North America Silicone Textile Chemicals Market

Market Size in USD Billion

USD

4.89 Billion

USD

7.25 Billion

2024

2032

USD

4.89 Billion

USD

7.25 Billion

2024

2032

| 2025 - 2032 | |

| USD 4.89 Billion | |

| USD 7.25 Billion | |

| % | |

|

Silicone Textile Chemicals Market Size

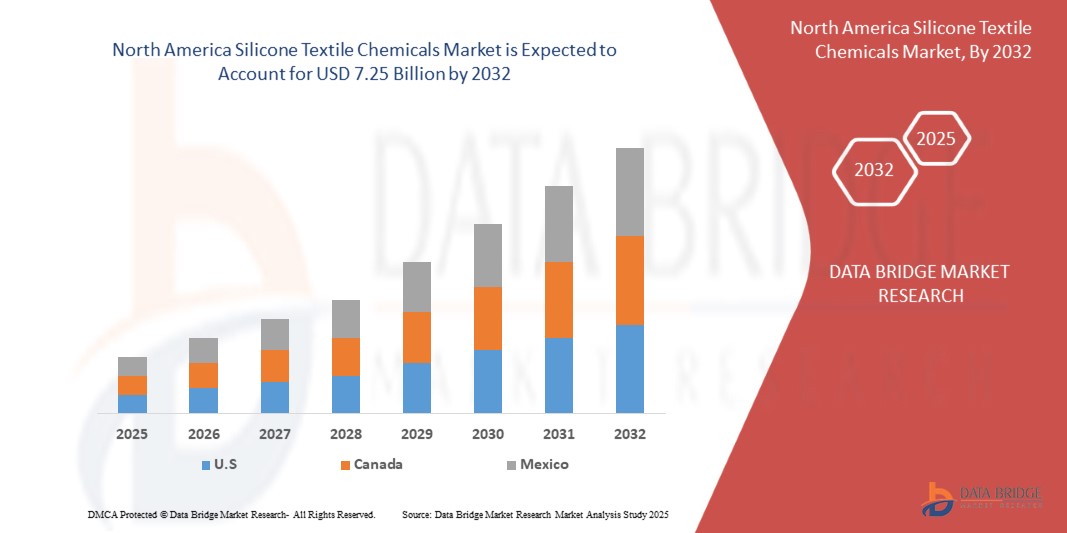

- The North America Silicone Textile Chemicals market size was valued at USD 4.89 billion in 2024 and is expected to reach USD 7.25 billion by 2032, at a CAGR of 5.9% during the forecast period

- The market growth is largely fueled by rising demand for high‑performance functional textiles in automotive, protective apparel, and healthcare sectors, driving the adoption of silicone‑based treatments for water repellency, softness, and durability

- Furthermore, stringent environmental regulations, a shift toward premium technical fabrics, and ongoing innovations in eco‑friendly silicone chemistries are accelerating the uptake of silicone textile chemicals, thereby significantly boosting the industry’s expansion

Silicone Textile Chemicals Market Analysis

- Silicone textile chemicals, offering advanced water‑repellent, softening, and durability enhancements for fabrics, are increasingly vital in high‑performance applications such as automotive interiors, protective apparel, healthcare textiles, and fashion, due to their ability to impart multifunctional properties without compromising fabric hand feel.

- The escalating demand for silicone textile chemicals is primarily fueled by the rapid expansion of technical textiles, stringent environmental regulations favoring eco‑friendly finishings, and a rising preference among consumers and manufacturers for high‑performance, long‑lasting textile treatments.

- U.S. dominates the Silicone Textile Chemicals market with the largest revenue share of 40.01% in 2025, characterized by strong automotive and healthcare sectors, substantial R&D investments in functional fabrics, and a robust presence of key industry players.

- U.S. is expected to be the fastest growing region in the Silicone Textile Chemicals market during the forecast period due to increasing urbanization, expanding textile and apparel manufacturing hubs, rising disposable incomes, and strong government support for sustainable and high‑tech textile production.

- The Silicon Softeners segment is expected to dominate the Silicone Textile Chemicals market with a market share of 49.21% in 2025, driven by its established reputation for protecting fabrics against moisture and stains, compatibility with diverse textile substrates, and ease of integration into existing finishing lines

Report Scope and Silicone Textile Chemicals Market Segmentation

|

Attributes |

Silicone Textile Chemicals Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Silicone Textile Chemicals Market Trends

“Shift Toward Sustainable and Bio‑Based Silicone Chemistries”

- A significant and accelerating trend in the North America Silicone Textile Chemicals market is the growing transition from petroleum‑derived silicones to bio‑based and green‑chemistry formulations. Manufacturers are developing renewable‑feedstock silanes and polysiloxanes that reduce carbon footprint and meet stringent eco‑certification standards.

- For instance, leading suppliers such as Dow and Wacker have introduced vegetable‑oil‑derived silicone softeners and low‑VOC emulsions that deliver comparable water‑repellency and fabric hand feel to conventional products, while earning sustainability credentials for textile brands.

- These bio‑based silicones maintain key performance attributes—such as durability, softness, and stain resistance—without relying on fossil resources, addressing consumer demand for eco‑friendly apparel, home textiles, and technical fabrics.

- The shift is reinforced by major retailers and fashion labels adopting closed‑loop supply chains and requiring LCA‑verified finishing agents, prompting finishers to integrate renewable silicone chemistries into existing production lines.

- This focus on sustainable silicone technologies is reshaping industry expectations, as brands seek both high performance and positive environmental impact—driving further R&D in biodegradable polymer backbones and water‑based delivery systems.

- The demand for bio‑based silicone textile chemicals is rising rapidly across apparel, automotive interiors, protective apparel, and home furnishing sectors, as manufacturers and end‑users alike prioritize circular‑economy solutions and regulatory compliance.

Silicone Textile Chemicals Market Dynamics

Driver

“Rising Demand for High‑Performance and Sustainable Textiles”

- The increasing need for fabrics that combine superior performance—such as water repellency, durability, and comfort—with eco‑friendly credentials is a significant driver for the growth of the North America Silicone Textile Chemicals market. Manufacturers and brands are under pressure to deliver high‑function textiles that meet stringent environmental and consumer expectations.

- For instance, in March 2024, Dow unveiled its GreenSil™ Bio‑Derived Softener line, offering silicone‑based treatments sourced from renewable feedstocks that deliver comparable softness and water‑repellency to traditional chemistries while reducing carbon footprint.

- As apparel, automotive, and home‑textile producers seek to differentiate through premium, sustainable offerings, silicone chemistries that impart long‑lasting performance without toxic byproducts have become essential.

- Furthermore, regulatory pressures—such as state‑level restrictions on per‑ and polyfluoroalkyl substances (PFAS)—and retailer sustainability mandates are accelerating the shift to low‑VOC, bio‑based silicone finishes.

- The ability to enhance fabric functionality (e.g., stain resistance, softness, UV protection) while supporting circular‑economy initiatives makes silicone textile chemicals a preferred solution across multiple end‑use sectors, thereby propelling market expansion throughout North America.

Restraint/Challenge

“Volatile Raw Material Costs and Supply Chain Disruptions”

- The frequent fluctuations in silicone monomer and specialty feedstock prices, coupled with global supply chain bottlenecks, pose a significant challenge to North America’s silicone textile chemicals market. Manufacturers face unpredictability in input costs and lead times, undermining production planning and pricing stability.

- For instance, in February 2024, Wacker Chemie AG announced a 15 % increase in prices for key methylchlorosilane intermediates, citing upstream capacity constraints and logistics delays—a move that rippled through textile finishers and converters across the region.

- These cost pressures force finishers to either absorb higher expenses—squeezing already-thin margins—or pass increases to apparel and home‑textile brands, risking volume losses in a competitive marketplace.

- Moreover, tightening environmental and safety regulations on volatile organic compound (VOC) emissions during silicone processing add compliance costs and operational complexity for chemical suppliers and textile mills alike.

- Overcoming these challenges through strategies such as diversified feedstock sourcing, improved demand forecasting, and strategic vertical integration will be essential for stabilizing supply, controlling costs, and sustaining market growth.

Silicone Textile Chemicals Market Scope

The market is segmented on the basis of type, form, silicone technology, silicone modifications, textile type, and application.

- By Type

On the basis of type, the Silicone Textile Chemicals market is segmented into Silicon Softeners, Micro Emulsion Silicon, and Others. The Silicon Softeners segment dominates the market with the largest revenue share of 38.6% in 2025, attributed to their widespread use in improving hand feel, softness, and smoothness in textile applications. Their compatibility with various textile finishing processes and fabric types makes them the preferred choice across apparel and home furnishing sectors.

The Micro Emulsion Silicon segment is anticipated to witness the fastest CAGR of 20.4% from 2025 to 2032, driven by its ability to offer superior softness, durability, and fabric surface smoothness while enabling lower dosage requirements. Their increasing adoption in premium textile processing, especially for technical textiles, is further boosting this segment's growth..

- By Form

On the basis of form, the market is categorized into Fluids, Emulsions, and Antifoams. The Emulsions segment held the largest market share in 2025, due to their ease of use in wet textile processing systems, better dispersion properties, and consistent finishing performance.

The Fluids segment is expected to grow at a CAGR from 2025 to 2032, owing to their increasing usage in specialized finishing applications that require deeper fiber penetration, and in high-performance textiles requiring long-lasting softness and flexibility.

- By Silicon Technology

On the basis of silicone technology, the market is segmented into Polydimethylsiloxanes (PDMS) and Special Silicone Fluids. Polydimethylsiloxanes dominate with a market share of 47.3% in 2025, due to their versatile properties such as thermal stability, water repellency, and compatibility with various fabric types. Their low surface tension makes them ideal for softening and lubricating applications in textiles.

Special Silicone Fluids are projected to be the fastest-growing segment, expanding at a CAGR during the forecast period, spurred by growing demand for tailored finishing solutions in high-performance and technical textile applications.

- By Silicone Modifications

On the basis of silicone modifications, the market is segmented into Methyl Group, Amino Group, Hydrophilic Group, Hydrogen Group, and Other Organo Modifications. The Amino Group modification segment leads with the largest market share of 35.8% in 2025, supported by its significant role in enhancing softness, lubricity, and fabric drape, particularly in garments and home textiles.

The Hydrophilic Group segment is expected to grow fastest, at a CAGR from 2025 to 2032, driven by increasing demand for breathable, moisture-wicking, and quick-dry textiles used in activewear and technical fabrics.

- By Textile Type

On the basis of textile type, the market is segmented into Component Fibers, Synthetic Fibers, and Inorganic Fibers. Synthetic Fibers account for the largest revenue share of 49.5% in 2025, attributed to their high volume production and the extensive use of silicone chemicals in enhancing fiber properties like softness, elasticity, and water repellency.

Inorganic Fibers are projected to grow rapidly at a CAGR mainly due to their rising use in technical and industrial textiles where silicone finishes provide heat resistance and mechanical durability.

- By Application

On the basis of application, the market is segmented into Apparel, Home and Office Furnishing, Technical Textiles, and Others. The Apparel segment holds the largest share of 40.7% in 2025, driven by increased consumer preference for high-comfort, premium-feel clothing. Silicone textile chemicals are widely used in garments to improve softness, wrinkle resistance, and color retention.

The Technical Textiles segment is expected to witness the fastest CAGR from 2025 to 2032, due to growing industrial and performance-based applications where silicone-based finishes enhance fabric durability, flexibility, and resistance to extreme environmental conditions.

Silicone Textile Chemicals Market Country Analysis

- North America dominates the Silicone Textile Chemicals market with the largest revenue share of 40.01% in 2024, driven by increasing demand from the apparel, home furnishing, and technical textile industries, alongside advancements in textile finishing technologies.

- Consumers and manufacturers in the region are increasingly prioritizing high-performance fabrics that offer superior softness, durability, and functional benefits such as moisture management and wrinkle resistance.

- The market is further bolstered by well-established textile production infrastructure, robust R&D activities, and rising investments in sustainable and eco-friendly chemical solutions that align with regulatory standards and consumer expectations.

U.S. Silicone Textile Chemicals Market Insight

The U.S. Silicone Textile Chemicals market captured the largest revenue share of 81% within North America in 2025, fueled by the presence of leading textile chemical manufacturers, significant domestic textile production, and innovation in performance and technical fabrics. U.S. textile processors are increasingly adopting silicone-based softeners, emulsions, and specialty finishes to meet evolving consumer demands for comfort, aesthetics, and functionality in fashion and activewear. The surge in demand for smart textiles, wearable technology, and high-durability fabrics in sectors like healthcare, military, and sports is further stimulating market growth. Additionally, government support for sustainable manufacturing and increasing adoption of water-saving, low-VOC formulations are boosting the use of silicone textile chemicals.

Canada Silicone Textile Chemicals Market Insight

The Canada Silicone Textile Chemicals market is experiencing steady growth, contributing significantly to North America's overall market performance. This growth is driven by rising demand for high-quality, functional textiles across both consumer and industrial segments. Canadian textile manufacturers are increasingly adopting silicone-based chemicals to improve fabric softness, durability, and performance, especially in home textiles, winter apparel, and technical fabrics suited for extreme weather conditions. The market is further supported by growing awareness around sustainable and eco-friendly chemical alternatives, as Canadian regulatory bodies and consumers increasingly favor low-VOC, non-toxic formulations. The expanding local production of niche and high-performance textiles, combined with increased investments in R&D and green chemistry initiatives, is positioning Canada as a growing contributor to the Silicone Textile Chemicals industry in North America.

Mexico Silicone Textile Chemicals Market Insight

The Mexico Silicone Textile Chemicals market is emerging as a key growth area within North America, driven by the expansion of the country’s textile and garment manufacturing sector and increasing foreign investments in production facilities. Mexican textile producers are adopting silicone-based chemicals to enhance fabric softness, elasticity, and finishing quality—particularly for apparel and denim, which are major export categories. The market is supported by Mexico’s strategic trade agreements (e.g., USMCA), proximity to the U.S., and the relocation of manufacturing from Asia to North America (nearshoring), which is increasing demand for advanced textile processing solutions. Government incentives for industrial modernization and growing awareness around sustainable textile practices are encouraging manufacturers to shift toward eco-friendly silicone formulations that improve operational efficiency and reduce environmental impact.

Silicone Textile Chemicals Market Share

The Silicone Textile Chemicals industry is primarily led by well-established companies, including:

- Mitsubishi Chemical Corporation (Japan)

- Shin‑Etsu Chemical Co., Ltd. (Japan)

- Huntsman International LLC (U.S.)

- Wacker Chemie AG (Germany)

- Momentive (U.S.)

- Evonik Industries AG (Germany)

- Elkem ASA (Norway)

- NICCA U.S.A. Inc. (U.S.)

- Piedmont Chemical Industries (U.S.)

- CHT Germany GmbH (Germany)

- Weifang Ruiguang Chemical Co., Ltd. (China)

- zxchem group (China)

- Dow (U.S.)

- Nouryon (Netherlands)

Latest Developments in North America Silicone Textile Chemicals Market

- In January 2023, Dow Inc., a leading chemical producer, introduced the SILASTIC™ SA 994X LSR series, an innovative line of liquid silicone rubbers designed for two-component injection molding with thermoplastic substrates. While primarily targeting the mobility and transportation industries, this development underscores Dow's commitment to advancing silicone technologies, which can have cross-industry applications, including in textile processing

- In 2023, Wacker Chemie AG expanded its silicone production capacities in North America to meet the growing demand for high-performance silicone products. This strategic move aims to enhance the supply chain for silicone-based chemicals, including those used in textile applications, thereby supporting the regional textile industry's need for advanced finishing agents

- In 2023, Shin-Etsu Chemical Co., Ltd. reported increased investments in research and development within North America, aiming to innovate silicone products tailored for textile applications. The company's focus includes creating silicone chemicals that enhance fabric properties such as softness, elasticity, and water repellency, aligning with market demands for high-quality textile finishes

- Archroma, a global color and specialty chemicals company, in 2023, expanded its portfolio of silicone-based textile chemicals in North America. The expansion includes eco-friendly silicone softeners and emulsions designed to improve fabric feel and performance, reflecting Archroma's commitment to sustainable and innovative solutions in the textile industry

- Momentive Performance Materials Inc. announced in 2023 the development of new silicone-based textile finishing agents that offer improved softness and durability. These innovations are part of Momentive's efforts to cater to the evolving requirements of the textile industry, focusing on enhancing fabric performance while maintaining environmental compliance

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

North America Silicone Textile Chemicals Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its North America Silicone Textile Chemicals Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as North America Silicone Textile Chemicals Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.