North America Invisible Orthodontics Market

Market Size in USD Billion

CAGR :

%

USD

4.65 Billion

USD

13.50 Billion

2025

2033

USD

4.65 Billion

USD

13.50 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.65 Billion | |

| USD 13.50 Billion | |

| % | |

|

North America Invisible Orthodontics Market Overview

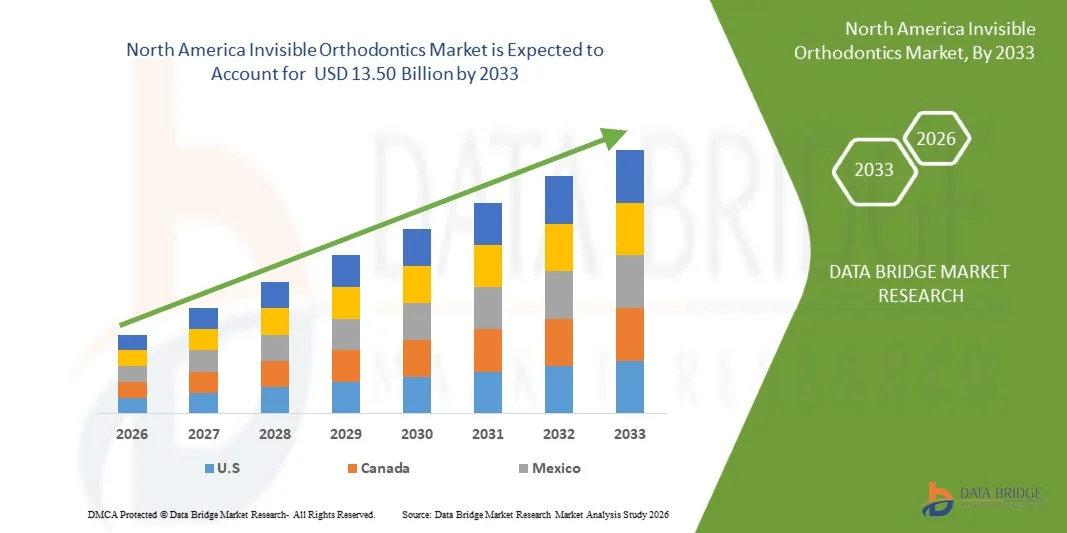

The North America invisible orthodontics market was valued at USD 4.65 billion in 2025 and is projected to reach USD 13.50 billion by 2033, growing at a CAGR of 14.30% from 2026 to 2033. The market is witnessing robust growth driven by increasing demand for aesthetically appealing dental treatments, rising awareness of oral health, and continuous advancements in clear aligner technologies. The growing preference for discreet orthodontic solutions among adults and teenagers, coupled with expanding digital dentistry adoption, is further accelerating market expansion.

The high prevalence of malocclusion and dental alignment disorders, along with rising disposable incomes and favorable reimbursement coverage in certain segments, is encouraging patients to opt for invisible orthodontic treatments. In addition, innovations in 3D scanning, AI-powered treatment planning, and customized aligner manufacturing are improving treatment outcomes and patient convenience, supporting widespread adoption across dental clinics and orthodontic practices throughout the region.

Key Market Trends & Insights

- North America held the largest revenue share of 38.7% in the invisible orthodontics market in 2025, supported by high adoption of advanced dental technologies, strong consumer awareness, and the presence of leading orthodontic solution providers.

- The Clear Aligners segment led the market with a 85.7% share in 2025, driven by increasing consumer preference for aesthetically appealing, removable, and comfortable orthodontic solutions, along with continuous advancements in digital treatment planning and 3D printing technologies

- Lingual Braces are the fastest-growing product type, projected to register a CAGR of 31.2% supported by technological advancements and increasing demand for nearly invisible treatment options among image-conscious consumers.

- The Adults segment dominated the age group category with a revenue share of 62.4% in 2025, driven by increasing awareness of cosmetic dentistry, higher spending capacity, and growing acceptance of orthodontic treatment among working professionals.

- Malocclusion dominated the application segment with highest revenue share in 2025, as it remains one of the most common dental alignment conditions requiring orthodontic intervention.

- Dental Clinics dominated the end-user segment in 2025, benefiting from a high volume of orthodontic procedures, widespread availability of specialized dental professionals, and increasing adoption of digital treatment planning technologies.

- Direct Sales dominated the distribution channel segment in 2025, as manufacturers increasingly collaborate directly with dental and orthodontic practices to improve product accessibility, training, and customer support.

Market Size & Forecast

- North America Market Value (2025): USD 4.65 Billion

- Expected Market Value (2033): USD 13.50 Billion

- Forecast CAGR (2026–2033): 14.30%

Report Scope and North America Invisible Orthodontics Market Segmentation

|

Attributes |

North America Invisible Orthodontics Key Market Insights |

|

Segments Covered |

· By Product Type: Clear Aligners, Ceramic Braces, and Lingual Braces, · By Age Group: Adults, Teenagers & Children, · By Application: Malocclusion, Crowding, Excessive Spacing & Others · By End User: Hospitals, Dental Clinics, Orthodontics Clinics & Others), · By Distribution Channel: Direct Sales & Third Party Distributors |

|

Countries Covered |

North America · U.S. · Canada · Mexico |

|

Key Market Players |

· Align Technology, Inc. (U.S.) · Dentsply Sirona (U.S.) · Envista (U.S.) · 3M (U.S.) · Henry Schein, Inc. (U.S.) · American Orthodontics (U.S.) · Institut Straumann AG (Switzerland) · Candid Care Co. (U.S.) · Great Lakes Dental Technologies (U.S.) · DynaFlex (U.S.) · G&H Orthodontics, Inc. (U.S.) · AlignerCo (U.S.) · OrthoFX (U.S.) · TP Orthodontics, Inc. (U.S.) · ClearPath Orthodontics (Pakistan) · Patterson Companies, Inc. (U.S.) |

|

Market Opportunities |

· Expansion of direct-to-consumer clear aligner and teleorthodontic treatment services · Increasing adoption of AI-powered treatment planning and digital dentistry technologies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

North America Invisible Orthodontics Market Trends

Trend: Rising Adoption of AI-Driven Digital Treatment Planning in Invisible Orthodontics

The growing integration of artificial intelligence and digital treatment planning technologies is emerging as a major trend in the North America invisible orthodontics market. Orthodontic providers and device manufacturers are increasingly leveraging AI-powered platforms to streamline aligner design, enhance diagnostic precision, and improve patient case acceptance — all without relying on traditional, time-intensive manual planning workflows. The deployment of AI-driven solutions is helping orthodontic practices expand treatment accessibility, reduce planning cycles, and deliver more personalized outcomes for patients across residential and clinical settings.

For instance, in October 2025, Align Technology, Inc. announced ClinCheck Live Plan, a new feature in its Invisalign digital treatment planning system that automates the generation of initial doctor-ready treatment plans within 15 minutes — reducing the Invisalign treatment planning cycle from days to minutes and enabling patients to start treatment faster.

In addition, according to an Overjet article published in April 2025, Overjet, a U.S.-based dental AI company, reported a 10–20% increase in treatment approvals following the adoption of its AI-powered imaging tools, which enhance diagnostic clarity by overlaying detailed annotations on dental scans, allowing patients to better understand their oral health and proposed aligner treatments. Furthermore, AI-driven treatment planning software utilizing machine learning in conjunction with 3D modelling is enhancing the predictability of orthodontic movements while reducing treatment time and increasing patient satisfaction. These advancements — spanning AI-based diagnostics, remote monitoring applications, and automated treatment planning — are collectively accelerating the adoption of invisible orthodontics across North America and reshaping the competitive landscape of the market.

North America Invisible Orthodontics Market Dynamics

Key Market Driver: Rising Prevalence of Malocclusion and Growing Aesthetic Consciousness

The rising prevalence of malocclusion and growing aesthetic consciousness among adults and teenagers are significantly driving demand for invisible orthodontic solutions across North America. Dental professionals, manufacturers, and patients are investing heavily in next-generation clear aligner technologies to support discreet, comfortable, and clinically effective teeth-straightening treatments. Increasing adoption of AI-driven treatment planning, 3D printing, and direct-to-consumer aligner platforms is further accelerating demand for advanced invisible orthodontic solutions capable of addressing a wide range of malocclusion cases.

For instance,

In May 2025, Align Technology Inc. introduced a new Invisalign system equipped with mandibular advancement and occlusal blocks in the U.S. and Canadian markets, marking a significant product milestone in addressing Class II malocclusions by simultaneously correcting tooth alignment and promoting lower jaw advancement.

Key Restraint/Challenge: High Treatment Cost and Limited Insurance Coverage

A major challenge in the North America invisible orthodontics market is the high cost associated with advanced clear aligner treatments and supporting digital orthodontic technologies. Premium invisible orthodontic solutions involving AI-driven treatment planning, 3D-printed custom aligners, and professional supervision entail substantial out-of-pocket expenditure. In addition, inconsistent insurance coverage, stringent regulatory requirements, and limited efficacy for complex malocclusion cases create barriers to widespread patient adoption.

For instance,

The average cost of clear aligners in the U.S. stands at USD 5,108, and while some insurance plans may cover up to USD 3,000, significant out-of-pocket expenses continue to restrict access for a large segment of the population.

Key Market Opportunity: Expansion of Manufacturing Infrastructure and Direct-to-Consumer Platforms

The increasing investment in domestic aligner manufacturing, tele-dentistry platforms, and AI-powered remote monitoring systems presents significant opportunities for the North America invisible orthodontics market. Growing adoption of direct-to-consumer models and advanced 3D printing technologies is enabling providers to improve treatment accessibility, reduce delivery timelines, and reach previously underserved patient populations across the region.

For instance,

In March 2025, Angel Aligner announced the establishment of its first U.S.-based manufacturing facility — a 52,000-square-foot center in Oak Creek, Wisconsin — equipped with automated, proprietary 3D printing technology, marking a significant expansion of clear aligner production capacity in North America.

North America Invisible Orthodontics Market Scope

The North America invisible orthodontics market is segmented on the basis of product type, age group, application, end user, and distribution channel.

- By Product Type

On the basis of product type, the North America invisible orthodontics market is segmented into clear aligners, ceramic braces, and lingual braces. The clear aligners segment held the largest market share of 85.7% in 2025, owing to its rising popularity as a comfortable, removable, and nearly invisible alternative to traditional metal braces. Increasing adoption of AI-driven treatment planning, 3D scanning, and direct-to-consumer marketing by key players has further strengthened segment dominance across both clinical and at-home treatment channels in North America.

The lingual braces segment is expected to witness the fastest CAGR of 31.2% over the forecast period, driven by their discreet placement behind the teeth, making them an attractive option for adults and professionals seeking invisible orthodontic solutions without compromising clinical outcomes. Growing technological innovations in custom bracket fabrication using 3D printing and AI-guided bonding tools are further accelerating adoption of lingual braces in premium orthodontic settings.

- By Age Group

On the basis of age group, the North America invisible orthodontics market is segmented into adults, teenagers, and children. The adult segment accounted for the highest market share of 62.4% in 2025, driven by growing aesthetic consciousness, financial autonomy, and rising social acceptance of adult orthodontic treatment. Increasing awareness that malocclusion impacts not only appearance but also oral health function has encouraged more adults to seek discreet and effective orthodontic correction through clear aligners and lingual braces.

The teenagers segment is anticipated to show the fastest growth over the forecast period, fueled by parental awareness of early orthodontic intervention, increasing incidence of malocclusion among adolescents, and strong demand for aesthetic alternatives to traditional metal braces during formative social years. The virtually invisible nature and removability of clear aligners make them especially popular among image-conscious teenage patients.

- By Application

On the basis of application, the North America invisible orthodontics market is segmented into malocclusion, crowding, excessive spacing, and others. The malocclusion segment accounts for the majority of the total market share, as it is a widespread issue affecting a significant portion of the global population, occurring in varying degrees of severity from mild to severe cases. The health implications of untreated malocclusion — including tooth decay, gum disease, TMJ disorders, and impaired chewing efficiency — drive patients to proactively seek invisible orthodontic solutions across clinical settings in North America.

The crowding segment is expected to witness the fastest CAGR over the forecast period, driven by the high prevalence of dental crowding among teenagers and adults, increasing availability of AI-customized clear aligner solutions for mild-to-moderate crowding cases, and growing patient preference for non-invasive treatment modalities over traditional extraction-based approaches.

- By End User

On the basis of end user, the North America invisible orthodontics market is segmented into hospitals, dental clinics, orthodontic clinics, and others. Dental and orthodontic clinics held a 71.2% share in 2025, leveraging clinical expertise, diagnostic imaging, and integrated CAD/CAM suites to deliver end-to-end personalized care. The strong presence of specialized orthodontists, growing adoption of intraoral scanners, and high patient preference for supervised in-office treatment continue to reinforce the segment's dominant position across North America.

The orthodontic clinics segment is expected to grow at a CAGR of 28.7%, driven by increasing consumer demand for specialized orthodontic treatments and advancements in invisible orthodontic technology. Rising investment in digital orthodontic workflows, AI-enabled case planning, and remote monitoring platforms is enabling orthodontic clinics to expand patient throughput and improve treatment outcomes efficiently.

- By Distribution Channel

On the basis of distribution channel, the North America invisible orthodontics market is segmented into direct sales and third-party distributors. The dentist-led direct sales channel dominated the market with a 82.4% revenue share of distribution channel in 2025, driven by strong institutional relationships between aligner manufacturers and dental professionals, bundled product-service offerings, and patient preference for clinically supervised treatment planning and monitoring across orthodontic and dental practices.

Third-party distributor segment is anticipated to witness the fastest CAGR of 16.6% CAGR during the forecast period, buoyed by teledentistry ordinances and lower entry costs. The growing proliferation of e-commerce platforms, expanding digital retail ecosystems, and increasing consumer appetite for at-home aligner solutions are further accelerating demand through third-party distribution channels across North America

North America Invisible Orthodontics Market Regional Analysis

North America dominated the invisible orthodontics market with a 45.8% share in 2024, supported by advanced dental healthcare infrastructure, strong investments in digital orthodontic technologies, and the presence of established aligner manufacturers and orthodontic networks. The region also benefits from high consumer spending on dental aesthetics, widespread adoption of AI-powered and 3D-printing-enabled treatment platforms, and growing use of clear aligners across adult, teenage, and direct-to-consumer channels. Increasing focus on discreet, comfortable treatment experiences and expanding teledentistry integration continues to strengthen North America's leadership position in the invisible orthodontics market.

U.S. Invisible Orthodontics Market Insight

The U.S. invisible orthodontics market is anticipated to grow at a CAGR of 23.2% between 2026 and 2033. The country's mature orthodontic ecosystem, along with increasing adoption of AI-driven treatment planning, intraoral scanning, and 3D printing technologies, is driving demand across clinical, direct-to-consumer, and research applications. In addition, growing awareness of the long-term health implications of untreated malocclusion — including difficulty chewing, speech issues, and increased risk of dental decay — is accelerating invisible orthodontic treatment adoption among adults and teenagers across dental clinics and standalone practices nationwide.

Canada Invisible Orthodontics Market Insight

The Canada invisible orthodontics market, growing at a CAGR of 27.5% from 2026 to 2033. The market remains a major contributor to regional revenue, driven by high dental care awareness, strong government support for oral health initiatives, and growing demand for advanced aesthetic treatment solutions. Canada is one of the most advanced countries in terms of dental care and services, with high awareness regarding the effectiveness and success of invisible orthodontics among the Canadian population, further supporting steady market expansion

North America Invisible Orthodontics Market Share

The North America Invisible Orthodontics industry is primarily led by well-established companies, including:

- Align Technology, Inc. (U.S.)

- Dentsply Sirona (U.S.)

- Envista (U.S.)

- 3M (U.S.)

- Henry Schein, Inc. (U.S.)

- American Orthodontics (U.S.)

- Institut Straumann AG (Switzerland)

- Candid Care Co. (U.S.)

- Great Lakes Dental Technologies (U.S.)

- DynaFlex (U.S.)

- G&H Orthodontics, Inc. (U.S.)

- AlignerCo (U.S.)

- OrthoFX (U.S.)

- TP Orthodontics, Inc. (U.S.)

- ClearPath Orthodontics (Pakistan)

- Patterson Companies, Inc. (U.S.)

Latest Developments in North America Invisible Orthodontics Market

- In April 2026, OrthoFX launched FXIntegrated Buttons, the industry's first fully manufactured buttons seamlessly formed within the aligner material — at the 2026 AAO Annual Session in Orlando. The one-piece design eliminates bonding steps, reduces chair time, enhances aligner durability, and improves patient comfort, significantly advancing treatment process efficiency and strengthening OrthoFX's competitive positioning in the North America invisible orthodontics market.

- In October 2025, Align Technology, Inc. announced ClinCheck Live Plan, an AI-powered feature automating initial Invisalign doctor-ready treatment plans within 15 minutes of case submission. Built on data from over 21 million patient cases, the innovation reduces planning cycles from days to minutes, accelerates case acceptance, and enhances practice workflow efficiency, reinforcing Align's leadership in AI-driven digital orthodontics across North America.

- In March 2025, Angel Aligner announced its first U.S. manufacturing facility in Oak Creek, Wisconsin, equipped with automated 3D printing technology. Generating nearly 200 jobs, the facility brings aligner production closer to North American customers, improving supply chain efficiency, reducing delivery timelines, and reinforcing Angel Aligner's long-term commitment to the North America invisible orthodontics market.

- In January 2024, Align Technology, Inc. completed the acquisition of Cubicure GmbH, a pioneer in direct 3D printing solutions, to enhance next-generation aligner manufacturing capabilities. Integrating Cubicure's advanced materials and processes into Align's platform improves aligner precision, production scalability, and material performance, further strengthening Align's manufacturing ecosystem and dominance in the North America clear aligner market.

- In November 2023, Vivos Therapeutics, Inc. announced a strategic partnership with Ormco Corporation's Spark Clear Aligner system to integrate VIVOS CARE devices with Spark Aligners, improving treatment time for complex malocclusion cases. The collaboration leverages Spark's TruGEN material and advanced treatment planning software, expanding the clinical applicability of Spark aligners and creating new growth avenues in North America's invisible orthodontics market.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.