North America Ldl Test Market

Market Size in USD Million

USD

847.20 Million

USD

1,340.15 Million

2025

2033

USD

847.20 Million

USD

1,340.15 Million

2025

2033

| 2026 - 2033 | |

| USD 847.20 Million | |

| USD 1,340.15 Million | |

| % | |

|

North America Low Density Lipoprotein (LDL) Test Market Size

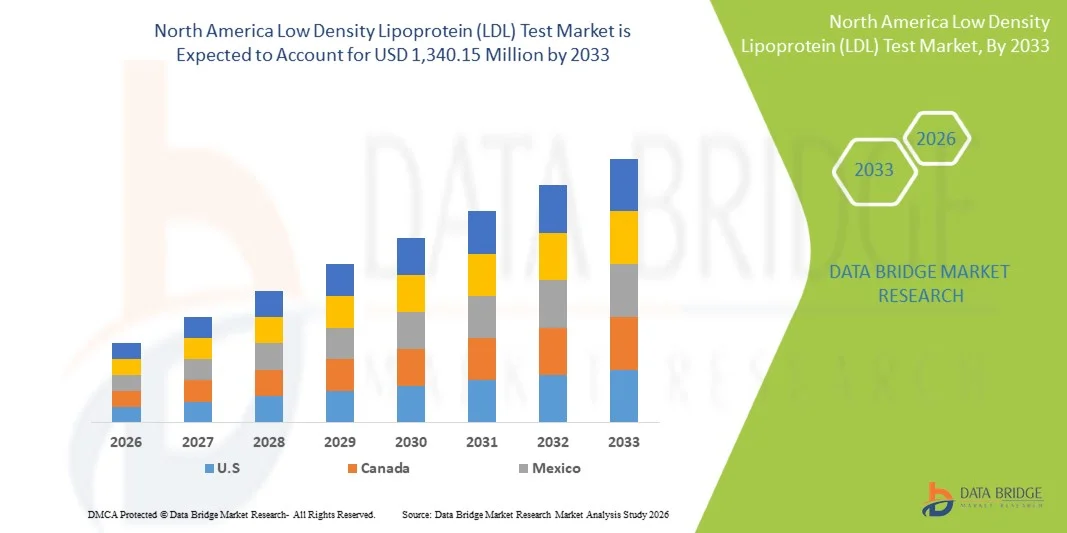

- The North America Low Density Lipoprotein (LDL) test market size was valued at USD 847.20 million in 2025 and is expected to reach USD 1,340.15 million by 2033, at a CAGR of 5.90% during the forecast period

- The market growth is primarily driven by the increasing prevalence of cardiovascular diseases and obesity, alongside a heightened focus on preventive healthcare and early diagnosis of lipid disorders across the region

- In addition, growing awareness of cholesterol management, coupled with technological advancements in lipid profiling and home-based diagnostic solutions, is enhancing adoption rates. These converging factors are accelerating the demand for LDL testing, thereby significantly propelling the market’s growth

North America Low Density Lipoprotein (LDL) Test Market Analysis

- Low Density Lipoprotein (LDL) tests, used to measure and monitor “bad cholesterol” levels, play a crucial role in diagnosing and managing cardiovascular diseases across hospitals, clinics, and diagnostic laboratories in North America

- The market’s expansion is primarily driven by the rising prevalence of atherosclerosis, obesity, diabetes, and other lipid-related disorders, coupled with an increasing focus on preventive healthcare and regular lipid monitoring programs among aging populations

- The United States dominated the North America LDL test market with the largest revenue share of 68.9% in 2025, supported by advanced diagnostic infrastructure, growing adoption of automated lipid analyzers, and the strong presence of leading biotechnology and healthcare firms

- Canada is projected to be the fastest-growing country in the LDL test market during the forecast period, driven by expanding government healthcare initiatives and growing public awareness of cholesterol-related health risks

- The Kits and Reagents segment dominated the market with the largest market share of 46.7% in 2025, attributed to their high consumption rate in routine testing and recurring demand across hospitals, clinics, and research laboratories

Report Scope and North America Low Density Lipoprotein (LDL) Test Market Segmentation

|

Attributes |

North America Low Density Lipoprotein (LDL) Test Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

North America Low Density Lipoprotein (LDL) Test Market Trends

“Integration of Advanced Diagnostics and AI-Based Lipid Profiling”

- A significant and accelerating trend in the North America LDL test market is the growing integration of artificial intelligence (AI) and advanced diagnostic analytics into lipid profiling systems. This advancement is enhancing the precision, efficiency, and predictive capability of LDL testing for cardiovascular risk assessment

- For instance, Abbott’s Alinity and Siemens Healthineers’ Atellica systems are incorporating AI algorithms to analyze lipid data, helping clinicians identify patients at risk of atherosclerosis and other cardiovascular conditions with higher accuracy

- AI-driven LDL testing platforms enable automated result interpretation, pattern recognition in lipid abnormalities, and intelligent alerts for potential disease risks. For instance, emerging diagnostic platforms from Roche and Beckman Coulter utilize AI for automated lipid profiling and quality control monitoring, reducing errors and improving workflow efficiency. Furthermore, machine learning-based insights are assisting physicians in designing personalized lipid management strategies

- The integration of AI into LDL testing also supports telemedicine and remote monitoring by enabling digital report sharing and predictive analytics. Through unified health data systems, laboratories and clinicians can monitor patient cholesterol levels alongside other biomarkers, enabling holistic cardiovascular health management

- This trend toward intelligent, data-driven, and interconnected testing systems is reshaping preventive healthcare approaches in North America. Consequently, companies such as Quest Diagnostics and Labcorp are developing AI-enhanced lipid analysis services with real-time reporting and digital health compatibility

- The demand for LDL tests integrated with AI-based analytics and automated reporting is growing rapidly across hospitals, clinics, and research laboratories, as healthcare providers increasingly prioritize precision diagnostics and preventive cardiovascular care

North America Low Density Lipoprotein (LDL) Test Market Dynamics

Driver

“Rising Cardiovascular Disease Burden and Emphasis on Preventive Screening”

- The increasing incidence of cardiovascular diseases, obesity, and diabetes across the U.S. and Canada, combined with a growing focus on early diagnosis and preventive healthcare, is a major driver fueling the demand for LDL testing in the region

- For instance, in February 2025, Abbott announced the expansion of its lipid testing solutions under the ARCHITECT platform to improve the accessibility and efficiency of cardiovascular diagnostic testing in clinical laboratories. Such initiatives by leading companies are expected to strengthen market growth during the forecast period

- As healthcare systems emphasize risk assessment and cholesterol management, LDL testing serves as a vital component in identifying patients requiring lifestyle interventions or lipid-lowering therapies, ensuring timely clinical decisions and improved patient outcomes

- Furthermore, the rising awareness of routine lipid screening and the adoption of advanced diagnostic instruments are making LDL testing a core part of preventive health programs across hospitals and clinics

- The convenience of automated analyzers, faster test turnaround times, and the increasing shift toward decentralized diagnostic solutions are propelling the adoption of LDL tests across multiple healthcare settings. The growing use of direct tenders by large hospital networks further contributes to steady market expansion

Restraint/Challenge

“Regulatory Complexity and Reimbursement Limitations”

- Stringent regulatory requirements governing in vitro diagnostic (IVD) devices and biochemical assays pose a significant challenge to the expansion of the LDL test market in North America. Delays in product approvals can limit the entry of innovative lipid testing solutions

- For instance, prolonged FDA clearance processes for new lipid analyzers and reagent kits often hinder timely commercialization, creating barriers for smaller manufacturers seeking market entry

- Addressing these regulatory challenges through improved validation frameworks, streamlined approval processes, and enhanced collaboration between manufacturers and regulatory bodies is essential for market progress. In addition, inconsistent reimbursement policies for preventive lipid testing across healthcare systems in the U.S. and Canada can discourage frequent screening

- For instance, variations in Medicare and private insurance coverage for lipid panels have led to disparities in patient access, particularly in low-income populations

- While technological advancements continue to improve the accuracy and efficiency of LDL testing, cost constraints and reimbursement gaps may restrict widespread adoption in smaller clinics and ambulatory care centers

- Overcoming these hurdles through supportive policies, cost-effective test development, and public health initiatives will be crucial for sustainable market growth

North America Low Density Lipoprotein (LDL) Test Market Scope

The market is segmented on the basis of type, component, disease, end user, and distribution channel.

- By Type

On the basis of type, the North America LDL test market is segmented into LDL-C, LDL-B, LDL-P, and Others. The LDL-C segment dominated the market with the largest revenue share of 46.5% in 2025, owing to its widespread clinical use as the standard parameter for cholesterol measurement and cardiovascular risk assessment. LDL-C testing is a key component of routine lipid panels across hospitals and diagnostic laboratories, aiding in the early detection and monitoring of coronary artery disease. Its reliability, cost-efficiency, and inclusion in preventive screening programs have made it the most utilized test type in the region. Moreover, continuous improvements in enzymatic and direct measurement assays have enhanced test accuracy and workflow efficiency. The growing burden of lifestyle-related conditions, such as obesity and diabetes, further sustains the high adoption of LDL-C testing.

The LDL-P segment is expected to witness the fastest growth rate of 8.9% from 2026 to 2033, driven by increasing recognition of particle-based lipid profiling as a more accurate predictor of cardiovascular events. LDL-P testing measures the number and size of lipoprotein particles, offering deeper diagnostic insights compared to LDL-C levels alone. The rising adoption of nuclear magnetic resonance (NMR) and ion mobility technologies in advanced laboratories supports this trend. Furthermore, growing research in personalized lipid management and the shift toward precision medicine are fueling LDL-P testing demand. The segment’s expansion is further supported by collaborations between diagnostic companies and cardiology clinics for advanced lipid analysis solutions.

- By Component

On the basis of component, the market is segmented into kits and reagents, devices, and services. The Kits and Reagents segment dominated the market with the largest share of 46.7% in 2025, attributed to their indispensable role in lipid quantification and frequent replenishment needs in laboratory workflows. These products are integral to routine LDL testing using both automated and manual assays, ensuring consistency and accuracy in diagnostic results. Advancements in reagent formulations, such as liquid-stable and ready-to-use systems, are improving laboratory efficiency and reducing turnaround times. Increasing test volumes driven by population health screening programs have further boosted reagent consumption. In addition, ongoing product innovation by companies such as Roche Diagnostics and Abbott in high-sensitivity assay kits is reinforcing this segment’s market dominance.

The Devices segment is projected to witness the fastest growth rate of 8.3% from 2026 to 2033, driven by rapid automation in clinical diagnostics and the growing adoption of compact, AI-enabled lipid analyzers. Automated analyzers reduce manual errors, deliver high-throughput testing, and integrate seamlessly with digital data management systems. The growing shift toward point-of-care testing (POCT) devices for faster results in clinics and ambulatory centers is also contributing to segment expansion. Moreover, increasing investments by key manufacturers in connected diagnostic instruments and telehealth-compatible platforms are transforming the lipid testing landscape across North America.

- By Disease

On the basis of disease, the market is segmented into diabetes, stroke, atherosclerosis, obesity, dyslipidaemia, carotid artery disease, peripheral arterial disease, angina, and others. The Atherosclerosis segment dominated the market with the largest share of 27.4% in 2025, as LDL testing is a primary diagnostic tool for evaluating and managing arterial plaque buildup. Physicians rely heavily on LDL concentration monitoring to assess cardiovascular risk and therapeutic efficacy, making it central to disease management protocols. The growing prevalence of coronary artery disease in the U.S. and Canada, along with increased awareness of cholesterol-related disorders, has fueled routine LDL testing demand. In addition, national preventive screening programs and improved access to laboratory services have expanded testing volumes. The availability of advanced lipid analyzers and integration of AI-based interpretation tools are also supporting accurate diagnosis and ongoing disease monitoring.

The Dyslipidaemia segment is anticipated to record the fastest growth rate of 9.2% from 2026 to 2033, driven by the increasing incidence of lipid metabolism disorders due to poor dietary habits and sedentary lifestyles. LDL testing plays a crucial role in identifying dyslipidemic profiles and guiding treatment decisions using statins and PCSK9 inhibitors. Rising public health initiatives aimed at cholesterol control and preventive cardiovascular care are also boosting this segment’s expansion. Furthermore, the growing use of LDL subfraction analysis for personalized treatment planning and improved disease management outcomes is expected to sustain long-term growth. Increasing partnerships between diagnostic laboratories and research organizations for lipidomics research further reinforce segment demand.

- By End User

On the basis of end user, the market is segmented into hospitals, clinics, ambulatory care, and research laboratories. The Hospitals segment accounted for the largest market share of 41.6% in 2025, owing to the high patient volume, availability of advanced testing equipment, and integration of LDL tests into standard cardiovascular care programs. Hospitals serve as primary testing centers for both emergency and preventive screenings, leveraging advanced analyzers for high-throughput processing. The increasing prevalence of cardiac and metabolic disorders has further intensified the need for hospital-based lipid diagnostics. Continuous investments in laboratory automation and quality assurance systems are also driving test accuracy and reliability. In addition, collaborations between hospitals and diagnostic companies to implement digital laboratory information systems (LIS) are enhancing workflow efficiency and supporting this segment’s leadership.

The Clinics segment is projected to grow at the fastest CAGR of 8.7% from 2026 to 2033, fueled by the rapid expansion of outpatient diagnostic services and increasing adoption of point-of-care testing solutions. Clinics provide convenient, cost-effective access to LDL testing, especially for patients seeking routine cholesterol monitoring and preventive care. The ongoing decentralization of diagnostic services and the availability of compact, AI-driven lipid analyzers are making clinics a preferred option for rapid testing. Moreover, the rise in private clinic chains across urban and semi-urban regions in the U.S. and Canada is contributing to increased testing volume. Enhanced patient awareness and healthcare accessibility initiatives are further accelerating this growth trajectory.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tenders and retail. The Direct Tenders segment dominated the market with the largest share of 58.3% in 2025, supported by long-term procurement contracts between hospitals, laboratories, and leading diagnostic suppliers. Bulk purchasing through tender systems ensures cost-effectiveness, standardized quality, and uninterrupted supply of testing kits, reagents, and devices. This channel is particularly prevalent in large healthcare networks, government hospitals, and academic institutions that conduct extensive cardiovascular screenings. In addition, favorable supplier relationships and centralized purchasing mechanisms have streamlined distribution efficiency. The increasing trend of institutional partnerships with global diagnostics firms further strengthens this channel’s growth across North America.

The Retail segment is expected to register the fastest growth rate of 8.1% from 2026 to 2033, driven by the expanding e-commerce presence of diagnostic suppliers and the rising popularity of home-based cholesterol testing kits. Consumers are increasingly opting for retail channels due to convenience, affordability, and accessibility. Pharmacies, online platforms, and diagnostic chains are now offering LDL test kits that enable users to monitor cholesterol levels at home. The growing emphasis on preventive healthcare and the shift toward patient-managed wellness are propelling this trend. Furthermore, collaborations between healthcare brands and retail chains for over-the-counter diagnostic solutions are reshaping consumer engagement in lipid testing.

North America Low Density Lipoprotein (LDL) Test Market Regional Analysis

- The United States dominated the North America LDL test market with the largest revenue share of 68.9% in 2025, supported by advanced diagnostic infrastructure, growing adoption of automated lipid analyzers, and the strong presence of leading biotechnology and healthcare firms

- Consumers and healthcare providers in the U.S. emphasize routine lipid profiling and cholesterol monitoring as part of preventive healthcare, supported by well-established laboratory networks and the availability of high-precision automated analyzers

- This dominance is further strengthened by favorable reimbursement frameworks, strong presence of leading diagnostic companies such as Abbott and Quest Diagnostics, and continuous innovation in lipid testing methods, positioning the U.S. as the core growth engine of the North American LDL test market

U.S. Low Density Lipoprotein (LDL) Test Market Insight

The U.S. Low Density Lipoprotein (LDL) Test Market captured the largest revenue share of 68.9% in 2025 within North America, driven by the high prevalence of cardiovascular and lifestyle-related diseases such as obesity, diabetes, and atherosclerosis. The increasing focus on preventive healthcare, coupled with government-backed awareness initiatives about cholesterol management, is fueling demand for LDL testing across hospitals and clinics. Widespread access to advanced diagnostic infrastructure and point-of-care testing solutions further strengthens market penetration. In addition, the presence of leading diagnostic companies such as Abbott, Quest Diagnostics, and Thermo Fisher Scientific enhances innovation and availability, ensuring faster and more accurate lipid profiling nationwide.

Canada Low Density Lipoprotein (LDL) Test Market Insight

The Canada LDL Test Market is projected to witness steady growth through the forecast period, driven by rising healthcare expenditure and growing awareness regarding cardiovascular risk assessment. The country’s strong emphasis on early disease detection and its publicly funded healthcare system are encouraging routine lipid panel screenings. Canadian healthcare providers are increasingly adopting automated analyzers and reagent kits to improve testing accuracy and efficiency. Furthermore, the growing aging population and increased focus on chronic disease management programs contribute to market expansion. Strategic collaborations between diagnostic centers and research institutions are also enhancing innovation and accessibility across provinces.

Mexico Low Density Lipoprotein (LDL) Test Market Insight

The Mexico LDL Test Market is anticipated to expand at the fastest CAGR in North America during the forecast period, driven by the increasing prevalence of obesity and dyslipidemia across the adult population. Government-led health initiatives promoting cholesterol awareness and routine lipid screening are improving diagnostic reach in both urban and semi-urban regions. The rise in private healthcare facilities and diagnostic laboratories has further increased accessibility to affordable LDL testing services. In addition, growing collaborations with U.S.-based diagnostic firms are helping introduce advanced testing technologies and high-quality reagent kits in the Mexican market, supporting modernization of lipid testing infrastructure.

North America Low Density Lipoprotein (LDL) Test Market Share

The North America Low Density Lipoprotein (LDL) Test industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Siemens Healthineers AG (Germany)

- Beckman Coulter, Inc. (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Ortho Clinical Diagnostics (U.S.)

- DiaSorin S.p.A. (Italy)

- numares AG. (Germany)

- Randox Laboratories Ltd (U.K.)

- SEKISUI Diagnostics (Japan)

- Bio-Rad Laboratories, Inc. (U.S.)

- Quest Diagnostics Incorporated (U.S.)

- Labcorp (U.S.)

- Werfen (Spain)

- Nova Biomedical (U.S.)

- PTS Diagnostics LLC (U.S.)

- ACON Laboratories, Inc. (U.S.)

- Abcam plc (U.K.)

- Eurofins Scientific (Luxembourg)

- ARKRAY, Inc. (Japan)

What are the Recent Developments in North America Low Density Lipoprotein (LDL) Test Market?

- In August 2025, Novartis AG announced that its LDL-lowering siRNA therapy (inclisiran; brand: Leqvio®) received a U.S. label update from the FDA to allow monotherapy use (i.e., without concurrent statin) for LDL-C reduction in adults with hypercholesterolemia. This regulatory change heightens the clinical importance of precise LDL-C testing and monitoring in routine practice

- In July 2025, Merck & Co., Inc. reported that its investigational oral PCSK9 inhibitor, enlicitide decanoate, in the Phase 3 CORALreef Lipids Trial reduced LDL-C by 55.8% at week 24 versus placebo. Although a therapeutic rather than pure diagnostic development, such results drive demand for precise LDL-C monitoring and advanced testing tools

- In April 2025, at the American College of Cardiology (ACC) 2025 meeting, a presentation highlighted multiple novel lipid lowering and diagnostic advances including advanced LDL-C and Lp(a) therapies and the unmet testing gaps underscoring the growing emphasis on advanced lipid diagnostics in the U.S.

- In May 2024, Roche Diagnostics was granted Breakthrough Device Designation by the FDA for its Tina-quant® Lp(a) assay a blood test measuring lipoprotein(a) in molar units (nmol/L) instead of mass units, thereby improving cardiovascular risk stratification

- In July 2023, Numares Health (USA/Germany) announced that its AXINON® LDL-p Test System received 510(k) clearance from the U.S. Food & Drug Administration (FDA). This test uses NMR spectroscopy to measure LDL particle number (“LDL-p”) rather than just LDL-C, offering a more refined lipoprotein risk assessment tool for cardiovascular disease

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.