North America Patient Monitoring Device Market

Market Size in USD Billion

USD

15.60 Billion

USD

27.11 Billion

2024

2032

USD

15.60 Billion

USD

27.11 Billion

2024

2032

| 2025 - 2032 | |

| USD 15.60 Billion | |

| USD 27.11 Billion | |

| % | |

|

Patient Monitoring Devices Market Size

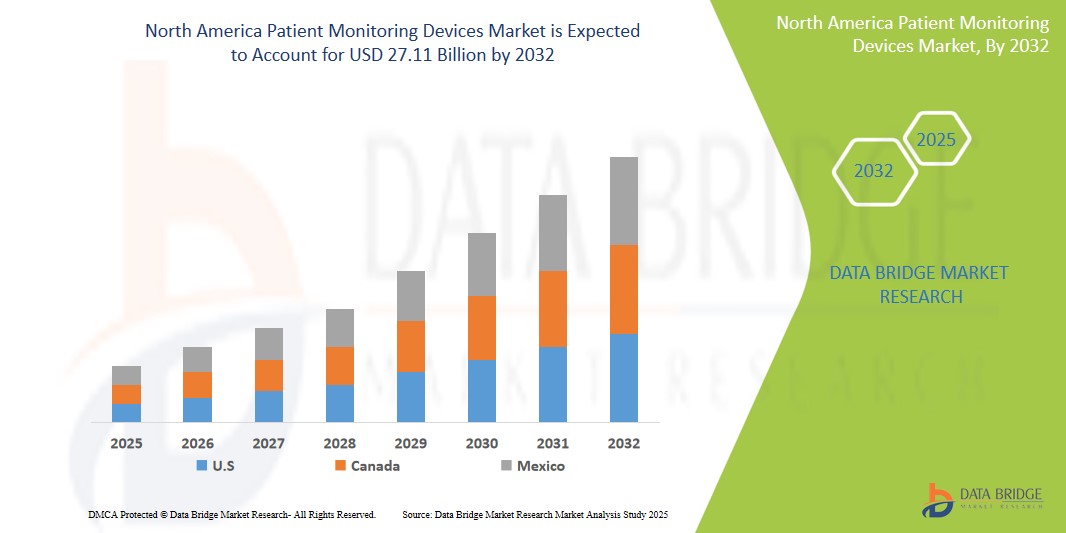

- The North America Patient Monitoring Devices market size was valued at USD 15.60 billion in 2024 and is expected to reach USD 27.11 billion by 2032, at a CAGR of 7.15% during the forecast period

- The market growth is largely fueled by the rising prevalence of chronic diseases, an increasing aging population, and the growing demand for remote patient monitoring (RPM) and home healthcare solutions.

- Furthermore, technological advancements leading to the development of more portable, wireless, and AI-driven monitoring devices are accelerating market expansion. These converging factors are significantly boosting the industry's growth by enabling personalized patient care and reducing the frequency of hospital visits.

Patient Monitoring Devices Market Analysis

- Patient Monitoring Devices market encompasses a broad range of medical devices designed to measure, display, and record various physiological parameters of patients. These devices play a crucial role in continuous health monitoring, early detection of health deterioration, and effective management of chronic diseases. The market includes products such as multi-parameter monitoring devices, cardiac monitoring devices, blood glucose monitoring systems, respiratory monitoring devices, and neuromonitoring devices, catering to diverse healthcare settings from hospitals to home care.

- The escalating demand for patient monitoring devices is primarily fueled by the increasing need for continuous vital sign monitoring, the growing adoption of telehealth services, and the rising focus on preventive healthcare and early diagnosis.

- The U.S. dominates the Patient Monitoring Devices market in North America, holding the largest revenue share of 84.6% in 2025, attributed to the presence of a well-established healthcare infrastructure, increasing prevalence of chronic diseases such as cardiovascular and respiratory disorders, and rising demand for real-time remote patient monitoring technologies. The widespread integration of IoT and AI-based monitoring systems further enhances market growth.

- The U.S. is expected to be the fastest-growing country in the North America Patient Monitoring Devices market during the forecast period, fueled by the surge in geriatric population, growing preference for home healthcare services, and proactive government initiatives supporting digital health solutions and telehealth platforms.

- Cardiac Monitoring Devices are expected to dominate the North America Patient Monitoring Devices market with a market share of 36.8% in 2025, driven by the high burden of cardiovascular diseases, increasing use of portable ECG and wearable heart rate monitors, and continuous innovations in wireless and mobile cardiac telemetry systems.

Report Scope and Patient Monitoring Devices Market Segmentation

|

Attributes |

Patient Monitoring Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Patient Monitoring Devices Market Trends

“Increasing adoption of remote patient monitoring (RPM)”

- Growing Demand for Remote Patient Monitoring (RPM) and Wearable Devices: A significant and accelerating trend in the North America patient monitoring devices market is the increasing demand for remote patient monitoring (RPM) solutions and the widespread adoption of wearable monitoring devices. This shift is driven by the need for continuous health tracking, particularly for chronic disease management, and the preference for home-based care.

- For instance, RPM allows healthcare professionals to monitor patients' health parameters in real-time from the comfort of their homes, reducing the necessity for frequent hospitalizations. Wearable technologies, initially basic fitness trackers, are now becoming vital tools for managing chronic conditions like hypertension, diabetes, and respiratory issues, providing real-time data for early intervention.

- The integration of AI-driven data analysis and machine learning is assisting clinicians in interpreting complex data, predicting early deterioration in patient health, and diagnosing conditions at an earlier stage. Cloud integration facilitates data collection and storage for further analysis.

- Companies are focusing on developing innovative monitoring technologies, such as contactless monitoring solutions, to enhance patient mobility and ease of use. This includes advancements in medical adhesives for long-term wear of sensors and wearables.

- This trend towards more connected, intelligent, and patient-centric monitoring solutions is fundamentally reshaping healthcare delivery, emphasizing proactive and preventive care.

Patient Monitoring Devices Market Dynamics

Driver

“Increasing prevalence of chronic diseases”

- The increasing incidence and prevalence of chronic disorders, such as cardiovascular diseases, metabolic diseases (e.g., diabetes), and respiratory conditions, coupled with a rapidly growing geriatric population in North America, are significant drivers for the heightened demand for patient monitoring devices.

- For instance, chronic diseases require continuous monitoring for effective management and prevention of complications. The aging population is more susceptible to developing these conditions, necessitating the widespread use of patient monitoring devices for regular check-ups and early diagnosis.

- The growing demand for personalized patient care and the emphasis on preventive healthcare further facilitate the use of these devices. Patients and healthcare providers are increasingly recognizing the benefits of continuous monitoring for improved treatment outcomes and reduced healthcare costs.

- Favorable government policies and initiatives, along with sufficient funding for developing novel patient monitoring devices, also support market growth

Restraint/Challenge

“Privacy and security concerns (data breaches, unauthorized access)”

- The major challenges faced by the North America patient monitoring devices market include privacy and security concerns related to patient data, along with the high cost associated with advanced monitoring devices.

- For instance, the collection and transmission of sensitive patient health data through digital devices raise concerns about unauthorized access, data breaches, and device manipulation, which can lead to increased theft, fraud, or other malicious activities. The integration of AI and ML further amplifies these privacy and security risks.

- The high initial cost of sophisticated patient monitoring devices, such as multi-parameter monitors and advanced continuous glucose monitoring systems, can be a significant barrier to widespread adoption, particularly for smaller healthcare facilities or individual patients with limited insurance coverage.

- Additionally, stringent regulatory frameworks and the need for interoperability between different monitoring systems can add complexity and cost to device development and deployment.

Patient Monitoring Devices Market Scope

The market is segmented on the basis type, application and end-user.

- By Type

On the basis of Product, the patient monitoring devices market in North America is segmented into Hemodynamic Monitoring Devices, Neuromonitoring Devices, Cardiac Monitoring Devices, Multi-parameter Monitors, Respiratory Monitoring Devices, and Other Types of Devices. Cardiac Monitoring Devices dominate the market with the largest revenue share of 36.8% in 2025 owing to the growing prevalence of cardiovascular diseases, increasing geriatric population, and rising use of wearable ECG monitors and Holter devices. Technological innovations, including wireless telemetry and smartphone-compatible cardiac patches, further enhance remote diagnosis and continuous monitoring capabilities.

The Multi-parameter Monitors segment is anticipated to witness the fastest growth rate of 7.8% driven by rising demand for comprehensive patient assessment tools in critical care, emergency rooms, and ambulatory settings. These monitors provide simultaneous tracking of vital signs such as heart rate, blood pressure, respiratory rate, and oxygen saturation—making them indispensable in acute and chronic care management.

- By Application

On the basis of application, the Patient Monitoring Devices market is segmented into cardiology, Neurology, Respiratory, Fetal and Neonatal, Weight Management and Fitness Monitoring, and Other Applications. The Cardiology held the largest market revenue share in 2025, attributed to the increasing burden of heart diseases, growing usage of remote ECG, and demand for post-operative cardiac rehabilitation monitoring. Clinical preference for early detection tools and the expansion of telecardiology services further supports growth.

The Fetal and Neonatal monitoring is expected to witness the fastest CAGR from 2025 to 2032, due to increasing birth rates, advancements in neonatal intensive care units (NICUs), and the growing emphasis on prenatal care. Devices such as fetal heart rate monitors and neonatal vital sign monitors ensure continuous surveillance of high-risk pregnancies and premature infants.

- By End users

On the basis of end users, the Patient Monitoring Devices market is segmented into Home Care Settings, Hospitals and Clinics, and Other End Users. The Hospitals and Clinics segment accounted for the largest market revenue share in 2025 driven by the growing number of hospital admissions, especially for chronic and critical illnesses, and the availability of advanced patient monitoring infrastructure. These settings benefit from high patient throughput and access to integrated EHR systems, which support real-time data analytic.

The Home Care Settings segment is expected to witness the fastest CAGR from 2025 to 2032, owing to the rising trend of home-based care, the shift toward value-based healthcare, and the increasing use of wearable and remote monitoring solutions for elderly and chronically ill patients.

Patient Monitoring Devices Market Regional Analysis

- U.S. dominates the Patient Monitoring Devices market with the largest revenue share of 84.6% in 2025, supported by a robust healthcare infrastructure, high prevalence of chronic diseases (such as cardiovascular, respiratory, and neurological disorders), and strong adoption of digital health technologies.

- The country's aging population and growing demand for remote and home-based care solutions are accelerating the uptake of portable and wearable monitoring devices. Integration of AI, cloud connectivity, and IoT-enabled platforms in patient monitoring further enhances real-time data accessibility for clinicians.

- Favorable reimbursement policies, coupled with CMS support for telehealth and remote patient monitoring (RPM) services, contribute significantly to market expansion. Additionally, major players such as Medtronic, GE Healthcare, and Philips continue to introduce advanced multi-parameter monitors and wireless telemetry systems.

- The proliferation of ambulatory surgical centers and outpatient clinics, along with increased hospital investment in intensive care and emergency department monitoring, further fuels demand for innovative and cost-effective patient monitoring technologies.

Canada Patient Monitoring Devices Market Insight

The Canada Patient Monitoring Devices market is projected to witness steady growth over the forecast period, driven by the rise in chronic disease incidence, especially diabetes and heart-related conditions. Canada's universal healthcare system emphasizes preventive care, encouraging investments in early diagnostics and continuous monitoring. Provinces such as Ontario and British Columbia have incorporated remote monitoring into their chronic care strategies, promoting wider adoption of wearable ECGs, pulse oximeters, and home-based monitoring kits. Federal and provincial telehealth initiatives, particularly accelerated during the COVID-19 pandemic, continue to bolster the demand for wireless and cloud-based monitoring solutions. Strong regulatory oversight by Health Canada ensures the availability of high-quality and safe monitoring devices, while collaborations with global medtech companies help bring in advanced technologies and support localized innovation.

Mexico Patient Monitoring Devices Market Insight

The Mexico Patient Monitoring Devices market is expected to grow at a notable CAGR, supported by the country’s ongoing healthcare modernization efforts and expanding middle-class population. Government-led public health initiatives focusing on cardiovascular disease management and diabetes screening have increased the demand for real-time and ambulatory monitoring tools. Urbanization and expansion of private healthcare facilities have created demand for multi-parameter monitors, fetal monitors, and neuromonitoring systems, particularly in metropolitan areas. Though access remains limited in rural zones, increasing foreign investment in medical infrastructure and partnerships with U.S.-based device firms are improving distribution and affordability. Training programs for healthcare professionals and digital transformation in hospitals are supporting the integration of connected monitoring technologies and enhancing patient outcomes across the country.

Patient Monitoring Devices Market Share

The Patient Monitoring Devices industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- Masimo (U.S.)

- Medtronic (U.S.)

- Dragerwerk AG and Co. KGaA (Germany)

- General Electric (U.S.)

- Johnson and Johnson Services, Inc. (U.S.)

- Mortara Instruments Inc (U.K)

- Natus Medical Incorporated (U.S)

- NIHON KOHDEN CORPORATION (Japan)

- Nonin (U.S.)

- OMRON Healthcare Co., Ltd (U.S)

- Koninklijke Philips N.V (Netherlands)

- F.Hoffmann-La Roche Ltd. (U.S.)

- Welch Allyn (U.S)

Latest Developments in North America Patient Monitoring Devices Market

- In April 2024, OMRON Healthcare acquired Luscii Healthtech, a digital health company, to advance its digital health services.

- In March 2023, Koninklijke Philips N.V. announced the launch of Philips Virtual Care Management, offering a complete telehealth method to individuals.

- In February 2023, 3M announced an advancement in their medical adhesive, designed for use with a range of health monitors, sensors, and long-term medical wearables, increasing wear longevity to double the previous duration.

- In January 2023, Biobeat, a global manufacturer of wearable remote patient monitoring devices, received U.S. FDA 510(k) clearance to monitor health indicators such as stroke volume, cardiac output, and cuffless blood pressure.

- In September 2024, Abbott announced the U.S. launch of its continuous glucose monitoring system, Lingo, comprising a biosensor and a mobile app aimed at improving overall health and wellness.

- In November 2024, Monitra Health secured a U.S. patent for its innovative wireless cardiac monitoring technology, featuring a wireless patch designed to enhance patient compliance and improve diagnostic accuracy.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.