North America Pipe Insulation Market

Market Size in USD Billion

USD

5.52 Billion

USD

7.84 Billion

2025

2033

USD

5.52 Billion

USD

7.84 Billion

2025

2033

| 2026 - 2033 | |

| USD 5.52 Billion | |

| USD 7.84 Billion | |

| % | |

|

North America Pipe Insulation Market Overview

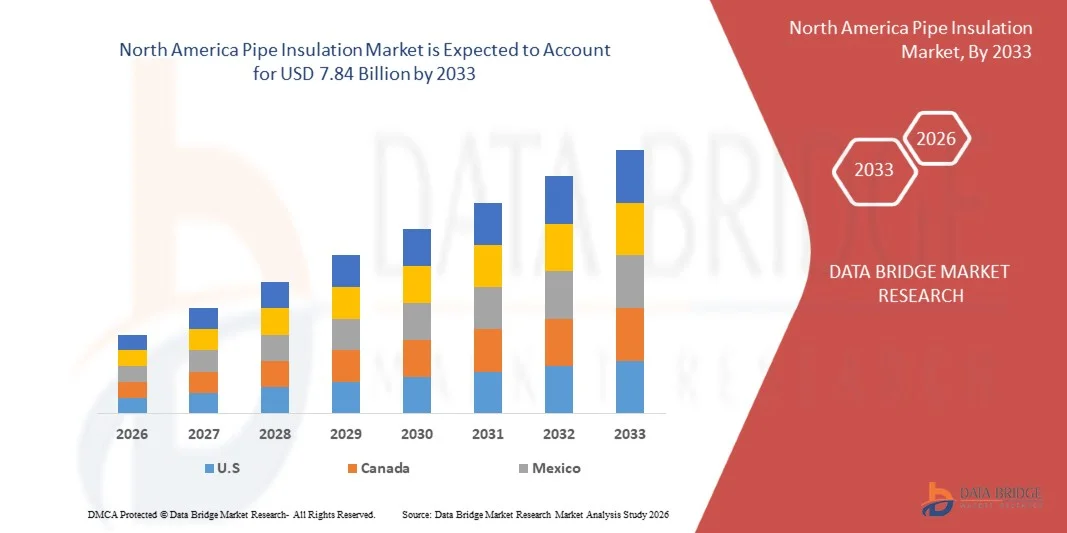

The North America pipe insulation market was valued at USD 5.52 billion in 2025 and is projected to reach USD 7.84 billion by 2033, growing at a CAGR of 4.50% from 2026 to 2033. The market is witnessing steady growth driven by increasing demand for energy-efficient infrastructure, rising adoption of HVAC systems, and growing emphasis on thermal efficiency across industrial, commercial, and residential sectors. Expanding construction activities and stringent energy conservation regulations are further supporting the adoption of advanced pipe insulation materials worldwide.

The increasing focus on reducing energy losses in heating and cooling systems, along with the need to prevent condensation, corrosion, and pipe freezing, is encouraging industries to invest in high-performance insulation solutions. Materials such as fiberglass, elastomeric foam, mineral wool, and polyurethane foam are gaining significant traction due to their superior thermal and acoustic insulation properties. In addition, rapid industrialization, growth in oil & gas and chemical processing industries, and rising investments in sustainable building infrastructure are accelerating the deployment of pipe insulation systems across both developed and emerging economies.

Key Market Trends & Insights

- U.S. dominated the North America pipe insulation market with the largest revenue share of approximately 76.4% in 2025, supported by strong demand from commercial construction, oil and gas infrastructure, district energy systems, and industrial energy efficiency modernization projects.

- Canada is expected to be the fastest-growing region, recording a CAGR of approximately 5.9% from 2026 to 2033. Growth is driven by expanding green building initiatives, increasing deployment of district heating infrastructure, and rising investments in cold chain logistics and energy-efficient HVAC systems.

- The Rigid Insulation Products segment held the largest market revenue share of approximately 34.6% in 2025 driven by its extensive adoption across industrial piping systems, district heating infrastructure, and commercial HVAC applications. These products are widely preferred because of their superior thermal resistance, durability, and ability to withstand high-pressure industrial environments while minimizing long-term energy losses.

- The Stone Wool Insulation Covers segment is projected to register the fastest growth at a CAGR of 6.4% from 2026 to 2033, driven by increasing demand for fire-resistant and environmentally sustainable insulation solutions across North America’s commercial construction and industrial sectors. Rising investments in green building renovation programs and stricter fire safety regulations are accelerating segment expansion across countries.

- The Fiberglass segment held the largest market revenue share of approximately 28.9% in 2025 driven by its cost-effectiveness, high thermal efficiency, and widespread deployment across commercial buildings, industrial plants, and district energy systems. Fiberglass insulation materials are extensively used because of their lightweight structure, corrosion resistance, and ease of installation in both hot and cold insulation applications.

- The Elastomeric Foam segment is projected to register the fastest growth at a CAGR of 7.1% from 2026 to 2033, driven by increasing demand for moisture-resistant and flexible insulation materials in HVAC, refrigeration, and pharmaceutical applications. Growing adoption in energy-efficient buildings and cold chain infrastructure modernization projects is supporting rapid segment growth across North America.

- The Hot Insulation segment held the largest market revenue share of approximately 61.3% in 2025 driven by strong demand from industrial manufacturing, district heating systems, and power generation facilities requiring efficient thermal retention and process temperature stability. Hot insulation systems are widely utilized across chemical processing plants and energy infrastructure to reduce thermal losses and improve operational efficiency.

- The Cold Insulation segment is projected to register the fastest growth at a CAGR of 6.8% from 2026 to 2033, driven by expanding refrigeration infrastructure, pharmaceutical cold storage facilities, and energy-efficient HVAC installations across North America. Increasing investments in food processing and temperature-controlled logistics are accelerating adoption of advanced cold insulation systems with improved condensation resistance.

- The Building and Construction segment held the largest market revenue share of approximately 31.7% in 2025 driven by rising investments in energy-efficient residential and commercial infrastructure projects across North America. Increasing implementation of green building standards and building energy performance regulations is accelerating demand for advanced pipe insulation systems in HVAC and plumbing networks.

- The Energy and Power segment is projected to register the fastest growth at a CAGR of 7.3% from 2026 to 2033, driven by modernization of district heating networks, expansion of renewable energy infrastructure, and increasing investments in thermal power efficiency improvement projects. Growing deployment of insulated piping systems in biomass plants, geothermal facilities, and hydrogen infrastructure projects is supporting rapid segment expansion across North America.

Market Size & Forecast

- Market Value (2025): USD 5.52 Billion

- Expected Market Value (2033): USD 7.84 Billion

- Forecast CAGR (2026–2033): 4.50%

- Leading Country in 2025: North America

- Fastest Growing Country: Asia-Pacific

Report Scope and North America Pipe Insulation Market Segmentation

|

Attributes |

North America Pipe Insulation Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

• Owens Corning (U.S.) |

|

Market Opportunities |

• Rising Adoption Of Energy-Efficient Building Infrastructure • Increasing Investments In Industrial And Commercial HVAC Systems |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

North America Pipe Insulation Market Trends

Trend: Rising Adoption Of Energy-Efficient Building Retrofits And Advanced Industrial Thermal Management Systems

Increasing demand for energy-efficient, durable, and environmentally sustainable thermal insulation technologies across commercial construction, industrial manufacturing, and energy infrastructure sectors. Conventional uninsulated piping systems result in substantial thermal energy losses, higher operational costs, and increased carbon emissions, encouraging industries and building operators to adopt advanced insulation solutions with improved thermal resistance and moisture protection capabilities.

In modern commercial buildings, developers are increasingly integrating high-performance pipe insulation systems, For instance elastomeric foam and fiberglass insulation, to improve HVAC efficiency, reduce energy consumption, and support green building certification standards. In industrial facilities, these insulation systems are being widely deployed to maintain process temperatures, prevent condensation, and improve operational reliability across chemical plants, refineries, and food processing units.

The rapid expansion of district energy infrastructure and energy-efficient renovation programs across North America is also increasing demand for durable and fire-resistant insulation systems capable of operating in extreme environmental conditions. In addition, pharmaceutical and cold chain logistics sectors continue to rely on advanced pipe insulation technologies, such as polyurethane and mineral wool systems, because of their ability to maintain precise temperature control in temperature-sensitive operations. Growing industry validation through large-scale retrofit projects in 2025 across the U.S. and Canada integrating advanced pipe insulation materials into aging commercial infrastructure demonstrated reductions of nearly 14–19% in heating and cooling energy losses under continuous operational conditions.

Global North America Pipe Insulation Market Dynamics

Key Market Driver: Rising Investments In Energy-Efficient Infrastructure And Industrial Modernization

Industries and governments across North America are facing increasing regulatory and economic pressure to reduce energy consumption, lower greenhouse gas emissions, and improve infrastructure efficiency. Large quantities of thermal energy generated across HVAC systems, industrial pipelines, and district heating networks are commonly lost because of insufficient insulation, creating strong demand for advanced pipe insulation technologies capable of minimizing thermal transfer losses and improving system performance.

Industries such as oil and gas, chemical processing, food and beverage, and power generation are increasingly deploying advanced insulation systems to maintain process stability, improve worker safety, and reduce operational energy costs. Commercial building operators are actively upgrading insulation infrastructure, For instance in hospitals, airports, and data centers, to comply with stringent energy efficiency standards and sustainability targets.

Similarly, district energy operators and cold storage facilities are expanding insulation deployment to improve thermal efficiency while reducing dependence on energy-intensive climate control systems. Real-world infrastructure modernization projects in Texas and Ontario during 2024 integrating high-performance pipe insulation systems into industrial steam and chilled water networks demonstrated reductions of around 11–17% in operational thermal losses during continuous industrial operations.

Key Restraint/Challenge: High Material Costs And Complex Installation Requirements

Advanced pipe insulation systems often involve significant material and installation costs, particularly across large industrial plants, aging commercial buildings, and complex retrofit projects requiring customized insulation designs. The process of replacing existing insulation systems without interrupting industrial operations creates installation challenges and increases labor expenses, limiting adoption among small-scale industries and budget-sensitive infrastructure projects.

In addition, fluctuating prices of raw materials such as fiberglass, polyurethane foam, and mineral wool increase overall project costs, creating affordability concerns across construction and industrial sectors. Strict fire safety, environmental, and occupational safety regulations further increase certification and maintenance expenses for insulation manufacturers and contractors. Limited availability of skilled installation professionals for large-scale retrofitting applications also restricts rapid market expansion across older infrastructure networks.

Commercial facility benchmarking studies indicate that retrofitting industrial steam and chilled water pipelines, For instance in aging manufacturing plants across the U.S. Midwest, can increase insulation project costs by around 18–28% compared to new construction installations because of dismantling requirements, labor intensity, and operational downtime considerations.

Key Market Opportunity: Expansion Of Green Building Infrastructure And Cold Chain Networks

Modern commercial buildings, industrial facilities, and temperature-controlled logistics systems increasingly require advanced thermal insulation technologies capable of improving energy efficiency and supporting sustainability goals. Conventional piping systems often experience excessive heat transfer losses, condensation formation, and temperature instability, creating demand for durable insulation materials with low maintenance requirements and long operational lifespans.

Infrastructure developers and industrial operators are increasingly exploring advanced insulation systems, For instance for HVAC pipelines, refrigeration systems, and district energy networks, to improve energy conservation, reduce operating costs, and enhance infrastructure reliability. In cold chain logistics and pharmaceutical storage facilities, rising demand for temperature-sensitive transportation and storage systems is accelerating adoption of moisture-resistant and high-performance insulation materials.

In addition, advancements in aerogel insulation technologies and flexible foam-based insulation systems are improving thermal efficiency and installation flexibility, opening opportunities across renewable energy, healthcare, and semiconductor infrastructure markets throughout North America. Industrial facility modernization programs conducted in 2025 across California and Quebec reported reductions of around 13–18% in annual energy consumption after integrating upgraded pipe insulation systems into centralized HVAC and process piping networks.

North America Pipe Insulation Market Scope

The market is segmented on the basis of product type, material type, temperature, and application.

• By Product Type

On the basis of product type, the North America pipe insulation market is segmented into Rigid Insulation Products, Stone Wool Insulation Covers, Coating Material, Thin Films, Wraps, Foils and Others. The Rigid Insulation Products segment held the largest market revenue share of approximately 34.6% in 2025 driven by its extensive adoption across industrial piping systems, district heating infrastructure, and commercial HVAC applications. These products are widely preferred because of their superior thermal resistance, durability, and ability to withstand high-pressure industrial environments while minimizing long-term energy losses.

The Stone Wool Insulation Covers segment is projected to register the fastest growth at a CAGR of 6.4% from 2026 to 2033, driven by increasing demand for fire-resistant and environmentally sustainable insulation solutions across North America’s commercial construction and industrial sectors. Rising investments in green building renovation programs and stricter fire safety regulations are accelerating segment expansion countries.

• By Material Type

On the basis of material type, the North America pipe insulation market is segmented into Rockwool, Fiberglass, Polyurethane, Polystyrene, Polyolefin, Polypropylene, Polycarbonate, Polyvinyl Chloride, Urea Formaldehyde, Phenolic Foam, Elastomeric Foam and Others. The Fiberglass segment held the largest market revenue share of approximately 28.9% in 2025 driven by its cost-effectiveness, high thermal efficiency, and widespread deployment across commercial buildings, industrial plants, and district energy systems. Fiberglass insulation materials are extensively used because of their lightweight structure, corrosion resistance, and ease of installation in both hot and cold insulation applications.

The Elastomeric Foam segment is projected to register the fastest growth at a CAGR of 7.1% from 2026 to 2033, driven by increasing demand for moisture-resistant and flexible insulation materials in HVAC, refrigeration, and pharmaceutical applications. Growing adoption in energy-efficient buildings and cold chain infrastructure modernization projects is supporting rapid segment growth across North America.

• By Temperature

On the basis of temperature, the North America pipe insulation market is segmented into Hot Insulation and Cold Insulation. The Hot Insulation segment held the largest market revenue share of approximately 61.3% in 2025 driven by strong demand from industrial manufacturing, district heating systems, and power generation facilities requiring efficient thermal retention and process temperature stability. Hot insulation systems are widely utilized across chemical processing plants and energy infrastructure to reduce thermal losses and improve operational efficiency.

The Cold Insulation segment is projected to register the fastest growth at a CAGR of 6.8% from 2026 to 2033, driven by expanding refrigeration infrastructure, pharmaceutical cold storage facilities, and energy-efficient HVAC installations across North America. Increasing investments in food processing and temperature-controlled logistics are accelerating adoption of advanced cold insulation systems with improved condensation resistance.

• By Application

On the basis of application, the North America pipe insulation market is segmented into Building and Construction, Electronics, Chemical Industry, Energy and Power, Oil and Gas, Automotive, Transportation, Food and Beverage and Others. The Building and Construction segment held the largest market revenue share of approximately 31.7% in 2025 driven by rising investments in energy-efficient residential and commercial infrastructure projects across North America. Increasing implementation of green building standards and building energy performance regulations is accelerating demand for advanced pipe insulation systems in HVAC and plumbing networks.

The Energy and Power segment is projected to register the fastest growth at a CAGR of 7.3% from 2026 to 2033, driven by modernization of district heating networks, expansion of renewable energy infrastructure, and increasing investments in thermal power efficiency improvement projects. Growing deployment of insulated piping systems in biomass plants, geothermal facilities, and hydrogen infrastructure projects is supporting rapid segment expansion across North America.

North America Pipe Insulation Market Regional Analysis

U.S. North America Pipe Insulation Market Insight

The U.S. North America pipe insulation market captured the largest revenue share of approximately 76.4% in 2025 within North America, fueled by rising investments in energy-efficient commercial infrastructure and increasing modernization of industrial piping systems. Industries and building operators are increasingly prioritizing thermal efficiency, operational cost reduction, and compliance with stringent energy conservation regulations through the adoption of advanced pipe insulation solutions. The growing preference for sustainable construction materials, combined with strong demand for HVAC optimization and district energy systems, further propels market expansion. Moreover, the increasing integration of smart building technologies and high-performance insulation materials across healthcare facilities, data centers, and manufacturing plants is significantly contributing to the market’s growth.

Canada North America Pipe Insulation Market Insight

The Canada North America pipe insulation market is expected to witness significant growth from 2026 to 2033, driven by increasing investments in green building infrastructure and rising demand for energy-efficient heating and cooling systems across residential and commercial sectors. Canada’s extreme climatic conditions and strong focus on reducing energy consumption are encouraging widespread adoption of advanced pipe insulation systems for district heating, refrigeration, and industrial processing applications. The growing expansion of cold chain logistics infrastructure, combined with modernization of public infrastructure and sustainable construction initiatives, is further supporting market growth. In addition, increasing deployment of high-performance insulation materials across oil and gas facilities, food processing plants, and healthcare infrastructure is accelerating demand for durable and moisture-resistant thermal insulation solutions throughout the country.

North America Pipe Insulation Market Share

The North America Pipe Insulation industry is primarily led by well-established companies, including:

• Owens Corning (U.S.)

• Johns Manville (U.S.)

• CertainTeed Corporation (U.S.)

• Knauf Insulation, Inc. (U.S.)

• Raven Industries, Inc. (U.S.)

• Aspen Aerogels, Inc. (U.S.)

• Distribution International, Inc. (U.S.)

• Ideal Products of America, Inc. (U.S.)

• Proto Corporation (Canada)

• IIGM Corporation (U.S.)

• Fibrex Insulations Inc. (Canada)

• Firwin Corporation (Canada)

• Bay Insulation Systems, Inc. (U.S.)

• Shannon Global Energy Solutions, Inc. (U.S.)

• Polyguard Products, Inc. (U.S.)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

North America Pipe Insulation Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its North America Pipe Insulation Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as North America Pipe Insulation Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.