North America Infectious Disease Diagnostics Market

Market Size in USD Billion

USD

8.98 Billion

USD

15.39 Billion

2025

2033

USD

8.98 Billion

USD

15.39 Billion

2025

2033

| 2026 - 2033 | |

| USD 8.98 Billion | |

| USD 15.39 Billion | |

| % | |

|

North America Infectious Disease Diagnostics Market Size

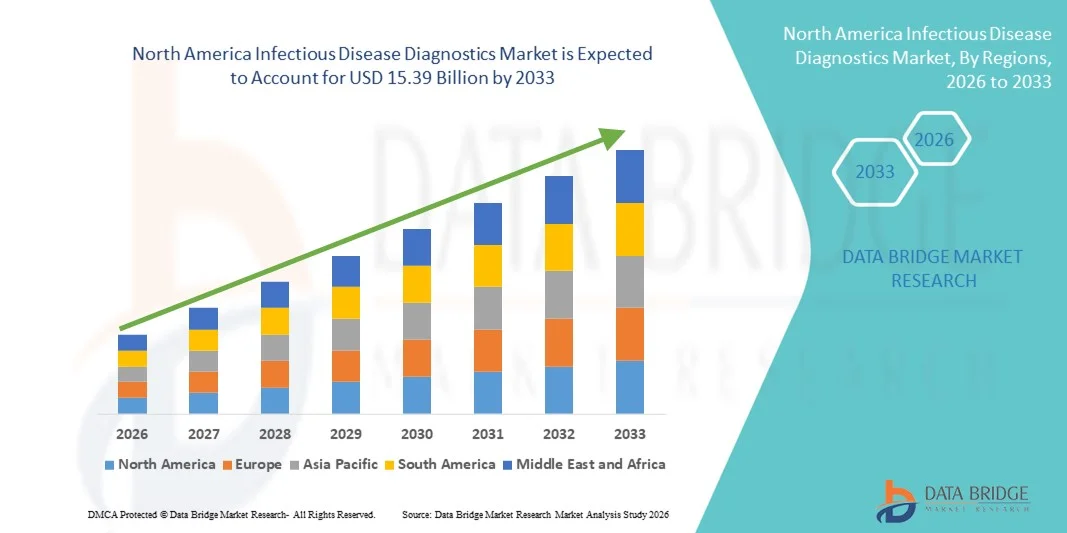

- The North America infectious disease diagnostics market size was valued at USD 8.98 billion in 2025 and is expected to reach USD 15.39 billion by 2033, at a CAGR of 6.90% during the forecast period

- The market growth is largely fueled by the increasing prevalence of infectious diseases, rising demand for rapid and accurate diagnostic solutions, and continuous technological advancements in molecular diagnostics and point-of-care testing, leading to improved disease detection and surveillance across hospitals, diagnostic laboratories, and community healthcare settings

- Furthermore, growing government initiatives for disease control and prevention, expanding healthcare infrastructure, increased funding for public health programs, and rising awareness regarding early diagnosis are accelerating the adoption of infectious disease diagnostic solutions, thereby significantly boosting the industry's growth

North America Infectious Disease Diagnostics Market Analysis

- Infectious disease diagnostics solutions, including molecular assays, immunoassays, and rapid point-of-care tests, are increasingly vital components of modern healthcare systems in both hospital and decentralized settings due to their ability to enable early detection, timely treatment decisions, and effective disease surveillance

- The escalating demand for infectious disease diagnostics is primarily fueled by the rising prevalence of viral and bacterial infections, growing awareness regarding early diagnosis, expanding screening programs, and increasing emphasis on outbreak preparedness and pandemic response

- The U.S. dominated the Infectious Disease Diagnostics market with the largest revenue share of 39.6% in 2025, characterized by advanced laboratory infrastructure, strong adoption of molecular diagnostic technologies, high healthcare expenditure, and the presence of leading diagnostic companies, with substantial growth in hospital-based and point-of-care testing across the country

- Canada is expected to be the fastest-growing country in the Infectious Disease Diagnostics market during the forecast period, expanding at a CAGR of 8.7% from 2026 to 2033, driven by increasing investments in public health infrastructure, rising demand for rapid testing solutions, expansion of diagnostic laboratories, and supportive government initiatives aimed at strengthening infectious disease monitoring and prevention

- The laboratory segment held the largest market revenue share of 62.3% in 2025, owing to high testing volumes and availability of advanced diagnostic infrastructure

Report Scope and Infectious Disease Diagnostics Market Segmentation

|

Attributes |

Infectious Disease Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

North America Infectious Disease Diagnostics Market Trends

Advancements in Molecular Diagnostics and Rapid Point-of-Care Testing

- A major and accelerating trend in the infectious disease diagnostics market is the growing adoption of advanced molecular diagnostic technologies and rapid point-of-care (POC) testing solutions. These innovations are transforming how infectious diseases are detected, monitored, and managed across healthcare systems worldwide

- For instance, the widespread use of RT-PCR–based diagnostic platforms during the COVID-19 pandemic significantly enhanced testing capabilities and set a benchmark for rapid molecular diagnostics in diseases such as influenza, tuberculosis, and HIV. Similarly, compact POC molecular systems such as Cepheid’s GeneXpert have enabled near-patient testing with high sensitivity and faster turnaround times

- The increasing integration of multiplex assays, which allow simultaneous detection of multiple pathogens from a single sample, is further strengthening diagnostic efficiency. This is particularly beneficial in respiratory and gastrointestinal infections where symptoms overlap, enabling clinicians to differentiate between viral and bacterial infections accurately and initiate appropriate treatment promptly

- Furthermore, technological advancements in isothermal amplification methods and CRISPR-based diagnostic platforms are contributing to faster, cost-effective, and highly specific disease detection. These technologies reduce dependency on centralized laboratories and enable decentralized testing in rural and resource-limited settings

- The shift toward home-based and self-testing kits is also gaining traction, especially for conditions such as HIV and COVID-19. These kits enhance accessibility, reduce healthcare burden, and promote early disease detection, thereby improving overall public health outcomes

- Overall, the continuous innovation in rapid, portable, and highly sensitive diagnostic tools is reshaping clinical decision-making processes and strengthening disease surveillance systems globally

North America Infectious Disease Diagnostics Market Dynamics

Driver

Rising Prevalence of Infectious Diseases and Growing Awareness of Early Diagnosis

- The increasing global burden of infectious diseases remains a primary driver fueling demand in the infectious disease diagnostics market

- The emergence of new pathogens, re-emergence of previously controlled infections, and rising antimicrobial resistance are intensifying the need for accurate and timely diagnostic solutions

- For instance, according to global health agencies, tuberculosis, malaria, HIV/AIDS, and seasonal influenza continue to affect millions annually, while emerging outbreaks such as COVID-19 and monkeypox have underscored the importance of rapid diagnostic preparedness. Governments worldwide significantly expanded diagnostic infrastructure during the pandemic, creating long-term growth momentum for the market

- Growing public and clinical awareness regarding the importance of early disease detection is further accelerating adoption. Early and precise diagnosis enables timely treatment initiation, reduces transmission rates, and minimizes healthcare costs associated with advanced-stage disease management

- In addition, increasing healthcare expenditure, improvements in laboratory infrastructure, and supportive government initiatives aimed at strengthening disease surveillance programs are contributing to market expansion. Many countries are investing in national screening programs for HIV, hepatitis, and other communicable diseases to curb large-scale transmission

- The expansion of diagnostic laboratories in developing economies and the integration of digital health technologies for reporting and tracking infectious diseases are also supporting market growth. These efforts enhance epidemiological monitoring and enable faster response to potential outbreaks

- Collectively, the rising incidence of infectious diseases combined with heightened emphasis on early, accurate diagnosis is substantially propelling the growth of the Infectious Disease Diagnostics market

Restraint/Challenge

High Testing Costs and Limited Access in Low-Resource Settings

- Despite technological advancements, the high cost associated with advanced diagnostic platforms and molecular testing remains a significant challenge for widespread adoption, particularly in low- and middle-income countries. The installation, maintenance, and calibration of sophisticated equipment require substantial financial investment

- For instance, molecular diagnostic systems such as real-time PCR platforms and automated analyzers involve considerable capital expenditure, limiting their accessibility in rural clinics and smaller healthcare facilities. In addition, recurring costs related to reagents and consumables further increase the overall financial burden

- Limited laboratory infrastructure and shortage of skilled healthcare professionals in underdeveloped regions also hinder effective implementation of advanced diagnostic technologies. In many remote areas, lack of electricity stability, cold chain storage, and trained technicians restrict reliable testing services

- Furthermore, regulatory complexities and delays in product approvals can slow the introduction of innovative diagnostic solutions into new markets. Variations in regulatory standards across countries create additional compliance challenges for manufacturers

- Data management and integration challenges, especially in regions lacking digital health frameworks, can affect efficient disease reporting and surveillance. Without streamlined data systems, real-time monitoring of infectious outbreaks becomes difficult

- Addressing these challenges through cost reduction strategies, public-private partnerships, infrastructure development, and capacity-building initiatives will be essential to ensure equitable access and sustained growth in the Infectious Disease Diagnostics market

North America Infectious Disease Diagnostics Market Scope

The market is segmented on the basis of product, test, technology, techniques, condition, and end user.

- By Product

On the basis of product, the Infectious Disease Diagnostics market is segmented into reagents, assays, and instrument. The reagents segment dominated the largest market revenue share of 44.5% in 2025, driven by their recurrent usage across diagnostic procedures and continuous demand in laboratories and hospitals. Reagents are essential consumables in PCR, immunoassays, and microbiology testing, ensuring steady revenue generation. The growing volume of infectious disease testing globally significantly supports segment growth. High testing frequency for viral and bacterial infections increases repeat purchases. Expansion of diagnostic laboratories and screening programs further fuels demand. Technological advancements in reagent formulations enhance sensitivity and specificity. Government initiatives promoting early disease detection contribute to higher reagent consumption. Increasing outbreaks and pandemics amplify demand for reliable reagents. The rise in point-of-care testing also boosts reagent usage. Strong distribution networks ensure product availability worldwide. Cost-effectiveness compared to capital equipment supports dominance. Continuous product innovation further consolidates the segment’s leading position.

The instrument segment is expected to witness the fastest CAGR of 10.8% from 2026 to 2033, driven by increasing automation and adoption of advanced molecular diagnostic platforms. Growing demand for high-throughput testing systems accelerates installations in hospitals and diagnostic labs. Technological advancements in PCR and NGS platforms enhance efficiency and accuracy. Rising investments in healthcare infrastructure, particularly in emerging economies, boost instrument procurement. Integration of AI-based analytics with diagnostic instruments supports rapid results interpretation. Government funding for laboratory modernization further stimulates growth. Demand for compact and portable devices in point-of-care settings contributes to expansion. Increasing focus on infection control and surveillance drives adoption. Collaborations between manufacturers and healthcare providers strengthen market penetration. The shift toward centralized and automated laboratories enhances instrument demand. Expanding molecular testing capabilities further accelerate growth. Continuous R&D investments ensure technological upgrades, supporting the segment’s rapid CAGR.

- By Test

On the basis of test, the market is segmented into laboratory and POC. The laboratory segment held the largest market revenue share of 62.3% in 2025, owing to high testing volumes and availability of advanced diagnostic infrastructure. Laboratories provide comprehensive and high-accuracy diagnostic services. Centralized testing ensures quality control and standardized results. Increasing prevalence of infectious diseases drives higher sample processing. Government screening programs further support laboratory dominance. Advanced molecular platforms are primarily housed in laboratories. Skilled professionals and established protocols enhance reliability. Integration of automated systems boosts efficiency. Strong reimbursement frameworks in developed regions sustain growth. Expansion of reference labs strengthens capacity. Growing research activities in infectious diseases further support demand. Rising awareness about early diagnosis consolidates segment leadership.

The POC segment is anticipated to register the fastest CAGR of 12.6% from 2026 to 2033, fueled by the need for rapid and decentralized testing. Increasing demand for immediate results enhances adoption in clinics and remote settings. Technological advancements improve accuracy of portable devices. Growing focus on outbreak management supports POC usage. Home healthcare trends drive demand for self-testing kits. Reduced turnaround time enhances patient management. Expanding healthcare access in rural areas accelerates growth. Government initiatives promoting rapid diagnostics strengthen adoption. Cost-effectiveness and ease of use boost preference. Rising awareness regarding early detection contributes to demand. Integration with digital health platforms enhances tracking. Continuous product innovation supports strong growth trajectory.

- By Technology

On the basis of technology, the market is segmented into immunodiagnostics, microbiology, PCR, NGS, and INAAT. The PCR segment dominated with a market share of 28.9% in 2025, driven by its high sensitivity and specificity in pathogen detection. PCR is widely used for viral infections and emerging pathogens. Growing molecular testing adoption enhances demand. Automation and real-time PCR advancements improve efficiency. Regulatory approvals for multiple assays strengthen adoption. Rising investments in molecular diagnostics fuel expansion. Increasing global outbreaks support PCR utilization. Clinical accuracy and rapid turnaround drive preference. Expansion of hospital molecular labs boosts growth. Integration with multiplex testing platforms enhances efficiency. Research institutions rely heavily on PCR-based methods. Strong reimbursement policies further sustain dominance.

The NGS segment is projected to grow at the fastest CAGR of 13.4% from 2026 to 2033, driven by its capability for comprehensive pathogen profiling. Increasing use in surveillance and outbreak tracing supports growth. Falling sequencing costs enhance accessibility. Personalized medicine initiatives accelerate adoption. Research funding in genomics boosts demand. Advanced bioinformatics tools strengthen data interpretation. Expansion of precision diagnostics supports uptake. Growing collaborations between biotech firms and hospitals accelerate innovation. Emerging applications in antimicrobial resistance detection drive growth. Rising awareness of genomic technologies supports expansion. Government initiatives in genomic surveillance enhance market penetration. Continuous technological improvements further propel segment growth.

- By Techniques

On the basis of techniques, the market is segmented into conventional techniques, biochemical techniques, and molecular techniques. The molecular techniques segment dominated with 47.2% revenue share in 2025, owing to high diagnostic accuracy and rapid turnaround time. Molecular methods such as PCR and other nucleic acid amplification tests are widely adopted for precise pathogen identification. Increasing prevalence of infectious diseases globally supports sustained demand. Automation in molecular platforms improves throughput and operational efficiency. Growing investments in advanced laboratory infrastructure further accelerate adoption. Strong regulatory approvals and clinical validation enhance physician confidence. Rising focus on early and accurate disease detection strengthens utilization. Integration with digital reporting systems streamlines workflow. Expansion of hospital-based molecular laboratories supports growth. Government funding for infectious disease surveillance programs further drives demand. Continuous R&D in molecular assays enhances sensitivity and specificity. Increasing awareness regarding precision diagnostics consolidates the segment’s leading market position.

The biochemical techniques segment is expected to grow at the fastest CAGR of 9.7% from 2026 to 2033, driven by advancements in rapid antigen and antibody-based detection technologies. These techniques are increasingly preferred for cost-effective mass screening programs. Growing demand in emerging economies supports expansion due to affordability. Rising focus on decentralized and community-based testing enhances adoption. Continuous technological improvements improve assay reliability and performance. Expanding use in point-of-care settings accelerates growth. Public health initiatives promoting early diagnosis further stimulate uptake. Minimal infrastructure requirements make biochemical methods suitable for rural areas. Increasing awareness of preventive healthcare strengthens demand. Collaborations between diagnostic firms and healthcare providers enhance accessibility. Rapid test kits gain popularity due to ease of use and quick results. Ongoing innovation ensures sustained segment growth over the forecast period.

- By Condition

On the basis of condition, the market is segmented into bacterial infection, viral infection, CNS infections, cardiovascular infection, fungal infection, GI infections, sexually transmitted disease, and others. The viral infection segment dominated with 36.8% share in 2025, due to the high global burden of respiratory and blood-borne viral diseases. Frequent outbreaks significantly increase diagnostic testing volumes. Government vaccination and screening programs further stimulate demand. Advanced molecular and immunodiagnostic tools enhance detection accuracy. Rising awareness regarding early viral detection supports routine screening. Expansion of hospital and laboratory networks strengthens capacity. Increased funding for infectious disease control programs drives growth. Strong regulatory support for viral diagnostic kits enhances penetration. Growing research on emerging viral strains supports innovation. Adoption of rapid testing platforms boosts accessibility. Integration with digital health systems improves monitoring efficiency. Continuous global travel and urbanization sustain testing demand.

The sexually transmitted disease segment is projected to grow at the fastest CAGR of 11.5% from 2026 to 2033, driven by rising global prevalence and increasing awareness initiatives. Government and NGO-led screening campaigns promote regular testing. Growing acceptance of confidential and at-home STD testing solutions accelerates adoption. Expansion of sexual health clinics enhances accessibility. Technological advancements in rapid and molecular STD diagnostics improve reliability. Increasing youth population and changing lifestyle patterns contribute to higher testing rates. Public health campaigns emphasizing preventive care enhance growth. Integration of telehealth services improves patient convenience. Rising investment in preventive healthcare strengthens demand. Availability of affordable testing kits in emerging markets boosts uptake. Improved reimbursement frameworks in developed countries further support expansion. Continuous innovation and awareness programs sustain strong CAGR growth.

- By End User

On the basis of end user, the market is segmented into diagnostic laboratories, academic and medical institutes, contract research organizations, hospitals and surgical centers, ambulatory clinics, and home healthcare. The diagnostic laboratories segment held the largest revenue share of 41.7% in 2025, supported by high testing volumes and advanced infrastructure. Laboratories offer comprehensive testing capabilities across multiple infectious conditions. Availability of skilled professionals ensures reliable results. Integration of automated systems improves efficiency and turnaround time. Government and private healthcare funding strengthens laboratory capacity. Expansion of reference laboratories enhances large-scale processing capabilities. Growing partnerships with hospitals and clinics boost sample inflow. Adoption of advanced molecular platforms drives dominance. Strong quality control protocols ensure standardized outcomes. Rising demand for confirmatory and specialized testing supports growth. Favorable reimbursement policies further sustain services. Increasing focus on centralized diagnostic systems consolidates market leadership.

The home healthcare segment is anticipated to register the fastest CAGR of 12.1% from 2026 to 2033, driven by growing self-testing adoption and telehealth integration. Increasing consumer preference for convenient and private diagnostic solutions supports expansion. Technological advancements enable accurate at-home rapid diagnostic kits. Telemedicine platforms facilitate remote consultation and interpretation. Rising awareness of preventive healthcare boosts self-screening trends. Expansion of e-commerce channels improves accessibility. Government initiatives encouraging decentralized healthcare further stimulate growth. Growing elderly population increases demand for home-based monitoring. Reduced hospital visits and cost savings enhance patient preference. Integration of smartphone applications with diagnostic kits improves usability. Pandemic-driven behavioral shifts toward home testing continue to influence adoption. Continuous product innovation sustains strong segment CAGR throughout the forecast period.

North America Infectious Disease Diagnostics Market Regional Analysis

- North America dominated the Infectious Disease Diagnostics market with the largest revenue share in 2025, driven by its highly developed healthcare infrastructure, strong disease surveillance systems, and early adoption of advanced diagnostic technologies. The region benefits from significant healthcare expenditure, well-established laboratory networks, and continuous investments in research and development. Additionally, the rising prevalence of infectious diseases, including respiratory infections, HIV, hepatitis, and emerging viral outbreaks, has reinforced the need for rapid and accurate diagnostic solutions across hospitals, reference laboratories, and point-of-care settings

- The region’s growth is further supported by the widespread integration of molecular diagnostic platforms, automation in clinical laboratories, and the adoption of multiplex and rapid antigen testing solutions. Healthcare providers in North America emphasize early disease detection, outbreak control, and antimicrobial resistance monitoring, which collectively drive demand for innovative diagnostic assays and high-throughput testing systems

- Favorable reimbursement frameworks, strong regulatory support, and the presence of leading diagnostic manufacturers also contribute significantly to market expansion. Continuous technological advancements, including portable molecular devices and home-based infectious disease test kits, are strengthening access to timely diagnostics across both urban and semi-urban populations

U.S. Infectious Disease Diagnostics Market Insight

The U.S. infectious disease diagnostics market dominated the infectious disease diagnostics market with the largest revenue share of 39.6% in 2025, characterized by advanced laboratory infrastructure, strong adoption of molecular diagnostic technologies, high healthcare expenditure, and the presence of leading diagnostic companies. The country has demonstrated substantial growth in hospital-based and point-of-care testing, supported by continuous innovation in PCR-based assays, immunoassays, and next-generation sequencing platforms. Increasing investments in infectious disease surveillance programs, coupled with preparedness initiatives following recent global outbreaks, have further strengthened diagnostic capacity nationwide. Additionally, strong collaboration between public health agencies, research institutions, and private diagnostic companies enhances rapid response capabilities and ensures widespread availability of testing solutions across healthcare facilities.

Canada Infectious Disease Diagnostics Market Insight

Canada infectious disease diagnostics market is expected to be the fastest-growing country in the Infectious Disease Diagnostics market during the forecast period, expanding at a CAGR of 8.7% from 2026 to 2033. Growth in the country is driven by rising investments in public health infrastructure, increasing demand for rapid and decentralized testing solutions, and expansion of diagnostic laboratories across provinces. Supportive government initiatives focused on strengthening infectious disease monitoring, improving rural healthcare access, and enhancing pandemic preparedness are accelerating adoption of advanced diagnostic technologies. Furthermore, Canada’s emphasis on preventive healthcare strategies and early detection programs is expected to significantly contribute to sustained market growth throughout the forecast period.

North America Infectious Disease Diagnostics Market Share

The Infectious Disease Diagnostics industry is primarily led by well-established companies, including:

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Abbott Laboratories (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Danaher Corporation (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Becton, Dickinson and Company (U.S.)

- Siemens Healthineers AG (Germany)

- QIAGEN N.V. (Netherlands)

- Hologic, Inc. (U.S.)

- bioMérieux SA (France)

- Grifols, S.A. (Spain)

- PerkinElmer, Inc. (U.S.)

- Seegene Inc. (South Korea)

- Mindray Bio-Medical Electronics Co., Ltd. (China)

- Agilent Technologies, Inc. (U.S.)

- GenMark Diagnostics, Inc. (U.S.)

- QuidelOrtho Corporation (U.S.)

- Luminex Corporation (U.S.)

- Werfen (Spain)

- SD Biosensor, Inc. (South Korea)

Latest Developments in North America Infectious Disease Diagnostics Market

- In March 2025, bioMérieux received U.S. FDA 510(k) clearance for its VITEK COMPACT PRO system, an automated system for microorganism identification (ID) and antibiotic susceptibility testing (AST) that enhances clinical laboratories’ ability to diagnose infectious diseases and support antimicrobial resistance management

- In March 2025, Revvity, Inc. (through EUROIMMUN) launched the IDS i20 analytical platform, a fully automated chemiluminescence immunoassay (ChLIA) system that enables high-throughput infectious disease testing alongside other specialty assays — CE-marked and FDA listed for clinical diagnostics

- In April 2025, BD (Becton, Dickinson and Company) received U.S. FDA 510(k) approval for its Respiratory Viral Panel (RVP) for the BD MAX System, which rapidly differentiates influenza A, SARS-CoV-2, influenza B, and respiratory syncytial virus (RSV) from a single test — enhancing multiplex respiratory pathogen detection

- In July 2025, Seegene Inc. launched the STAgora infectious disease analytics platform, a next-generation system integrating real-time diagnostic data and statistical modeling to improve epidemiological insights and outbreak response capabilities

- In September 2024, Roche launched the cobas Respiratory flex test, powered by TAGS (Temperature-Activated Generation of Signal) technology, capable of identifying up to 12 respiratory pathogens from one patient sample, improving high-throughput molecular diagnostics performance in clinical labs

- In January 2024, QIAGEN introduced two new syndromic testing panels (Gastrointestinal Panel 2 and Meningitis/Encephalitis Panel) for its QIAstat-Dx system in India with CDSCO approval, expanding local access to multiplex diagnostics for critical infectious diseases

- In February 2023, Thermo Fisher Scientific announced the launch of its Applied Biosystems TaqPath PCR kits for a range of infectious diseases — including multi-drug-resistant tuberculosis (MTB MDR), hepatitis B (HBV), hepatitis C (HCV), and HIV — with regulatory licensing from India’s CDSCO to be manufactured locally with partner Mylab Discovery Solutions. These kits support screening, diagnosis, monitoring therapeutic response, and identifying genetic risk factors

- In April 2023, QIAGEN launched its QIAstat-Dx syndromic testing solution in Japan with a respiratory panel capable of detecting more than 20 pathogens from a single sample, strengthening syndromic infectious disease diagnostics in the Asia-Pacific region

- In June 2023, T2 Biosystems submitted an application to the U.S. FDA for Breakthrough Device designation for its Candida auris diagnostic test and announced plans to add this target to its FDA-cleared T2Candida Panel — a step toward broader rapid fungal diagnostics

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.