North America Smoke Detector Market

Market Size in USD Billion

USD

1.11 Billion

USD

2.19 Billion

2025

2033

USD

1.11 Billion

USD

2.19 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.11 Billion | |

| USD 2.19 Billion | |

| % | |

|

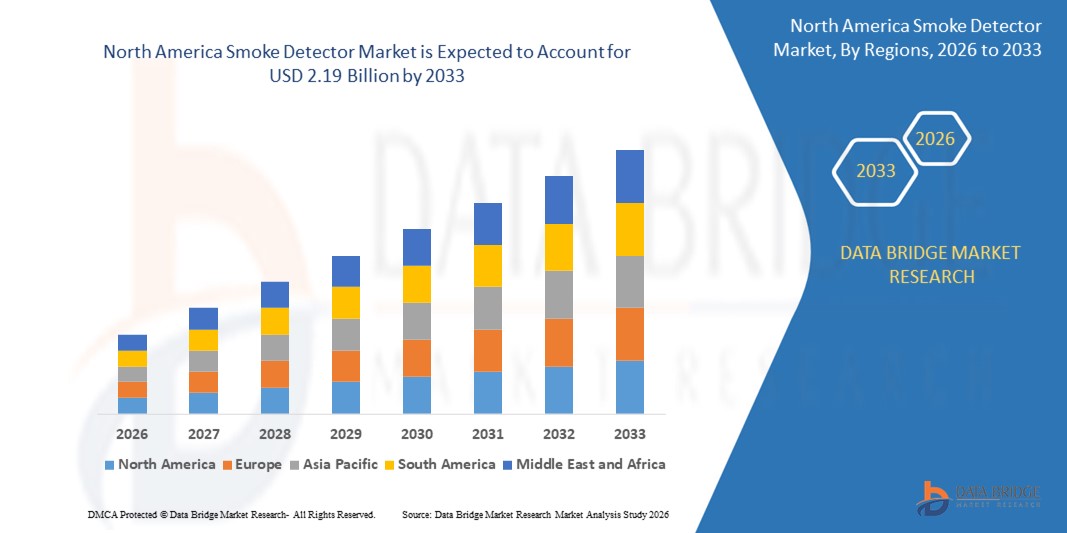

North America Smoke Detector Market Size

- The North America smoke detector market size was valued at USD 1.11 billion in 2025 and is expected to reach USD 2.19 billion by 2033, at a CAGR of 8.9% during the forecast period

- The market growth is largely fueled by the increasing adoption of smart and connected fire safety solutions, as well as technological advancements in smoke detection systems, leading to enhanced safety and digitalization in both residential and commercial environments

- Furthermore, rising awareness of fire hazards, stricter government safety regulations, and growing consumer demand for reliable, easy-to-install, and integrated smoke detection solutions are driving adoption. These converging factors are accelerating the uptake of advanced smoke detectors, thereby significantly boosting the industry’s growth

North America Smoke Detector Market Analysis

- Smoke detectors, offering early warning and fire monitoring capabilities, are becoming essential components of modern building safety systems in homes, offices, and industrial facilities due to their improved sensitivity, real-time alerts, and compatibility with smart building and IoT systems

- The escalating demand for smoke detectors is primarily fueled by increasing safety concerns among consumers and businesses, the growing emphasis on workplace and residential fire safety, and the preference for smart, automated systems that provide timely alerts and reduce property damage

- U.S. dominated the smoke detector market in 2025, due to strong adoption of smart home technologies, extensive commercial and residential construction, and increasing investments in advanced fire safety solutions across buildings, healthcare, and industrial sectors

- Canada is expected to be the fastest growing country in the smoke detector market during the forecast period due to rising adoption of smart building solutions, modernization of residential and commercial infrastructure, and growing awareness of fire safety standards

- Photoelectric smoke detector segment dominated the market with a market share of 43.2% in 2025, due to its superior performance in detecting slow-smoldering fires and reduced false alarms in residential environments. Photoelectric detectors are preferred in homes, offices, and hospitality spaces for their accuracy and compatibility with smart home systems. The market also sees demand due to advancements in wireless connectivity and integration with mobile apps, allowing remote alerts and monitoring for enhanced safety

Report Scope and Smoke Detector Market Segmentation

|

Attributes |

Smoke Detector Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

North America Smoke Detector Market Trends

Increasing Adoption of IoT-Enabled and Smart Smoke Detectors

- A notable trend in the smoke detector market is the rising integration of IoT-enabled and smart devices that provide real-time alerts, remote monitoring, and automated safety responses. This shift is driven by growing consumer preference for connected home safety solutions and industrial adoption for facility monitoring

- For instance, Nest (Google) offers smart smoke and CO alarms that connect with mobile apps and home automation systems, allowing users to receive instant notifications and control devices remotely. Such smart solutions enhance fire safety management and provide actionable insights for both residential and commercial environments

- The integration of advanced sensors, including photoelectric and ionization technologies, is enhancing detection accuracy and reducing false alarms. This trend is positioning smart smoke detectors as essential components in intelligent building and home safety ecosystems

- Emerging features such as voice alerts, integration with smart speakers, and adaptive sensitivity are accelerating adoption among tech-savvy consumers. These functionalities make smoke detectors more user-friendly and improve overall responsiveness to potential fire hazards

- Industrial and commercial sectors are increasingly deploying networked smoke detectors to meet safety compliance standards and support centralized monitoring. This trend strengthens fire prevention strategies in large-scale operations, warehouses, and critical infrastructure

- The market is witnessing growth in devices with combined fire, smoke, and gas detection capabilities, providing comprehensive hazard management. This consolidation of functionalities is reinforcing the transition toward smarter, more interconnected safety systems

North America Smoke Detector Market Dynamics

Driver

Rising Awareness of Fire Safety and Regulatory Compliance

- Increasing focus on fire safety awareness and stringent regulatory standards is driving demand for advanced smoke detection systems across residential, commercial, and industrial sectors. Governments and organizations are emphasizing compliance with building codes and fire prevention protocols

- For instance, Kidde manufactures smoke alarms compliant with NFPA standards, promoting safer living spaces and industrial facilities. These solutions encourage proactive fire safety management and adoption of certified safety devices

- Growing public campaigns and insurance incentives are motivating property owners to upgrade traditional detectors to smart and interconnected systems. These initiatives enhance community safety and minimize potential property losses

- Companies and institutions are investing in integrated safety systems that combine smoke detection with emergency lighting, sprinklers, and evacuation alerts. This holistic approach strengthens overall preparedness and reduces risk exposure

- The rising adoption of fire safety technologies in high-risk environments such as hospitals, data centers, and industrial plants is reinforcing this driver. Advanced smoke detection is increasingly viewed as an essential compliance and safety measure

Restraint/Challenge

High Initial Cost and Installation Complexity of Advanced Systems

- The smoke detector market faces challenges from the higher upfront costs associated with smart and IoT-enabled devices, which are significantly more expensive than conventional detectors. Installation often requires professional services, network integration, and compatibility with existing systems

- For instance, First Alert smart detectors often require complex setup with wireless networks, hub connections, and app configurations. This complexity can delay adoption among cost-sensitive residential and small commercial users

- Advanced sensors and multi-functional devices increase both material and labor costs during production and deployment. These factors create barriers to large-scale adoption, especially in emerging markets

- Maintaining connectivity, software updates, and regular battery replacement add to operational complexity, limiting user convenience. These operational requirements can deter users from replacing legacy detectors

- Balancing affordability with technological sophistication continues to challenge manufacturers. The market must optimize device pricing and simplify installation processes to accelerate adoption while ensuring reliable fire safety coverage

North America Smoke Detector Market Scope

The market is segmented on the basis of power source, product type, service, and end use.

- By Power Source

On the basis of power source, the smoke detector market is segmented into battery powered, hardwired with battery backup, and hardwired without battery backup. The battery-powered segment dominated the market with the largest revenue share in 2025, driven by its ease of installation, portability, and suitability for retrofit applications in residential and commercial buildings. Battery-powered smoke detectors are preferred by homeowners and small businesses for their independence from electrical wiring, reducing installation complexity and downtime. The rising demand is also fueled by advances in long-life lithium batteries and smart monitoring features that alert users about low battery levels, enhancing safety and convenience.

The hardwired with battery backup segment is anticipated to witness the fastest growth from 2026 to 2033, fueled by adoption in commercial, industrial, and high-rise residential buildings. For instance, Honeywell’s combination detectors integrate hardwiring with battery backup, ensuring uninterrupted operation during power outages and offering seamless integration with building management systems. These detectors appeal to developers and facility managers who prioritize reliability, compliance with safety codes, and reduced maintenance interventions. Their growing popularity in smart building setups contributes to accelerating market growth, supported by incentives for safety-standard compliance.

- By Product Type

On the basis of product type, the smoke detector market is segmented into photoelectric smoke detectors, ionization smoke detectors, dual sensor smoke detectors, and others. The photoelectric smoke detector segment dominated the market with the largest revenue share of 43.2% in 2025, driven by its superior performance in detecting slow-smoldering fires and reduced false alarms in residential environments. Photoelectric detectors are preferred in homes, offices, and hospitality spaces for their accuracy and compatibility with smart home systems. The market also sees demand due to advancements in wireless connectivity and integration with mobile apps, allowing remote alerts and monitoring for enhanced safety.

The dual sensor smoke detector segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing adoption across commercial and industrial applications. For instance, First Alert’s dual sensor detectors combine photoelectric and ionization technologies, providing comprehensive detection against both fast-flaming and smoldering fires. This versatility attracts end users seeking higher reliability and reduced risk of property damage, especially in large buildings and facilities with mixed-risk areas. Enhanced connectivity features and compliance with stringent safety standards further fuel growth for this segment.

- By Service

On the basis of service, the smoke detector market is segmented into engineering services, installation and design services, maintenance services, managed services, and other services. The installation and design services segment dominated the market with the largest revenue share in 2025, driven by the increasing complexity of modern fire safety systems and regulatory mandates requiring professional deployment. Businesses and residential complexes rely on expert services to ensure optimal placement, integration with building management systems, and adherence to local fire codes. The market also benefits from bundled offerings by service providers, combining installation with system testing and compliance certification.

The maintenance services segment is anticipated to witness the fastest growth from 2026 to 2033, fueled by the need for periodic testing, battery replacement, and calibration of advanced smoke detection systems. For instance, Johnson Controls provides scheduled maintenance services that ensure continuous operational efficiency and early fault detection. Facilities with high fire risk or regulatory oversight increasingly invest in maintenance contracts to avoid liability, extend detector lifespan, and integrate predictive alerts for safety management. This sustained service demand drives revenue growth across residential, commercial, and industrial sectors.

- By End Use

On the basis of end use, the smoke detector market is segmented into commercial, residential, oil and gas and mining, transportation and logistics, telecommunication, manufacturing, and others. The residential segment dominated the market with the largest revenue share in 2025, driven by heightened awareness of home fire safety, smart home integration, and regulatory encouragement for installing detectors in new constructions. Homeowners prioritize residential smoke detectors for early warning capabilities, ease of use, and remote monitoring features compatible with smartphones. Market growth is also supported by government campaigns and insurance incentives promoting residential fire safety adoption.

The commercial segment is expected to witness the fastest growth from 2026 to 2033, fueled by expanding office spaces, hospitality, and retail sectors requiring large-scale fire detection coverage. For instance, Siemens offers commercial-grade smoke detection systems with centralized monitoring and integration with emergency response protocols. Businesses increasingly invest in scalable solutions that combine advanced detection, minimal false alarms, and regulatory compliance, driving rapid adoption. The growing emphasis on workplace safety, insurance compliance, and smart building technologies further accelerates growth in this segment.

North America Smoke Detector Market Regional Analysis

- U.S. dominated the smoke detector market with the largest revenue share in 2025, driven by strong adoption of smart home technologies, extensive commercial and residential construction, and increasing investments in advanced fire safety solutions across buildings, healthcare, and industrial sectors

- The demand for IoT-enabled, interconnected, and multi-sensor smoke detectors is supported by well-established infrastructure, growing emphasis on regulatory fire safety compliance, and increasing integration of smart building systems for real-time monitoring and hazard prevention

- The presence of major fire safety solution providers, extensive urban and industrial development, and ongoing modernization of residential and commercial properties reinforce the U.S. leadership position in the North America smoke detector market

Canada Smoke Detector Market Insight

Canada is projected to register the fastest CAGR in the North America smoke detector market from 2026 to 2033, supported by rising adoption of smart building solutions, modernization of residential and commercial infrastructure, and growing awareness of fire safety standards. Expanding urban development and investments in healthcare, commercial, and industrial facilities are driving demand for advanced smoke detection systems. Increasing deployment of IoT-enabled detectors, networked safety systems, and predictive alert solutions is accelerating market growth, positioning Canada as the fastest-growing country in the region during the forecast period.

Mexico Smoke Detector Market Insight

Mexico is expected to grow steadily from 2026 to 2033, driven by gradual modernization of residential, commercial, and industrial buildings and increasing adoption of automated fire detection systems. Growing deployment of smoke detectors for real-time hazard monitoring, integrated safety management, and regulatory compliance supports consistent demand. Infrastructure improvements, urbanization, and focus on fire safety awareness contribute to sustained growth of the smoke detector market throughout the forecast period.

North America Smoke Detector Market Share

The smoke detector industry is primarily led by well-established companies, including:

- Honeywell International, Inc. (U.S.)

- Siemens (Germany)

- ABB (Switzerland)

- Schneider Electric (France)

- Carrier (U.S.)

- Analog Devices, Inc. (U.S.)

- Emerson Electric Co. (U.S.)

- Robert Bosch GmbH (Germany)

- Apollo Fire Detectors Ltd. (U.K.)

- Mircom Group of Companies (Canada)

- BRK Brands, Inc. (U.S.)

- Johnson Controls (Ireland)

- HOCHIKI Corporation (Japan)

- SECOM CO., LTD (Japan)

- Protec Fire & Security Group Ltd (U.K.)

- ADT INC (U.S.)

- Securiton AG (Switzerland)

Latest Developments in North America Smoke Detector Market

- In January 2025, Amazon's Ring announced a partnership with fire safety product manufacturer Kidde to launch a connected smoke alarm at the Consumer Electronics Show in Las Vegas. This collaboration is expected to enhance Ring's presence in the smart home safety market by integrating advanced fire detection features with IoT connectivity. The new solution allows real-time alerts, remote monitoring, and integration with other smart home devices, thereby driving demand for connected fire safety solutions and intensifying competition in the rapidly growing IoT-enabled smoke detector segment

- In July 2023, Hikvision India launched a new range of standalone smoke and gas detectors, including two models in the Photoelectric Smoke Detector category—HF-S2E Eco and NP-FY200. The company also introduced the HF-GM100 Carbon Monoxide Gas Detector for the Indian market. This expansion is expected to strengthen Hikvision's position in India’s fire safety sector by providing advanced, cost-effective solutions that meet growing regulatory standards. By offering accessible, high-performance detectors, Hikvision aims to increase market penetration, consumer trust, and adoption across residential and commercial environments

- In January 2023, Siemens launched two new aspirating smoke detectors (ASD), FDA261 and FDA262, designed for challenging fire safety environments such as large data centers, e-commerce warehouses, and industrial manufacturing sites. These detectors offer coverage of up to 6,700 m², currently the largest in the market, and up to 2,000 m² in Class A installations with high sensitivity. Their wide-area detection capability positions Siemens as a leader in advanced fire detection solutions, catering to sectors that demand large-scale, high-performance systems and improving the company’s market share in industrial and commercial fire safety

- In April 2021, Siemens AG's Smart Infrastructure segment launched Cerberus FIT, aimed at enhancing fire safety in small to medium-sized buildings. The system expands functionality and simplifies installation, enabling quick deployment, minimal maintenance, and reliable protection. This launch strengthens Siemens’ offerings for compact building environments, ensuring improved safety standards, faster adoption, and broader market coverage in residential and small commercial spaces

- In March 2021, Johnson introduced the 700 Series, its first microprocessor-based conventional fire detector, transforming the smoke detector market for small commercial buildings. This detector uses advanced algorithms to accurately monitor fire conditions, providing high detection performance while minimizing false alarms. Its introduction represents a step forward in precision fire monitoring technology, enhancing building safety, operational efficiency, and Johnson’s competitive position in the commercial fire detection segment

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.