North America Instrument Cluster Market

Market Size in USD Billion

USD

2.51 Billion

USD

3.73 Billion

2025

2033

USD

2.51 Billion

USD

3.73 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.51 Billion | |

| USD 3.73 Billion | |

| % | |

|

North America Instrument Cluster Market Size

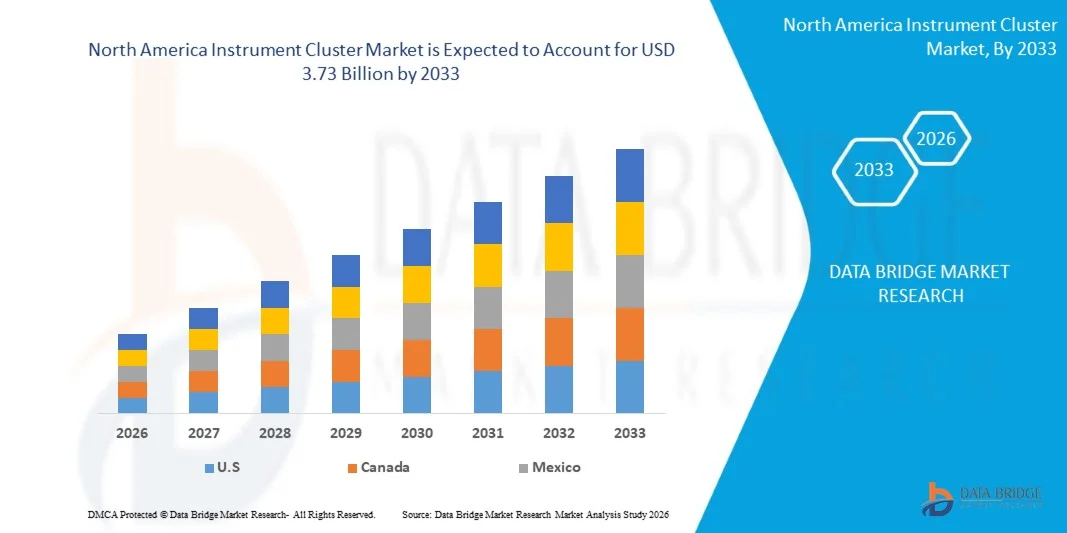

- The North America instrument cluster market size was valued at USD 2.51 billion in 2025 and is expected to reach USD 3.73 billion by 2033, at a CAGR of 5.10% during the forecast period

- The market growth is largely fuelled by the increasing integration of advanced driver assistance systems (ADAS) and digital cockpit technologies in modern vehicles

- Rising demand for enhanced vehicle aesthetics, real-time data visualization, and connected car features is further supporting market expansion

North America Instrument Cluster Market Analysis

- The market is experiencing steady growth driven by technological advancements in display systems such as TFT-LCD and OLED clusters, enabling improved user interface and driving experience

- Automakers are increasingly focusing on digitalization and customization of instrument clusters to enhance brand differentiation and driver engagement

- U.S. instrument cluster market captured the largest revenue share in 2025 within North America, driven by rapid advancements in automotive electronics and the growing trend of vehicle digitalization. Automakers are increasingly focusing on integrating advanced display systems and driver assistance features into vehicles

- Canada is expected to witness the highest compound annual growth rate (CAGR) in the North America instrument cluster market due to rising adoption of electric vehicles, growing investments in automotive innovation, and increasing demand for advanced driver assistance and digital display technologies

- The speedometer segment held the largest market revenue share in 2025 driven by its essential role in providing real-time vehicle speed information and ensuring compliance with safety regulations. Speedometers are a fundamental component in all vehicle types, supporting driver awareness and contributing to safe driving practices

Report Scope and North America Instrument Cluster Market Segmentation

|

Attributes |

North America Instrument Cluster Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

• Visteon Corporation (U.S.) |

|

Market Opportunities |

• Increasing Adoption Of Fully Digital Instrument Clusters |

|

Value Added Data Infosets |

to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

North America Instrument Cluster Market Trends

“Rising Demand for Digital And Connected Cockpit Systems”

• The increasing shift toward digitalization in the automotive industry is significantly shaping the North America instrument cluster market, as consumers and automakers prefer advanced display systems that provide real-time information, improved visibility, and enhanced user experience. Digital instrument clusters are gaining traction due to their ability to integrate navigation, vehicle diagnostics, and infotainment features within a single interface, strengthening their adoption across passenger and commercial vehicles and encouraging manufacturers to invest in innovative display technologies

• Growing consumer preference for connected vehicles and smart mobility solutions has accelerated the adoption of instrument clusters with advanced connectivity features. Drivers are increasingly seeking seamless integration with smartphones, voice assistants, and cloud-based services, prompting automakers to enhance functionality and customization. This has also led to collaborations between automotive OEMs and technology providers to develop intelligent cockpit solutions that improve convenience and driving efficiency

• Technological advancements in display technologies such as TFT-LCD and OLED are influencing purchasing decisions, with manufacturers emphasizing high-resolution graphics, flexible interfaces, and energy-efficient designs. These innovations are helping brands differentiate their offerings in a competitive market while improving driver engagement and safety. Companies are also focusing on software upgrades and over-the-air updates to maintain product relevance and performance over time

• For instance, in 2024, automakers such as Ford Motor Company and General Motors expanded their vehicle portfolios by incorporating advanced digital instrument clusters in new and upgraded models. These systems were introduced to enhance driver interaction, improve safety features, and support connected vehicle ecosystems, with availability across multiple vehicle segments. The solutions were also marketed as technologically advanced features, increasing consumer interest and brand loyalty

• While demand for digital instrument clusters is rising, sustained market growth depends on continuous innovation, cost optimization, and ensuring compatibility with evolving vehicle architectures. Manufacturers are focusing on improving system integration, cybersecurity, and scalability to meet changing consumer expectations and regulatory requirements

North America Instrument Cluster Market Dynamics

Driver

“Increasing Adoption Of Advanced Driver Assistance And Digital Display Technologies”

• The growing integration of advanced driver assistance systems and digital display technologies is a major driver for the North America instrument cluster market. Automakers are increasingly replacing analog clusters with digital interfaces to enhance safety, improve information accessibility, and support modern vehicle functionalities. This trend is also driving research into next-generation display solutions that offer higher performance and adaptability

• Expanding applications across passenger cars, electric vehicles, and commercial fleets are influencing market growth. Instrument clusters play a critical role in delivering essential driving data, alerts, and navigation support, enabling manufacturers to meet evolving consumer expectations for safety and convenience. The increasing shift toward electric and autonomous vehicles further reinforces this demand

• Automotive manufacturers are actively promoting advanced instrument cluster systems through product innovation, strategic partnerships, and technology integration. These efforts are supported by rising consumer demand for smart and connected vehicles, encouraging collaborations between OEMs and technology firms to enhance system capabilities and reduce development timelines

• For instance, in 2023, companies such as Tesla and Stellantis reported increased deployment of fully digital and customizable instrument clusters in their latest vehicle models. This expansion followed rising consumer demand for intelligent vehicle interfaces and enhanced driving experiences, driving product differentiation and repeat purchases. Both companies also emphasized software-driven features and connectivity to strengthen market positioning

• Although technological advancements support market growth, wider adoption depends on reducing production costs, ensuring system reliability, and maintaining user-friendly interfaces. Investment in software development, hardware optimization, and efficient manufacturing processes will be critical for sustaining long-term growth

Restraint/Challenge

“High Development Costs And Integration Complexity”

• The high cost associated with advanced instrument cluster systems remains a key challenge, limiting adoption among cost-sensitive vehicle segments. Expenses related to high-quality displays, software development, and system integration contribute to increased production costs. In addition, rapid technological advancements require continuous upgrades, further impacting cost efficiency

• Complexity in system integration and compatibility with existing vehicle architectures poses challenges for manufacturers. Ensuring seamless interaction between instrument clusters, infotainment systems, and ADAS components requires advanced engineering and testing, which can slow down product development cycles and increase time-to-market

• Supply chain disruptions and dependency on electronic components also impact market growth, as shortages of semiconductors and display panels can delay production and increase costs. Manufacturers must invest in supply chain resilience, strategic sourcing, and inventory management to mitigate these risks and maintain production continuity

• For instance, in 2024, several automotive manufacturers in the U.S. and Canada reported delays in vehicle production due to semiconductor shortages affecting digital instrument cluster systems. Companies also faced challenges in sourcing high-quality display components, leading to increased costs and extended delivery timelines. These issues impacted product availability and slowed market expansion

• Overcoming these challenges will require cost-effective manufacturing, improved supply chain management, and advancements in system integration technologies. Collaboration between automakers, component suppliers, and technology providers will be essential to enhance efficiency, reduce costs, and support long-term market growth

North America Instrument Cluster Market Scope

The market is segmented on the basis of utility, vehicle type, technology, enterprise size, and end-user.

• By Utility

On the basis of utility, the North America instrument cluster market is segmented into Speedometer, Odometer, Tachometer, Coolant Temperature Gauge, Oil Pressure Gauge, and Others. The speedometer segment held the largest market revenue share in 2025 driven by its essential role in providing real-time vehicle speed information and ensuring compliance with safety regulations. Speedometers are a fundamental component in all vehicle types, supporting driver awareness and contributing to safe driving practices.

The tachometer segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for performance monitoring and engine efficiency optimization. Tachometers are widely used in modern vehicles to provide precise engine RPM data, supporting better gear shifting decisions and enhancing overall vehicle performance and longevity.

• By Vehicle Type

On the basis of vehicle type, the market is segmented into ICE Vehicle, Battery Electric Vehicle (BEV), Plug-In Hybrid Electric Vehicle (PHEV), Hybrid Electric Vehicle (HEV), and Fuel Cell Electric Vehicle (FCEV). The ICE vehicle segment held the largest market revenue share in 2025 driven by the continued dominance of conventional vehicles and their widespread presence across the region. These vehicles rely heavily on traditional and digital instrument clusters for essential driving data and diagnostics.

The battery electric vehicle segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the rising adoption of electric mobility and supportive government initiatives. BEVs require advanced digital instrument clusters to display battery status, energy consumption, and range information, encouraging innovation in cluster design and functionality.

• By Technology

On the basis of technology, the market is segmented into Hybrid, Analog, and Digital. The digital segment held the largest market revenue share in 2025 driven by increasing consumer preference for advanced display systems and customizable interfaces. Digital instrument clusters offer enhanced visualization, integration with infotainment systems, and real-time data presentation, making them a preferred choice among automakers.

The hybrid segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the balance it offers between cost and functionality. Hybrid clusters combine analog elements with digital displays, providing improved user experience while maintaining affordability and ease of adoption.

• By Enterprise Size

On the basis of enterprise size, the market is segmented into Small-Scale Organization, Semi-Urban Mid-Scale Organization, and Large-Scale Organizations. The large-scale organizations segment held the largest market revenue share in 2025 driven by higher production capacity, strong R&D capabilities, and greater investment in advanced automotive technologies. These organizations play a key role in developing and deploying innovative instrument cluster solutions.

The semi-urban mid-scale organization segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing participation in automotive component manufacturing and rising demand for cost-effective solutions. These organizations are focusing on expanding production capabilities and adopting new technologies to remain competitive.

• By End-User

On the basis of end-user, the market is segmented into Passenger Cars, Commercial Vehicles, Two-Wheelers, Off-Highway Vehicle, Agriculture Vehicle, and Others. The passenger cars segment held the largest market revenue share in 2025 driven by high vehicle ownership rates and increasing demand for advanced in-vehicle technologies. Instrument clusters in passenger cars are evolving rapidly with the integration of digital and connected features.

The commercial vehicles segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the need for efficient fleet management and real-time vehicle monitoring. Instrument clusters in commercial vehicles provide critical data such as fuel efficiency, engine performance, and maintenance alerts, supporting operational efficiency and reducing downtime.

North America Instrument Cluster Market Regional Analysis

- U.S. instrument cluster market captured the largest revenue share in 2025 within North America, driven by rapid advancements in automotive electronics and the growing trend of vehicle digitalization. Automakers are increasingly focusing on integrating advanced display systems and driver assistance features into vehicles

- The rising demand for electric and autonomous vehicles, combined with strong consumer preference for connected car technologies and customizable digital interfaces, further propels the market

- Moreover, integration with advanced systems such as voice control, navigation, and real-time diagnostics is significantly contributing to market growth

Canada Instrument Cluster Market Insight

The Canada instrument cluster market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing adoption of electric vehicles and rising demand for technologically advanced automotive systems. Growing investments in automotive innovation and supportive government initiatives promoting clean mobility are accelerating market expansion. Consumers are increasingly preferring vehicles equipped with digital instrument clusters that offer enhanced safety, efficiency, and user experience. In addition, the expansion of connected vehicle infrastructure and rising awareness regarding advanced driver assistance systems are further supporting the growth of the instrument cluster market in Canada.

North America Instrument Cluster Market Share

The North America instrument cluster industry is primarily led by well-established companies, including:

• Visteon Corporation (U.S.)

• BorgWarner Inc. (U.S.)

• Aptiv PLC (Ireland)

• Lear Corporation (U.S.)

• Gentex Corporation (U.S.)

• Methode Electronics, Inc. (U.S.)

• L3Harris Technologies, Inc. (U.S.)

• Mercury Systems, Inc. (U.S.)

• Park-Ohio Holdings Corp. (U.S.)

• Sparton Corporation (U.S.)

• Celestica Inc. (Canada)

• Magna International Inc. (Canada)

• Linamar Corporation (Canada)

• Martinrea International Inc. (Canada)

• Ballard Power Systems Inc. (Canada)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

North America Instrument Cluster Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its North America Instrument Cluster Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as North America Instrument Cluster Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.