North America Pharmacogenetic Testing In Psychiatry Depression Market

Market Size in USD Million

USD

677.59 Million

USD

1,421.08 Million

2025

2033

USD

677.59 Million

USD

1,421.08 Million

2025

2033

| 2026 - 2033 | |

| USD 677.59 Million | |

| USD 1,421.08 Million | |

| % | |

|

North America Pharmacogenetics Testing in Psychiatry/Depression Market Overview

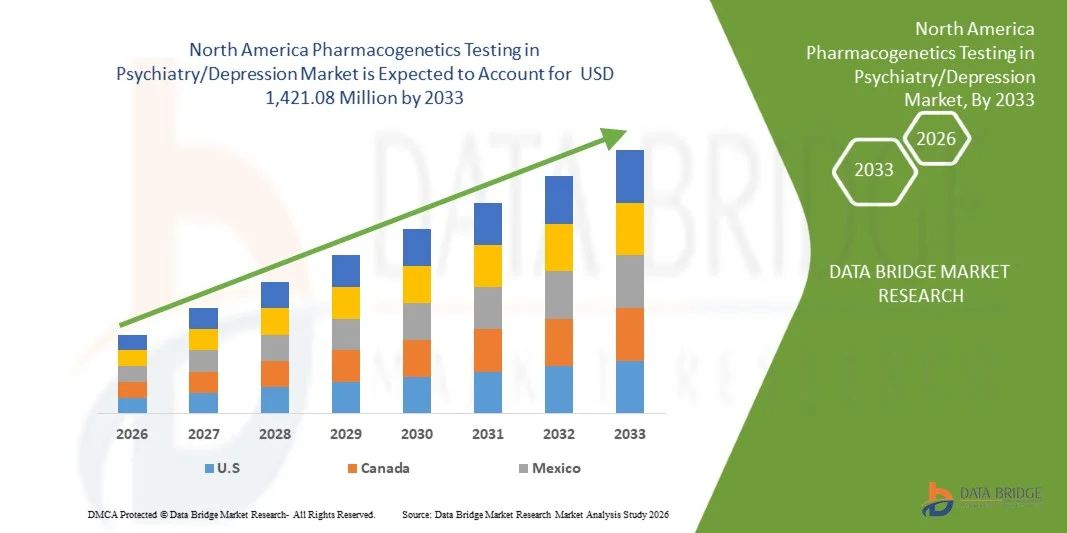

The North America pharmacogenetics testing in psychiatry/depression market was valued at USD 677.59 million in 2025 and is projected to reach USD 1,421.08 million by 2033, growing at a CAGR of 9.7% from 2026 to 2033. The market is witnessing steady expansion driven by the increasing prevalence of depression and other psychiatric disorders, rising adoption of precision medicine approaches, and growing clinical evidence supporting gene–drug interaction testing to improve antidepressant treatment outcomes.

The strong healthcare infrastructure in the United States and Canada, along with higher awareness among psychiatrists regarding personalized treatment strategies, is accelerating the integration of pharmacogenetic testing into routine psychiatric care. Additionally, favorable reimbursement trends in selected regions, expanding use of companion diagnostics, and ongoing advancements in genomic technologies are further supporting market growth, while the shift toward value-based care is encouraging wider adoption of cost-effective, outcome-driven testing solutions in mental health management.

Key Market Trends & Insights

- The United States dominated the global pharmacogenetics testing in psychiatry/depression market with the largest revenue share of 88.42% in 2025, supported by strong adoption of precision medicine, advanced genomic testing infrastructure, and high awareness among psychiatrists and healthcare providers.

- The Depression segment led the market with a 38.42% share in 2025, driven by the high prevalence of major depressive disorder across the U.S. and Canada and strong clinical need for optimized antidepressant therapy.

- Canada represented the fastest-growing country at a CAGR of 7.5% from 2026 to 2033, fueled by expanding reimbursement coverage, increasing mental health burden, and gradual integration of pharmacogenomics into psychiatric care pathways.

- Bipolar disorders are the fastest-growing type, projected to register a CAGR of 8.5%, reflecting the surge in rising diagnosis rates and growing complexity in mood stabilization therapy.

- The Chromosomal array-based tests segment dominated the test type category with a 55.60% revenue share in 2025, led by cost-effectiveness, faster turnaround time, and strong clinical validation in psychiatric pharmacogenetics.

- Adult accounted for 60.65% of the market, preferred by the high prevalence of depression, anxiety, and mood disorders in working-age populations.

- The Software & services segment is the fastest-growing products category, with a CAGR of 10.2%, driven by the increasing need for advanced interpretation of genetic data. AI-based clinical decision support tools are being integrated into psychiatric workflows.

Market Size & Forecast

- Global Market Value (2025): USD 677.59 Million

- Expected Market Value (2033): USD 1,421.08 Million

- Forecast CAGR (2026–2033): 9.7%

- Leading Country in 2025: United States

- Fastest Growing Country: Canada

Report Scope and North America Pharmacogenetics Testing in Psychiatry/Depression Market Segmentation

|

Attributes |

North America Pharmacogenetics Testing in Psychiatry/Depression Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico |

|

Key Market Players |

· Illumina, Inc. (U.S.) · Thermo Fisher Scientific Inc. (U.S.) · QIAGEN (Germany) · F. Hoffmann-La Roche Ltd (Switzerland) · Agilent Technologies, Inc. (U.S.) · PerkinElmer Inc. (U.S.) · Centogene N.V. (Germany) · Eurofins Scientific SE (Luxembourg) · Abbott (U.S.) · Labcorp (U.S.) · BGI Group (China) · Quest Diagnostics Incorporated (U.S.) · Revvity, Inc. (U.S.) · Azenta Life Sciences (U.S.) · Oxford Nanopore Technologies plc (U.K.) · PathCare Laboratories (South Africa) · Ampath Laboratories (South Africa) · Lancet Laboratories (South Africa) · Al Borg Diagnostics (Saudi Arabia) · Synlab International GmbH (Germany) |

|

Market Opportunities |

· Expansion of pharmacogenetic testing into treatment-resistant depression management · Integration of pharmacogenetic decision-support tools within electronic health record (EHR) systems · Growing adoption of direct-to-provider genomic testing services |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

North America Pharmacogenetics Testing in Psychiatry/Depression Market Trends

Trend: Expansion of Clinical Adoption in Psychiatric Care

Pharmacogenetic testing is increasingly being integrated into routine psychiatric practice across North America, enabling clinicians to personalize antidepressant selection based on genetic profiles. Hospitals and mental health clinics are adopting gene–drug interaction panels to reduce trial-and-error prescribing and improve treatment outcomes. The growing use of multi-gene testing platforms is standardizing decision-making in depression management, while digital health integration supports seamless reporting into electronic medical records. For instance, large academic medical centers in the United States are embedding pharmacogenomics reports directly into psychiatric workflows to guide treatment selection.

North America Pharmacogenetics Testing in Psychiatry/Depression Market Dynamics

Key Market Driver: Rising Burden of Treatment-Resistant Depression

The increasing prevalence of treatment-resistant depression and other psychiatric disorders is driving demand for pharmacogenetic testing to optimize antidepressant therapy. Clinicians are using genetic insights to predict drug response and minimize adverse drug reactions, improving patient outcomes and reducing healthcare costs. Expanding clinical evidence supporting gene–drug interactions is accelerating physician confidence in test adoption. For instance, healthcare systems in the United States are increasingly utilizing pharmacogenetic panels in patients who fail multiple antidepressant therapies.

Key Restraint/Challenge: Limited Reimbursement and High Testing Costs

A major restraint in the North American market is the inconsistent reimbursement coverage for pharmacogenetic testing across insurance providers and healthcare systems. High out-of-pocket costs for multi-gene panels limit adoption, particularly in smaller clinics and community healthcare settings. Additionally, lack of standardized clinical guidelines across psychiatric applications slows widespread integration into routine care. For instance, several outpatient mental health providers in Canada continue to face reimbursement barriers when implementing comprehensive pharmacogenomic testing.

Key Market Opportunity: Expansion of AI-Driven Clinical Decision Support Systems

The integration of artificial intelligence and clinical decision support tools presents a major opportunity for scaling pharmacogenetic testing adoption in psychiatry. AI-powered platforms can interpret complex gene–drug interactions and provide real-time prescribing recommendations to clinicians. Cloud-based genomic analytics and digital health platforms are further enabling scalable deployment across healthcare systems. For instance, digital psychiatry networks in the United States are deploying AI-enabled pharmacogenomic tools to assist psychiatrists in selecting optimized antidepressant therapies.

North America Pharmacogenetics Testing in Psychiatry/Depression Market Scope

The North America pharmacogenetics testing in psychiatry/depression market is segmented on the basis of type, test type, patient type, gene type, products, end user, and distribution channel.

- By Type

On the basis of type, the North America pharmacogenetics testing in psychiatry/depression market is segmented into anxiety disorders, mood disorders, depression, bipolar disorders, psychotic disorders, and eating disorders. The Depression segment dominated the market with a 2025 share of 38.42%, owing to the high prevalence of major depressive disorder across the U.S. and Canada and strong clinical need for optimized antidepressant therapy. Depression is the most commonly treated psychiatric condition where pharmacogenetic testing is applied to reduce trial-and-error prescribing. High prescription rates of SSRIs and SNRIs, which show gene–drug interactions, further strengthen demand. Insurance coverage and reimbursement support are also more established for depression-related testing. Clinical guidelines increasingly recommend genetic testing in treatment-resistant depression cases. Continuous expansion of commercial gene panels focused on antidepressant response reinforces its dominance.

The Bipolar disorders segment is projected to register the fastest growth with a CAGR of 8.5% (2026–2033), driven by rising diagnosis rates and growing complexity in mood stabilization therapy. Bipolar patients often require multiple drug classes including mood stabilizers and antipsychotics, which have strong pharmacogenetic relevance. Increasing awareness of lithium toxicity risk and adverse drug reactions is boosting testing adoption. Improved diagnostic accuracy is expanding the identifiable patient base. Pharmacogenetic testing is increasingly used to guide drug selection and dose optimization in bipolar disorder management. Expansion of specialized psychiatric care and telepsychiatry is further accelerating segment growth.

- By Test Type

On the basis of test type, the market is segmented into whole genome sequencing and chromosomal array-based tests. The Chromosomal array-based tests segment dominated the market with a 2025 share of 55.60%, due to its cost-effectiveness, faster turnaround time, and strong clinical validation in psychiatric pharmacogenetics. These tests are widely used in routine clinical settings for detecting known pharmacogenomic variants. Standardized interpretation and easier integration into clinical workflows make them highly preferred by hospitals and diagnostic laboratories. Insurance reimbursement is more readily available for array-based panels. High scalability and established infrastructure further support adoption. Their widespread use in commercial psychiatric gene panels reinforces market dominance.

The Whole genome sequencing segment is expected to register the fastest growth with a CAGR of 10.1% (2026–2033), driven by increasing demand for comprehensive genetic profiling. WGS enables identification of rare and novel variants influencing psychiatric drug response. Declining sequencing costs and improved bioinformatics tools are making it more clinically viable. Pharmaceutical companies are increasingly using WGS for drug discovery and precision psychiatry research. Growing adoption in academic and translational research is accelerating commercialization. Expansion of personalized medicine initiatives is further boosting demand.

- By Patient Type

On the basis of patient type, the market is segmented into child, adult, and geriatric populations. The Adult segment dominated the market with a 2025 share of 60.65%, due to the high prevalence of depression, anxiety, and mood disorders in working-age populations. Adults represent the largest prescription base for antidepressants and antipsychotics, making them the primary target for pharmacogenetic testing. High exposure to stress-related psychiatric conditions further increases demand. Established clinical guidelines support genetic testing in adult psychiatric care. Insurance coverage and employer-sponsored healthcare systems also enhance adoption. Routine integration of pharmacogenetics in adult psychiatric treatment pathways reinforces dominance.

The Child segment is projected to register the fastest growth with a CAGR of 9.0% (2026–2033), driven by rising awareness of pediatric mental health disorders such as ADHD, anxiety, and early-onset depression. There is increasing focus on reducing adverse drug reactions in children through personalized medicine. Pediatric psychiatrists are increasingly adopting pharmacogenetic testing to improve medication safety. Parental awareness and demand for precision treatment options are growing rapidly. Expansion of pediatric mental health services and school-based screening programs supports growth. Regulatory emphasis on safer pediatric prescribing further accelerates adoption.

- By Gene Type

On the basis of gene type, the market is segmented into CYP2C19, CYP2C9, VKORC1, CYP2D6, HLA-B, HLA-A, CYP3A4, SLC6A4, MTHFR, COMT, HTR2A/C, and others. The CYP2D6 segment dominated the market with a 2025 share of 28.32%, as it plays a central role in metabolizing a wide range of antidepressants and antipsychotics. It is one of the most clinically validated pharmacogenes in psychiatry and is included in most commercial testing panels. CYP2D6 variations significantly impact drug efficacy, dosing, and risk of adverse effects. Strong guideline support from clinical pharmacology organizations reinforces its widespread adoption. It is routinely used in precision psychiatry for antidepressant optimization. High clinical utility ensures continued dominance.

The HLA-B segment is expected to register the fastest growth with a CAGR of 9.1% (2026–2033), due to increasing awareness of severe drug-induced hypersensitivity reactions. HLA-B testing helps identify patients at risk of adverse reactions to certain psychiatric medications. Regulatory guidance for screening high-risk populations is supporting adoption. Expanding focus on pharmacovigilance and drug safety is increasing its clinical relevance. Integration into psychiatric safety panels is rising. Growing emphasis on preventing life-threatening adverse drug reactions is accelerating demand.

- By Products

On the basis of products, the market is segmented into instruments, consumables, and software & services. The Consumables segment dominated the market with a 2025 share of 50.55%, due to continuous demand for test kits, reagents, and assay panels used in pharmacogenetic testing. Every test requires consumable inputs, ensuring recurring revenue generation. High testing volumes in psychiatric diagnostics further strengthen demand. Standardization of consumable-based gene panels supports widespread adoption. Hospitals and laboratories maintain regular procurement cycles. Rising test penetration directly drives consumables market leadership.

The Software & services segment is projected to register the fastest growth with a CAGR of around 10.2% (2026–2033), driven by increasing need for advanced interpretation of genetic data. AI-based clinical decision support tools are being integrated into psychiatric workflows. Cloud-based genomic platforms are enabling scalable data analysis and reporting. Integration with electronic health records is improving usability in clinical settings. Expansion of telepsychiatry is further increasing demand for remote interpretation services. Growing complexity of genomic datasets is accelerating software adoption.

- By End User

On the basis of end user, the market is segmented into hospitals and clinics, diagnostic laboratories, academic and research institutes, and others. The Hospitals and clinics segment dominated the market with a 2025 share of 45.50%, due to their primary role in psychiatric diagnosis and treatment. They are the main point of care for patients receiving antidepressant and antipsychotic therapy. Integration of pharmacogenetic testing into routine psychiatric workflows is increasing. Hospitals benefit from strong reimbursement frameworks and established laboratory partnerships. High patient volume ensures consistent demand for testing services. Clinical adoption guidelines further strengthen dominance.

The Diagnostic laboratories segment is projected to register the fastest growth with a CAGR of 9.5% (2026–2033), driven by increasing outsourcing of genetic testing services. Specialized labs offer cost-efficient and scalable pharmacogenetic testing solutions. Expansion of direct-to-consumer and physician-ordered testing models is increasing adoption. Technological advancements are enabling faster and more accurate genomic analysis. Partnerships between labs and healthcare providers are expanding access. Rising demand for centralized genomic testing services is fueling rapid growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, third party distribution, hospital pharmacy, and others.nThe Direct tender segment dominated the market with a 2025 share of 40.45%, due to bulk procurement by hospitals, government healthcare systems, and integrated care networks. Direct contracts ensure cost efficiency and standardized supply of pharmacogenetic testing services. Long-term agreements with diagnostic companies provide stable revenue flow. It is widely used in institutional psychiatric programs. Bulk purchasing reduces per-test costs significantly. Strong presence in public healthcare systems reinforces dominance.

The Third party distribution segment is expected to register the fastest growth with a CAGR of around 8.5% (2026–2033), driven by increasing commercialization and expansion of testing access. Distributors are helping smaller clinics and diagnostic centers adopt advanced pharmacogenetic solutions. Growth of private healthcare systems is boosting indirect sales channels. Logistics improvements are enhancing reach in semi-urban and rural regions. Strategic partnerships between manufacturers and distributors are expanding market penetration. Rising demand for decentralized testing is accelerating growth.

North America Pharmacogenetics Testing in Psychiatry/Depression Market Regional Analysis

The United States dominated the global pharmacogenetics testing in psychiatry/depression market with the largest revenue share of 88.42% in 2025, supported by strong adoption of precision medicine, advanced genomic testing infrastructure, and high awareness among psychiatrists and healthcare providers. The country benefits from a highly advanced healthcare infrastructure, widespread availability of commercial genetic testing panels, and strong presence of key market players driving innovation and clinical adoption. Favorable reimbursement policies from private insurers and growing inclusion of pharmacogenetic testing in treatment-resistant depression management further strengthen market penetration. Increasing investments in digital health, AI-driven clinical decision support tools, and genomic medicine initiatives are also accelerating adoption.

The U.S. Pharmacogenetics Testing in Psychiatry/Depression Market Insight

The U.S. pharmacogenetics testing in psychiatry/depression market is witnessing strong growth due to rising prevalence of mental health disorders, increasing adoption of precision medicine, and growing use of gene-guided antidepressant prescribing. The country’s advanced healthcare infrastructure, strong presence of genomic testing companies, and high integration of pharmacogenetic panels in clinical psychiatry are driving demand across hospitals, specialty clinics, and diagnostic laboratories. In addition, favorable reimbursement coverage, expansion of commercial genetic test offerings, and increasing use of clinical decision support tools are accelerating adoption across treatment-resistant depression and anxiety disorders.

Canada Pharmacogenetics Testing in Psychiatry/Depression Market Insight

The Canada pharmacogenetics testing in psychiatry/depression market is experiencing steady growth, supported by increasing mental health awareness, expansion of public healthcare initiatives, and gradual integration of personalized medicine into psychiatric care. Growing adoption of pharmacogenetic testing in major urban healthcare centers and academic hospitals is supporting market expansion. Increasing government focus on mental health treatment accessibility, along with rising utilization of antidepressants and mood stabilizers, is further driving demand. However, slower reimbursement harmonization compared to the U.S. slightly limits widespread adoption.

Mexico Pharmacogenetics Testing in Psychiatry/Depression Market Insight

The Mexico pharmacogenetics testing in psychiatry/depression market is witnessing emerging growth, driven by increasing awareness of mental health disorders, gradual adoption of precision medicine, and rising demand for improved treatment outcomes in depression and anxiety management. The country is seeing expanding use of antidepressants and antipsychotics, which is encouraging interest in pharmacogenetic testing to reduce trial-and-error prescribing and improve drug response predictability. Growing presence of private diagnostic laboratories, improving healthcare infrastructure in urban centers, and increasing collaborations with international genomic testing providers are supporting early market development.

North America Pharmacogenetics Testing in Psychiatry/Depression Market Share

The North America pharmacogenetics testing in psychiatry/depression industry is primarily led by well-established companies, including:

- Illumina, Inc. (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- QIAGEN (Germany)

- Hoffmann-La Roche Ltd (Switzerland)

- Agilent Technologies, Inc. (U.S.)

- PerkinElmer Inc. (U.S.)

- Centogene N.V. (Germany)

- Eurofins Scientific SE (Luxembourg)

- Abbott (U.S.)

- Labcorp (U.S.)

- BGI Group (China)

- Quest Diagnostics Incorporated (U.S.)

- Revvity, Inc. (U.S.)

- Azenta Life Sciences (U.S.)

- Oxford Nanopore Technologies plc (U.K.)

- PathCare Laboratories (South Africa)

- Ampath Laboratories (South Africa)

- Lancet Laboratories (South Africa)

- Al Borg Diagnostics (Saudi Arabia)

- Synlab International GmbH (Germany)

Latest Developments in North America Pharmacogenetics Testing in Psychiatry/Depression Market

- In November 2023, Myriad Genetics reported continued strong adoption of its GeneSight pharmacogenomic testing platform across psychiatric care settings in the United States. The platform supports personalized antidepressant selection by analyzing multiple gene–drug interactions, including CYP2D6 and CYP2C19 pathways, to guide treatment decisions in depression and anxiety disorders. Real-world clinical evidence has shown improved patient outcomes and reduced adverse drug reactions with its use. The solution is widely implemented in outpatient psychiatry clinics, reinforcing the growing role of commercial pharmacogenetic testing in North American mental healthcare

- In July 2023, the U.S. FDA issued a safety communication warning about unapproved pharmacogenetic tests being marketed for predicting antidepressant response. The agency highlighted concerns regarding limited clinical validity and the potential risk of misleading treatment decisions in psychiatric care. It clarified that only specific gene–drug interactions have sufficient scientific evidence for clinical use and encouraged healthcare providers to rely on validated guidelines such as CPIC recommendations. This regulatory action reinforced evidence-based adoption and improved quality standards in pharmacogenetics testing across North America

- In May 2023, the Clinical Pharmacogenetics Implementation Consortium (CPIC), a leading U.S.-based guideline authority, updated its recommendations for CYP2D6 and CYP2C19 gene–drug interactions in antidepressant therapy. The updated guidelines refined dosing and prescribing strategies for commonly used SSRIs and tricyclic antidepressants, improving clinical decision-making in treatment-resistant depression and anxiety disorders. These updates have been widely integrated into electronic health record systems and clinical workflows across North America, strengthening standardized use of pharmacogenetic testing in psychiatry

- In October 2022, the U.S. Food and Drug Administration (FDA) updated its Table of Pharmacogenomic Biomarkers in Drug Labeling, reinforcing the clinical importance of gene–drug interactions in psychiatric medications. The update included multiple antidepressants and psychotropic drugs linked to CYP2D6 and CYP2C19 metabolic pathways, helping standardize genetic information used in prescribing decisions. This regulatory action strengthened clinician confidence in pharmacogenetic testing for depression and mood disorders and supported broader adoption of precision psychiatry practices across the region

- In May 2021, the U.S. National Institutes of Health (NIH) All of Us Research Program achieved a major milestone by returning genomic data to more than 100,000 participants, significantly strengthening the foundation for precision medicine research relevant to psychiatric pharmacogenetics. The initiative integrates genomic, clinical, and behavioral data, enabling researchers to better understand genetic variability influencing antidepressant response and psychiatric drug metabolism, particularly involving CYP450 enzyme pathways. This large-scale dataset is helping improve diversity in genomic research and supporting the development of more accurate pharmacogenetic applications in depression and anxiety treatment

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.