North America Medical Equipment Maintenance Market

Market Size in USD Billion

USD

23.96 Billion

USD

50.25 Billion

2025

2033

USD

23.96 Billion

USD

50.25 Billion

2025

2033

| 2026 - 2033 | |

| USD 23.96 Billion | |

| USD 50.25 Billion | |

| % | |

|

North America Medical Equipment Maintenance Market Size

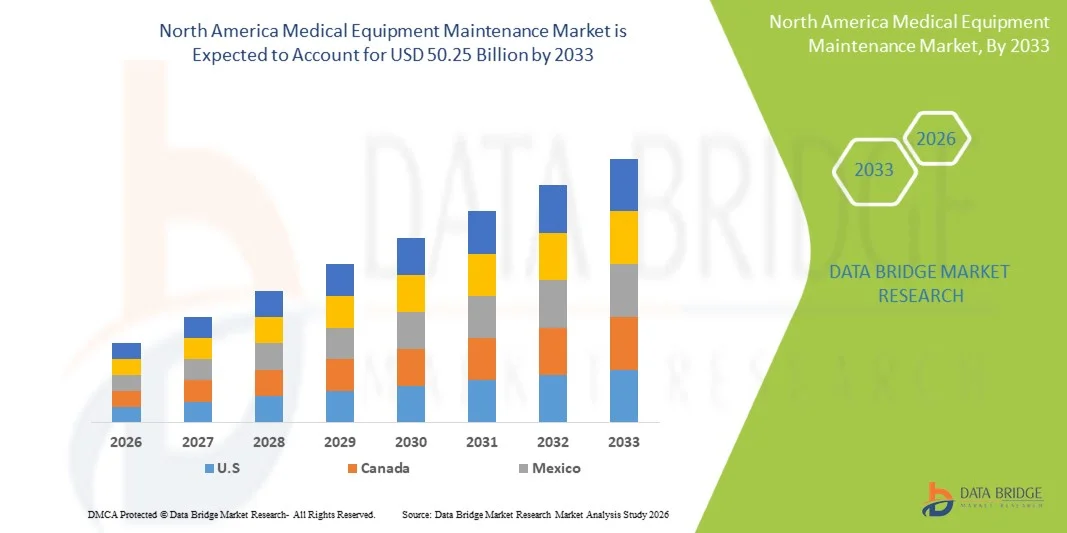

- The North America Medical Equipment Maintenance Market size was valued at USD 23.96 billion in 2025 and is expected to reach USD 50.25 billion by 2033, at a CAGR of 9.70% during the forecast period

- The market growth is largely fueled by increasing investments in healthcare infrastructure, rising adoption of advanced medical devices, and the growing need for efficient maintenance and calibration services across hospitals and diagnostic centers

- Furthermore, rising regulatory requirements, focus on patient safety, and the need to minimize equipment downtime are establishing comprehensive maintenance solutions as a critical component of healthcare operations. These converging factors are accelerating the uptake of Medical Equipment Maintenance solutions, thereby significantly boosting the industry's growth

North America Medical Equipment Maintenance Market Analysis

- Medical equipment maintenance services, including preventive, corrective, and operational maintenance, are increasingly vital components of modern healthcare systems across hospitals and diagnostic centers due to their role in ensuring equipment reliability, operational efficiency, and patient safety

- The escalating demand for medical equipment maintenance is primarily fueled by the growing adoption of advanced medical devices, increasing regulatory compliance requirements, rising healthcare infrastructure investments, and a strong focus on minimizing equipment downtime and improving clinical outcomes

- The U.S. dominated the North America Medical Equipment Maintenance Market with the largest revenue share of approximately 41.5% in 2025, driven by advanced healthcare infrastructure, high adoption of medical devices, and strong presence of key industry players, with hospitals and diagnostic centers investing heavily in preventive maintenance and calibration services

- Canada is expected to be the fastest-growing region in the North America Medical Equipment Maintenance Market during the forecast period, with a projected CAGR of 8.7%, supported by increasing healthcare expenditure, modernization of medical facilities, and rising demand for efficient maintenance solution

- The external service providers segment dominated the largest market revenue share of 52% in 2025, driven by cost efficiency and availability of specialized expertise. Hospitals and clinics prefer outsourcing maintenance services to third-party providers and OEMs to reduce operational burden

Report Scope and North America Medical Equipment Maintenance Market Segmentation

|

Attributes |

Medical Equipment Maintenance Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

• GE HealthCare (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

North America Medical Equipment Maintenance Market Trends

“Increasing Adoption of Predictive and Preventive Maintenance Solutions”

- A significant and accelerating trend in the North America Medical Equipment Maintenance Market is the growing adoption of predictive and preventive maintenance strategies aimed at minimizing equipment downtime and improving operational efficiency across healthcare facilities. This shift is enabling hospitals and diagnostic centers to proactively monitor equipment performance and ensure uninterrupted clinical operations

- For instance, in 2024, GE HealthCare introduced advanced predictive maintenance solutions integrated with digital monitoring platforms, enabling real-time tracking of imaging equipment performance and early detection of potential failures, thereby reducing unplanned downtime and maintenance costs

- The increasing use of connected medical devices and IoT-enabled systems is further supporting this trend, as healthcare providers can continuously track equipment health, schedule timely servicing, and extend the lifecycle of critical assets such as MRI machines, ventilators, and infusion pumps

- In addition, the rising complexity of modern medical equipment is encouraging healthcare providers to shift from reactive to preventive maintenance models, ensuring compliance with regulatory standards and improving patient safety outcomes

- The integration of data analytics and cloud-based platforms is also enhancing maintenance efficiency by providing actionable insights into equipment usage patterns, failure rates, and service requirements

- Furthermore, the growing emphasis on cost optimization in healthcare systems is driving the adoption of maintenance contracts and managed services, which offer predictable costs and improved service quality

- Healthcare facilities are increasingly prioritizing equipment uptime, especially in critical care units, where equipment failure can directly impact patient outcomes

- The expansion of multi-vendor service providers is also contributing to the trend, offering flexible and cost-effective maintenance solutions for diverse medical equipment portfolios

- Regulatory requirements for equipment safety and performance are further reinforcing the need for structured maintenance programs across hospitals and clinics

- This trend towards proactive, technology-driven maintenance solutions is significantly transforming how healthcare organizations manage their medical equipment infrastructure

North America Medical Equipment Maintenance Market Dynamics

Driver

“Growing Need Due to Increasing Healthcare Infrastructure and Equipment Utilization”

- The rapid expansion of healthcare infrastructure, coupled with the increasing utilization of advanced medical equipment, is a key driver for the growth of the North America Medical Equipment Maintenance Market

- For instance, in 2025, World Health Organization highlighted the rising global demand for diagnostic imaging and critical care equipment, prompting hospitals to invest significantly in maintenance services to ensure continuous and safe operations

- As hospitals and diagnostic centers continue to adopt technologically advanced devices, the need for regular maintenance, calibration, and repair services is becoming increasingly critical

- The growing number of surgical procedures and diagnostic tests is also contributing to higher equipment usage rates, thereby increasing wear and tear and the need for timely servicing

- Furthermore, the rising demand for high-quality patient care is compelling healthcare providers to maintain equipment in optimal working condition to avoid delays and errors in diagnosis and treatment

- Government initiatives aimed at improving healthcare infrastructure, particularly in emerging economies, are further driving the demand for maintenance service

- The increasing adoption of refurbished medical equipment is also boosting the need for maintenance, as these devices require frequent servicing to ensure reliability

- In addition, service contracts and outsourcing of maintenance activities are gaining traction, allowing healthcare providers to focus on core clinical operations

- The shortage of skilled biomedical engineers in some regions is also encouraging reliance on third-party maintenance service providersOverall, the continuous growth in healthcare facilities and equipment deployment is significantly fueling the demand for medical equipment maintenance services

Restraint/Challenge

“High Maintenance Costs and Shortage of Skilled Professionals”

- The high cost associated with medical equipment maintenance and the shortage of skilled professionals are major challenges hindering market growth

- For instance, according to American Hospital Association, hospitals in developed regions allocate a substantial portion of their operational budgets to equipment maintenance and servicing, which can strain financial resources, particularly for small and mid-sized healthcare facilities

- Advanced medical devices such as MRI scanners, CT systems, and robotic surgical equipment require specialized maintenance, which involves high service costs and expensive replacement parts

- The lack of adequately trained biomedical technicians in several regions further complicates maintenance processes, leading to delays and increased downtime

- In addition, reliance on original equipment manufacturers (OEMs) for servicing can limit flexibility and increase costs for healthcare providers

- Frequent technological upgrades in medical devices also require continuous training and skill development for maintenance personnel

- In emerging markets, limited access to quality maintenance services and infrastructure can negatively impact equipment performance and lifespan

- Budget constraints in public healthcare systems often lead to delayed maintenance, increasing the risk of equipment failure

- Furthermore, compliance with stringent regulatory standards adds to the complexity and cost of maintenance operations

- Addressing these challenges through workforce training, cost-effective service models, and technological advancements will be crucial for sustaining market growth

North America Medical Equipment Maintenance Market Scope

The market is segmented on the basis of service type, service providers, device type, level of maintenance, and end user.

• By Service Type

On the basis of service type, the North America Medical Equipment Maintenance Market is segmented into preventive, corrective, and performance/operational services. The preventive maintenance segment dominated the largest market revenue share of 47% in 2025, driven by the increasing focus on minimizing equipment downtime and ensuring patient safety. Hospitals and healthcare centers widely adopt preventive maintenance to extend the lifespan of high-value medical equipment such as imaging systems and surgical devices. Scheduled inspections, calibration, and routine servicing help avoid costly breakdowns and ensure regulatory compliance. Healthcare providers prefer preventive maintenance as it reduces unexpected failures and enhances operational efficiency. Government regulations and accreditation requirements further encourage routine maintenance practices. OEMs and service providers offer annual maintenance contracts (AMCs), boosting segment growth. Preventive maintenance is also cost-effective compared to emergency repairs. Increasing adoption of digital monitoring tools and predictive analytics further supports this segment. The rising volume of diagnostic procedures globally increases demand for reliable equipment performance. Overall, preventive maintenance remains essential for ensuring uninterrupted healthcare services

The corrective maintenance segment is expected to witness the fastest CAGR of 10.8% from 2026 to 2033, driven by the rising complexity of medical devices and increasing equipment usage. Corrective services are required for repairing malfunctioning or failed equipment, especially in high-demand hospital environments. Growing adoption of advanced imaging and diagnostic equipment increases the likelihood of technical faults, boosting demand for corrective services. Hospitals rely on specialized technicians and OEM support for quick issue resolution. The segment is also driven by the increasing number of aging medical devices requiring frequent repairs. Emerging markets contribute significantly due to limited preventive infrastructure. Service providers are offering rapid-response maintenance and remote troubleshooting solutions. Integration of AI-based diagnostics helps identify issues quickly, improving service efficiency. Increasing outsourcing of maintenance services further supports growth. High demand for uptime in critical care environments ensures continuous need for corrective services. Overall, increasing equipment complexity and utilization drive rapid expansion of this segment.

• By Service Providers

On the basis of service providers, the North America Medical Equipment Maintenance Market is segmented into in-house service providers and external service providers. The external service providers segment dominated the largest market revenue share of 52% in 2025, driven by cost efficiency and availability of specialized expertise. Hospitals and clinics prefer outsourcing maintenance services to third-party providers and OEMs to reduce operational burden. External providers offer comprehensive service packages, including installation, maintenance, and repair. These providers have access to advanced tools, trained professionals, and spare parts, ensuring efficient servicing. Outsourcing allows healthcare facilities to focus on core clinical operations. OEM partnerships also enhance reliability and compliance with regulatory standards. External providers offer flexible service contracts tailored to healthcare facility needs. Increasing adoption of multi-vendor service agreements further boosts this segment. Cost savings and improved service quality are key factors driving adoption. Overall, external providers remain the preferred choice for maintenance services globally.

The in-house service providers segment is expected to witness the fastest CAGR of 9.7% from 2026 to 2033, driven by the need for immediate response and better control over maintenance operations. Large hospitals and healthcare institutions are increasingly developing internal maintenance teams to reduce downtime. In-house teams ensure faster troubleshooting and minimize dependency on external vendors. Hospitals handling critical care equipment prefer in-house expertise for quick repairs. Technological advancements enable training of biomedical engineers within healthcare facilities. Cost savings over long-term operations also support this trend. Integration of digital maintenance management systems enhances efficiency. Growing emphasis on data security and equipment handling further drives in-house adoption. Emerging markets are witnessing increased investment in internal maintenance capabilities. The need for continuous monitoring and real-time support boosts this segment. Overall, operational control and faster service delivery fuel its rapid growth.

• By Device Type

On the basis of device type, the North America Medical Equipment Maintenance Market is segmented into imaging equipment, endoscopic devices, electromedical equipment, surgical instruments, and other medical equipment. The imaging equipment segment dominated the largest market revenue share of 49% in 2025, driven by the high cost and critical importance of devices such as MRI, CT scanners, and X-ray systems. These devices require regular calibration and maintenance to ensure accurate diagnostics. Hospitals and diagnostic centers heavily rely on imaging systems, increasing maintenance demand. High installation and repair costs further necessitate preventive maintenance. OEMs provide specialized service contracts for imaging equipment. Increasing diagnostic imaging procedures globally support segment growth. Regulatory requirements for imaging accuracy also drive maintenance demand. The complexity of imaging systems requires skilled technicians and advanced tools. Growing adoption of AI-enabled imaging devices increases maintenance needs. Overall, imaging equipment remains the dominant segment due to high value and critical application.

The electromedical equipment segment is expected to witness the fastest CAGR of 11.3% from 2026 to 2033, driven by increasing adoption of patient monitoring systems, ventilators, and therapeutic devices. Rising demand for critical care equipment boosts maintenance requirements. Hospitals and clinics require continuous monitoring equipment to function without interruption. Technological advancements in electromedical devices increase complexity, driving service demand. Home healthcare adoption also contributes to segment growth. Preventive and corrective maintenance ensures patient safety and device reliability. Growing healthcare infrastructure in emerging markets supports expansion. Integration of IoT-enabled monitoring systems enhances maintenance efficiency. Increasing focus on patient-centric care further drives demand. The segment benefits from continuous innovation and expanding applications. Overall, rising demand for advanced medical devices fuels rapid growth.

• By Level of Maintenance

On the basis of level of maintenance, the North America Medical Equipment Maintenance Market is segmented into Level 3 (specialized), Level 2 (technician), and Level 1 (user/first-line). The Level 3 (specialized) segment dominated the largest market revenue share of 44% in 2025, driven by the need for highly skilled professionals to maintain complex medical equipment. Specialized maintenance includes advanced diagnostics, calibration, and repair of sophisticated devices. Hospitals rely on OEM-certified experts for high-end equipment servicing. Increasing adoption of technologically advanced devices boosts demand for specialized maintenance. Regulatory compliance and quality standards further require expert handling. Level 3 services ensure high accuracy and reliability in equipment performance. Healthcare facilities invest heavily in specialized maintenance contracts. The segment benefits from increasing use of robotic surgery and AI-based systems. Overall, complexity and criticality of equipment drive dominance of this segment.

The Level 2 (technician) segment is expected to witness the fastest CAGR of 10.5% from 2026 to 2033, driven by the growing need for routine maintenance and intermediate repairs. Technician-level services are widely used for regular servicing and troubleshooting. Hospitals and clinics rely on trained technicians for efficient maintenance operations. Increasing number of healthcare facilities boosts demand for technician-level services. Training programs and certifications support workforce expansion. Integration of digital tools enhances technician efficiency. Cost-effectiveness compared to specialized services drives adoption. Emerging markets contribute significantly to growth. Technicians play a key role in preventive maintenance and equipment uptime. Overall, rising healthcare demand supports rapid expansion of this segment.

• By End User

On the basis of end user, the North America Medical Equipment Maintenance Market is segmented into hospitals, clinics, laboratories, and other healthcare centers. The hospitals segment dominated the largest market revenue share of 51% in 2025, driven by high patient inflow and extensive use of advanced medical equipment. Hospitals require continuous maintenance services to ensure uninterrupted operations. Large healthcare facilities invest in comprehensive maintenance contracts. Adoption of advanced diagnostic and therapeutic equipment increases service demand. Regulatory compliance and accreditation standards drive maintenance practices. Hospitals rely on both in-house and external service providers. Increasing surgical procedures and diagnostic tests boost equipment usage. Government and private hospital investments support growth. Overall, hospitals remain the largest consumers of maintenance services.

The clinics segment is expected to witness the fastest CAGR of 9.9% from 2026 to 2033, driven by the expansion of outpatient care and diagnostic services. Clinics are increasingly adopting advanced medical equipment, increasing maintenance needs. Growth in specialized clinics supports demand for service contracts. Cost-effective maintenance solutions drive adoption in smaller facilities. Rising patient preference for outpatient care boosts equipment usage. Technological advancements enable clinics to adopt compact diagnostic devices. Increasing healthcare access in emerging regions supports growth. Clinics are investing in preventive maintenance to avoid downtime. Integration of digital service solutions enhances efficiency. Overall, expanding healthcare infrastructure drives rapid growth in this segment.

North America Medical Equipment Maintenance Market Regional Analysis

- North America dominated the North America Medical Equipment Maintenance Market with the largest revenue share in 2025, driven by the presence of advanced healthcare infrastructure, high adoption of sophisticated medical devices, and strong emphasis on equipment uptime and patient safety across hospitals and diagnostic centers

- Healthcare providers in the region place significant importance on regular servicing, calibration, and preventive maintenance of critical medical equipment such as imaging systems, ventilators, and patient monitoring devices to ensure accurate diagnostics and uninterrupted clinical operations

- This widespread adoption is further supported by high healthcare spending, the presence of leading market players, and the increasing reliance on third-party service providers and annual maintenance contracts, establishing medical equipment maintenance as a critical component of healthcare operations

U.S. North America Medical Equipment Maintenance Market Insight

The U.S. North America Medical Equipment Maintenance Market captured the largest revenue share of approximately 41.5% in 2025 within North America, driven by the country’s highly developed healthcare system and extensive use of advanced medical technologies. Hospitals and diagnostic centers are heavily investing in preventive maintenance, equipment calibration, and lifecycle management services to ensure compliance with stringent regulatory standards and to minimize equipment downtime. The increasing volume of diagnostic and surgical procedures, along with the growing adoption of high-end imaging and critical care devices, is further propelling demand for maintenance services. Additionally, the strong presence of original equipment manufacturers (OEMs) and independent service organizations (ISOs) is contributing to the growth of the market in the U.S.

Canada North America Medical Equipment Maintenance Market Insight

The Canada North America Medical Equipment Maintenance Market is expected to grow at the fastest CAGR of 8.7% during the forecast period, supported by increasing healthcare expenditure and ongoing modernization of healthcare facilities across the country. The rising adoption of advanced diagnostic and therapeutic equipment in hospitals and clinics is driving the demand for efficient maintenance solutions. Furthermore, government initiatives aimed at strengthening healthcare infrastructure and improving service delivery are encouraging investments in maintenance services. The growing focus on equipment reliability, patient safety, and cost optimization is also prompting healthcare providers to adopt preventive and predictive maintenance strategies, thereby contributing to market expansion in Canada

North America Medical Equipment Maintenance Market Share

The Medical Equipment Maintenance industry is primarily led by well-established companies, including:

• GE HealthCare (U.S.)

• Siemens Healthineers (Germany)

• Philips Healthcare (Netherlands)

• Canon Medical Systems Corporation (Japan)

• Fujifilm Holdings Corporation (Japan)

• Hitachi High-Tech Corporation (Japan)

• Medtronic (Ireland)

• Drägerwerk AG (Germany)

• Stryker Corporation (U.S.)

• Getinge AB (Sweden)

• Althea Group (Italy)

• Aramark Healthcare Technologies (U.S.)

• ISS A/S (Denmark)

• Sodexo (France)

• Agiliti Health (U.S.)

• Crothall Healthcare (U.S.)

• TRIMEDX (U.S.)

• UHS (U.S.)

• TBS Group (Italy)

• Olympus Corporation (Japan)

Latest Developments in North America Medical Equipment Maintenance Market

- In June 2021, Koninklijke Philips N.V. announced a large-scale recall of its sleep apnea devices and ventilators due to potential health risks associated with foam degradation. This development significantly increased the demand for repair, replacement, and maintenance services globally, highlighting the critical importance of lifecycle maintenance and regulatory compliance in medical equipment management

- In January 2022, GE Healthcare expanded its digital service solutions by strengthening its remote monitoring and predictive maintenance capabilities for imaging and diagnostic equipment. These solutions leveraged data analytics and AI to reduce equipment downtime and improve operational efficiency for healthcare providers, marking a shift toward proactive maintenance models in the industry

- In March 2023, Siemens Healthineers expanded its service portfolio with advanced equipment lifecycle management solutions, focusing on predictive maintenance and performance optimization of imaging systems. The development aimed to enhance uptime, reduce operational costs, and support healthcare providers with integrated maintenance services

- In April 2024, Koninklijke Philips N.V. reached an agreement with the U.S. government to improve manufacturing quality and servicing processes for its respiratory devices following its earlier recall. The agreement allowed the company to continue servicing existing devices and emphasized stricter maintenance, repair, and compliance standards in the medical equipment sector

- In February 2025, GE HealthCare Technologies reported strong demand for medical devices and associated service solutions, including maintenance and lifecycle management services. The company highlighted continued investment in service capabilities to support growing equipment installations, reinforcing the importance of maintenance services as a core revenue stream

- In May 2025, Koninklijke Philips N.V. announced strategic adjustments to its supply chain and service operations to mitigate the impact of global tariffs, including enhancing localized maintenance and support services. This move aimed to ensure continuity in equipment servicing and reduce operational disruptions across key markets

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.