early detection of inherited cancer risks through advanced genomic testing solutions. The growing preference for personalized treatment planning, combined with robust demand for next-generation sequencing and genetic counseling services, further propels the market. Moreover, the increasing integration of digital health platforms and AI-driven genomic analysis is significantly contributing to the market's expansion.

Canada Hereditary Cancer Testing Market Insight

The Canada hereditary cancer testing market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness of genetic disorders and supportive government healthcare initiatives. The rising prevalence of cancer, coupled with the demand for early diagnosis and preventive healthcare, is fostering the adoption of hereditary cancer testing. Canadian healthcare systems are also emphasizing precision medicine and expanding access to genetic counseling services. The country is experiencing significant growth across hospitals and diagnostic laboratories, with genetic testing being increasingly integrated into routine clinical practices and screening programs.

Mexico Hereditary Cancer Testing Market Insight

The Mexico hereditary cancer testing market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by improving healthcare infrastructure and increasing awareness regarding hereditary cancer risks. In addition, rising investments in diagnostic technologies are encouraging the adoption of genetic testing services. The country’s expanding healthcare access, along with growing demand for early detection solutions, is expected to continue to stimulate market growth. The integration of genetic testing into clinical settings and the expansion of private diagnostic laboratories are further supporting the development of the market in Mexico.

North America Hereditary Cancer Testing Market Share

The North America Hereditary Cancer Testing industry is primarily led by well-established companies, including:

- F. Hoffmann-La Roche Ltd (Switzerland)

- QIAGEN (Netherlands)

- Illumina, Inc. (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Abbott (U.S.)

- Danaher (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Eurofins Scientific (Luxembourg)

- Myriad Genetics, Inc. (U.S.)

- Invitae Corporation (U.S.)

- Agilent Technologies, Inc. (U.S.)

- Quest Diagnostics Incorporated (U.S.)

- Fulgent Genetics, Inc. (U.S.)

- Natera, Inc. (U.S.)

- Exact Sciences Corporation (U.S.)

- Guardant Health, Inc. (U.S.)

- BGI Genomics Co., Ltd. (China)

- Macrogen, Inc. (South Korea)

- MedGenome Labs Ltd. (India)

- Strand Life Sciences Pvt Ltd (India)

What are the Recent Developments in North America Hereditary Cancer Testing Market?

- In January 2026, researchers published findings through American Society of Clinical Oncology emphasizing expanded education programs for BRCA1/2 genetic testing among healthcare providers in North America, aiming to improve identification of high-risk patients. The initiative focuses on enhancing physician awareness and optimizing referral pathways for hereditary cancer testing

- In September 2025, the Association of Community Cancer Centers highlighted the expansion of hereditary cancer genetic testing programs across North America during Hereditary Cancer Awareness Week, emphasizing the growing adoption of early screening initiatives and preventive oncology strategies. The initiative underscored how early identification of inherited mutations enables proactive surveillance and risk-reduction interventions, reflecting a significant shift toward precision medicine in cancer care

- In July 2025, 23andMe completed the transition of its assets to a nonprofit entity following its acquisition, raising significant attention around the future of direct-to-consumer genetic testing services, including hereditary cancer screening. The move triggered discussions among regulators and healthcare stakeholders regarding genetic data privacy, accessibility, and long-term sustainability of consumer-based genetic testing models

- In March 2024, updated best-practice guidelines for hereditary breast and ovarian cancer (HBOC) genetic testing were published in European Molecular Genetics Quality Network journal collaborations, influencing laboratories and clinical practices globally, including North America. These guidelines incorporated advancements in multi-gene panel testing and variant interpretation, helping standardize testing quality and improve diagnostic accuracy

- In September 2023, the U.S. Food and Drug Administration (FDA) granted de novo marketing authorization for the Invitae Common Hereditary Cancers Panel, a first-of-its-kind blood-based genetic test capable of analyzing 47 genes associated with inherited cancer risk. The test enables healthcare providers to assess predisposition to multiple cancer types through a single assay, improving early detection and personalized risk management

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.