North America Meal Replacement Products Market

Market Size in USD Billion

USD

8.52 Billion

USD

14.38 Billion

2025

2033

USD

8.52 Billion

USD

14.38 Billion

2025

2033

| 2026 - 2033 | |

| USD 8.52 Billion | |

| USD 14.38 Billion | |

| % | |

|

North America Meal Replacement Products Market Size

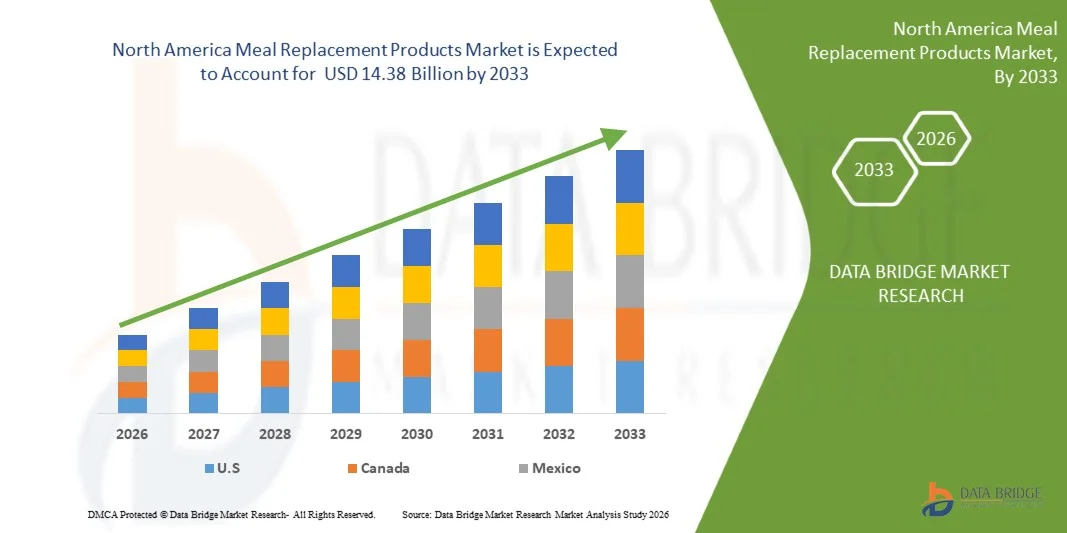

- The North America meal replacement products market is expected to reach USD 14.38 billion by 2033 from USD 8.52 billion in 2025, growing with a CAGR of 6.9% in the forecast period of 2026 to 2033.

- The increasing consumer awareness about health, nutrition, and weight management is a major growth driver, with more individuals seeking balanced, portion-controlled, and functional food alternatives to support active and healthy lifestyles.

- The rising demand for convenient, on-the-go food solutions, especially among urban populations with busy schedules, is significantly boosting the popularity of meal replacement shakes, bars, and ready-to-mix powders.

North America Meal Replacement Products Market Analysis

- The North America meal replacement products market has evolved significantly over the past decades, driven by shifting dietary habits, rising health consciousness, and increasing demand for convenient, nutritionally balanced food alternatives among busy consumers worldwide.

- The market is further supported by continuous product innovation, expanding e-commerce channels, and growing disposable incomes in emerging economies.

- In 2025, U.S. is expected to dominate the North America meal replacement products market, capturing 82.01% market share due to its strong fitness culture, high consumer awareness, and widespread availability of advanced nutritional products.

- Canada is the fastest growing country with a CAGR of 7.3%, the growth of the market is supported by increasing adoption of weight management solutions and a rising preference for functional and fortified foods across diverse consumer groups.

- Powdered meal replacements are expected to dominate the market, holding the largest share of 27.19%, due to their affordability, longer shelf life, and ease of customization with various nutritional ingredients.

Report Scope and North America Meal Replacement Products Market Segmentation

|

Attributes |

North America Meal Replacement Products Market Insights |

|

Segments Covered |

· By Type- Powdered Meal Replacements, Ready-To-Drink (RTD) Shakes, Bars, Liquid Concentrates, Meal Replacement Soups, Specialty Formulations, Others · By Ingredient Type- Protein, Carbohydrates, Fats, Vitamins and Minerals, Fiber, and Others · By Function- Weight Management, Sports Nutrition, Wellness & Lifestyle, Clinical Nutrition, and Others · By Distribution Channel- Supermarkets / Hypermarkets, Online Retail, Pharmacy / Drug Stores, Specialty Stores, Convenience Stores, and Others · By End User- Adults, Geriatric Population, Athletes, Pediatrics, and Others |

|

Countries Covered |

North America · U.S. · Canada · Mexico |

|

Key Market Players |

· Nestlé S.A. (Switzerland) · Glanbia PLC (Ireland) · Amway Corporation (U.S.) · Unilever PLC (U.K.) · The Simply Good Foods Company (Quest, Atkins) (U.S.) · Growequal Limited (U.K.) · General Mills, Inc. (U.S.) · Huel Ltd. (U.K.) · Soylent Nutrition, Inc. (U.S.) · Bob's Red Mill Natural Foods (U.S.) · Labrada Nutrition (U.S.) · YFood (Germany) · Saturo Foods GmbH (Austria) · Jimmy Joy (Netherlands) · Bertrand Bio SAS (France) · So Shape (France) · Saipro Biotech Pvt. Ltd. (India) · PhenQ (Slimming Shake) (U.K.) |

|

Market Opportunities |

· Rise of Veganism · Increasing Internet Penetration in Emerging Economies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

North America Meal Replacement Products Market Trends

“Growing Popularity of Personalized Nutrition”

- The growing popularity of personalized nutrition is transforming the North America meal replacement products market, as consumers increasingly seek tailored solutions that align with their individual health goals, dietary preferences, and lifestyles. Advances in digital health technologies, wearable devices, and data analytics enable companies to offer customized meal plans based on factors such as age, metabolism, activity levels, and specific nutritional deficiencies.

- This trend is particularly strong among fitness enthusiasts, athletes, and health-conscious individuals who demand precise nutrient intake for optimized performance and wellness. As a result, brands are developing flexible product lines that allow consumers to personalize protein content, calorie levels, and ingredient composition, enhancing user engagement and satisfaction while strengthening brand loyalty in a competitive market landscape.

- Furthermore, the integration of artificial intelligence and mobile applications is accelerating the adoption of personalized meal replacement solutions by providing real-time dietary recommendations and progress tracking.

- Subscription-based models are gaining traction, offering convenience and continuity for users seeking long-term health management. Companies are also leveraging genetic testing and microbiome analysis to deliver highly targeted nutritional products, further advancing personalization.

- This shift toward individualized nutrition not only improves consumer outcomes but also opens new revenue streams for manufacturers, positioning personalized meal replacements as a key growth driver in the evolving North America nutrition and wellness industry.

North America Meal Replacement Products Market Dynamics

Driver

“Rising Health & Wellness Awareness”

- The growing North America emphasis on health and wellness has become a major driver of the meal replacement products market. Consumers are increasingly recognizing the direct relationship between dietary habits and long term health outcomes, particularly in preventing chronic diseases such as obesity, diabetes, and cardiovascular conditions.

- This shift has encouraged the adoption of nutritionally balanced, portion-controlled, and functional food options, positioning meal replacement products as a practical solution for modern dietary needs. In addition, the increasing focus on preventive healthcare and self-management of health has significantly influenced consumer behavior. North America institutions such as the World Health Organization emphasize the importance of balanced nutrition and healthy eating patterns. As a result, consumers are actively seeking convenient products that provide controlled calorie intake and essential nutrients, thereby driving demand for meal replacement solutions.

- For instance, in December 2025, the World Health Organization published a fact sheet reporting that in 2022 about 2.5 billion adults worldwide were overweight, including 890 million living with obesity, highlighting a significant North America rise in excess weight and related health risks. This widespread prevalence has intensified awareness about diet‑related health issues and encouraged consumers to seek structured, calorie‑controlled nutritional solutions such as meal replacement products to support better health outcomes.

- In conclusion, rising health and wellness awareness is a fundamental driver of the North America meal replacement products market. The increasing prevalence of lifestyle-related diseases, combined with strong advocacy from North America health organizations, is encouraging consumers to adopt healthier and more structured dietary practices. As awareness continues to grow, the demand for convenient, nutritionally balanced food solutions such as meal replacements is expected to expand steadily, supporting long-term market growth.

Restraint/Challenge

“High Prices of Premium Meal Replacement Products”

- Premium meal replacement products often command higher price points compared with traditional meal options. These products typically contain high‑quality proteins, added vitamins/minerals, organic or plant‑based ingredients, and specialized formulations tailored to fitness or clinical nutrition needs. While this can deliver nutritional benefits, higher retail prices can discourage broader consumer adoption; especially among price‑sensitive population segments and emerging markets.

- The higher cost of premium options also reinforces the perception that meal replacements are a “niche or luxury” choice rather than an everyday dietary staple. This cost barrier limits the potential customer base, restrains repeat purchases among mainstream consumers, and reduces total market growth.

- For instance, in February 2026, Nuffoods Spectrum highlighted the “price sensitivity trap” in India, where consumers want premium, science‑backed nutrition but expect mass‑market pricing, forcing brands to compromise on formulation or pricing to attract buyers. This commentary illustrates that even when premium nutrition exists, consumers are reluctant to pay higher prices, constraining growth for higher‑priced meal replacement products.

- High prices of premium meal replacement products are a clear restraint on the North America market. While advanced formulations and quality ingredients can offer health and convenience benefits, elevated costs make such products less accessible to many consumers.

- This limits broader adoption, particularly among price‑sensitive segments and in emerging economies, and constrains overall market growth unless manufacturers balance price with value or introduce more affordable alternatives.

North America Meal Replacement Products Market Scope

The North America meal replacement products market is categorized into five segments based on type, ingredient type, function, distribution channel, and end user.

- By Type

On the basis of type, the market is segmented into powdered meal replacements, ready-to-drink (RTD) shakes, bars, liquid concentrates, meal replacement soups, specialty formulations, and others.

In 2026, the powdered meal replacements segment is expected to dominate with 27.19% market share, driven by affordability, longer shelf life, and ease of customization with nutrients and flavors. These products are widely used across fitness and daily nutrition routines, making them highly preferred among cost-conscious and health-focused consumers in North America.

However, the ready-to-drink (RTD) shakes segment is projected to register the highest CAGR of 7.5% during the forecast period of 2026 to 2033, driven by rising demand for convenient, portable nutrition solutions, busy lifestyles, increasing urbanization, and growing preference for on-the-go consumption among working professionals and younger populations worldwide.

- By Ingredient Type

On the basis of ingredient type, the market is segmented into protein, carbohydrates, fats, vitamins and minerals, fiber, and others.

In 2026, the protein segment is expected to dominate with 32.28% market share, driven by increasing demand for muscle growth, satiety, and weight management benefits. Protein-based formulations are highly preferred among fitness enthusiasts and health-conscious individuals, contributing to strong adoption across various consumer groups and supporting overall market expansion in North America.

Moreover, the protein segment is projected to register the highest CAGR of 7.7% during the forecast period of 2026 to 2033, driven by rising adoption of high-protein diets, increasing awareness of nutritional benefits, expanding vegan protein options, and growing demand among fitness enthusiasts and health-conscious consumers seeking balanced nutrition in North America.

- By Function

On the basis of function, the market is segmented into weight management, sports nutrition, wellness & lifestyle, clinical nutrition, and others.

In 2026, the weight management segment is expected to dominate with 38.45% market share, driven by rising obesity rates, increasing health awareness, and growing focus on calorie control and structured diet plans. Consumers widely use meal replacements for portion control, supporting consistent demand and long-term market growth in North America.

However, the sports nutrition segment is projected to register the highest CAGR of 7.7% during the forecast period of 2026 to 2033, driven by increasing gym participation, rising interest in athletic performance, growing demand for energy-boosting nutrition, and expanding fitness culture among younger populations and professional athletes worldwide.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into supermarkets / hypermarkets, online retail, pharmacy / drug stores, specialty stores, convenience stores, and others.

In 2026, the supermarkets / hypermarkets segment is expected to dominate with 41.98% market share, driven by strong retail networks, wide product availability, and consumer preference for physical inspection before purchase. These outlets offer multiple brands, enhancing consumer choice and contributing significantly to overall sales across regions

However, the online retail segment is projected to register the highest CAGR of 7.7% during the forecast period of 2026 to 2033, driven by increasing internet penetration, rising smartphone usage, convenience of home delivery, availability of discounts, and access to a wide range of brands attracting digitally active consumers

- By End User

On the basis of end user, the market is segmented into adults, geriatric population, athletes, pediatrics, and others.

In 2026, the adults segment is expected to dominate with 46.48% market share, driven by busy lifestyles, increasing health awareness, and growing reliance on convenient nutrition solutions. Adults represent the primary consumer base, supporting consistent demand for meal replacement products across North America markets.

However, the athletes segment is projected to register the highest CAGR of 7.4% during the forecast period of 2026 to 2033, driven by rising participation in sports, increasing focus on performance enhancement, growing use of nutritional supplements, and expanding awareness of fitness and strength training among professional and amateur athletes worldwide.

North America Meal Replacement Products Market Regional Analysis

- North America remains one of the largest regional markets for meal replacement products market, with an estimated 44.61% share of North America demand. With a projected CAGR of 6.9%, the region is expected to grow steadily, supported by high health awareness, strong demand for convenient nutrition, and widespread adoption of fitness-oriented lifestyles among consumers across the U.S. and Canada markets.

- The region benefits from well-established retail infrastructure, strong presence of leading market players, advanced product innovation, and high disposable incomes. Additionally, increasing preference for protein-rich diets, clean-label products, and functional nutrition continues to support sustained demand and product diversification in the region.

- North America is projected to register the highest CAGR of 6.9% during 2026–2033, mainly driven by rapid urbanization, rising middle-class population, increasing disposable incomes, and growing awareness of health, wellness, and convenient dietary solutions among consumers in emerging economies.

U.S. Meal Replacement Products Market Insight

U.S. is expected to dominate the meal replacement products the North America market, North America meal replacement products market due to high health awareness, a strong fitness culture, and widespread adoption of convenient nutrition solutions. Increasing demand for protein-rich, plant-based, and functional products, along with robust retail and e-commerce channels, supports steady growth. Leading brands continue to innovate with new flavors, fortified formulations, and personalized options, catering to diverse consumer needs across the country.

Canada Meal Replacement Products Market Insight

The Canada meal replacement products market is positioned for strong growth, fueled by rapid urbanization, rising disposable incomes, and increasing health consciousness among consumers. Growing demand for convenient, on-the-go nutritional solutions and functional ingredients is driving adoption. Expansion of e-commerce platforms, fitness trends, and awareness of weight management and wellness products further support market growth, attracting both domestic and international brands to invest in the region.

North America Meal Replacement Products Market Share

The North America meal replacement products market industry is primarily led by well-established companies, including:

- Nestlé S.A. (Switzerland)

- Glanbia PLC (Ireland)

- Amway Corporation (U.S.)

- Unilever PLC (U.K.)

- The Simply Good Foods Company (Quest, Atkins) (U.S.)

- Growequal Limited (U.K.)

- General Mills, Inc. (U.S.)

- Huel Ltd. (U.K.)

- Soylent Nutrition, Inc. (U.S.)

- Bob's Red Mill Natural Foods (U.S.)

- Labrada Nutrition (U.S.)

- YFood (Germany)

- Saturo Foods GmbH (Austria)

- Jimmy Joy (Netherlands)

- Bertrand Bio SAS (France)

- So Shape (France)

- Saipro Biotech Pvt. Ltd. (India)

- PhenQ (Slimming Shake) (U.K.)

Latest Developments in North America Meal Replacement Products Market

- In December 2025, Abbott Laboratories launched two new Ensure Max Protein shakes 42g Protein and 2-in-1 Muscle Support targeting muscle health in active and aging adults. The products combine high-quality protein, essential nutrients, and HMB to support muscle building and preservation. The launch reflects growing consumer focus on strength, longevity, and overall wellness, with initial exclusive availability through Walmart.

- In September 2025, Nutrilite by Amway received a ‘Trusted Certification’ recognition from the National Forensic Sciences University (NFSU) under its Nutritional Supplementation Testing for Sportspersons (NSTS) programme. This certification confirms that several key Nutrilite supplements have been independently tested and found free from unsafe or banned substances, meeting international standards used in sports nutrition.

- In April 2025, Herbalife announced the planned acquisition of assets from Pro2col Health LLC and Pruvit Ventures, Inc. to strengthen its personalized nutrition and digital wellness capabilities. The move aims to integrate advanced health tracking, consumer data insights, and customized nutrition solutions into Herbalife’s existing product ecosystem. By combining personalized health technology with its established nutrition portfolio, the company seeks to enhance product innovation and improve customer engagement in weight-management and meal replacement programs. This development is expected to positively impact the market by accelerating the shift toward personalized nutrition, increasing competition among manufacturers, and encouraging innovation in data-driven meal replacement and functional nutrition solutions globally.

- In December 2024, Nestlé has launched a new Boost pre-meal beverage designed to support hunger suppression and stimulate natural GLP-1 production, aligning with the growing demand for weight management solutions. Containing 10g of protein and only 45 calories, the mocha-flavoured drink is targeted at consumers using GLP-1 medications, reinforcing Nestlé’s focus on innovation in functional nutrition and obesity-related health trends.

- In April 2024, Glanbia plc announced the acquisition of Flavor Producers LLC for USD 300 million to strengthen its Nutritional Solutions segment. The deal enhances Glanbia’s capabilities in natural and organic flavors, expands its R&D and formulation expertise, and aligns with growing clean-label trends. The acquisition supports long-term growth and portfolio diversification strategy.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 MULTIVARIATE MODELING

2.7 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.8 DBMR MARKET POSITION GRID

2.9 DBMR VENDOR SHARE ANALYSIS

2.1 MARKET END USER COVERAGE GRID

2.11 SECONDARY SOURCES

2.12 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PORTERS FIVE FORCES ANALYSIS

4.2 TECHNOLOGICAL ADVANCEMENTS

4.3 VENDOR SELECTION CRITERIA

4.3.1 VENDOR EVALUATION CRITERIA

4.3.2 WEIGHTAGE ALLOCATION:

4.4 RAW MATERIAL COVERAGE

4.4.1 CARBOHYDRATE BASE (OATS, QUINOA, BANANAS, MUESLI, GRAIN POWDERS)

4.4.2 PROTEIN BUILDUP (GREEK YOGURT, TOFU, WHEY PROTEIN, PLANT-BASED PROTEINS)

4.4.3 VEGETABLE OR FRUIT FLAVOR (BERRIES, BANANAS, SPINACH, CARROT, BEETROOT)

4.4.4 FAT GARNISH (NUTS, SEEDS, NUT BUTTERS, COCONUT)

4.4.5 ADDITIONAL FUNCTIONAL AND FLAVOR INGREDIENTS (COCOA, DARK CHOCOLATE, COFFEE, CINNAMON, VANILLA EXTRACT, XANTHAN GUM)

4.5 BRAND OUTLOOK

4.6 INDUSTRY ECOSYSTEM ANALYSIS

4.6.1 PROMINENT COMPANIES

4.6.2 SMALL & MEDIUM SIZE COMPANIES

4.6.3 END USERS

4.7 PRICING ANALYSIS

4.8 CONSUMER BUYING BEHAVIOUR

4.9 SUPPLY CHAIN ANALYSIS

4.9.1 OVERVIEW

4.9.2 LOGISTIC COST SCENARIO

4.9.3 IMPORTANCE OF LOGISTICS SERVICE PROVIDERS

4.1 CLIMATE CHANGE SCENARIO

4.10.1 ENVIRONMENTAL CONCERNS

4.10.2 INDUSTRY RESPONSE

4.10.3 GOVERNMENT’S ROLE

4.10.4 ANALYST RECOMMENDATIONS

4.11 VALUE CHAIN ANALYSIS

4.11.1 RAW MATERIAL SOURCING

4.11.2 MANUFACTURING AND ASSEMBLY

4.11.3 PRODUCT DESIGN AND ENGINEERING

4.11.4 QUALITY ASSURANCE AND CERTIFICATION

4.11.5 DISTRIBUTION AND LOGISTICS

4.11.6 CONCLUSION

5 TARIFFS & IMPACT ON THE MARKET

5.1 OVERVIEW

5.2 CURRENT TARIFF RATE(S) IN TOP-5 COUNTRIES MARKETS

5.3 OUTLOOK: LOCAL PRODUCTION VS IMPORT RELIANCE

5.3.1 UNITED STATES

5.3.2 CHINA

5.3.3 INDIA

5.4 VENDOR SELECTION CRITERIA DYNAMICS

5.5 IMPACT ON SUPPLY CHAIN

5.5.1 RAW MATERIAL PROCUREMENT

5.5.2 MANUFACTURING AND PRODUCTION

5.5.3 LOGISTICS AND DISTRIBUTION

5.5.4 PRICE PITCHING AND POSITION OF MARKET

5.6 INDUSTRY PARTICIPANTS: PROACTIVE MOVES

5.6.1 SUPPLY CHAIN OPTIMIZATION

5.6.2 JOINT VENTURE ESTABLISHMENTS

5.7 IMPACT ON PRICES

5.8 REGULATORY INCLINATION

5.8.1 GEOPOLITICAL SITUATION

5.8.2 TRADE PARTNERSHIPS BETWEEN COUNTRIES

5.8.2.1 FREE TRADE AGREEMENTS

5.8.2.2 ALLIANCES ESTABLISHMENTS

5.8.3 STATUS ACCREDITATION (INCLUDING MFN)

5.8.4 DOMESTIC COURSE OF CORRECTION

5.8.4.1 INCENTIVE SCHEMES TO BOOST PRODUCTION OUTPUTS

5.8.4.2 ESTABLISHMENT OF SEZS / INDUSTRIAL PARKS

6 REGULATION COVERAGE

6.1 PRODUCT CODES

6.2 CERTIFIED STANDARDS

6.2.1 CODEX ALIMENTARIUS STANDARDS

6.2.2 EUROPEAN UNION REGULATIONS (EU COMPOSITIONAL & HEALTH CLAIMS RULES)

6.2.3 CANADA – FOOD AND DRUG REGULATIONS (COMPOSITIONAL STANDARDS)

6.2.4 AUSTRALIA & NEW ZEALAND FOOD STANDARDS CODE – STANDARD 2.9.3

6.2.5 ISO & FOOD SAFETY MANAGEMENT SYSTEM STANDARDS

6.3 SAFETY STANDARDS

6.3.1 MATERIAL HANDLING & STORAGE

6.3.2 TRANSPORT & PRECAUTIONS

6.3.3 HAZARD IDENTIFICATION

7 MARKET OVERVIEW

7.1 DRIVERS

7.1.1 RISING HEALTH & WELLNESS AWARENESS

7.1.2 RISING URBANIZATION AND CHANGING DIETARY PATTERNS

7.1.3 GROWTH IN FITNESS & WEIGHT MANAGEMENT TRENDS

7.1.4 EXPANSION OF E-COMMERCE AND SUBSCRIPTION MODELS

7.2 RESTRAINTS

7.2.1 HIGH PRICES OF PREMIUM MEAL REPLACEMENT PRODUCTS

7.2.2 NEGATIVE PERCEPTION OF ARTIFICIAL INGREDIENTS

7.3 OPPORTUNITIES

7.3.1 EXPANSION IN EMERGING MARKETS

7.3.2 EXPANSION OF PLANT-BASED & CLEAN-LABEL PRODUCTS

7.3.3 INTEGRATION WITH DIGITAL HEALTH AND WELLNESS ECOSYSTEMS

7.4 CHALLENGES

7.4.1 SUPPLY CHAIN VOLATILITY

7.4.2 INTENSE COMPETITION FROM TRADITIONAL AND ALTERNATIVE FOODS

8 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE

8.1 OVERVIEW

8.2 POWDERED MEAL REPLACEMENTS

8.3 READY-TO-DRINK (RTD) SHAKES

8.4 BARS

8.5 LIQUID CONCENTRATES

8.6 MEAL REPLACEMENT SOUPS

8.7 SPECIALTY FORMULATIONS

8.8 OTHERS

8.9 NORTH AMERICA POWDERED MEAL REPLACEMENTS IN MEAL REPLACEMENT PRODUCTS MARKET, BY FORMULATION, 2018-2033 (USD THOUSAND)

8.9.1 DAIRY-BASED

8.9.2 PLANT-BASED

8.1 NORTH AMERICA POWDERED MEAL REPLACEMENTS IN MEAL REPLACEMENT PRODUCTS MARKET, BY FLAVOR, 2018-2033 (USD THOUSAND)

8.10.1 CHOCOLATE

8.10.2 VANILLA

8.10.3 FRUITS

8.10.4 STRAWBERRY

8.10.5 OTHERS

8.11 NORTH AMERICA POWDERED MEAL REPLACEMENTS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.11.1 NORTH AMERICA

8.11.2 EUROPE

8.11.3 ASIA-PACIFIC

8.11.4 SOUTH AMERICA

8.11.5 MIDDLE EAST & AFRICA

8.12 NORTH AMERICA READY-TO-DRINK (RTD) SHAKES IN MEAL REPLACEMENT PRODUCTS MARKET, BY FLAVOR, 2018-2033 (USD THOUSAND)

8.12.1 CHOCOLATE

8.12.2 VANILLA

8.12.3 BERRY

8.12.4 STRAWBERRY

8.12.5 CRANEBERRY

8.12.6 RASPBERRY

8.12.7 OTHERS

8.13 NORTH AMERICA READY-TO-DRINK (RTD) SHAKES IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.13.1 NORTH AMERICA

8.13.2 EUROPE

8.13.3 ASIA-PACIFIC

8.13.4 SOUTH AMERICA

8.13.5 MIDDLE EAST & AFRICA

8.14 NORTH AMERICA BARS IN MEAL REPLACEMENT PRODUCTS MARKET, BY FLAVOR, 2018-2033 (USD THOUSAND)

8.14.1 CHOCOLATE

8.14.2 PEANUT BUTTER

8.14.3 FRUIT

8.14.4 OTHERS

8.15 NORTH AMERICA BARS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.15.1 NORTH AMERICA

8.15.2 EUROPE

8.15.3 ASIA-PACIFIC

8.15.4 SOUTH AMERICA

8.15.5 MIDDLE EAST & AFRICA

8.16 NORTH AMERICA LIQUID CONCENTRATES IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.16.1 NORTH AMERICA

8.16.2 EUROPE

8.16.3 ASIA-PACIFIC

8.16.4 SOUTH AMERICA

8.16.5 MIDDLE EAST & AFRICA

8.17 NORTH AMERICA MEAL REPLACEMENT SOUPS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.17.1 NORTH AMERICA

8.17.2 EUROPE

8.17.3 ASIA-PACIFIC

8.17.4 SOUTH AMERICA

8.17.5 MIDDLE EAST & AFRICA

8.18 NORTH AMERICA SPECIALTY FORMULATIONS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.18.1 NORTH AMERICA

8.18.2 EUROPE

8.18.3 ASIA-PACIFIC

8.18.4 SOUTH AMERICA

8.18.5 MIDDLE EAST & AFRICA

8.19 NORTH AMERICA OTHERS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.19.1 NORTH AMERICA

8.19.2 EUROPE

8.19.3 ASIA-PACIFIC

8.19.4 SOUTH AMERICA

8.19.5 MIDDLE EAST & AFRICA

9 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY INGREDIENT TYPE

9.1 OVERVIEW

9.2 PROTEIN

9.3 CARBOHYDRATES

9.4 FATS

9.5 VITAMINS AND MINERALS

9.6 FIBER

9.7 OTHERS

9.8 NORTH AMERICA PROTEIN IN MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.8.1 WHEY

9.8.2 SOY

9.8.3 CASEIN

9.8.4 PEA

9.8.5 OTHERS

9.9 NORTH AMERICA WHEY IN MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.9.1 CONCENTRATE

9.9.2 ISOLATE

9.1 NORTH AMERICA PROTEIN IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.10.1 NORTH AMERICA

9.10.2 EUROPE

9.10.3 ASIA-PACIFIC

9.10.4 SOUTH AMERICA

9.10.5 MIDDLE EAST & AFRICA

9.11 NORTH AMERICA CARBOHYDRATES IN MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.11.1 MALTODEXTRIN

9.11.2 OATS

9.11.3 SWEET POTATO

9.11.4 OTHERS

9.12 NORTH AMERICA CARBOHYDRATES IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.12.1 NORTH AMERICA

9.12.2 EUROPE

9.12.3 ASIA-PACIFIC

9.12.4 SOUTH AMERICA

9.12.5 MIDDLE EAST & AFRICA

9.13 NORTH AMERICA FATS IN MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.13.1 MCT OIL

9.13.2 SUNFLOWER OIL

9.13.3 OTHERS

9.14 NORTH AMERICA FATS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.14.1 NORTH AMERICA

9.14.2 EUROPE

9.14.3 ASIA-PACIFIC

9.14.4 SOUTH AMERICA

9.14.5 MIDDLE EAST & AFRICA

9.15 NORTH AMERICA VITAMINS AND MINERALS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.15.1 NORTH AMERICA

9.15.2 EUROPE

9.15.3 ASIA-PACIFIC

9.15.4 SOUTH AMERICA

9.15.5 MIDDLE EAST & AFRICA

9.16 NORTH AMERICA FIBER IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.16.1 NORTH AMERICA

9.16.2 EUROPE

9.16.3 ASIA-PACIFIC

9.16.4 SOUTH AMERICA

9.16.5 MIDDLE EAST & AFRICA

9.17 NORTH AMERICA OTHERS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.17.1 NORTH AMERICA

9.17.2 EUROPE

9.17.3 ASIA-PACIFIC

9.17.4 SOUTH AMERICA

9.17.5 MIDDLE EAST & AFRICA

10 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY FUNCTION

10.1 OVERVIEW

10.2 WEIGHT MANAGEMENT

10.3 SPORTS NUTRITION

10.4 WELLNESS & LIFESTYLE

10.5 CLINICAL NUTRITION

10.6 OTHERS

10.7 NORTH AMERICA WEIGHT MANAGEMENT IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.7.1 NORTH AMERICA

10.7.2 EUROPE

10.7.3 ASIA-PACIFIC

10.7.4 SOUTH AMERICA

10.7.5 MIDDLE EAST & AFRICA

10.8 NORTH AMERICA SPORTS NUTRITION IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.8.1 NORTH AMERICA

10.8.2 EUROPE

10.8.3 ASIA-PACIFIC

10.8.4 SOUTH AMERICA

10.8.5 MIDDLE EAST & AFRICA

10.9 NORTH AMERICA WELLNESS & LIFESTYLE IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.9.1 NORTH AMERICA

10.9.2 EUROPE

10.9.3 ASIA-PACIFIC

10.9.4 SOUTH AMERICA

10.9.5 MIDDLE EAST & AFRICA

10.1 NORTH AMERICA CLINICAL NUTRITION IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.10.1 NORTH AMERICA

10.10.2 EUROPE

10.10.3 ASIA-PACIFIC

10.10.4 SOUTH AMERICA

10.10.5 MIDDLE EAST & AFRICA

10.11 NORTH AMERICA OTHERS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.11.1 NORTH AMERICA

10.11.2 EUROPE

10.11.3 ASIA-PACIFIC

10.11.4 SOUTH AMERICA

10.11.5 MIDDLE EAST & AFRICA

11 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY DISTRIBUTION CHANNEL

11.1 OVERVIEW

11.2 SUPERMARKETS / HYPERMARKETS

11.3 ONLINE RETAIL

11.4 PHARMACY / DRUG STORES

11.5 SPECIALTY STORES

11.6 CONVENIENCE STORES

11.7 OTHERS

11.8 NORTH AMERICA SUPERMARKETS / HYPERMARKETS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.8.1 NORTH AMERICA

11.8.2 EUROPE

11.8.3 ASIA-PACIFIC

11.8.4 SOUTH AMERICA

11.8.5 MIDDLE EAST & AFRICA

11.9 NORTH AMERICA ONLINE RETAIL IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.9.1 NORTH AMERICA

11.9.2 EUROPE

11.9.3 ASIA-PACIFIC

11.9.4 SOUTH AMERICA

11.9.5 MIDDLE EAST & AFRICA

11.1 NORTH AMERICA PHARMACY / DRUG STORES IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.10.1 NORTH AMERICA

11.10.2 EUROPE

11.10.3 ASIA-PACIFIC

11.10.4 SOUTH AMERICA

11.10.5 MIDDLE EAST & AFRICA

11.11 NORTH AMERICA SPECIALTY STORES IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.11.1 NORTH AMERICA

11.11.2 EUROPE

11.11.3 ASIA-PACIFIC

11.11.4 SOUTH AMERICA

11.11.5 MIDDLE EAST & AFRICA

11.12 NORTH AMERICA CONVENIENCE STORES IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.12.1 NORTH AMERICA

11.12.2 EUROPE

11.12.3 ASIA-PACIFIC

11.12.4 SOUTH AMERICA

11.12.5 MIDDLE EAST & AFRICA

11.13 NORTH AMERICA OTHERS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.13.1 NORTH AMERICA

11.13.2 EUROPE

11.13.3 ASIA-PACIFIC

11.13.4 SOUTH AMERICA

11.13.5 MIDDLE EAST & AFRICA

12 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY END USER

12.1 OVERVIEW

12.2 ADULTS

12.3 GERIATRIC POPULATION

12.4 ATHLETES

12.5 PEDIATRICS

12.6 OTHERS

12.7 NORTH AMERICA ADULTS IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

12.7.1 POWDERED MEAL REPLACEMENTS

12.7.2 READY-TO-DRINK (RTD) SHAKES

12.7.3 BARS

12.7.4 LIQUID CONCENTRATES

12.7.5 MEAL REPLACEMENT SOUPS

12.7.6 SPECIALTY FORMULATIONS

12.7.7 OTHERS

12.8 NORTH AMERICA ADULTS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.8.1 NORTH AMERICA

12.8.2 EUROPE

12.8.3 ASIA-PACIFIC

12.8.4 SOUTH AMERICA

12.8.5 MIDDLE EAST & AFRICA

12.9 NORTH AMERICA GERIATRIC POPULATION IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

12.9.1 READY-TO-DRINK (RTD) SHAKES

12.9.2 POWDERED MEAL REPLACEMENTS

12.9.3 LIQUID CONCENTRATES

12.9.4 MEAL REPLACEMENT SOUPS

12.9.5 BARS

12.9.6 SPECIALTY FORMULATIONS

12.9.7 OTHERS

12.1 NORTH AMERICA GERIATRIC POPULATION IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.10.1 NORTH AMERICA

12.10.2 EUROPE

12.10.3 ASIA-PACIFIC

12.10.4 SOUTH AMERICA

12.10.5 MIDDLE EAST & AFRICA

12.11 NORTH AMERICA ATHLETES IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

12.11.1 POWDERED MEAL REPLACEMENTS

12.11.2 READY-TO-DRINK (RTD) SHAKES

12.11.3 BARS

12.11.4 SPECIALTY FORMULATIONS

12.11.5 LIQUID CONCENTRATES

12.11.6 MEAL REPLACEMENT SOUPS

12.11.7 OTHERS

12.12 NORTH AMERICA ATHLETES IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.12.1 NORTH AMERICA

12.12.2 EUROPE

12.12.3 ASIA-PACIFIC

12.12.4 SOUTH AMERICA

12.12.5 MIDDLE EAST & AFRICA

12.13 NORTH AMERICA PEDIATRICS IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

12.13.1 POWDERED MEAL REPLACEMENTS

12.13.2 READY-TO-DRINK (RTD) SHAKES

12.13.3 SPECIALTY FORMULATIONS

12.13.4 BARS

12.13.5 LIQUID CONCENTRATES

12.13.6 MEAL REPLACEMENT SOUPS

12.13.7 OTHERS

12.14 NORTH AMERICA PEDIATRICS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.14.1 NORTH AMERICA

12.14.2 EUROPE

12.14.3 ASIA-PACIFIC

12.14.4 SOUTH AMERICA

12.14.5 MIDDLE EAST & AFRICA

12.15 NORTH AMERICA OTHERS IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

12.15.1 POWDERED MEAL REPLACEMENTS

12.15.2 READY-TO-DRINK (RTD) SHAKES

12.15.3 BARS

12.15.4 LIQUID CONCENTRATES

12.15.5 SPECIALTY FORMULATIONS

12.15.6 MEAL REPLACEMENT SOUPS

12.15.7 OTHERS

12.16 NORTH AMERICA OTHERS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.16.1 NORTH AMERICA

12.16.2 EUROPE

12.16.3 ASIA-PACIFIC

12.16.4 SOUTH AMERICA

12.16.5 MIDDLE EAST & AFRICA

13 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY REGION

13.1 NORTH AMERICA

13.1.1 U.S.

13.1.2 CANADA

13.1.3 MEXICO

14 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET: COMPANY LANDSCAPE

14.1 MANUFACTURER COMPANY SHARE ANALYSIS: GLOBAL

15 SWOT ANALYSIS

16 COMPANY PROFILES

16.1 ABBOTT

16.1.1 COMPANY SNAPSHOT

16.1.2 REVENUE ANALYSIS

16.1.3 COMPANY SHARE ANALYSIS

16.1.4 PRODUCT PORTFOLIO

16.1.5 RECENT DEVELOPMENT/ NEWS

16.2 HERBALIFE INTERNATIONAL OF AMERICA, INC.

16.2.1 COMPANY SNAPSHOT

16.2.2 REVENUE ANALYSIS

16.2.3 COMPANY SHARE ANALYSIS

16.2.4 PRODUCT PORTFOLIO

16.2.5 RECENT DEVELOPMENT

16.3 NESTLÉ S.A.

16.3.1 COMPANY SNAPSHOT

16.3.2 REVENUE ANALYSIS

16.3.3 COMPANY SHARE ANALYSIS

16.3.4 PRODUCT PORTFOLIO

16.3.5 RECENT DEVELOPMENT/ NEWS

16.4 GLANBIA PLC

16.4.1 COMPANY SNAPSHOT

16.4.2 REVENUE ANALYSIS

16.4.3 COMPANY SHARE ANALYSIS

16.4.4 PRODUCT PORTFOLIO

16.4.5 RECENT DEVELOPMENT/ NEWS

16.5 AMWAY CORP.

16.5.1 COMPANY SNAPSHOT

16.5.2 COMPANY SHARE ANALYSIS

16.5.3 PRODUCT PORTFOLIO

16.5.4 RECENT DEVELOPMENT

16.6 BERTRAND FOOD GMBH

16.6.1 COMPANY SNAPSHOT

16.6.2 PRODUCT PORTFOLIO

16.6.3 RECENT DEVELOPMENT

16.7 BOB’S RED MILL NATURAL FOODS

16.7.1 COMPANY SNAPSHOT

16.7.2 PRODUCT PORTFOLIO

16.7.3 RECENT DEVELOPMENT

16.8 FITSHIT HEALTH SOLUTIONS

16.8.1 COMPANY SNAPSHOT

16.8.2 PRODUCT PORTFOLIO

16.8.3 RECENT DEVELOPMENT

16.9 GENERAL MILLS INC.

16.9.1 COMPANY SNAPSHOT

16.9.2 REVENUE ANALYSIS

16.9.3 BRAND PORTFOLIO

16.9.4 RECENT DEVELOPMENT

16.1 GROWEQUAL LIMITED

16.10.1 COMPANY SNAPSHOT

16.10.2 PRODUCT PORTFOLIO

16.10.3 RECENT DEVELOPMENT

16.11 HUEL LIMITED

16.11.1 COMPANY SNAPSHOT

16.11.2 PRODUCT PORTFOLIO

16.11.3 RECENT DEVELOPMENT

16.12 JIMMY JOY

16.12.1 COMPANY SNAPSHOT

16.12.2 PRODUCT PORTFOLIO

16.12.3 RECENT DEVELOPMENT

16.13 LABRADA NUTRITION

16.13.1 COMPANY SNAPSHOT

16.13.2 PRODUCT PORTFOLIO

16.13.3 RECENT DEVELOPMENT

16.14 LYFEFUEL

16.14.1 COMPANY SNAPSHOT

16.14.2 PRODUCT PORTFOLIO

16.14.3 RECENT DEVELOPMENT

16.15 SAIPRO BIOTECH PVT. LTD.

16.15.1 COMPANY SNAPSHOT

16.15.2 PRODUCT PORTFOLIO

16.15.3 RECENT DEVELOPMENT

16.16 SATURO

16.16.1 COMPANY SNAPSHOT

16.16.2 PRODUCT PORTFOLIO

16.16.3 RECENT DEVELOPMENT

16.17 SO SHAPE, S.A.S.

16.17.1 COMPANY SNAPSHOT

16.17.2 PRODUCT PORTFOLIO

16.17.3 RECENT DEVELOPMENT

16.18 SOYLENT

16.18.1 COMPANY SNAPSHOT

16.18.2 PRODUCT PORTFOLIO

16.18.3 RECENT DEVELOPMENT

16.19 THE SIMPLY GOOD FOODS COMPANY

16.19.1 COMPANY SNAPSHOT

16.19.2 REVENUE ANALYSIS

16.19.3 PRODUCT PORTFOLIO

16.19.4 RECENT DEVELOPMENT

16.2 UNILEVER

16.20.1 COMPANY SNAPSHOT

16.20.2 REVENUE ANALYSIS

16.20.3 PRODUCT PORTFOLIO

16.20.4 RECENT DEVELOPMENT

17 QUESTIONNAIRE

18 RELATED REPORTS

List of Table

TABLE 1 VENDOR EVALUATION CRITERIA: NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET

TABLE 2 WEIGHTAGE ALLOCATION: NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET

TABLE 3 RAW MATERIAL COVERAGE DISTRIBUTION IN THE NORTH AMERICA MEAL REPLACEMENT PRODUCTS INDUSTRY

TABLE 4 BRAND COMPARATIVE ANALYSIS

TABLE 5 COMPANY VS PRODUCT OVERVIEW

TABLE 6 CONSUMER BUYING BEHAVIOR

TABLE 7 MEAL REPLACEMENT PRODUCTS HS CODES

TABLE 8 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 9 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (TONS)

TABLE 10 NORTH AMERICA POWDERED MEAL REPLACEMENTS IN MEAL REPLACEMENT PRODUCTS MARKET, BY FORMULATION, 2018-2033 (USD THOUSAND)

TABLE 11 NORTH AMERICA POWDERED MEAL REPLACEMENTS IN MEAL REPLACEMENT PRODUCTS MARKET, BY FLAVOR, 2018-2033 (USD THOUSAND)

TABLE 12 NORTH AMERICA POWDERED MEAL REPLACEMENTS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 13 NORTH AMERICA READY-TO-DRINK (RTD) SHAKES IN MEAL REPLACEMENT PRODUCTS MARKET, BY FLAVOR, 2018-2033 (USD THOUSAND)

TABLE 14 NORTH AMERICA READY-TO-DRINK (RTD) SHAKES IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 15 NORTH AMERICA BARS IN MEAL REPLACEMENT PRODUCTS MARKET, BY FLAVOR, 2018-2033 (USD THOUSAND)

TABLE 16 NORTH AMERICA BARS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 17 NORTH AMERICA LIQUID CONCENTRATES IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 18 NORTH AMERICA MEAL REPLACEMENT SOUPS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 19 NORTH AMERICA SPECIALTY FORMULATIONS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 20 NORTH AMERICA OTHERS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 21 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY INGREDIENT TYPE, 2018-2033 (USD THOUSAND)

TABLE 22 NORTH AMERICA PROTEIN IN MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 23 NORTH AMERICA WHEY IN MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 24 NORTH AMERICA PROTEIN IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 25 NORTH AMERICA CARBOHYDRATES IN MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 26 NORTH AMERICA CARBOHYDRATES IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 27 NORTH AMERICA FATS IN MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 28 NORTH AMERICA FATS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 29 NORTH AMERICA VITAMINS AND MINERALS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 30 NORTH AMERICA FIBER IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 31 NORTH AMERICA OTHERS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 32 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY FUNCTION, 2018-2033 (USD THOUSAND)

TABLE 33 NORTH AMERICA WEIGHT MANAGEMENT IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 34 NORTH AMERICA SPORTS NUTRITION IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 35 NORTH AMERICA WELLNESS & LIFESTYLE IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 36 NORTH AMERICA CLINICAL NUTRITION IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 37 NORTH AMERICA OTHERS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 38 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 39 NORTH AMERICA SUPERMARKETS / HYPERMARKETS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 40 NORTH AMERICA ONLINE RETAIL IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 41 NORTH AMERICA PHARMACY / DRUG STORES IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 42 NORTH AMERICA SPECIALTY STORES IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 43 NORTH AMERICA CONVENIENCE STORES IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 44 NORTH AMERICA OTHERS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 45 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 46 NORTH AMERICA ADULTS IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 47 NORTH AMERICA ADULTS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 48 NORTH AMERICA GERIATRIC POPULATION IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 49 NORTH AMERICA GERIATRIC POPULATION IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 50 NORTH AMERICA ATHLETES IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 51 NORTH AMERICA ATHLETES IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 52 NORTH AMERICA PEDIATRICS IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 53 NORTH AMERICA PEDIATRICS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 54 NORTH AMERICA OTHERS IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 55 NORTH AMERICA OTHERS IN MEAL REPLACEMENT PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 56 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, 2018-2033 (USD THOUSAND AND TONS)

TABLE 57 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 58 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (TONS)

TABLE 59 USD THOUSAND

TABLE 60 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 61 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (TONS)

TABLE 62 NORTH AMERICA POWDERED MEAL REPLACEMENTS IN MEAL REPLACEMENT PRODUCTS MARKET, BY FORMULATION, 2018-2033 (USD THOUSAND)

TABLE 63 NORTH AMERICA POWDERED MEAL REPLACEMENTS IN MEAL REPLACEMENT PRODUCTS MARKET, BY FLAVOR, 2018-2033 (USD THOUSAND)

TABLE 64 NORTH AMERICA READY-TO-DRINK (RTD) SHAKES IN MEAL REPLACEMENT PRODUCTS MARKET, BY FLAVOR, 2018-2033 (USD THOUSAND)

TABLE 65 NORTH AMERICA BARS IN MEAL REPLACEMENT PRODUCTS MARKET, BY FLAVOR, 2018-2033 (USD THOUSAND)

TABLE 66 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY INGREDIENT TYPE, 2018-2033 (USD THOUSAND)

TABLE 67 NORTH AMERICA PROTEIN IN MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 68 NORTH AMERICA WHEY IN MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 69 NORTH AMERICA CARBOHYDRATES IN MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 70 NORTH AMERICA FATS IN MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 71 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY FUNCTION, 2018-2033 (USD THOUSAND)

TABLE 72 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 73 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 74 NORTH AMERICA ADULTS IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 75 NORTH AMERICA GERIATRIC POPULATION IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 76 NORTH AMERICA ATHLETES IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 77 NORTH AMERICA PEDIATRICS IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 78 NORTH AMERICA OTHERS IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 79 USD THOUSAND

TABLE 80 U.S. MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 81 U.S. MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (TONS)

TABLE 82 U.S. POWDERED MEAL REPLACEMENTS IN MEAL REPLACEMENT PRODUCTS MARKET, BY FORMULATION, 2018-2033 (USD THOUSAND)

TABLE 83 U.S. POWDERED MEAL REPLACEMENTS IN MEAL REPLACEMENT PRODUCTS MARKET, BY FLAVOR, 2018-2033 (USD THOUSAND)

TABLE 84 U.S. READY-TO-DRINK (RTD) SHAKES IN MEAL REPLACEMENT PRODUCTS MARKET, BY FLAVOR, 2018-2033 (USD THOUSAND)

TABLE 85 U.S. BARS IN MEAL REPLACEMENT PRODUCTS MARKET, BY FLAVOR, 2018-2033 (USD THOUSAND)

TABLE 86 U.S. MEAL REPLACEMENT PRODUCTS MARKET, BY INGREDIENT TYPE, 2018-2033 (USD THOUSAND)

TABLE 87 U.S. PROTEIN IN MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 88 U.S. WHEY IN MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 89 U.S. CARBOHYDRATES IN MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 90 U.S. FATS IN MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 91 U.S. MEAL REPLACEMENT PRODUCTS MARKET, BY FUNCTION, 2018-2033 (USD THOUSAND)

TABLE 92 U.S. MEAL REPLACEMENT PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 93 U.S. MEAL REPLACEMENT PRODUCTS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 94 U.S. ADULTS IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 95 U.S. GERIATRIC POPULATION IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 96 U.S. ATHLETES IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 97 U.S. PEDIATRICS IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 98 U.S. OTHERS IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 99 USD THOUSAND

TABLE 100 CANADA MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 101 CANADA MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (TONS)

TABLE 102 CANADA POWDERED MEAL REPLACEMENTS IN MEAL REPLACEMENT PRODUCTS MARKET, BY FORMULATION, 2018-2033 (USD THOUSAND)

TABLE 103 CANADA POWDERED MEAL REPLACEMENTS IN MEAL REPLACEMENT PRODUCTS MARKET, BY FLAVOR, 2018-2033 (USD THOUSAND)

TABLE 104 CANADA READY-TO-DRINK (RTD) SHAKES IN MEAL REPLACEMENT PRODUCTS MARKET, BY FLAVOR, 2018-2033 (USD THOUSAND)

TABLE 105 CANADA BARS IN MEAL REPLACEMENT PRODUCTS MARKET, BY FLAVOR, 2018-2033 (USD THOUSAND)

TABLE 106 CANADA MEAL REPLACEMENT PRODUCTS MARKET, BY INGREDIENT TYPE, 2018-2033 (USD THOUSAND)

TABLE 107 CANADA PROTEIN IN MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 108 CANADA WHEY IN MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 109 CANADA CARBOHYDRATES IN MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 110 CANADA FATS IN MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 111 CANADA MEAL REPLACEMENT PRODUCTS MARKET, BY FUNCTION, 2018-2033 (USD THOUSAND)

TABLE 112 CANADA MEAL REPLACEMENT PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 113 CANADA MEAL REPLACEMENT PRODUCTS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 114 CANADA ADULTS IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 115 CANADA GERIATRIC POPULATION IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 116 CANADA ATHLETES IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 117 CANADA PEDIATRICS IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 118 CANADA OTHERS IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 119 USD THOUSAND

TABLE 120 MEXICO MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 121 MEXICO MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (TONS)

TABLE 122 MEXICO POWDERED MEAL REPLACEMENTS IN MEAL REPLACEMENT PRODUCTS MARKET, BY FORMULATION, 2018-2033 (USD THOUSAND)

TABLE 123 MEXICO POWDERED MEAL REPLACEMENTS IN MEAL REPLACEMENT PRODUCTS MARKET, BY FLAVOR, 2018-2033 (USD THOUSAND)

TABLE 124 MEXICO READY-TO-DRINK (RTD) SHAKES IN MEAL REPLACEMENT PRODUCTS MARKET, BY FLAVOR, 2018-2033 (USD THOUSAND)

TABLE 125 MEXICO BARS IN MEAL REPLACEMENT PRODUCTS MARKET, BY FLAVOR, 2018-2033 (USD THOUSAND)

TABLE 126 MEXICO MEAL REPLACEMENT PRODUCTS MARKET, BY INGREDIENT TYPE, 2018-2033 (USD THOUSAND)

TABLE 127 MEXICO PROTEIN IN MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 128 MEXICO WHEY IN MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 129 MEXICO CARBOHYDRATES IN MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 130 MEXICO FATS IN MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 131 MEXICO MEAL REPLACEMENT PRODUCTS MARKET, BY FUNCTION, 2018-2033 (USD THOUSAND)

TABLE 132 MEXICO MEAL REPLACEMENT PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 133 MEXICO MEAL REPLACEMENT PRODUCTS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 134 MEXICO ADULTS IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 135 MEXICO GERIATRIC POPULATION IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 136 MEXICO ATHLETES IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 137 MEXICO PEDIATRICS IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 138 MEXICO OTHERS IN MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

List of Figure

FIGURE 1 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET

FIGURE 2 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET: DATA TRIANGULATION

FIGURE 3 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET: DROC ANALYSIS

FIGURE 4 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET: REGIONAL VS COUNTRY MARKET ANALYSIS

FIGURE 5 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET: MULTIVARIATE MODELLING

FIGURE 7 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 8 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET: DBMR MARKET POSITION GRID

FIGURE 9 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET: VENDOR SHARE ANALYSIS

FIGURE 10 MARKET END USER COVERAGE GRID

FIGURE 11 EXECUTIVE SUMMARY

FIGURE 12 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET: SEGMENTATION

FIGURE 13 STRATEGIC DECISIONS

FIGURE 14 SEVEN SEGMENTS COMPRISE THE NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY TYPE (2025)

FIGURE 15 RISING HEALTH & WELLNESS AWARENESS AND RISING URBANIZATION AND CHANGING DIETARY PATTERNS IS EXPECTED TO DRIVE THE NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET IN THE FORECAST PERIOD OF 2026 TO 2033

FIGURE 16 POWDERED MEAL REPLACEMENT SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE NORTH AMERICA PIPE FABRICATION MARKET IN 2026 & 2033

FIGURE 17 VALUE CHAIN OF NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET-

FIGURE 18 DROC ANALYSIS

FIGURE 19 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY PRODUCT TYPE, 2025

FIGURE 20 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY INGREDIENT TYPE, 2025

FIGURE 21 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY FUNCTION, 2025

FIGURE 22 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2025

FIGURE 23 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET, BY END USER, 2025

FIGURE 24 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET: SNAPSHOT (2026)

FIGURE 25 NORTH AMERICA MEAL REPLACEMENT PRODUCTS MARKET: COMPANY SHARE 2025 (%)

North America Meal Replacement Products Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its North America Meal Replacement Products Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as North America Meal Replacement Products Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.