North America Orthopedic Surgical Robots Market

Market Size in USD Billion

USD

5.18 Billion

USD

33.53 Billion

2025

2033

USD

5.18 Billion

USD

33.53 Billion

2025

2033

| 2026 - 2033 | |

| USD 5.18 Billion | |

| USD 33.53 Billion | |

| % | |

|

What is the North America Orthopedic Surgical Robots Market Size and Growth Rate?

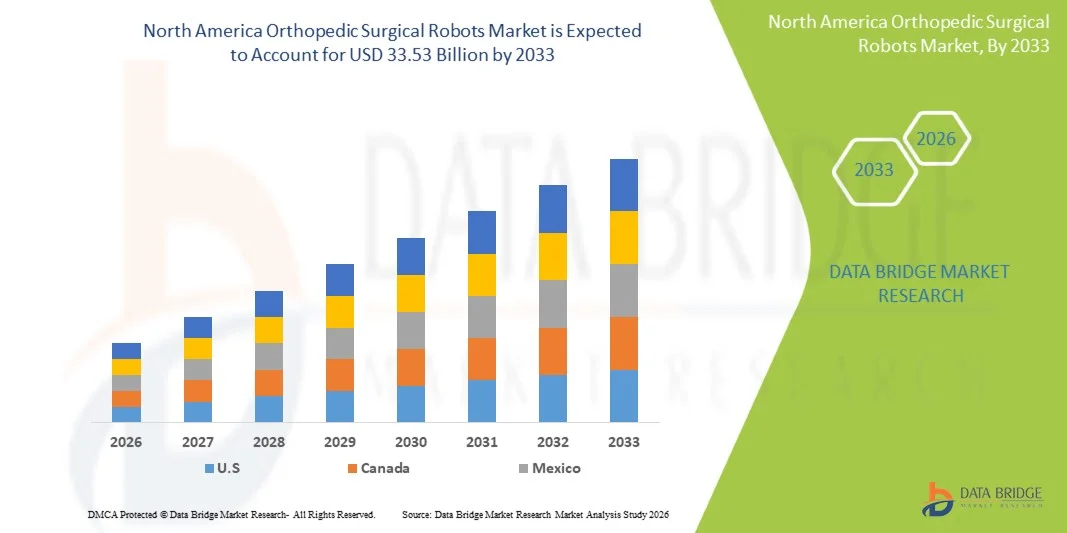

- As per Data Bridge Market Research Analysis the North America Orthopedic Surgical Robots Market size was valued at USD 5.18 billion in 2025 and is expected to reach USD 33.53 billion by 2033, at a CAGR of 26.30% during the forecast period

- The market growth is largely fueled by the increasing adoption of robotic-assisted surgery systems, continuous technological advancements in precision imaging and navigation platforms, and growing digitalization across hospitals and surgical centers

- Furthermore, rising demand for minimally invasive procedures, enhanced surgical accuracy, reduced recovery times, and integrated operating room solutions is establishing Orthopedic Surgical Robots as a modern standard in advanced orthopedic care. These converging factors are accelerating the uptake of Orthopedic Surgical Robots solutions, thereby significantly boosting the industry's growth

Market Size & Forecast

- Global Market Value (2025): USD 5.18 billion in 2025

- Expected Market Value (2033): USD 33.53 billion by 2033

- Forecast CAGR (2026–2033): 26.30%

North America Orthopedic Surgical Robots Market Analysis

- Orthopedic Surgical Robots, offering robotic-assisted systems for joint replacement, spine surgery, trauma fixation, and precision bone alignment procedures, are increasingly vital components of modern orthopedic care in hospitals and specialty surgical centers due to their enhanced accuracy, reduced invasiveness, faster recovery times, and integration with advanced imaging and navigation technologies

- The escalating demand for Orthopedic Surgical Robots is primarily fueled by the growing adoption of minimally invasive surgery, rising incidence of musculoskeletal disorders, increasing aging population, and a rising preference for precision-guided surgical outcomes

- S. dominated the North America Orthopedic Surgical Robots Market in North America with the largest revenue share of approximately 41.7% in 2025, characterized by advanced healthcare infrastructure, high healthcare expenditure, strong presence of key medical technology players, and increasing robotic-assisted orthopedic procedures across major hospitals and surgical centers

- Canada is expected to be the fastest-growing market in the Orthopedic Surgical Robots sector during the forecast period, projected to register a CAGR of approximately 10.6%, due to increasing healthcare investments, rising demand for joint replacement surgeries, expanding adoption of robotic technologies, and strong focus on technologically advanced surgical care

- The robotic system segment dominated the largest market revenue share of 57.6% in 2025, driven by the high capital value of robotic platforms and increasing adoption of precision-assisted orthopedic surgeries

Report Scope and North America Orthopedic Surgical Robots Market Segmentation

|

Attributes |

Orthopedic Surgical Robots Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

What is the Key Trend in the North America Orthopedic Surgical Robots Market?

“Increasing Adoption of Robotic-Assisted Precision Surgery and AI-Enabled Navigation”

- A significant and rapidly growing trend in the North America Orthopedic Surgical Robots Market is the increasing adoption of robotic-assisted precision surgery systems integrated with artificial intelligence, real-time imaging, and navigation technologies. These innovations are transforming orthopedic procedures by improving implant placement accuracy, surgical consistency, and patient outcomes

- For instance, robotic platforms such as Stryker’s Mako system and Zimmer Biomet’s ROSA Knee system are being increasingly adopted across European hospitals for knee and hip replacement procedures. These systems assist surgeons in pre-operative planning and intraoperative guidance, helping optimize alignment and reduce human error

- Advanced robotic systems enable surgeons to create personalized surgical plans based on patient-specific anatomy using CT scans or 3D imaging. For example, AI-supported software can analyze bone structure and recommend optimal implant positioning, leading to better joint function and faster recovery after surgery

- The integration of orthopedic robots with digital operating rooms and hospital information systems supports seamless workflow management. Surgeons can access imaging data, surgical plans, and real-time analytics through a unified platform, improving procedural efficiency and reducing operating room time

- This trend toward minimally invasive and technology-assisted orthopedic care is reshaping expectations for joint replacement and spine surgeries across Europe. Consequently, companies such as Smith+Nephew, Medtronic, and Globus Medical are expanding robotic portfolios and launching advanced navigation-enabled systems

- Demand for orthopedic surgical robots is rising across both public and private healthcare institutions as providers increasingly prioritize precision surgery, shorter hospital stays, and long-term cost savings through reduced revision surgeries

North America Orthopedic Surgical Robots Market Dynamics

Driver

“Growing Need Due to Rising Orthopedic Disorders and Demand for Minimally Invasive Procedures”

- The increasing prevalence of musculoskeletal disorders such as osteoarthritis, osteoporosis, sports injuries, and degenerative joint diseases is a major driver for the North America Orthopedic Surgical Robots Market. Aging populations across countries such as Germany, France, Italy, and the UK are significantly increasing the need for joint replacement and spine procedures

- For instance, in March 2025, several European hospitals expanded robotic knee and hip replacement programs to address rising waiting lists and improve surgical efficiency. Such strategic investments by healthcare providers are expected to support market growth during the forecast period

- As patients seek safer and faster recovery options, robotic-assisted surgery offers advantages such as smaller incisions, reduced blood loss, lower post-operative pain, and improved implant accuracy compared with conventional surgery

- Furthermore, growing awareness among surgeons regarding the clinical benefits of robotic systems is increasing adoption in hospitals and specialty orthopedic centers. Training programs and surgeon certification initiatives are further accelerating acceptance

- The rising demand for outpatient orthopedic procedures and same-day discharge surgeries is also driving robotic system installations, as these technologies help standardize procedures and shorten recovery timelines. Increasing healthcare spending across North America further supports market expansion

Restraint/Challenge

“High Capital Investment and Limited Accessibility in Smaller Healthcare Facilities”

- The high acquisition and maintenance cost of orthopedic surgical robots remains a significant challenge for wider market penetration. Robotic systems often require substantial upfront investment, software licensing fees, disposable instruments, and staff training, making adoption difficult for smaller hospitals and regional clinics

- For instance, many mid-sized healthcare centers in Eastern and Southern North America continue to rely on conventional orthopedic techniques due to budget constraints and limited reimbursement support for robotic-assisted procedures

- In addition to cost barriers, hospitals may face workflow disruptions during installation and surgeon learning curves during the early adoption phase. Training requirements and integration with existing operating room infrastructure can delay implementation

- Reimbursement uncertainty for robotic procedures in some European countries can also discourage investment, particularly where healthcare systems are highly cost-regulated. Providers may hesitate if robotic surgeries are not adequately compensated

- Concerns regarding system downtime, software updates, and dependency on specialized technical support can further slow adoption in certain regions

- Overcoming these challenges through lower-cost robotic platforms, improved reimbursement frameworks, leasing models, and broader surgeon training programs will be vital for sustained market growth in Europe

North America Orthopedic Surgical Robots Market Scope

The market is segmented on the basis of product type, end user, and distribution channel.

- By Product Type

On the basis of product type, the North America Orthopedic Surgical Robots Market is segmented into robotic system, robotic accessories, and software and services. The robotic system segment dominated the largest market revenue share of 57.6% in 2025, driven by the high capital value of robotic platforms and increasing adoption of precision-assisted orthopedic surgeries. Hospitals are investing in robotic systems for knee, hip, and spine procedures to improve surgical accuracy and patient outcomes. These systems help reduce revision surgeries and shorten hospital stays. Growing demand for minimally invasive orthopedic interventions supports adoption. Advanced navigation, imaging, and AI-assisted planning tools further strengthen demand. Surgeons increasingly prefer robotic systems for reproducible implant placement. Expansion of specialty orthopedic centers also contributes to segment growth. Developed markets continue to replace conventional systems with robotic platforms. Strategic partnerships between hospitals and manufacturers support installations. Rising aging populations and joint replacement volumes further sustain dominance. Continuous innovation in next-generation robotic platforms accelerates market penetration globally.

The software and services segment is projected to witness the fastest CAGR of 18.4% from 2026 to 2033, owing to rising need for analytics, maintenance, training, workflow optimization, and cloud-based planning solutions. Robotic platforms increasingly rely on software upgrades for enhanced functionality. Hospitals are demanding predictive maintenance and remote technical support. AI-powered surgical planning modules are gaining traction rapidly. Growing installed base of robots creates recurring service revenue opportunities. Subscription-based software models improve affordability for healthcare providers. Training services are increasingly required as surgeon adoption rises. Vendors are focusing on digital ecosystems integrating imaging and robotics. Expansion of data-driven post-operative analytics supports demand. Emerging markets are adopting software-first robotic solutions. Continuous innovation in navigation software further accelerates this segment’s growth.

- By End User

On the basis of end user, the North America Orthopedic Surgical Robots Market is segmented into hospital and ambulatory surgery centers (ASCs). The hospital segment accounted for the largest market revenue share of 71.3% in 2025, driven by higher purchasing capacity, large surgical volumes, and availability of advanced infrastructure. Hospitals perform the majority of complex orthopedic procedures including total joint replacements and spine surgeries. They are early adopters of robotic systems due to access to capital budgets. Presence of skilled surgeons and multidisciplinary teams supports utilization. Hospitals also benefit from integrated imaging and navigation systems. Rising patient preference for technologically advanced surgical care drives demand. Academic hospitals are increasingly using robotics for training and research. Large healthcare networks continue expanding robotic surgery programs. Favorable reimbursement in developed markets strengthens hospital leadership. Increasing trauma and degenerative bone disease cases support continued growth. Investments in smart operating rooms further reinforce segment dominance.

The ambulatory surgery centers (ASCs) segment is expected to witness the fastest CAGR of 16.9% from 2026 to 2033, fueled by growing shift toward outpatient orthopedic procedures. ASCs offer lower treatment costs and shorter patient stays. Technological miniaturization of robotic systems makes deployment easier in compact facilities. Rising demand for same-day knee and hip surgeries supports adoption. Patients increasingly prefer convenient outpatient settings. Surgeons are partnering with ASCs for efficient scheduling and lower overhead costs. Improved anesthesia and recovery protocols enable more procedures in ASCs. Vendors are launching cost-effective robotic solutions tailored for these centers. Expansion of private healthcare infrastructure further boosts growth. Increasing insurer support for outpatient care accelerates adoption globally.

- By Distribution Channel

On the basis of distribution channel, the North America Orthopedic Surgical Robots Market is segmented into direct tenders and third party distributors. The direct tenders segment held the largest market revenue share of 64.8% in 2025, driven by the complex and high-value nature of robotic system procurement. Hospitals prefer direct purchasing from manufacturers for installation, customization, and long-term service agreements. Direct channels ensure better training and technical support. Manufacturers can offer bundled packages including accessories and maintenance contracts. Large hospital groups negotiate multi-unit tenders directly with suppliers. Government institutions also rely on formal tender processes for acquisitions. Direct procurement improves transparency and lifecycle management. Strong manufacturer-customer relationships support repeat business. Customized financing models further strengthen this segment. Continuous upgrades and service renewals contribute to revenue leadership.

The third party distributors segment is anticipated to witness the fastest CAGR of 14.7% from 2026 to 2033, driven by expanding penetration in emerging and mid-sized markets. Distributors help manufacturers reach regional hospitals and smaller surgical centers efficiently. They provide localized sales support and market knowledge. Growing demand in Asia-Pacific and Latin America supports channel expansion. Smaller facilities prefer distributor-led procurement for faster access and flexible pricing. Distributors also assist with installation coordination and consumables supply. Increasing partnerships between OEMs and regional dealers boost reach. Expansion of aftermarket service networks supports adoption. Rising awareness of robotic orthopedics in untapped markets accelerates growth.

North America Orthopedic Surgical Robots Market Regional Analysis

- The North America Orthopedic Surgical Robots Market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising demand for minimally invasive orthopedic procedures, increasing prevalence of musculoskeletal disorders, and growing adoption of robotic-assisted technologies across hospitals and specialty surgical centers

- The region benefits from advanced healthcare infrastructure, favorable reimbursement frameworks in several countries, and increasing focus on improving surgical precision, patient outcomes, and recovery times

- In addition, rising volumes of knee, hip, and spine procedures are supporting continued market expansion across North America

U.S. North America Orthopedic Surgical Robots Market Insight

The U.S. North America Orthopedic Surgical Robots Market dominated the North America Orthopedic Surgical Robots Market in North America with the largest revenue share of approximately 41.7% in 2025, characterized by advanced healthcare infrastructure, high healthcare expenditure, strong presence of key medical technology players, and increasing robotic-assisted orthopedic procedures across major hospitals and surgical centers. Growing demand for precision-based joint replacement surgeries, along with rising investments in next-generation operating rooms, continues to support market growth. Furthermore, increasing awareness among surgeons and patients regarding the benefits of robotic-assisted procedures is accelerating adoption across the country.

Canada North America Orthopedic Surgical Robots Market Insight

Canada North America Orthopedic Surgical Robots Market is expected to be the fastest-growing market in the Orthopedic Surgical Robots sector during the forecast period, projected to register a CAGR of approximately 10.6%, due to increasing healthcare investments, rising demand for joint replacement surgeries, expanding adoption of robotic technologies, and strong focus on technologically advanced surgical care. The country’s robust hospital network, emphasis on innovation, and growing geriatric population are further driving demand for robotic orthopedic systems. Additionally, increasing training programs for surgeons and continued investments in smart operating theaters are expected to enhance future market growth.

Which are the Top Companies in North America Orthopedic Surgical Robots Market?

The Orthopedic Surgical Robots industry is primarily led by well-established companies, including:

- Stryker Corporation (U.S.)

- Zimmer Biomet Holdings, Inc. (U.S.)

- Smith+Nephew plc (U.K.)

- Johnson & Johnson MedTech (U.S.)

- Medtronic plc (Ireland)

- Globus Medical, Inc. (U.S.)

- Intuitive Surgical, Inc. (U.S.)

- THINK Surgical, Inc. (U.S.)

- Corin Group (U.K.)

- CUREXO, Inc. (South Korea)

- Renishaw plc (U.K.)

- Brainlab AG (Germany)

- Exactech, Inc. (U.S.)

- MicroPort Scientific Corporation (China)

- OrthAlign, Inc. (U.S.)

- Omnicare Medical Technology Co., Ltd. (China)

- Asensus Surgical, Inc. (U.S.)

- ZBEdge / Zimmer Biomet Robotics (U.S.)

- eCential Robotics (France)

- Meril Life Sciences Pvt. Ltd. (India)

Latest Developments in North America Orthopedic Surgical Robots Market

- In June 2021, Zimmer Biomet Holdings, Inc. announced the U.S. commercial launch of ROSA Hip, expanding its ROSA Robotics platform beyond knee arthroplasty into total hip replacement procedures. The launch strengthened Zimmer Biomet’s position in robot-assisted joint reconstruction and broadened surgeon adoption of robotic orthopedic systems

- In September 2022, Point Robotics MedTech Inc. received U.S. FDA clearance for its orthopedic surgical robot, becoming one of the first emerging robotics companies to secure approval in the orthopedic segment. This milestone highlighted growing competition and innovation beyond incumbent players in robot-assisted orthopedic surgery

- In November 2022, Johnson & Johnson MedTech expanded the commercial rollout of its VELYS Robotic-Assisted Solution for knee replacement surgery, supporting surgeon precision, workflow efficiency, and intraoperative data-driven alignment in total knee arthroplasty. This strengthened J&J’s presence in the fast-growing orthopedic robotics market

- In May 2023, Smith+Nephew reported continued global expansion of its CORI Surgical System, a handheld robotic-assisted platform for knee arthroplasty. The company highlighted rising adoption in ambulatory surgery centers and hospitals seeking portable, image-free robotic solutions

- In August 2023, Stryker Corporation launched a direct-to-patient marketing campaign for its Mako SmartRobotics platform, aimed at increasing awareness of robotic-assisted hip and knee replacement procedures. The campaign underscored the growing role of consumer education in driving orthopedic robotics adoption

- In November 2023, Monogram Orthopaedics Inc. announced the first delivery of its mBôs surgical robot to a major global robotics distributor. The milestone marked Monogram’s commercial entry into orthopedic robotics with a next-generation semi-autonomous platform focused on joint replacement procedures

- In February 2024, THINK Surgical, Inc. announced a strategic collaboration with Maxx Orthopedics to integrate Maxx implant systems with the TMINI Miniature Robotic System. The partnership advanced open-platform robotics by allowing broader implant compatibility in knee arthroplasty

- In May 2024, leading orthopedic companies including Stryker, Zimmer Biomet, and Globus Medical reported double-digit growth in robotic system sales and placements, reflecting accelerating hospital demand for robotic-assisted orthopedic procedures and increasing installations in ambulatory surgery centers

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.