North America Persistent Corneal Epithelial Defects Treatment Market

Market Size in USD Billion

CAGR :

%

USD

409.65 Billion

USD

655.38 Billion

2025

2033

USD

409.65 Billion

USD

655.38 Billion

2025

2033

| 2026 –2033 | |

| USD 409.65 Billion | |

| USD 655.38 Billion | |

| % | |

|

Persistent Corneal Epithelial Defects Treatment Market Size

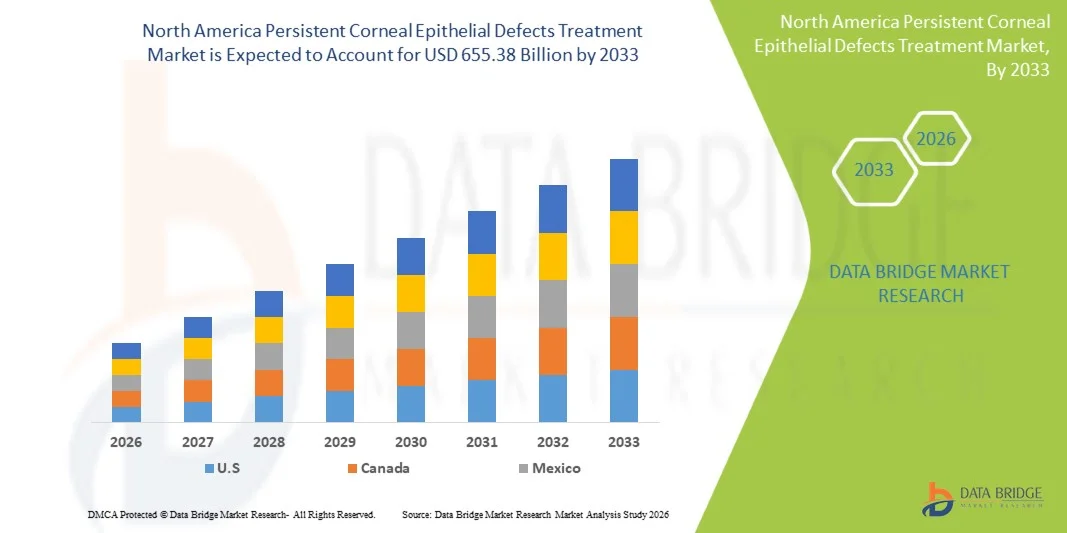

- The North America persistent corneal epithelial defects treatment market size was valued at USD 409.65 billion in 2025and is expected to reach USD 655.38 billion by 2033, at a CAGR of 6.05% during the forecast period

- The market growth is largely fueled by the increasing prevalence of ocular surface disorders, corneal injuries, and post-surgical eye complications, leading to rising demand for advanced ophthalmic therapies and regenerative treatment solutions for persistent corneal epithelial defects across global healthcare systems

- Furthermore, growing adoption of biologics, amniotic membrane therapies, lubricating agents, and regenerative ophthalmology approaches, along with increasing awareness regarding early diagnosis and treatment of chronic corneal conditions, is establishing Persistent Corneal Epithelial Defects Treatment as a critical component of modern ophthalmic care. These converging factors are accelerating the uptake of Persistent Corneal Epithelial Defects Treatment solutions, thereby significantly boosting the industry's growth

Persistent Corneal Epithelial Defects Treatment Market Analysis

- Persistent corneal epithelial defects treatment solutions, which include lubricating agents, biologics, amniotic membrane transplantation, and regenerative ophthalmic therapies, are increasingly vital in modern eye care due to their role in promoting corneal healing, preventing vision loss, and reducing complications associated with chronic ocular surface disorders

- The escalating demand for persistent corneal epithelial defects treatment is primarily fueled by the rising prevalence of corneal injuries, dry eye disease, diabetic keratopathy, post-surgical ocular complications, and increasing adoption of advanced regenerative ophthalmology therapies in clinical practice

- S. dominated the persistent corneal epithelial defects treatment market with the largest revenue share of 39.2% in 2025, driven by advanced ophthalmology infrastructure, strong adoption of biologic and regenerative eye therapies, increasing prevalence of ocular surface disorders, and substantial healthcare spending, with the U.S. dominating the regional market due to high procedural volumes and strong presence of leading ophthalmic treatment providers

- Canada is expected to be the fastest growing country in the North American persistent corneal epithelial defects treatment market during the forecast period due to improving access to specialized ophthalmic care, rising awareness regarding early corneal disease treatment, and growing adoption of advanced ocular regenerative therapies

- The medication segment accounted for the largest market revenue share of 63.2% in 2025, driven by widespread use of topical lubricants, antibiotics, corticosteroids, and biologic agents in corneal healing management

Report Scope and Persistent Corneal Epithelial Defects Treatment Market Segmentation

|

Attributes |

Persistent Corneal Epithelial Defects Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico |

|

Key Market Players |

• Santen Pharmaceutical Co., Ltd. (Japan) |

|

Market Opportunities |

· Growing Adoption of Regenerative and Biologic Ophthalmic Therapies · Rising Prevalence of Ocular Surface Disorders and Post-Surgical Eye Complications |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Persistent Corneal Epithelial Defects Treatment Market Trends

“Increasing Adoption of Regenerative Ophthalmic Therapies and Advanced Biologic Treatments”

- A significant and accelerating trend in the North America Persistent Corneal Epithelial Defects Treatment market is the growing adoption of regenerative ophthalmic therapies and advanced biologic treatment approaches aimed at improving corneal healing and reducing long-term vision complications

- For instance, therapies such as amniotic membrane transplantation, autologous serum eye drops, and biologic tear substitutes are increasingly being utilized to promote epithelial regeneration and accelerate corneal surface healing in patients with persistent epithelial defects

- The rising prevalence of ocular surface disorders, neurotrophic keratitis, diabetic eye complications, and post-surgical corneal injuries is driving increased demand for advanced therapeutic interventions across North America

- Furthermore, advancements in ophthalmic drug delivery systems and regenerative medicine technologies are improving treatment efficacy, patient comfort, and long-term clinical outcomes

- The increasing focus on early diagnosis and specialized ophthalmic care is also encouraging the use of targeted therapies that minimize the risk of corneal ulceration, infection, and permanent visual impairment

- This trend toward regenerative medicine, biologic therapies, and advanced ocular surface management is reshaping ophthalmic treatment strategies. Consequently, companies such as Dompé and Santen Pharmaceutical are expanding their ophthalmic treatment portfolios and clinical research initiatives

- The demand for advanced Persistent Corneal Epithelial Defects treatments is increasing steadily across hospitals, ophthalmology clinics, and specialty eye care centers due to growing awareness regarding vision preservation and ocular surface health

Persistent Corneal Epithelial Defects Treatment Market Dynamics

Driver

“Rising Prevalence of Ocular Surface Disorders and Growing Aging Population”

- The increasing prevalence of ocular surface disorders and age-related eye diseases is a major driver supporting the growth of the North America Persistent Corneal Epithelial Defects Treatment market

- For instance, conditions such as neurotrophic keratitis, dry eye disease, diabetic keratopathy, and post-refractive surgery complications are contributing significantly to the growing number of persistent corneal epithelial defect cases

- The expanding aging population across North America is further increasing susceptibility to corneal healing disorders and chronic ophthalmic conditions, thereby driving demand for advanced treatment solutions

- Furthermore, rising awareness regarding early ophthalmic intervention and improved access to specialized eye care services are encouraging higher treatment adoption rates

- Advancements in corneal imaging technologies, biologic therapies, and minimally invasive ophthalmic procedures are also improving diagnostic accuracy and therapeutic effectiveness

- In addition, increasing healthcare expenditure, favorable reimbursement support for ophthalmic treatments, and ongoing clinical research activities are contributing to market expansion across the region

Restraint/Challenge

“High Treatment Costs and Limited Accessibility of Advanced Therapies”

- The high cost associated with advanced regenerative ophthalmic therapies and biologic treatments remains a significant challenge affecting broader market adoption

- For instance, therapies such as amniotic membrane transplantation and biologic eye drop formulations may involve substantial procedural and treatment costs, limiting affordability for certain patient populations

- In addition, limited availability of specialized ophthalmology centers and trained corneal specialists in some regions may restrict timely diagnosis and treatment access

- The complexity of long-term disease management and the need for continuous follow-up care may also create adherence challenges among patients with chronic ocular surface conditions

- Furthermore, regulatory approval requirements and limited long-term clinical data for certain emerging regenerative therapies can slow commercialization and widespread adoption

- Overcoming these challenges through improved reimbursement frameworks, expanded ophthalmic specialist access, continued clinical research, and development of cost-effective treatment solutions will be essential for sustaining long-term growth in the North America Persistent Corneal Epithelial Defects Treatment market

Persistent Corneal Epithelial Defects Treatment Market Scope

The market is segmented on the basis of clinical causes, type, end user, and distribution channel.

- By Clinical Causes

On the basis of clinical causes, the Persistent Corneal Epithelial Defects Treatment market is segmented into inflammatory disease, neurotrophic keratitis (NK), epithelial/limbal stem cell deficiency, and others. The neurotrophic keratitis (NK) segment dominated the largest market revenue share of 41.7% in 2025, driven by the increasing prevalence of corneal nerve damage associated with diabetes, herpes simplex infections, and ocular surgeries. Neurotrophic keratitis is a severe degenerative corneal disorder that often results in delayed epithelial healing and chronic corneal defects. Rising awareness regarding early diagnosis and specialized ophthalmic care is significantly supporting segment growth. Healthcare providers are increasingly utilizing advanced biologics and regenerative therapies for NK management. The segment benefits from growing research into nerve growth factor-based treatments and novel ophthalmic drugs. Increasing aging population and higher incidence of chronic eye diseases are also contributing to market expansion. Favorable regulatory approvals for innovative therapies are further driving adoption. Expansion of ophthalmology specialty centers globally is supporting treatment accessibility. Furthermore, increasing investment in rare ocular disease treatment development is expected to sustain segment dominance during the forecast period.

The epithelial/limbal stem cell deficiency segment is expected to witness the fastest CAGR of 10.9% from 2026 to 2033, driven by rising incidence of ocular burns, trauma, autoimmune disorders, and long-term contact lens complications. Limbal stem cell deficiency leads to impaired corneal regeneration and persistent epithelial defects, increasing the need for advanced regenerative therapies. The segment benefits from growing adoption of stem cell-based ophthalmic treatments and tissue engineering technologies. Increasing investment in regenerative medicine research is significantly supporting growth. Healthcare providers are increasingly focusing on biologic therapies for restoring corneal integrity. Rising awareness regarding advanced ocular treatment options is further boosting demand. Academic research institutions are actively exploring novel limbal transplantation techniques. Expanding access to specialty ophthalmology clinics is also contributing to segment growth. Technological advancements in cell therapy and biomaterials are improving clinical outcomes. Furthermore, increasing focus on personalized ophthalmic treatments is expected to drive strong segment expansion during the forecast period.

- By Type

On the basis of type, the Persistent Corneal Epithelial Defects Treatment market is segmented into devices and medication. The medication segment accounted for the largest market revenue share of 63.2% in 2025, driven by widespread use of topical lubricants, antibiotics, corticosteroids, and biologic agents in corneal healing management. Medications remain the first-line treatment approach for persistent epithelial defects due to ease of administration and broad therapeutic effectiveness. The segment benefits from increasing availability of advanced ophthalmic formulations with enhanced healing properties. Growing prevalence of ocular surface disorders is significantly supporting market demand. Pharmaceutical companies are investing in innovative therapies such as growth factor-based eye drops and regenerative biologics. Rising healthcare expenditure and improved ophthalmic care infrastructure are also contributing to market growth. Increasing patient preference for non-invasive treatment approaches further strengthens adoption. Expanding awareness regarding early intervention is helping improve treatment uptake. Furthermore, continuous development of targeted ocular therapies is expected to sustain segment dominance during the forecast period.

The devices segment is expected to witness the fastest CAGR of 11.6% from 2026 to 2033, driven by increasing adoption of advanced ophthalmic devices such as amniotic membrane grafts, therapeutic contact lenses, and corneal bandage systems. These devices help accelerate epithelial healing and protect the ocular surface from further damage. The segment benefits from rising demand for minimally invasive ophthalmic procedures. Technological advancements in bioengineered corneal devices are significantly improving treatment outcomes. Healthcare providers are increasingly integrating device-assisted therapies into chronic corneal defect management. Growing awareness regarding regenerative ophthalmology solutions is further supporting growth. Expansion of specialty eye care centers globally is improving treatment accessibility. Rising incidence of severe ocular trauma and post-surgical complications is also driving demand. Research collaborations between medical device companies and ophthalmology institutes are accelerating innovation. Furthermore, increasing focus on advanced wound healing technologies is expected to drive strong segment growth during the forecast period.

- By End User

On the basis of end user, the Persistent Corneal Epithelial Defects Treatment market is segmented into hospital/clinical laboratories, physician offices, reference laboratories, and other end users. The hospital/clinical laboratories segment dominated the largest market revenue share of 48.5% in 2025, driven by the high volume of ophthalmic procedures and specialized diagnostic capabilities available in hospitals. These facilities serve as primary treatment centers for severe and chronic corneal disorders requiring multidisciplinary management. The segment benefits from availability of advanced imaging technologies and skilled ophthalmologists. Increasing prevalence of corneal injuries and ocular surface diseases is significantly contributing to hospital admissions. Healthcare providers increasingly rely on hospital-based infrastructure for surgical interventions and regenerative therapies. Rising healthcare investments and expansion of ophthalmology departments are also supporting market growth. Hospitals are actively adopting advanced biologics and corneal repair technologies. The segment further benefits from favorable reimbursement frameworks in developed markets. Increasing collaborations between hospitals and research institutions are accelerating innovation. Furthermore, rising patient preference for specialized eye care services is expected to sustain segment dominance during the forecast period.

The physician offices segment is expected to witness the fastest CAGR of 9.8% from 2026 to 2033, driven by increasing demand for accessible outpatient ophthalmic care and early-stage treatment services. Physician offices provide cost-effective diagnosis and treatment for mild to moderate corneal epithelial defects. The segment benefits from growing awareness regarding preventive eye care and routine ophthalmic evaluations. Increasing availability of portable diagnostic technologies is improving treatment efficiency in outpatient settings. Rising adoption of teleophthalmology services is further supporting market expansion. Healthcare providers are increasingly offering personalized treatment plans in office-based settings. Growing patient preference for convenient and shorter consultation visits is contributing to demand. Expanding private ophthalmology practices in emerging economies are also supporting growth. Continuous advancements in outpatient ocular therapies are improving clinical outcomes. Furthermore, increasing focus on early intervention and follow-up care is expected to drive strong segment growth during the forecast period.

- By Distribution Channel

On the basis of distribution channel, the Persistent Corneal Epithelial Defects Treatment market is segmented into direct tender, retail sales, and other. The direct tender segment accounted for the largest market revenue share of 45.3% in 2025, driven by bulk procurement of ophthalmic medications and devices by hospitals and specialty eye care institutions. Direct tender agreements ensure cost-effective purchasing and uninterrupted supply of critical ophthalmic treatment products. The segment benefits from increasing government healthcare spending and expansion of public ophthalmology programs. Healthcare institutions prefer direct procurement channels for high-value regenerative therapies and surgical devices. Rising prevalence of chronic ocular disorders is significantly supporting demand. Pharmaceutical and medical device companies are increasingly entering long-term supply agreements with hospitals. Growing adoption of biologics and specialty ocular products is also driving market expansion. The segment further benefits from centralized purchasing systems in developed healthcare markets. Increasing public-private partnerships in eye care infrastructure are supporting procurement efficiency. Furthermore, rising investments in ophthalmic healthcare systems are expected to sustain segment dominance during the forecast period.

The retail sales segment is expected to witness the fastest CAGR of 10.4% from 2026 to 2033, driven by increasing availability of ophthalmic medications through pharmacies and retail healthcare outlets. Retail channels provide easy accessibility to lubricating eye drops, antibiotics, and supportive ocular therapies for outpatient management. The segment benefits from rising awareness regarding eye health and self-care treatments. Expanding pharmacy networks and e-commerce healthcare platforms are significantly supporting growth. Patients increasingly prefer retail pharmacies for convenience and faster access to medications. Pharmaceutical companies are strengthening retail distribution partnerships to improve product reach. Growing prevalence of dry eye disease and ocular surface disorders is also contributing to rising sales volumes. Technological advancements in ophthalmic formulations are further driving adoption. Increasing healthcare spending and urbanization are improving market penetration. Furthermore, expanding over-the-counter ophthalmic product availability is expected to drive strong segment growth during the forecast period.

Persistent Corneal Epithelial Defects Treatment Market Regional Analysis

- North America dominated the Persistent Corneal Epithelial Defects Treatment market with the largest revenue share of 39.2% in 2025, driven by advanced ophthalmology infrastructure, strong adoption of biologic and regenerative eye therapies, increasing prevalence of ocular surface disorders, and substantial healthcare spending. The region benefits from high awareness regarding early diagnosis and treatment of corneal diseases, along with increasing availability of specialized ophthalmic care centers and advanced therapeutic options for persistent corneal epithelial defects

- Rising incidence of dry eye syndrome, neurotrophic keratitis, corneal injuries, and post-surgical ocular complications is significantly driving demand for advanced corneal epithelial defect treatments across hospitals and specialty eye clinics. In addition, growing adoption of regenerative therapies, amniotic membrane transplantation, and biologic eye drops is supporting market expansion across the region

- Furthermore, strong presence of leading ophthalmic treatment providers, increasing ophthalmic research activities, and favorable reimbursement frameworks are reinforcing North America’s leadership in the global Persistent Corneal Epithelial Defects Treatment market, with the U.S. accounting for the majority of regional procedural volumes and treatment adoption

U.S. Persistent Corneal Epithelial Defects Treatment Market Insight

The U.S. Persistent Corneal Epithelial Defects Treatment market captured the largest revenue share within North America in 2025, driven by advanced ophthalmic healthcare infrastructure, high procedural volumes, and strong adoption of biologic and regenerative eye therapies. Increasing prevalence of ocular surface disorders, rising incidence of corneal injuries, and growing demand for innovative treatment approaches are significantly contributing to market growth. Additionally, strong presence of leading ophthalmic treatment providers, increasing ophthalmology research activities, and favorable reimbursement frameworks continue to propel the market expansion in the U.S.

Canada Persistent Corneal Epithelial Defects Treatment Market Insight

The Canada Persistent Corneal Epithelial Defects Treatment market is expected to witness the fastest growth in North America during the forecast period due to improving access to specialized ophthalmic care, rising awareness regarding early corneal disease treatment, and growing adoption of advanced ocular regenerative therapies. Increasing healthcare investments, expanding ophthalmology services, and rising focus on preventive eye care are further supporting market growth. Moreover, growing availability of advanced corneal treatment procedures and supportive healthcare initiatives are contributing significantly to the expansion of the market in Canada.

Latest Developments in North America Persistent Corneal Epithelial Defects Treatment Market

- In March 2021, clinical studies published in ophthalmology journals demonstrated long-term efficacy of cenegermin (Oxervate), a recombinant human nerve growth factor therapy, in treating neurotrophic keratitis associated with persistent corneal epithelial defects (PCED). Researchers reported sustained corneal healing, improved visual acuity, and reduced recurrence rates for up to 48 months following treatment, reinforcing the growing adoption of regenerative biologic therapies in ocular surface disease management

- In December 2021, Health Canada approved reimbursement recommendations for Oxervate (cenegermin) for the treatment of moderate and severe neurotrophic keratitis with persistent epithelial defects in adults. The recommendation supported broader patient access to the first approved recombinant nerve growth factor therapy for difficult-to-heal corneal defects.

- In April 2023, industry reports highlighted accelerated R&D activity in the Persistent Corneal Epithelial Defects Treatment market, with companies advancing regenerative biologics, ocular surface modulators, and growth factor-based therapeutics designed to improve epithelial regeneration and reduce corneal scarring. The development underscored growing investment in advanced ophthalmic biologics for chronic ocular surface disorders

- In May 2025, EyeWorld reported a rapidly expanding pharmaceutical pipeline for neurotrophic keratitis and persistent corneal epithelial defects, with several novel biologics, growth factor therapies, and regenerative ophthalmic treatments advancing through clinical development. Experts noted that the commercial success of Oxervate had significantly accelerated innovation and investment in the PCED treatment space

- In July 2025, Kala Bio announced completion of enrollment in the CHASE clinical trial evaluating KPI-012 for the treatment of persistent corneal epithelial defects. The company stated that the study could potentially support a future Biologics License Application (BLA) submission to the U.S. FDA, marking a major milestone in the development of next-generation ocular surface regenerative therapies

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.