North America Ophthalmology Market

Market Size in USD Billion

USD

31.77 Billion

USD

52.37 Billion

2024

2032

USD

31.77 Billion

USD

52.37 Billion

2024

2032

| 2025 - 2032 | |

| USD 31.77 Billion | |

| USD 52.37 Billion | |

| % | |

North America Ophthalmology Market Analysis

The North America ophthalmology market has evolved significantly over the centuries, beginning with ancient treatments for eye conditions in Egypt and Greece. The field began to take shape in the 17th and 18th centuries, with the development of more advanced surgical techniques and tools. In the 19th century, innovations like the ophthalmoscope transformed diagnostic capabilities. The 20th century saw breakthroughs such as cataract surgery and the invention of intraocular lenses, along with the advent of LASIK surgery in the 1990s. The 21st century brought continued growth driven by an aging population, technological advancements, and the development of specialized diagnostic and surgical devices, including optical coherence tomography (OCT) and retinal imaging systems. Recent trends focus on the increasing use of artificial intelligence, telemedicine, and biologic therapies, such as gene therapy and stem cell treatments, further shaping the market's growth. Today, the ophthalmology market continues to expand due to rising eye disease prevalence, new technologies, and evolving treatment options.

North America Ophthalmology Market Size

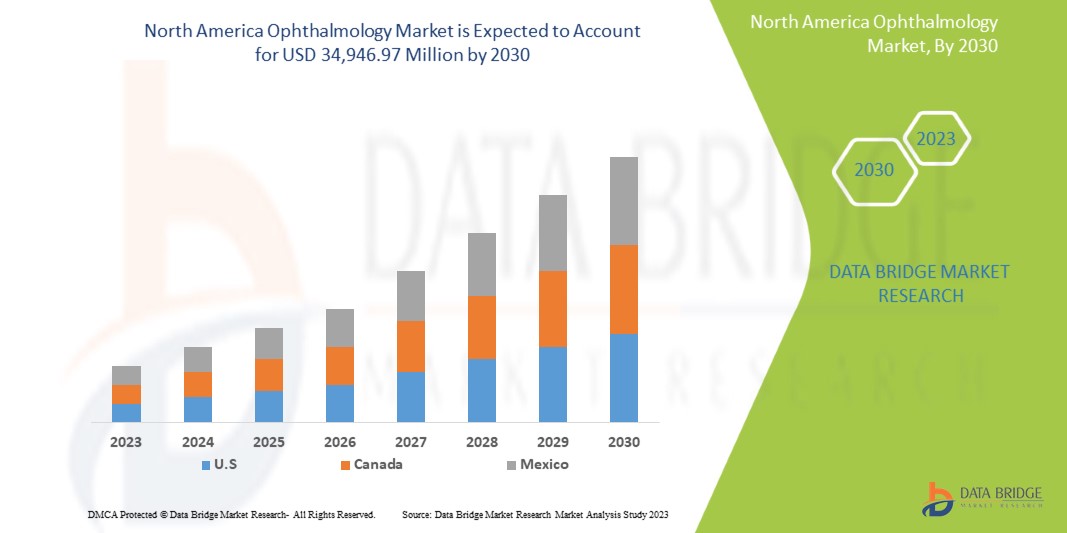

The North America ophthalmology market is expected to reach USD 52.37 billion by 2032 from USD 31.77 billion in 2024, growing at a CAGR of 6.5% in the forecast period of 2025 to 2032.

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework.

North America Ophthalmology Market Trends

“The Growing Adoption of Telemedicine and AI-Powered Diagnostic tools”

The North America ophthalmology market is the growing adoption of telemedicine and AI-powered diagnostic tools. These innovations are transforming the way eye care is delivered by enabling remote consultations and screenings, which increases accessibility, especially in underserved and rural areas. AI technologies, including machine learning algorithms, are being used to analyze retinal images, detect early signs of conditions like diabetic retinopathy, glaucoma, and macular degeneration, and provide faster, more accurate diagnoses. Telemedicine platforms allow patients to connect with ophthalmologists for follow-up consultations, reducing the need for in-person visits and making eye care more convenient and efficient. This trend is not only improving patient access to timely treatments but also enhancing the overall efficiency of healthcare systems, making it a key driver of market growth in the ophthalmology sector. As a result, the integration of these technologies is expected to continue expanding, particularly in emerging markets, where healthcare infrastructure is still developing.

Report Scope and North America Ophthalmology Market Segmentation

|

Attributes |

North America Ophthalmology Market Insights |

|

Segments Covered |

By Products: Device, Drugs, and Others By Diseases: Cataract, Refractive Disorders, Glaucoma, Age-Related Macular Degeneration, Inflammatory Diseases, and Others By Comprehensive Eye Examination: Refraction, Visual Acuity Test, Intraocular Pressure, Anterior Segment and Pupillary Examination, Visual Fields Test, Color Vision Test, and Others By End User: Clinics, Hospitals, Home Healthcare, and Others By Distribution Channel: Retail Sales, Direct Tender, and Others |

|

Region Covered |

U.S., Canada, and Mexico |

|

Key Market Players |

Alcon (Switzerland), Bausch + Lomb (Canada), Carl Zeiss Meditec (Germany), Hoya Corporation (Japan), Johnson & Johnson Services, Inc. (U.S.), Essilor International (France), Topcon Corporation(Japan), Glaukos Corporation (U.S.), Haag-Streit Group (Switzerland), Nidek Co., Ltd (U.S.), Staar Surgical (California), Ziemer Ophthalmic Systems Ag (Switzerland), Cooper Companies (U.S.), Lumenis Be Ltd. (Israel), Reichert Inc. (New York), Bayer Ag (Germany), Novartis Ag (Switzerland), Abbvie Inc.(U.S.), F. Hoffmann-La Roche Ltd. (Switzerland), Dompé (Italy), Santen Pharmaceutical Co. (Japan), Ltd among others. |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

North America Ophthalmology Market Definition

Ophthalmology is a branch of medicine and surgery that focuses on the diagnosis, treatment, and prevention of eye disorders and diseases. It includes medical and surgical care for conditions affecting the eyes and visual systems, such as cataracts, glaucoma, macular degeneration, and diabetic retinopathy.

North America Ophthalmology Market Definition Dynamics

Drivers

- Increasing Prevalence of Eye Diseases

The increasing prevalence of eye conditions, such as cataracts, macular degeneration, and diabetic retinopathy, is a significant driver of the North America ophthalmology market. As the North America population ages, the incidence of these conditions is rise. Cataracts, which lead to blurred vision and blindness, demand an expanding market for surgeries and corrective treatments. Similarly, macular degeneration and diabetic retinopathy are contributing to the need for advanced diagnostic tools and specialized therapies. The growing number of affected individuals ensures sustained demand for eye care services, including surgeries, medications, and innovative diagnostic technologies. This surge in eye diseases directly drives market expansion, as healthcare providers and manufacturers strive to meet the growing need for effective treatments and solutions.

For instance,

- In July 2022, according to the article published by NCBI, The prevalence of blindness rises with age, increasing from 0.45% in those aged 50-59 to 11.62% in individuals 80 and older. Females (2.31%) and rural residents (2.14%) experience higher rates. Visual impairment also affects 26.68% of participants, showing similar trends. This growing burden of eye diseases, particularly among the elderly, drives demand for ophthalmic treatments and technologies, boosting the ophthalmology market

- In August 2023, according to the article published by WHO, North America, over 2.2 billion people suffer from vision impairment, with nearly 1 billion cases being preventable or untreated. This growing prevalence of vision issues highlights the increasing demand for eye care services, treatments, and corrective solutions. As more people seek medical attention for preventable or unresolved conditions, the rising burden of eye diseases acts as a significant driver for the ophthalmology market

The rising prevalence of age-related eye conditions like cataracts, macular degeneration, and diabetic retinopathy is fueling the North America ophthalmology market. As the population ages, these diseases become more common, increasing the demand for treatments, surgeries, and diagnostic tools. The need for advanced technologies and therapies grows as more people require care. This surge in eye conditions drives market growth, as healthcare providers and manufacturers aim to meet the rising demand for effective solutions.

- Focus on Preventative Eye Care

There is a growing emphasis on preventative eye care and early detection of vision-related issues, which is playing a significant role in driving the North America ophthalmology market. As awareness about the importance of eye health increases, more people are seeking routine eye checkups to detect conditions like glaucoma, diabetic retinopathy, and cataracts in their early stages. Early diagnosis allows for timely interventions, reducing the risk of vision loss and improving overall eye health. This proactive approach is not only improving patient outcomes but also fueling demand for ophthalmic services, diagnostic tools, and corrective treatments. The growing focus on preventative care is leading to a surge in investments in eye care technologies, ophthalmic devices, and services, thereby contributing to the market's expansion. This trend strongly acts as a driver for growth in the ophthalmology sector.

For instance,

- In October 2022, according to the article published by National Eye Institute, National Eye Health Education Program(NEHEP) collaborates with health professionals to promote awareness on early detection, treatment of eye diseases, and the benefits of vision rehabilitation. It also targets populations at high risk of eye disease and vision loss. This focus on preventative care encourages people to seek timely eye checkups and treatments, driving demand for ophthalmic services, diagnostic tools, and products, thereby fueling the ophthalmology market

- In October 2024, according to the article published by Directorate General of Health Services, The National Programme for Control of Blindness and Visual Impairment (NPCB&VI) aims to reduce blindness prevalence by identifying and treating curable blindness at all healthcare levels. By focusing on early detection and addressing avoidable blindness, the program highlights the importance of preventative care. This initiative drives demand for eye care services, diagnostic tools, and treatments, contributing significantly to the growth of the North America ophthalmology market

The increasing focus on preventative eye care and early detection is significantly driving the North America ophthalmology market. As awareness of eye health rises, more individuals are opting for routine eye exams to identify conditions like glaucoma and cataracts early. Early detection allows for effective treatments that prevent further vision loss. This proactive approach is driving demand for diagnostic tools, ophthalmic services, and corrective treatments. The growing importance of preventative care is prompting investment in advanced eye care technologies, thus contributing to the overall growth of the ophthalmology market and ensuring its continued expansion.

Opportunities

- Rise in the Aging Population

The rise in the aging population presents a significant opportunity for the North America ophthalmology market, as older individuals are more susceptible to various eye disorders and diseases. Conditions such as cataracts, age-related macular degeneration (AMD), diabetic retinopathy, and glaucoma are prevalent among the elderly, creating a substantial demand for ophthalmic care and treatments. As a result, healthcare systems and ophthalmic providers are poised to expand their services, enhance diagnostic and therapeutic options, and cater to the unique needs of this demographic. This growing patient base necessitates an array of solutions, from surgical interventions and advanced drug therapies to vision correction products, ensuring a steady and increasing demand for ophthalmic procedures and products.

For instance,

- In March 2023, according to an article published in the National Library of Medicine, Cataract is a leading cause of visual impairment in old age. Lens opacification is notoriously associated with several geriatric conditions, including frailty, fall risk, depression and cognitive impairment. Moreover, according to the same source, in 2020, the leading worldwide causes of blindness in patients aged 50 years and older were cataract, followed by glaucoma, under-corrected refractive error, age-related macular degeneration, and diabetic retinopathy

- In August 2022, according to an article published in the American Academy of Ophthalmology, AMD is a common eye disease, usually found in adults over the age of 50. Moreover, it is stated that Half of Americans over the age of 75 develop cataracts

Moreover, addressing the eye health needs of the aging population can stimulate further investments in research and development within the ophthalmology sector. Pharmaceutical companies and medical device manufacturers are focus on creating innovative solutions tailored specifically for age-related conditions, potentially leading to breakthroughs in treatment protocols and patient care. The integration of new technologies, such as tele ophthalmology and advanced imaging techniques, facilitate better management of eye health in older adults, making it easier to monitor and treat conditions remotely. Overall, the aging population amplifies the need for existing ophthalmic services and presents a fertile ground for innovation and growth within the North America ophthalmology market.

- Rise in Online Retail and E-Health Platforms

The rise of online retail and e-health platforms offers a significant opportunity for the North America ophthalmology market by providing consumers with easier access to a wide array of eye care products and services. With the increasing adoption of e-commerce, patients can conveniently purchase items such as prescription glasses, contact lenses, and over-the-counter eye care products from the comfort of their homes. This trend is especially appealing to younger, tech-savvy consumers and those in remote areas with limited access to traditional optical stores. The ability to compare prices, read reviews, and access a wider range of products online enhances customer satisfaction and encourages usage, thereby driving growth in the ophthalmic product segment.

For instance,

- In September 2023, according to a news article from The Times of India, the 'pink eye' outbreak led to a surge in sales of ophthalmology medicine. Sales jumped nearly 30% year-on-year for the second month in a row in August - outgrowing the overall market by almost five times. The rise reflects the massive incidence of conjunctivitis and eye-complications in the last few months across the country

- In April 2020, according to an article, ‘Patient views about online purchasing of eyewear’, online purchasing of contact lenses is on the rise: 10%–20% of contact lens wearers in Australia, U.S. and the UK have considered or researched the possibility of Internet purchasing

In addition to retail opportunities, e-health platforms facilitate telehealth services that allow patients to consult with eye care professionals remotely. Virtual consultations for routine eye examinations, follow-ups, and triaging for more serious conditions can significantly improve access to care, particularly for older adults or individuals with mobility challenges. These platforms enhance patient engagement and adherence to eye health recommendations and allow ophthalmologists to reach a broader patient base without the constraints of geographic boundaries. Furthermore, the integration of digital health tools, such as mobile apps for monitoring eye health or managing chronic conditions, can create a seamless patient experience and foster proactive eye care, further propelling growth in the ophthalmology market.

Restraints/Challenges

- Side Effects and Complications Related to Eye Surgeries

Despite the significant advancements in ophthalmology treatments, certain ophthalmic procedures, particularly surgical interventions, carry risks of side effects and complications such as infection, scarring, or vision impairment. These potential risks can deter patients from undergoing specific therapies, especially those that involve invasive procedures. The fear of adverse outcomes, such as reduced vision or prolonged recovery times, can lead to hesitancy in seeking treatment, limiting the overall adoption of certain therapies. Additionally, complications arising from surgeries might require additional treatments, further raising healthcare costs and impacting patient trust in advanced treatments. This reluctance to undergo treatments due to the potential for negative side effects restricts the overall growth of the ophthalmology market by slowing down the adoption of new technologies and therapies.

For instance,

- In October 2024, according to the article published by Harvard Health, Modern eye surgeries, while effective in treating conditions like cataracts and glaucoma, often lead to complications such as dry eye disease, characterized by a burning, gritty, or itchy sensation. This side effect can be uncomfortable and discouraging for patients, leading some to hesitate or avoid eye surgeries. As a result, complications from treatments act as a restraint on the growth of the ophthalmology market

- In July 2021, according to the article published by Medical News Today, Up to 95% of individuals who undergo laser eye surgery may experience dry eyes, while 20% report visual disturbances like glare or halos. Additionally, 1 in 50 people may suffer from blurry vision or “sands of Sahara” syndrome. These side effects can discourage patients from opting for surgery, limiting the adoption of laser procedures and acting as a restraint on the ophthalmology market’s growth

Despite advancements in ophthalmology, some surgical treatments carry risks such as infection, scarring, or vision impairment. These complications can discourage patients from opting for certain therapies, particularly invasive procedures. The fear of adverse outcomes and additional treatment costs can hinder patient willingness to seek care, slowing the adoption of new treatments. This reluctance limits the growth of the North America ophthalmology market.

- Limited Access to specialized Ophthalmic Care in Rural Areas

Despite advancements in healthcare infrastructure, access to specialized ophthalmic care remains limited in rural and remote areas, significantly hindering the growth potential of the ophthalmology market in these regions. Many rural populations still face challenges such as a lack of trained eye care professionals, inadequate facilities, and limited access to advanced diagnostic and treatment technologies. As a result, individuals in these areas often struggle to receive timely diagnosis and treatment for eye conditions, leading to a higher incidence of preventable blindness and vision impairment. The limited availability of specialized care restricts market expansion by reducing the adoption of advanced eye care services and products. This barrier to access continues to act as a major restraint on the North America ophthalmology market’s overall growth.

For instance,

- In February 2023, according to the article published by NCBI, India's large rural population faces significant unmet eye care needs, with most facilities and professionals concentrated in urban and semi-urban areas. The disparity in access to eye care between rural and urban regions remains a challenge, limiting treatment availability. This unequal distribution of healthcare resources restricts the growth of the North America ophthalmology market by preventing widespread access to essential services in rural areas

- In March 2024, according to the article published by Research Gate, The lack of connectivity and trained staff in remote areas hampers access to continuous eye care, even after successful eye camps. Patients in these areas struggle to receive follow-up care or advanced treatments due to the absence of proper infrastructure. This gap in healthcare delivery limits the reach and effectiveness of eye care programs, acting as a restraint on the North America ophthalmology market's growth

Access to specialized eye care is still limited in rural areas, despite healthcare improvements. The shortage of eye care professionals, advanced technology, and facilities prevents timely treatment and diagnosis, leading to higher rates of avoidable blindness. This limited access hampers the growth of the North America ophthalmology market by restricting adoption of advanced treatments and services in these regions.

North America Ophthalmology Market Scope

The market is segmented on the basis of products, diseases, comprehensive eye examination, end user, and distribution channel. The growth amongst these segments will help you analyze meagre growth segments in the industries and provide the users with a valuable market overview and market insights to help them make strategic decisions for identifying core market applications.

By Products

- Device

- Surgical Device

- Cataract Surgical Devices

- Ophthalmic Viscoelastic Devices

- Phacoemulsification Devices

- Cataract Surgical Lasers

- IOL Injectors

- Vitreoretinal Surgical Devices

- Vitrectomy Machines

- Vitreoretinal Packs

- Photocoagulation Lasers

- Vitrectomy Probes

- Illumination Devices

- Refractive Surgical Devices

- Femtosecond Lasers

- Excimer Lasers

- Other Refractive Surgical Lasers

- Glaucoma Surgical Devices

- Glaucoma Drainage Devices

- Microinvasive Glaucoma Surgery Devices

- Glaucoma Laser Systems

- Diagnostic Device

- Optical Coherence Tomography (OCT) Scanners

- Autorefractors & Keratometers

- Tonometers

- Phoropters

- Retinoscopes

- Ophthalmoscopes

- Slit lamps

- Perimeters/Visual Field Analyzers

- Corneal Topography Systems

- Fundus Cameras

- Ophthalmic Ultrasound Imaging Systems

- A- Scan Imaging System

- B-Scan Imaging System

- Pachymeters

- Ultrasound Biomicroscopes

- Lensmeters

- Wavefront Aberrometers

- Optical biometry Systems

- Specular Microscopes

- Chart Projectors

- Ophthalmic Surgical Accessories

- Surgical Instruments & Kits

- Ophthalmic Forceps

- Ophthalmic Spatula

- Ophthalmic Tips and Handles

- Ophthalmic Cannulas

- Ophthalmic Scissors

- Others Surgical Accessories

- Ophthalmic Microscopes

- Surgical Device

- Drugs, By Products

- Anti-VEGF Drugs

- Ranibizumab

- Bevacizumab

- Retinal Disorder Drugs

- Anti-Glaucoma Drugs

- Prostaglandin Analogs

- Latanoprost

- Bimatoprost

- Travoprost

- Tafluprost

- Latanoprostene

- BETA Adrenergic Antagonists

- Timolal Maleate

- Betaxolol

- Alpha Adrenergic Agonists

- Epinephrine

- Depiveprine

- Miotics

- Pilocarpine

- Eserine

- Prostaglandin Analogs

- Dry Eye Drugs

- Anti-Inflammatory Drugs

- Steroidal anti-Inflammatory Drugs

- Non-steroidal Anti-Inflammatory Drugs

- Allergic Conjuctivitis Drugs

- Others

- Anti-VEGF Drugs

- Drugs, By Drug Type

- Branded

- Generic

- Drugs, By Presciption Mode

- Prescription

- Over the Counter

- Drugs, By Route of Administration

- Topical

- Eye Drops

- Eye Solution

- Cream & Ointments

- Gel

- Others

- Local Ocular

- Intravitreal

- Subconjunctival

- Retrobulbar

- Intracameral

- Injectables

- Intramuscular

- Intravenous

- Others

- Oral

- Tablet

- Capsules

- Others

- Others

- Topical

- Others

- Vision Care Products

- Spectacles

- Contact Lenses

- Soft Contact Lenses

- Hybrid Contact Lenses

- Rigid Gas Permeable Lenses

- Others

- Vision Care Products

By Diseases

- Cataract

- Refractive Disorders

- Glaucoma

- Age-related Macular Degeneration

- Inflammatory Diseases

- Others

By Comprehensive Eye Examination

- Refraction

- Automated Refractometers

- Set of Trial Lenses

- Cycloplegic Drugs

- Trial Frame

- Self-Illuminated/ Mirror Retinoscope

- Jackson Cross Cylinder

- Visual Acuity Test

- Snellen's Chart

- Near Vision Charts

- Intraocular Pressure

- Tonometers (Goldmann, Tono-Pen, Perkins, Shiotz)

- Others

- Anterior Segment and Pupillary Examination

- Slit Lamp Biomicroscope

- Torch Light

- Visual Fields Test

- Central 30-2 Full Threshold Humphrey Visual Field Analyzer

- Frequency Doubling Perimeter

- Goldmann Kinetic Perimeter

- Color Vision Test

- Others

By End User

- Clinics

- Hospitals

- Home Healthcare

- Others

By Distribution Channel

- Retail sales

- Retail Shops

- Hospital Pharmacy

- Online Pharmacy

- Direct Tender

- Others

North America Ophthalmology Market Regional Analysis

The market is segmented on the basis of products, diseases, comprehensive eye examination, end user, and distribution channel.

The countries covered in this market are U.S, Canada, and Mexico.

U.S. is expected to dominate the market due to advanced healthcare infrastructure, high healthcare spending, and a large aging population with a growing prevalence of eye diseases. Additionally, significant investments in research, development, and the adoption of cutting-edge technologies drive market leadership in the region.

The country section of the report also provides individual market impacting factors and changes in regulation in the market domestically that impacts the current and future trends of the market. Data points like down-stream and upstream value chain analysis, technical trends and porter's five forces analysis, case studies are some of the pointers used to forecast the market scenario for individual countries. Also, the presence and availability of North America brands and their challenges faced due to large or scarce competition from local and domestic brands, impact of domestic tariffs and trade routes are considered while providing forecast analysis of the country data.

North America Ophthalmology Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, North America presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

North America Ophthalmology Market Leaders Operating in the Market Are:

- Alcon (Switzerland)

- Bausch + Lomb (Canada)

- Carl Zeiss Meditec( Germany)

- Hoya Corporation (Japan)

- Johnson & Johnson Services, Inc. (U.S.)

- Essilor International (France)

- Topcon Corporation(Japan)

- Glaukos Corporation (U.S.)

- Haag-Streit Group (Switzerland)

- Nidek Co., Ltd (U.S.)

- Staar Surgical (California)

- Ziemer Ophthalmic Systems Ag (Switzerland)

- Cooper Companies (U.S.)

- Lumenis Be Ltd. (Israel)

- Reichert Inc. (New York)

- Bayer Ag (Germany)

- Novartis Ag (Switzerland)

- Abbvie Inc. (U.S.)

- F. Hoffmann-La Roche Ltd.(Switzerland)

- Dompé (Italy)

- Santen Pharmaceutical Co.(Japan), Ltd

Latest Developments in North America Ophthalmology Market

- In October 2024, At the AAO 2024 meeting, Alcon showcased its innovations, including the Voyager DSLT for glaucoma treatment, UNIFEYE and UNIPEXY handheld gas delivery systems, and pivotal data for AR-15512, a dry eye treatment. These advancements aimed to improve outcomes and surgical efficiency

- In September 2024, EssilorLuxottica and Meta have extended their partnership, entering a long-term agreement to develop multi-generational smart eyewear products. Building on the success of Ray-Ban Meta glasses, the companies aim to shape the future of wearable technology together

- In OCTOBER 2024, Bausch + Lomb presented new scientific data and educational events at the 2024 AAO meeting in Chicago. Highlights included studies on the enVista Envy IOL, TENEO Excimer Laser, VYZULTA, and presentations on Blink Nutritears, MIEBO, and Xiidra

- In April 2024, AbbVie has completed its acquisition of Cerevel Therapeutics, enhancing its neuroscience portfolio. The acquisition includes Cerevel’s promising clinical-stage assets like Emraclidine for schizophrenia and Tavapadon for Parkinson's disease, strengthening AbbVie’s position in neurology and psychiatry

- In September, 2023, Novartis completed the divestment of its 'front of eye' ophthalmology assets to Bausch + Lomb for up to USD 2.5 billion, including USD 1.75 billion in upfront cash and potential milestone payments. The deal included Xiidra, SAF312, AcuStream, and OJL332. Novartis advanced its strategy to focus on prioritized therapeutic areas for future growth

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF THE NORTH AMERICA OPHTHALMOLOGY MARKET

1.4 CURRENCY AND PRICING

1.5 LIMITATIONS

1.6 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 DBMR TRIPOD DATA VALIDATION MODEL

2.5 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.6 MULTIVARIATE MODELLING

2.7 MARKET APPLICATION COVERAGE GRID

2.8 PRODUCT LIFELINE CURVE

2.9 DBMR MARKET POSITION GRID

2.1 VENDOR SHARE ANALYSIS

2.11 SECONDARY SOURCES

2.12 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PESTAL ANALYSIS

4.2 PORTERS FIVE FORCES ANALYSIS

5 NORTH AMERICA OPHTHALMOLOGY MARKET : REGULATIONS

6 MARKET OVERVIEW

6.1 DRIVERS

6.1.1 INCREASING PREVALENCE OF EYE DISEASES

6.1.2 FOCUS ON PREVENTATIVE EYE CARE

6.1.3 GOVERNMENT EYECARE INITIATIVES

6.1.4 INNOVATIONS IN OPHTHALMIC SURGICAL TECHNIQUES

6.2 RESTRAINTS

6.2.1 SIDE EFFECTS AND COMPLICATIONS RELATED TO EYE SURGERIES

6.2.2 LIMITED ACCESS TO SPECIALIZED OPHTHALMIC CARE IN RURAL AREAS

6.3 OPPORTUNITIES

6.3.1 RISE IN THE AGING POPULATION

6.3.2 RISE IN ONLINE RETAIL AND E-HEALTH PLATFORMS

6.3.3 ENHANCED PATIENT EDUCATION

6.4 CHALLENGES

6.4.1 RISING COSTS OF OPHTHALMIC TREATMENTS

6.4.2 SHORTAGE OF EYE CARE PROFESSIONALS

7 NORTH AMERICA OPHTHALMOLOGY MARKETNORTH AMERICA OPHTHALMOLOGY MARKET, BY PRODUCTS

7.1 OVERVIEW

7.2 DEVICE

7.2.1 SURGICAL DEVICE

7.2.1.1 CATARACT SURGICAL DEVICES

7.2.1.2 OPHTHALMIC VISCOELASTIC DEVICES

7.2.1.2.1 PHACOEMULSIFICATION DEVICES

7.2.1.2.2 CATARACT SURGICAL LASERS

7.2.1.2.3 IOL INJECTORS

7.2.1.3 VITREORETINAL SURGICAL DEVICES

7.2.1.3.1 VITREORETINAL PACKS

7.2.1.3.2 VITRECTOMY MACHINES

7.2.1.3.3 VITRECTOMY PROBES

7.2.1.3.4 PHOTOCOAGULATION LASERS

7.2.1.3.5 ILLUMINATION DEVICES

7.2.1.4 REFRACTIVE SURGICAL DEVICES

7.2.1.4.1 FEMTOSECOND LASERS

7.2.1.4.2 EXCIMER LASERS

7.2.1.4.3 OTHER REFRACTIVE SURGICAL LASERS

7.2.1.5 GLAUCOMA SURGICAL DEVICES

7.2.1.5.1 GLAUCOMA DRAINAGE DEVICES

7.2.1.5.2 GLAUCOMA LASER SYSTEMS

7.2.1.5.3 MICRO INVASIVE GLAUCOMA SURGERY DEVICES

7.2.2 DIAGNOSTIC DEVICE

7.2.2.1 OPTICAL COHERENCE TOMOGRAPHY (OCT) SCANNERS

7.2.2.2 AUTOREFRACTORS & KERATOMETERS

7.2.2.3 TONOMETERS

7.2.2.4 PHOROPTERS

7.2.2.5 RETINOSCOPES

7.2.2.6 OPHTHALMOSCOPES

7.2.2.7 SLIT LAMPS

7.2.2.8 PERIMETERS/VISUAL FIELD ANALYZERS

7.2.2.9 CORNEAL TOPOGRAPHY SYSTEMS

7.2.2.10 FUNDUS CAMERAS

7.2.2.11 OPHTHALMIC ULTRASOUND IMAGING SYSTEMS

7.2.2.11.1 A- SCAN IMAGING SYSTEM

7.2.2.11.2 B-SCAN IMAGING SYSTEM

7.2.2.11.3 PACHYMETERS

7.2.2.11.4 ULTRASOUND BIOMICROSCOPES

7.2.2.12 LENSMETERS

7.2.2.13 WAVEFRONT ABERROMETERS

7.2.2.14 OPTICAL BIOMETRY SYSTEMS

7.2.2.15 SPECULAR MICROSCOPES

7.2.2.16 CHART PROJECTORS

7.2.3 OPHTHALMIC SURGICAL ACCESSORIES

7.2.3.1 SURGICAL INSTRUMENTS & KITS

7.2.3.2 OPHTHALMIC FORCEPS

7.2.3.3 OPHTHALMIC SPATULA

7.2.3.4 OPHTHALMIC TIPS AND HANDLES

7.2.3.5 OPHTHALMIC CANNULAS

7.2.3.6 OPHTHALMIC SCISSORS

7.2.3.7 OTHERS SURGICAL ACCESSORIES

7.2.4 OPHTHALMIC MICROSCOPES

7.3 DRUGS

7.3.1 ANTI-VEGF DRUGS

7.3.1.1 RANIBIZUMAB

7.3.1.2 BEVACIZUMAB

7.3.2 ANTI-GLAUCOMA DRUGS

7.3.2.1 PROSTAGLANDIN ANALOGS

7.3.2.1.1 LATANOPROST

7.3.2.1.2 BIMATOPROST

7.3.2.1.3 TRAVOPROST

7.3.2.1.4 TAFLUPROST

7.3.2.1.5 LATANOPROSTENE

7.3.2.2 BETA ADRENERGIC ANTAGONISTS

7.3.2.2.1 TIMOLAL MALEATE

7.3.2.2.2 BETAXOLOL

7.3.2.3 ALPHA ADRENERGIC AGONISTS

7.3.2.3.1 EPINEPHRINE

7.3.2.3.2 DEPIVEPRINE

7.3.2.4 MIOTICS

7.3.2.4.1 PILOCARPINE

7.3.2.4.2 ESERINE

7.3.3 ANTI-INFLAMMATION DRUGS

7.3.3.1 STEROIDAL ANTI-INFLAMMATORY DRUGS

7.3.3.2 NON-STEROIDAL ANTI-INFLAMMATORY DRUGS

7.3.4 RETINAL DISORDER DRUGS

7.3.5 DRY EYE DRUGS

7.3.6 ALLERGIC CONJUCTIVITIS DRUGS

7.3.7 OTHERS

7.3.7.1 BRANDED

7.3.7.2 GENERIC

7.3.7.3 PRESCRIPTION

7.3.7.4 OVER THE COUNTER

7.3.7.5 TOPICAL

7.3.7.6 LOCAL OCULAR

7.3.7.7 INJECTABLES

7.3.7.8 ORAL

7.3.7.9 OTHERS

7.3.7.10 EYE DROPS

7.3.7.11 EYE SOLUTION

7.3.7.12 CREAM & OINTMENTS

7.3.7.13 GEL

7.3.7.14 OTHERS

7.3.7.15 INTRAVITREAL

7.3.7.16 SUBCONJUNCTIVAL

7.3.7.17 RETROBULBAR

7.3.7.18 INTRACAMERAL

7.3.7.19 INTRAMUSCULAR

7.3.7.20 INTRAVENOUS

7.3.7.21 OTHERS

7.3.7.22 TABLET

7.3.7.23 CAPSULES

7.3.7.24 OTHERS

7.4 OTHERS

7.4.1 VISION CARE PRODUCTS

7.4.1.1 SPECTACLES

7.4.1.2 CONTACT LENSES

7.4.1.2.1 SOFT CONTACT LENSES

7.4.1.2.2 HYBRID CONTACT LENSES

7.4.1.2.3 RIGID GAS PERMEABLE LENSES

7.4.2 OTHERS

8 NORTH AMERICA OPHTHALMOLOGY MARKET, BY DISEASES

8.1 OVERVIEW

8.2 CATARACT

8.3 REFRACTIVE DISORDERS

8.4 GLAUCOMA

8.5 AGE-RELATED MACULAR DEGENERATION

8.6 INFLAMMATORY DISEASES

8.7 OTHERS

9 NORTH AMERICA OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION

9.1 OVERVIEW

9.2 REFRACTION

9.2.1 AUTOMATED REFRACTOMETERS

9.2.2 SET OF TRIAL LENSES

9.2.3 CYCLOPLEGIC DRUGS

9.2.4 TRIAL FRAME

9.2.5 SELF-ILLUMINATED/ MIRROR RETINOSCOPE

9.2.6 JACKSON CROSS CYLINDER

9.3 VISUAL ACUITY TEST

9.3.1 SNELLEN'S CHART

9.3.2 NEAR VISION CHARTS

9.4 INTRAOCULAR PRESSURE

9.4.1 TONOMETERS (GOLDMANN, TONO-PEN, PERKINS, SHIOTZ)

9.4.2 OTHERS

9.5 ANTERIOR SEGMENT AND PUPILLARY EXAMINATION

9.5.1 SLIT LAMP BIOMICROSCOPE

9.5.2 TORCH LIGHT

9.6 VISUAL FIELDS TEST

9.6.1 CENTRAL 30-2 FULL THRESHOLD HUMPHREY VISUAL FIELD ANALYZER

9.6.2 FREQUENCY DOUBLING PERIMETER

9.6.3 GOLDMANN KINETIC PERIMETER

9.7 COLOR VISION TEST

9.8 OTHERS

10 NORTH AMERICA OPHTHALMOLOGY MARKET, BY END USER

10.1 OVERVIEW

10.2 CLINICS

10.3 HOSPITALS

10.4 HOME HEALTHCARE

10.5 OTHERS

11 NORTH AMERICA OPHTHALMOLOGY MARKET, BY DISTRIBUTION CHANNEL

11.1 OVERVIEW

11.2 RETAIL SALES

11.2.1 RETAIL SHOPS

11.2.2 HOSPITAL PHARMACY

11.2.3 ONLINE PHARMACY

11.3 DIRECT TENDER

11.4 OTHERS

12 NORTH AMERICA OPHTHALMOLOGY MARKET BY GEOGRAPHY

12.1 NORTH AMERICA

12.1.1 U.S.

12.1.2 CANADA

12.1.3 MEXICO

13 NORTH AMERICA OPHTHALMOLOGY MARKET: COMPANY LANDSCAPE

13.1 COMPANY SHARE ANALYSIS: NORTH AMERICA

14 SWOT ANALYSIS

15 COMPANY PROFILES

15.1 ALCON

15.1.1 COMPANY SNAPSHOT

15.1.2 REVENUE ANALYSIS

15.1.3 COMPANY SHARE ANALYSIS

15.1.4 PRODUCT PORTFOLIO

15.1.5 RECENT DEVELOPMENT

15.2 JOHNSON & JOHNSON SERVICES, INC.

15.2.1 COMPANY SNAPSHOT

15.2.2 REVENUE ANALYSIS

15.2.3 COMPANY SHARE ANALYSIS

15.2.4 PRODUCT PORTFOLIO

15.2.5 RECENT DEVELOPMENT

15.3 ESSILOR LUXOTTICA

15.3.1 COMPANY SNAPSHOT

15.3.2 REVENUE ANALYSIS

15.3.3 COMPANY SHARE ANALYSIS

15.3.4 PRODUCT PORTFOLIO

15.3.5 RECENT DEVELOPMENT

15.4 NOVARTIS AG

15.4.1 COMPANY SNAPSHOT

15.4.2 REVENUE ANALYSIS

15.4.3 COMPANY SHARE ANALYSIS

15.4.4 PRODUCT PORTFOLIO

15.4.5 RECENT DEVELOPMENT

15.5 BAUSCH + LOMB

15.5.1 COMPANY SNAPSHOT

15.5.2 COMPANY SHARE ANALYSIS

15.5.3 REVENUE ANALYSIS

15.5.4 PRODUCT PORTFOLIO

15.5.5 RECENT DEVELOPMENT

15.6 ABBVIE INC.

15.6.1 COMPANY SNAPSHOT

15.6.2 REVENUE ANALYSIS

15.6.3 PRODUCT PORTFOLIO

15.6.4 RECENT DEVELOPMENT

15.7 BAYER AG

15.7.1 COMPANY SNAPSHOT

15.7.2 REVENUE ANALYSIS

15.7.3 PRODUCT PORTFOLIO

15.7.4 RECENT DEVELOPMENT

15.8 CARL ZEISS MEDITEC AG

15.8.1 COMPANY SNAPSHOT

15.8.2 REVENUE ANALYSIS

15.8.3 PRODUCT PORTFOLIO

15.8.4 RECENT DEVELOPMENT

15.9 COOPER COMPANIES

15.9.1 COMPANY SNAPSHOT

15.9.2 REVENUE ANALYSIS

15.9.3 PRODUCT PORTFOLIO

15.1 DOMPÉ

15.10.1 COMPANY SNAPSHOT

15.10.2 PRODUCT PORTFOLIO

15.10.3 RECENT DEVELOPMENT

15.11 F. HOFFMANN-LA ROCHE LTD

15.11.1 COMPANY SNAPSHOT

15.11.2 REVENUE ANALYSIS

15.11.3 PRODUCT PORTFOLIO

15.11.4 RECENT DEVELOPMENT

15.12 GLAUKOS CORPORATION

15.12.1 COMPANY SNAPSHOT

15.12.2 REVENUE ANALYSIS

15.12.3 PRODUCT PORTFOLIO

15.12.4 RECENT DEVELOPMENT

15.13 HAAG-STREIT

15.13.1 COMPANY SNAPSHOT

15.13.2 PRODUCT PORTFOLIO

15.13.3 RECENT DEVELOPMENT

15.14 HOYA CORPORATION

15.14.1 COMPANY SNAPSHOT

15.14.2 REVENUE ANALYSIS

15.14.3 PRODUCT PORTFOLIO

15.14.4 RECENT DEVELOPMENT

15.15 LUMENIS BE LTD.

15.15.1 COMPANY SNAPSHOT

15.15.2 PRODUCT PORTFOLIO

15.15.3 RECENT DEVELOPMENT

15.16 NIDEK CO.

15.16.1 COMPANY SNAPSHOT

15.16.2 PRODUCT PORTFOLIO

15.16.3 RECENT DEVELOPMENT

15.17 REICHERT, INC

15.17.1 COMPANY SNAPSHOT

15.17.2 REVENUE ANALYSIS

15.17.3 PRODUCT PORTFOLIO

15.17.4 RECENT DEVELOPMENT

15.18 SANTEN PHARMACEUTICAL CO.

15.18.1 COMPANY SNAPSHOT

15.18.2 REVENUE ANALYSIS

15.18.3 PRODUCT PORTFOLIO

15.18.4 RECENT DEVELOPMENT

15.19 STAAR SURGICAL

15.19.1 COMPANY SNAPSHOT

15.19.2 REVENUE ANALYSIS

15.19.3 PRODUCT PORTFOLIO

15.19.4 RECENT DEVELOPMENT

15.2 TOPCON CORPORATION

15.20.1 COMPANY SNAPSHOT

15.20.2 REVENUE ANALYSIS

15.20.3 PRODUCT PORTFOLIO

15.20.4 RECENT DEVELOPMENT

15.21 ZIEMER OPHTHALMIC SYSTEMS AG

15.21.1 COMPANY SNAPSHOT

15.21.2 PRODUCT PORTFOLIO

15.21.3 RECENT DEVELOPMENT

16 QUESTIONNAIRE

17 RELATED REPORTS

List of Table

TABLE 1 NORTH AMERICA OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 2 NORTH AMERICA DEVICE IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 3 NORTH AMERICA SURGICAL DEVICE IN OPHTHALMOLOGY MARKET, BY PRODUCT, 2018-2032 (USD MILLION)

TABLE 4 NORTH AMERICA OPHTHALMIC VISCOELASTIC DEVICES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 5 NORTH AMERICA VITREORETINAL SURGICAL DEVICES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 6 NORTH AMERICA REFRACTIVE SURGICAL DEVICES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2021-2032 (USD MILLION)

TABLE 7 NORTH AMERICA GLAUCOMA SURGICAL DEVICES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 8 NORTH AMERICA DIAGNOSTIC DEVICE IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 9 NORTH AMERICA OPHTHALMIC ULTRASOUND IMAGING SYSTEMS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 10 NORTH AMERICA OPHTHALMIC SURGICAL ACCESSORIES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 11 NORTH AMERICA DRUGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2021-2032 (USD MILLION)

TABLE 12 NORTH AMERICA ANTI-VEGF DRUGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2021-2032 (USD MILLION)

TABLE 13 NORTH AMERICA ANTI-GLAUCOMA DRUGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 14 NORTH AMERICA PROSTAGLANDIN ANALOGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 15 NORTH AMERICA BETA ADRENERGIC ANTAGONISTS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 16 NORTH AMERICA ALPHA ADRENERGIC AGONISTS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2021-2032 (USD MILLION)

TABLE 17 NORTH AMERICA MIOTICS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2021-2032 (USD MILLION)

TABLE 18 NORTH AMERICA ANTI INFLAMMATION DRUGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2021-2032 (USD MILLION)

TABLE 19 NORTH AMERICA DRUGS IN OPHTHALMOLOGY MARKET, BY DRUG TYPE, 2018-2032 (USD MILLION)

TABLE 20 NORTH AMERICA DRUGS IN OPHTHALMOLOGY MARKET, BY PRESCRIPTION MODE, 2018-2032 (USD MILLION)

TABLE 21 NORTH AMERICA DRUGS IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 22 NORTH AMERICA TOPICAL IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 23 NORTH AMERICA LOCAL OCULAR IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 24 NORTH AMERICA INJECTABLES IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 25 NORTH AMERICA ORAL IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 26 NORTH AMERICA OTHERS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 27 NORTH AMERICA VISION CARE PRODUCTS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 28 NORTH AMERICA CONTACT LENSES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 29 NORTH AMERICA OPHTHALMOLOGY MARKET, BY DISEASES, 2018-2032 (USD MILLION)

TABLE 30 NORTH AMERICA CATARACT IN OPHTHALMOLOGY MARKET, BY REGION, 2018-2032 (USD MILLION)

TABLE 31 NORTH AMERICA REFRACTIVE DISORDERS IN OPHTHALMOLOGY MARKET, BY REGION, 2018-2032 (USD MILLION)

TABLE 32 NORTH AMERICA GLAUCOMA IN OPHTHALMOLOGY MARKET, BY REGION, 2018-2032 (USD MILLION)

TABLE 33 NORTH AMERICA AGE-RELATED MACULAR DEGENERATION IN OPHTHALMOLOGY MARKET, BY REGION, 2018-2032 (USD MILLION)

TABLE 34 NORTH AMERICA INFLAMMATORY DISEASES IN OPHTHALMOLOGY MARKET, BY REGION, 2018-2032 (USD MILLION)

TABLE 35 NORTH AMERICA OTHERS IN OPHTHALMOLOGY MARKET, BY REGION, 2018-2032 (USD MILLION)

TABLE 36 NORTH AMERICA OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 37 NORTH AMERICA REFRACTION IN OPHTHALMOLOGY MARKET, BY REGION, 2018-2032 (USD MILLION)

TABLE 38 NORTH AMERICA REFRACTION IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 39 NORTH AMERICA VISUAL ACUITY TEST IN OPHTHALMOLOGY MARKET, BY REGION, 2018-2032 (USD MILLION)

TABLE 40 NORTH AMERICA VISUAL ACUITY TEST IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 41 NORTH AMERICA INTRAOCULAR PRESSURE IN OPHTHALMOLOGY MARKET, BY REGION, 2018-2032 (USD MILLION)

TABLE 42 NORTH AMERICA INTRAOCULAR PRESSURE IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 43 NORTH AMERICA ANTERIOR SEGMENT AND PUPILLARY EXAMINATION IN OPHTHALMOLOGY MARKET, BY REGION, 2018-2032 (USD MILLION)

TABLE 44 NORTH AMERICA ANTERIOR SEGMENT AND PUPILLARY EXAMINATION IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 45 NORTH AMERICA VISUAL FIELDS TEST IN OPHTHALMOLOGY MARKET, BY REGION, 2018-2032 (USD MILLION)

TABLE 46 NORTH AMERICA VISUAL FIELDS TEST IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 47 NORTH AMERICA COLOR VISION TEST IN OPHTHALMOLOGY MARKET, BY REGION, 2018-2032 (USD MILLION)

TABLE 48 NORTH AMERICA OTHERS IN OPHTHALMOLOGY MARKET, BY REGION, 2018-2032 (USD MILLION)

TABLE 49 NORTH AMERICA OPHTHALMOLOGY MARKET, BY END USER, 2018-2032 (USD MILLION)

TABLE 50 NORTH AMERICA CLINICS IN OPHTHALMOLOGY MARKET, BY REGION, 2018-2032 (USD MILLION)

TABLE 51 NORTH AMERICA HOSPITALS IN OPHTHALMOLOGY MARKET, BY REGION, 2018-2032 (USD MILLION)

TABLE 52 NORTH AMERICA HOME HEALTHCARE IN OPHTHALMOLOGY MARKET, BY REGION, 2018-2032 (USD MILLION)

TABLE 53 NORTH AMERICA OTHERS IN OPHTHALMOLOGY MARKET, BY REGION, 2018-2032 (USD MILLION)

TABLE 54 NORTH AMERICA OPHTHALMOLOGY MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD MILLION)

TABLE 55 NORTH AMERICA RETAIL SALES IN OPHTHALMOLOGY MARKET, BY REGION, 2018-2032 (USD MILLION)

TABLE 56 NORTH AMERICA RETAIL SALES IN OPHTHALMOLOGY MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD MILLION)

TABLE 57 NORTH AMERICA DIRECT TENDER IN OPHTHALMOLOGY MARKET, BY REGION, 2018-2032 (USD MILLION)

TABLE 58 NORTH AMERICA OTHERS IN OPHTHALMOLOGY MARKET, BY REGION, 2018-2032 (USD MILLION)

TABLE 59 NORTH AMERICA OPHTHALMOLOGY MARKET, BY COUNTRY, 2018-2032 (USD MILLION)

TABLE 60 NORTH AMERICA OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 61 NORTH AMERICA DEVICE IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 62 NORTH AMERICA SURGICAL DEVICE IN OPHTHALMOLOGY MARKET, BY PRODUCT, 2018-2032 (USD MILLION)

TABLE 63 NORTH AMERICA OPHTHALMIC VISCOELASTIC DEVICES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 64 NORTH AMERICA VITREORETINAL SURGICAL DEVICES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 65 NORTH AMERICA REFRACTIVE SURGICAL DEVICES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 66 NORTH AMERICA GLAUCOMA SURGICAL DEVICES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 67 NORTH AMERICA DIAGNOSTIC DEVICE IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 68 NORTH AMERICA OPHTHALMIC ULTRASOUND IMAGING SYSTEMS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 69 NORTH AMERICA OPHTHALMIC SURGICAL ACCESSORIES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 70 NORTH AMERICA DRUGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 71 NORTH AMERICA ANTI-VEGF DRUGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 72 NORTH AMERICA ANTI-GLAUCOMA DRUGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 73 NORTH AMERICA PROSTAGLANDIN ANALOGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 74 NORTH AMERICA BETA ADRENERGIC ANTAGONISTS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 75 NORTH AMERICA ALPHA ADRENERGIC AGONISTS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 76 NORTH AMERICA MIOTICS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 77 NORTH AMERICA ANTI-INFLAMMATORY DRUGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 78 NORTH AMERICA OTHERS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 79 NORTH AMERICA VISION CARE PRODUCTS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 80 NORTH AMERICA CONTACT LENSES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 81 NORTH AMERICA OPHTHALMOLOGY MARKET, BY DISEASES, 2018-2032 (USD MILLION)

TABLE 82 NORTH AMERICA DRUGS IN OPHTHALMOLOGY MARKET, BY DRUG TYPE, 2018-2032 (USD MILLION)

TABLE 83 NORTH AMERICA DRUGS IN OPHTHALMOLOGY MARKET, BY PRESCRIPTION MODE, 2018-2032 (USD MILLION)

TABLE 84 NORTH AMERICA DRUGS IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 85 NORTH AMERICA TOPICAL IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 86 NORTH AMERICA LOCAL OCULAR IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 87 NORTH AMERICA INJECTABLES IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 88 NORTH AMERICA ORAL IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 89 NORTH AMERICA OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 90 NORTH AMERICA REFRACTION IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 91 NORTH AMERICA VISUAL ACUITY TEST IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 92 NORTH AMERICA INTRAOCULAR PRESSURE IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 93 NORTH AMERICA ANTERIOR SEGMENT AND PUPILLARY EXAMINATION IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 94 NORTH AMERICA VISUAL FIELDS TEST IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 95 NORTH AMERICA OPHTHALMOLOGY MARKET, BY END USER, 2018-2032 (USD MILLION)

TABLE 96 NORTH AMERICA OPHTHALMOLOGY MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD MILLION)

TABLE 97 NORTH AMERICA RETAIL SALES IN OPHTHALMOLOGY MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD MILLION)

TABLE 98 U.S. OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 99 U.S. DEVICE IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 100 U.S. SURGICAL DEVICE IN OPHTHALMOLOGY MARKET, BY PRODUCT, 2018-2032 (USD MILLION)

TABLE 101 U.S. OPHTHALMIC VISCOELASTIC DEVICES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 102 U.S. VITREORETINAL SURGICAL DEVICES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 103 U.S. REFRACTIVE SURGICAL DEVICES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 104 U.S. GLAUCOMA SURGICAL DEVICES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 105 U.S. DIAGNOSTIC DEVICE IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 106 U.S. OPHTHALMIC ULTRASOUND IMAGING SYSTEMS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 107 U.S. OPHTHALMIC SURGICAL ACCESSORIES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 108 U.S. DRUGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 109 U.S. ANTI-VEGF DRUGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 110 U.S. ANTI-GLAUCOMA DRUGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 111 U.S. PROSTAGLANDIN ANALOGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 112 U.S. BETA ADRENERGIC ANTAGONISTS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 113 U.S. ALPHA ADRENERGIC AGONISTS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 114 U.S. MIOTICS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 115 U.S. ANTI-INFLAMMATORY DRUGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 116 U.S. OTHERS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 117 U.S. VISION CARE PRODUCTS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 118 U.S. CONTACT LENSES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 119 U.S. OPHTHALMOLOGY MARKET, BY DISEASES, 2018-2032 (USD MILLION)

TABLE 120 U.S. DRUGS IN OPHTHALMOLOGY MARKET, BY DRUG TYPE, 2018-2032 (USD MILLION)

TABLE 121 U.S. DRUGS IN OPHTHALMOLOGY MARKET, BY PRESCRIPTION MODE, 2018-2032 (USD MILLION)

TABLE 122 U.S. DRUGS IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 123 U.S. TOPICAL IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 124 U.S. LOCAL OCULAR IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 125 U.S. INJECTABLES IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 126 U.S. ORAL IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 127 U.S. OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 128 U.S. REFRACTION IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 129 U.S. VISUAL ACUITY TEST IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 130 U.S. INTRAOCULAR PRESSURE IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 131 U.S. ANTERIOR SEGMENT AND PUPILLARY EXAMINATION IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 132 U.S. VISUAL FIELDS TEST IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 133 U.S. OPHTHALMOLOGY MARKET, BY END USER, 2018-2032 (USD MILLION)

TABLE 134 U.S. OPHTHALMOLOGY MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD MILLION)

TABLE 135 U.S. RETAIL SALES IN OPHTHALMOLOGY MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD MILLION)

TABLE 136 CANADA OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 137 CANADA DEVICE IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 138 CANADA SURGICAL DEVICE IN OPHTHALMOLOGY MARKET, BY PRODUCT, 2018-2032 (USD MILLION)

TABLE 139 CANADA OPHTHALMIC VISCOELASTIC DEVICES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 140 CANADA VITREORETINAL SURGICAL DEVICES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 141 CANADA REFRACTIVE SURGICAL DEVICES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 142 CANADA GLAUCOMA SURGICAL DEVICES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 143 CANADA DIAGNOSTIC DEVICE IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 144 CANADA OPHTHALMIC ULTRASOUND IMAGING SYSTEMS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 145 CANADA OPHTHALMIC SURGICAL ACCESSORIES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 146 CANADA DRUGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 147 CANADA ANTI-VEGF DRUGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 148 CANADA ANTI-GLAUCOMA DRUGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 149 CANADA PROSTAGLANDIN ANALOGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 150 CANADA BETA ADRENERGIC ANTAGONISTS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 151 CANADA ALPHA ADRENERGIC AGONISTS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 152 CANADA MIOTICS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 153 CANADA ANTI-INFLAMMATORY DRUGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 154 CANADA OTHERS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 155 CANADA VISION CARE PRODUCTS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 156 CANADA CONTACT LENSES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 157 CANADA OPHTHALMOLOGY MARKET, BY DISEASES, 2018-2032 (USD MILLION)

TABLE 158 CANADA DRUGS IN OPHTHALMOLOGY MARKET, BY DRUG TYPE, 2018-2032 (USD MILLION)

TABLE 159 CANADA DRUGS IN OPHTHALMOLOGY MARKET, BY PRESCRIPTION MODE, 2018-2032 (USD MILLION)

TABLE 160 CANADA DRUGS IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 161 CANADA TOPICAL IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 162 CANADA LOCAL OCULAR IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 163 CANADA INJECTABLES IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 164 CANADA ORAL IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 165 CANADA OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 166 CANADA REFRACTION IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 167 CANADA VISUAL ACUITY TEST IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 168 CANADA INTRAOCULAR PRESSURE IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 169 CANADA ANTERIOR SEGMENT AND PUPILLARY EXAMINATION IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 170 CANADA VISUAL FIELDS TEST IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 171 CANADA OPHTHALMOLOGY MARKET, BY END USER, 2018-2032 (USD MILLION)

TABLE 172 CANADA OPHTHALMOLOGY MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD MILLION)

TABLE 173 CANADA RETAIL SALES IN OPHTHALMOLOGY MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD MILLION)

TABLE 174 MEXICO OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 175 MEXICO DEVICE IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 176 MEXICO SURGICAL DEVICE IN OPHTHALMOLOGY MARKET, BY PRODUCT, 2018-2032 (USD MILLION)

TABLE 177 MEXICO OPHTHALMIC VISCOELASTIC DEVICES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 178 MEXICO VITREORETINAL SURGICAL DEVICES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 179 MEXICO REFRACTIVE SURGICAL DEVICES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 180 MEXICO GLAUCOMA SURGICAL DEVICES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 181 MEXICO DIAGNOSTIC DEVICE IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 182 MEXICO OPHTHALMIC ULTRASOUND IMAGING SYSTEMS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 183 MEXICO OPHTHALMIC SURGICAL ACCESSORIES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 184 MEXICO DRUGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 185 MEXICO ANTI-VEGF DRUGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 186 MEXICO ANTI-GLAUCOMA DRUGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 187 MEXICO PROSTAGLANDIN ANALOGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 188 MEXICO BETA ADRENERGIC ANTAGONISTS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 189 MEXICO ALPHA ADRENERGIC AGONISTS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 190 MEXICO MIOTICS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 191 MEXICO ANTI-INFLAMMATORY DRUGS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 192 MEXICO OTHERS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 193 MEXICO VISION CARE PRODUCTS IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 194 MEXICO CONTACT LENSES IN OPHTHALMOLOGY MARKET, BY PRODUCTS, 2018-2032 (USD MILLION)

TABLE 195 MEXICO OPHTHALMOLOGY MARKET, BY DISEASES, 2018-2032 (USD MILLION)

TABLE 196 MEXICO DRUGS IN OPHTHALMOLOGY MARKET, BY DRUG TYPE, 2018-2032 (USD MILLION)

TABLE 197 MEXICO DRUGS IN OPHTHALMOLOGY MARKET, BY PRESCRIPTION MODE, 2018-2032 (USD MILLION)

TABLE 198 MEXICO DRUGS IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 199 MEXICO TOPICAL IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 200 MEXICO LOCAL OCULAR IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 201 MEXICO INJECTABLES IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 202 MEXICO ORAL IN OPHTHALMOLOGY MARKET, BY ROUTE OF ADMINISTRATION, 2018-2032 (USD MILLION)

TABLE 203 MEXICO OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 204 MEXICO REFRACTION IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 205 MEXICO VISUAL ACUITY TEST IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 206 MEXICO INTRAOCULAR PRESSURE IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 207 MEXICO ANTERIOR SEGMENT AND PUPILLARY EXAMINATION IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 208 MEXICO VISUAL FIELDS TEST IN OPHTHALMOLOGY MARKET, BY COMPREHENSIVE EYE EXAMINATION, 2018-2032 (USD MILLION)

TABLE 209 MEXICO OPHTHALMOLOGY MARKET, BY END USER, 2018-2032 (USD MILLION)

TABLE 210 MEXICO OPHTHALMOLOGY MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD MILLION)

TABLE 211 MEXICO RETAIL SALES IN OPHTHALMOLOGY MARKET, BY DISTRIBUTION CHANNEL, 2018-2032 (USD MILLION)

List of Figure

FIGURE 1 NORTH AMERICA OPHTHALMOLOGY MARKET: SEGMENTATION

FIGURE 2 NORTH AMERICA OPHTHALMOLOGY MARKET: DATA TRIANGULATION

FIGURE 3 NORTH AMERICA OPHTHALMOLOGY MARKET: DROC ANALYSIS

FIGURE 4 NORTH AMERICA OPHTHALMOLOGY MARKET: NORTH AMERICA VS REGIONAL MARKET ANALYSIS

FIGURE 5 NORTH AMERICA OPHTHALMOLOGY MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 NORTH AMERICA OPHTHALMOLOGY MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 NORTH AMERICA OPHTHALMOLOGY MARKET: MARKET APPLICATION COVERAGE GRID

FIGURE 8 NORTH AMERICA OPHTHALMOLOGY MARKET: DBMR MARKET POSITION GRID

FIGURE 9 NORTH AMERICA OPHTHALMOLOGY MARKET: VENDOR SHARE ANALYSIS

FIGURE 10 NORTH AMERICA OPHTHALMOLOGY MARKET: SEGMENTATION

FIGURE 11 THREE SEGMENTS COMPRISE THE NORTH AMERICA OPHTHALMOLOGY MARKET, BY PRODUCTS

FIGURE 12 EXECUTIVE SUMMARY

FIGURE 13 STRATEGIC DECISIONS

FIGURE 14 RISING INCIDENCE OF EYE DISORDERS IS DRIVING THE GROWTH OF THE NORTH AMERICA OPHTHALMOLOGY MARKET FROM 2025 TO 2032

FIGURE 15 THE PRODUCTS SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE NORTH AMERICA OPHTHALMOLOGY MARKET IN 2025 AND 2032

FIGURE 16 DROC ANALYSIS

FIGURE 17 NORTH AMERICA OPHTHALMOLOGY MARKET: BY PRODUCTS, 2024

FIGURE 18 NORTH AMERICA OPHTHALMOLOGY MARKET: BY PRODUCTS, 2025-2032 (USD MILLION)

FIGURE 19 NORTH AMERICA OPHTHALMOLOGY MARKET: BY PRODUCTS, CAGR (2025-2032)

FIGURE 20 NORTH AMERICA OPHTHALMOLOGY MARKET: BY PRODUCTS, LIFELINE CURVE

FIGURE 21 NORTH AMERICA OPHTHALMOLOGY MARKET: BY DISEASES, 2024

FIGURE 22 NORTH AMERICA OPHTHALMOLOGY MARKET: BY DISEASES, 2025-2032 (USD MILLION)

FIGURE 23 NORTH AMERICA OPHTHALMOLOGY MARKET: BY DISEASES, CAGR (2025-2032)

FIGURE 24 NORTH AMERICA OPHTHALMOLOGY MARKET: BY DISEASES, LIFELINE CURVE

FIGURE 25 NORTH AMERICA OPHTHALMOLOGY MARKET: BY COMPREHENSIVE EYE EXAMINATION, 2024

FIGURE 26 NORTH AMERICA OPHTHALMOLOGY MARKET: BY COMPREHENSIVE EYE EXAMINATION, 2025-2032 (USD MILLION)

FIGURE 27 NORTH AMERICA OPHTHALMOLOGY MARKET: BY COMPREHENSIVE EYE EXAMINATION, CAGR (2025-2032)

FIGURE 28 NORTH AMERICA OPHTHALMOLOGY MARKET: BY COMPREHENSIVE EYE EXAMINATION, LIFELINE CURVE

FIGURE 29 NORTH AMERICA OPHTHALMOLOGY MARKET: BY END USER, 2024

FIGURE 30 NORTH AMERICA OPHTHALMOLOGY MARKET: BY END USER, 2025-2032 (USD MILLION)

FIGURE 31 NORTH AMERICA OPHTHALMOLOGY MARKET: BY END USER, CAGR (2025-2032)

FIGURE 32 NORTH AMERICA OPHTHALMOLOGY MARKET: BY END USER, LIFELINE CURVE

FIGURE 33 NORTH AMERICA OPHTHALMOLOGY MARKET: BY DISTRIBUTION CHANNEL ,2024

FIGURE 34 NORTH AMERICA OPHTHALMOLOGY MARKET: BY DISTRIBUTION CHANNEL, 2025-2032 (USD MILLION)

FIGURE 35 NORTH AMERICA OPHTHALMOLOGY MARKET: BY DISTRIBUTION CHANNEL, CAGR (2025-2032)

FIGURE 36 NORTH AMERICA OPHTHALMOLOGY MARKET: BY DISTRIBUTION CHANNEL, LIFELINE CURVE

FIGURE 37 NORTH AMERICA OPHTHALMOLOGY MARKET SNAPSHOT

FIGURE 38 NORTH AMERICA OPHTHALMOLOGY MARKET: COMPANY SHARE 2024 (%)

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.