North America Protein Purification Isolation Market

Market Size in USD Billion

USD

6.60 Billion

USD

13.15 Billion

2025

2033

USD

6.60 Billion

USD

13.15 Billion

2025

2033

| 2026 - 2033 | |

| USD 6.60 Billion | |

| USD 13.15 Billion | |

| % | |

|

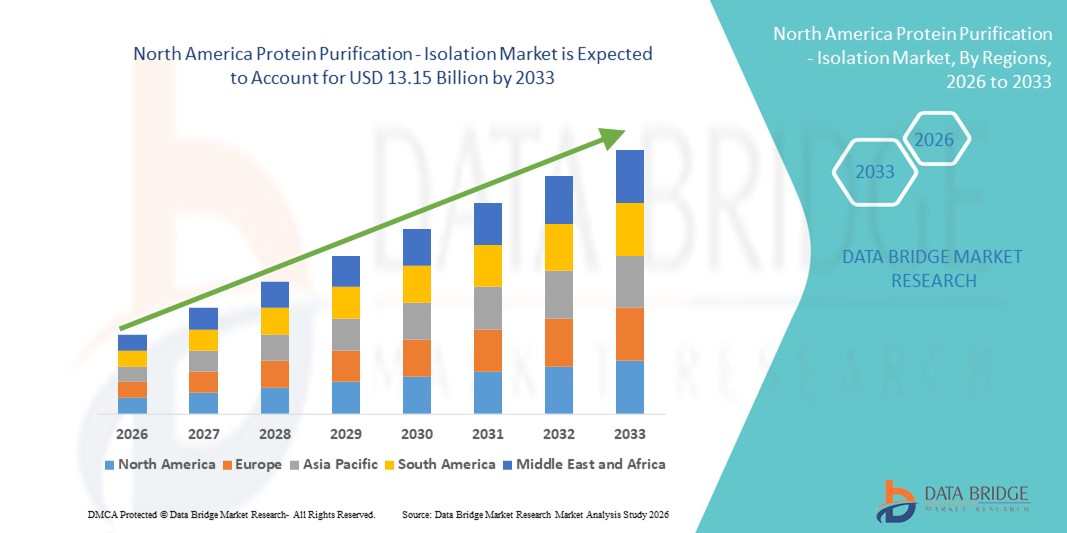

North America Protein Purification - Isolation Market Size

- The North America protein purification - isolation market size was valued at USD 6.60 billion in 2025 and is expected to reach USD 13.15 billion by 2033, at a CAGR of 9.00% during the forecast period

- The market growth is largely fueled by rapid advancements in biopharmaceutical R&D, increasing demand for high‑purity proteins in therapeutic development, proteomics, and drug screening, and the strong presence of research institutions and biotechnology firms in North America

- Furthermore, rising investments in cutting‑edge purification technologies, integration of advanced techniques such as ultrafiltration and chromatography, and growing needs for precise and efficient protein isolation solutions in academic, clinical, and industrial settings are driving demand. These converging factors are accelerating the adoption of protein purification solutions, thereby significantly boosting the region’s market growth

North America Protein Purification - Isolation Market Analysis

- Protein purification and isolation technologies, enabling the separation and concentration of specific proteins from complex biological samples, are increasingly critical components of modern biopharmaceutical research, drug development, and proteomics studies in both academic and industrial settings due to their accuracy, scalability, and compatibility with advanced analytical platforms

- The escalating demand for protein purification solutions is primarily driven by the growth of biopharmaceutical R&D, increasing focus on therapeutic protein development, rising proteomics research, and the need for high-purity proteins in drug discovery and diagnostic applications

- The United States dominated the protein purification- isolation market with the largest revenue share of 88.5% in 2025, characterized by a strong presence of leading biotechnology and life sciences companies, extensive research infrastructure, and high adoption of advanced purification technologies, with substantial growth in protein purification workflows across academic institutions, contract research organizations, and biopharmaceutical manufacturing, driven by innovations in chromatography, ultrafiltration, and automated purification systems

- Canada is expected to be the fastest growing country in the protein purification- isolation market during the forecast period due to increasing investment in life sciences research, expansion of biopharmaceutical manufacturing, and rising proteomics and biotechnology research activities

- Chromatography segment dominated the protein purification – isolation market with a market share of 45.3% in 2025, driven by its high resolution, scalability, and established reputation for delivering high-purity proteins across diverse research and industrial applications

Report Scope and North America Protein Purification - Isolation Market Segmentation

|

Attributes |

North America Protein Purification - Isolation Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

North America Protein Purification - Isolation Market Trends

Advancements Through Automation and High-Throughput Systems

- A significant and accelerating trend in the North America protein purification – isolation market is the growing adoption of automated and high-throughput purification systems, which are enhancing workflow efficiency and reproducibility in research and biopharmaceutical manufacturing

- For instance, Tecan’s Freedom EVO liquid handling platform allows fully automated protein purification workflows, reducing manual intervention and increasing throughput for proteomics and antibody research

- Integration of robotics and automated chromatography systems enables laboratories to perform complex purification protocols with minimal human error and faster turnaround times. For instance, Agilent’s automated protein purification systems streamline sample processing while maintaining high purity and yield

- The combination of automation and high-throughput platforms facilitates scalability, allowing researchers and biopharma companies to handle increasing sample volumes without compromising quality

- For instance, Cytiva has developed automated chromatography and filtration solutions with software integration for optimized protein isolation

- Increasing integration of data analytics and AI-driven process monitoring in protein purification is improving process optimization, reducing trial-and-error experiments, and enabling predictive maintenance. For instance, Bio-Rad’s advanced process control software allows real-time monitoring and optimization of protein purification runs, enhancing reproducibility and efficiency

- The demand for automated and high-throughput purification systems is growing rapidly across both academic and industrial sectors, as organizations increasingly prioritize efficiency, reproducibility, and scalability in protein purification processes

North America Protein Purification - Isolation Market Dynamics

Driver

Rising Demand from Biopharmaceutical R&D and Therapeutic Protein Development

- The increasing focus on biopharmaceutical research, therapeutic protein development, and proteomics studies is a significant driver for the heightened demand for protein purification and isolation solutions

- For instance, in March 2025, Thermo Fisher Scientific expanded its chromatography and filtration portfolio to support high-purity monoclonal antibody production in contract manufacturing organizations

- As pharmaceutical and biotech companies develop complex biologics, precise and efficient protein purification becomes essential, driving adoption of advanced purification technologies

- Furthermore, the growing emphasis on personalized medicine and targeted therapies is increasing the need for highly purified proteins in research and clinical applications

- High demand for high-throughput, scalable, and reproducible purification workflows in academic, industrial, and contract research laboratories is further propelling market growth. For instance, Sartorius introduced integrated protein purification platforms that reduce processing time and increase yield, catering to the rising demand for rapid biologics development

- Increasing collaborations between research institutions and biopharmaceutical companies to accelerate biologics research is creating additional demand for efficient and reliable protein purification systems

- For instance, Genentech and academic partners utilize automated purification platforms to streamline antibody research and therapeutic protein production

Restraint/Challenge

High Costs and Complex Technical Requirements

- Concerns regarding the high cost and technical complexity of advanced protein purification systems pose a significant challenge to broader market adoption. Sophisticated chromatography, ultrafiltration, and automated systems often require specialized expertise for operation and maintenance

- For instance, smaller research laboratories may face budget constraints when investing in high-end purification platforms such as Cytiva ÄKTA systems

- Addressing these challenges through user-friendly interfaces, modular systems, and cost-effective solutions is crucial for increasing accessibility and adoption. For instance, some emerging vendors now offer compact, semi-automated purification platforms suitable for small-scale labs

- In addition, maintaining consistent protein quality and yield across complex workflows requires significant technical know-how, which can limit adoption among organizations with limited trained personnel

- Overcoming these challenges through simplified system design, technical support, and training programs will be vital for sustained market growth. For instance, companies such as Bio-Rad provide extensive training and technical support programs to help laboratories optimize system usage and reduce operational errors

- High operational costs associated with consumables, buffers, and maintenance can also restrict adoption, particularly in smaller academic or early-stage biotech labs

- For instance, Sigma-Aldrich offers cost-effective purification kits and consumables to mitigate some of the financial burden on smaller research organizations

North America Protein Purification - Isolation Market Scope

The market is segmented on the basis of product, technology, application, and end user.

- By Product

On the basis of product, the North America protein purification – isolation market is segmented into instruments and consumables. The instruments segment dominated the market with the largest market revenue share in 2025, driven by high adoption of chromatography systems, ultrafiltration units, and automated purification platforms in pharmaceutical and biotechnological industries. Instruments provide high precision, reproducibility, and scalability, which are critical for therapeutic protein production and research applications. Their ability to integrate with automated and high-throughput workflows enhances laboratory efficiency and reduces manual errors. Leading instrument providers also offer advanced monitoring and software control features, enabling consistent purification outcomes. Institutions with complex purification needs prefer instruments for long-term research and industrial workflows. Continuous innovations and modular designs in instrument platforms further support their dominance in the market.

The consumables segment is expected to witness the fastest growth from 2026 to 2033, fueled by increasing demand for chromatography resins, filters, membranes, and kits in both academic and industrial laboratories. Consumables are essential for routine purification processes and are replaced frequently, creating recurring revenue streams for manufacturers. Rising biologics R&D, proteomics research, and small-scale therapeutic protein production are driving this growth. Consumables also enable laboratories to implement scalable processes without large upfront capital expenditure on instruments. The availability of pre-packed columns, kits, and ready-to-use reagents enhances ease of use and encourages adoption.

- By Technology

On the basis of technology, the market is segmented into ultrafiltration, precipitation, centrifugation, chromatography, electrophoresis, dialysis and diafiltration, western blotting, and others. The chromatography segment dominated the market in 2025 with a market share of 45.3% due to its high resolution, scalability, and ability to deliver high-purity proteins for research and therapeutic applications. Chromatography is widely employed for monoclonal antibody purification, protein therapeutics, and biomarker isolation. Its adaptability across different scales—from lab to industrial production—makes it indispensable for pharmaceutical and biopharmaceutical R&D. The precision, reproducibility, and ability to separate complex mixtures efficiently drive its strong adoption. Chromatography systems are often integrated with automated platforms, increasing throughput and reducing human error. Continued innovation in resin chemistry and column technology further consolidates its market leadership.

The ultrafiltration segment is expected to witness the fastest growth from 2026 to 2033, driven by its importance in protein concentration, buffer exchange, and purification workflows. Ultrafiltration is crucial for large-scale biologics production and downstream processing in contract research organizations and biotech companies. Its compatibility with automated and high-throughput purification platforms enhances efficiency. Increasing demand for high-concentration therapeutic proteins, monoclonal antibodies, and vaccines accelerates adoption. Ultrafiltration also reduces processing time and improves yield, making it attractive for industrial-scale purification. Growing applications in proteomics and diagnostics further support the rapid market expansion.

- By Application

On the basis of application, the market is segmented into drug screening, target identification, biomarker discovery, protein-protein interaction studies, protein therapeutics, and disease diagnosis and monitoring. The protein therapeutics segment dominated the market in 2025, driven by rising demand for monoclonal antibodies, vaccines, and recombinant proteins for treatment of chronic and rare diseases. Protein therapeutics require high-purity proteins with consistent quality, making efficient purification critical. Pharmaceutical companies rely heavily on advanced chromatography and automated purification platforms for this purpose. The growth of personalized medicine and targeted biologics further fuels the segment. Contract research organizations and biopharmaceutical manufacturers are increasing investment in protein therapeutic production capabilities. Regulatory requirements for purity, potency, and safety also strengthen the demand for reliable purification workflows in this application.

The biomarker discovery segment is expected to witness the fastest growth from 2026 to 2033, fueled by increasing research in proteomics, diagnostics, and early disease detection. Biomarker discovery requires isolation of specific proteins from complex biological samples for identification and validation. High-throughput and automated purification technologies accelerate this process and enable large-scale screening. Academic and clinical research institutes are investing in advanced purification workflows to support biomarker-based diagnostic development. The rise of personalized medicine and liquid biopsy research further drives adoption.

- By End User

On the basis of end user, the market is segmented into pharmaceutical and biotechnological industries, contract research organizations, academic and research institutes, and hospital and diagnostic centers. The pharmaceutical and biotechnological industries segment dominated the market in 2025 due to high demand for purified proteins for drug development, monoclonal antibody production, and therapeutic protein manufacturing. These industries require scalable, reproducible, and high-purity purification workflows to meet regulatory standards. Integration of automated instruments and chromatography systems helps streamline large-scale protein production. Strategic partnerships with instrument and consumable providers further strengthen their market position. Continuous biologics research and development investments maintain robust demand from this segment. Companies are increasingly adopting integrated purification platforms to improve efficiency and product quality.

The academic and research institutes segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing proteomics research, biomarker discovery, and protein interaction studies. Research institutions are adopting both consumables and small-scale automated instruments to support high-throughput workflows. Government grants, biotechnology research funding, and collaborations with industry partners are fueling market expansion. Easy-to-use purification kits and modular platforms support rapid adoption in laboratories. The trend towards high-throughput protein analysis and reproducible experimental results is driving growth in academic and research settings.

North America Protein Purification - Isolation Market Regional Analysis

- The United States dominated the protein purification- isolation market with the largest revenue share of 88.5% in 2025, characterized by a strong presence of leading biotechnology and life sciences companies, extensive research infrastructure, and high adoption of advanced purification technologies, with substantial growth in protein purification workflows across academic institutions

- Researchers and industry professionals in the region highly value the precision, scalability, and reproducibility offered by modern protein purification systems, as well as their seamless integration with downstream applications such as drug development, biomarker discovery, and proteomics studies

- This widespread adoption is further supported by substantial R&D investments, government funding, highly skilled technical personnel, and collaborations between academic institutions and biopharmaceutical companies, establishing the United States as the central hub for protein purification and isolation activities in North America

The U.S. Protein Purification – Isolation Market Insight

The U.S. protein purification – isolation market captured the largest revenue share of 88.5% in 2025 within North America, fueled by the strong presence of biotechnology and pharmaceutical companies and the extensive adoption of advanced purification technologies. Researchers and manufacturers increasingly prioritize high-purity proteins for therapeutic protein development, monoclonal antibody production, and proteomics research. The growing trend of automated and high-throughput purification platforms, combined with the demand for reproducible and scalable workflows, further propels the market. Moreover, integration with analytical platforms and software for real-time monitoring enhances process efficiency and reliability. Strategic collaborations between academic institutions and industry leaders also contribute significantly to market expansion.

Canada Protein Purification – Isolation Market Insight

The Canada protein purification – isolation market is projected to grow at a substantial CAGR throughout the forecast period, primarily driven by increasing investments in life sciences research and biopharmaceutical manufacturing. Rising proteomics and biomarker discovery initiatives are fostering the adoption of protein purification systems in both academic and industrial laboratories. Canadian researchers value the precision, reproducibility, and flexibility offered by chromatography, ultrafiltration, and automated purification platforms. Government funding, biotechnology grants, and collaboration with pharmaceutical companies are supporting market growth. In addition, the integration of high-throughput systems is enabling faster research outputs and improved efficiency.

Mexico Protein Purification – Isolation Market Insight

The Mexico protein purification – isolation market is expected to expand at a notable CAGR during the forecast period, driven by the growing focus on contract research organizations (CROs) and academic research centers. Increased outsourcing of protein purification and analytical services by international pharmaceutical and biotech companies is fueling demand. Mexico’s expanding biotechnology ecosystem, coupled with rising research funding, encourages adoption of automated purification systems and consumables. The demand for cost-effective and modular purification solutions is rising in small and mid-scale laboratories. Moreover, collaborations with global instrument and consumable providers support technology transfer and process optimization.

North America Protein Purification - Isolation Market Share

The North America Protein Purification - Isolation industry is primarily led by well-established companies, including:

- Thermo Fisher Scientific Inc., (U.S.)

- Bio Rad Laboratories, Inc., (U.S.)

- Waters Corporation (U.S.)

- QIAGEN (Netherlands)

- Agilent Technologies, Inc., (U.S.)

- New England Biolabs, Inc., (U.S.)

- GE Healthcare (U.S.)

- Promega Corporation, (U.S.)

- Norgen Biotek Corp., (Canada)

- Abcam plc, (U.K.)

- Purolite Corporation, (U.S.)

- BioVision, Inc., (U.S.)

- PerkinElmer, Inc., (U.S.)

- 3M Purification Inc., (U.S.)

- MilliporeSigma (U.S.)

- Tosoh Bioscience, (Japan)

- GenScript Biotech Corp., (China)

- Takara Bio Inc., (Japan)

- Chromatrap (U.K.)

- Revvity, Inc., (U.S.)

What are the Recent Developments in North America Protein Purification - Isolation Market?

- In April 2025, Waters Corporation expanded its Alliance™ iS Bio HPLC product line by integrating a photodiode array (PDA) detector, significantly enhancing spectral analysis capabilities for biopharma development and QC labs, improving sensitivity and operational efficiency

- In December 2024, Repligen Corporation launched its AVIPure® dsRNA Clear OPUS® columns, a groundbreaking affinity chromatography solution designed to simplify and enhance the removal of double‑stranded RNA (dsRNA) impurities during mRNA therapeutic and vaccine production, improving purity and workflow efficiency

- In April 2024, Waters Corporation officially launched the Alliance™ iS Bio High Performance Liquid Chromatography (HPLC) System, a next‑generation chromatography platform that reduces common lab errors and increases efficiency for biopharmaceutical QC laboratories

- In June 2023, Waters Corporation and Sartorius expanded their collaboration to deliver integrated bioanalytical solutions for downstream biomanufacturing, combining chromatographic analytics with multi‑column processing to enhance the speed and quality of protein purification workflows

- In March 2023, Waters Corporation introduced the Alliance™ iS HPLC System, an intelligent HPLC platform that integrates proactive error detection and enhanced automation to help labs reduce up to 40% of common chromatographic errors in biopharmaceutical separation workflow

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.