North America Snack Food Packaging Market

Market Size in USD Billion

USD

6.57 Billion

USD

9.75 Billion

2025

2033

USD

6.57 Billion

USD

9.75 Billion

2025

2033

| 2026 - 2033 | |

| USD 6.57 Billion | |

| USD 9.75 Billion | |

| % | |

|

North America Snack Food Packaging Market Overview

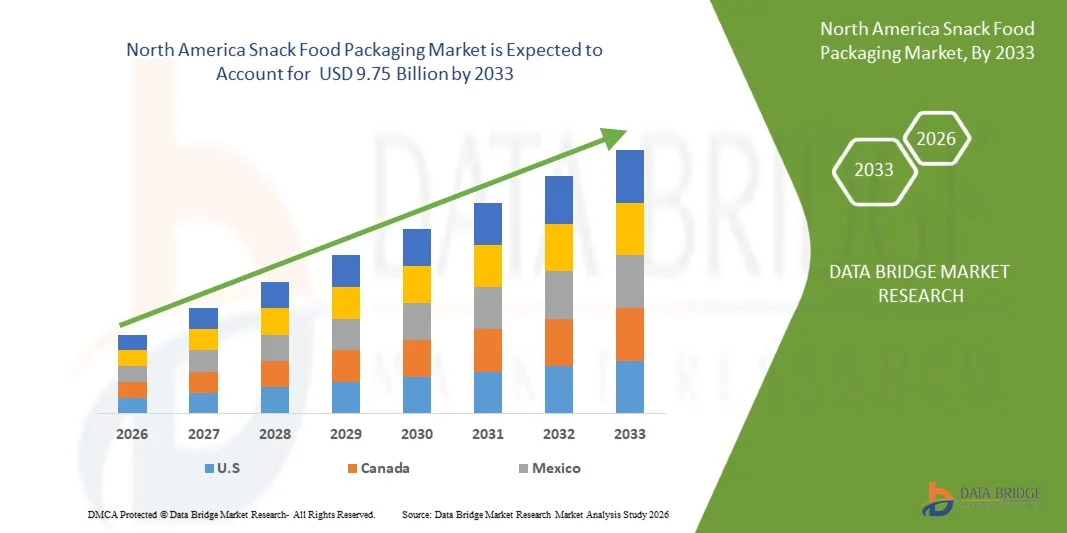

The North America snack food packaging market was valued at USD 6.57 billion in 2025 and is projected to reach USD 9.75 billion by 2033, growing at a CAGR of 5.2% from 2026 to 2033. The market is driven by strong demand for convenient and on-the-go snack products across the U.S., Canada, and Mexico, coupled with increasing consumer preference for sustainable packaging solutions.

Sustainability has become a key transformation factor in the North American snack food packaging industry. Stringent environmental regulations, corporate sustainability initiatives, and growing consumer awareness regarding packaging waste are accelerating the adoption of recyclable, recycled-content, compostable, paper-based, and mono-material packaging formats. Manufacturers are increasingly focusing on lightweight packaging designs that reduce material usage while maintaining product freshness, shelf life, and protection.

The region is witnessing significant investments in recycling infrastructure, circular economy programs, and advanced packaging technologies to support sustainability goals. Additionally, the integration of digital printing, smart labeling, QR-code-enabled packaging, and automation technologies is enhancing operational efficiency, supply chain transparency, and consumer engagement. The rising popularity of healthy snacks, single-serve packaging, and e-commerce distribution channels is further influencing packaging innovation across North America. As snack consumption continues to grow throughout the region, the market is evolving toward packaging solutions that effectively balance functionality, sustainability, convenience, product safety, and cost efficiency.

Market Size & Forecast

- North America Market Value (2025): USD 6.57 Billion

- Expected Market Value (2033): USD 9.75 Billion

- Forecast CAGR (2026–2033): 5.2%

- Leading Region in 2025: U.S.

- Fastest Growing Region: Mexico

Key Market Trends & Insights

- S. dominated the North America snack food packaging market with the largest revenue share of 69.67% in 2025, due to its large packaged snack industry, high consumer spending on convenience foods, and strong presence of leading snack food manufacturers and packaging companies. The country's well-established retail infrastructure, expanding e-commerce sector, and continuous demand for innovative snack formats further support packaging consumption across multiple product categories.

- The flexible packaging segment led the market with a 66.36% share in 2025, driven by its lightweight nature, cost-effectiveness, superior barrier properties, and suitability for on-the-go snack consumption. Flexible packaging also offers enhanced design flexibility, reduced transportation costs, and lower material usage compared to rigid alternatives, making it the preferred choice for manufacturers seeking both efficiency and sustainability.

- Mexico is expected to be the fastest-growing region at a CAGR of 6.0% from 2026 to 2033, fueled by rising urbanization, expanding middle-class populations, increasing consumption of packaged snacks, and growth in modern retail channels. Investments in food processing facilities and the growing presence of international snack brands are also creating significant opportunities for packaging suppliers in the country.

- Flexible packaging is the fastest-growing packaging type, projected to register a CAGR of 5.4%, reflecting the increasing demand for resealable, portable, and sustainable packaging formats that enhance product convenience and shelf life. Technological advancements in film structures and mono-material packaging solutions are further accelerating adoption among snack food manufacturers.

- The plastic segment dominates the packaging material category with a 54.00% revenue share in 2025, led by its durability, moisture resistance, lightweight characteristics, and ability to provide effective product protection at competitive costs. Plastic materials continue to play a critical role in preserving product quality and extending shelf life, particularly for chips, nuts, confectionery products, and other moisture-sensitive snacks.

- Heat seal segment accounts for 43.44% of the market, preferred for its strong sealing performance, extended product freshness, tamper-evident properties, and compatibility with high-speed packaging operations. Its widespread use across flexible pouches, bags, and sachets makes it an essential sealing technology for maintaining product integrity throughout distribution and storage.

- The paper & paperboard segment is the fastest-growing packaging material category, with a CAGR of 5.9%, driven by increasing consumer preference for environmentally friendly packaging, regulatory support for sustainable materials, and advancements in recyclable and compostable packaging technologies. Brand owners are increasingly incorporating paper-based solutions into their packaging portfolios to meet sustainability targets and strengthen their environmental credentials among eco-conscious consumers.

Report Scope and North America Snack Food Packaging Market Segmentation

|

Attributes |

North America Snack Food Packaging Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

North America Snack Food Packaging Market Trends

Trend: Growing Adoption of Sustainable, Recyclable, and Eco-Friendly Packaging Solutions

The increasing adoption of sustainable, recyclable, and eco-friendly packaging solutions is creating a significant growth opportunity for the global snack food packaging market. Consumers, retailers, food manufacturers, and regulatory authorities are placing greater emphasis on reducing packaging waste, lowering carbon footprints, and improving recyclability. Snack food brands are therefore investing in paper-based packaging, mono-material recyclable films, post-consumer recycled (PCR) plastics, compostable materials, and fiber-based alternatives to conventional multi-layer plastics. These innovations are helping manufacturers meet sustainability commitments while enhancing brand value and consumer trust. Furthermore, advancements in barrier technologies are enabling sustainable materials to provide the shelf-life protection required for snacks such as chips, nuts, granola bars, confectionery products, and baked goods. As governments worldwide introduce circular economy initiatives and extended producer responsibility (EPR) regulations, packaging companies that can deliver recyclable and resource-efficient solutions are gaining a competitive advantage. This transition is expected to accelerate demand for innovative snack food packaging formats and materials over the coming years.

North America Snack Food Packaging Market Dynamics

Key Market Driver: Increasing Demand for Convenience and Ready-To-Eat Snack Products

The growing consumer preference for convenience foods and ready-to-eat (RTE) snack products is a major factor driving demand in the global snack food packaging market. Rapid urbanization, increasingly busy lifestyles, rising workforce participation, and the expansion of on-the-go consumption habits have led consumers to seek snack products that are portable, easy to store, and ready for immediate consumption. This shift has encouraged food manufacturers to introduce a wider range of packaged snacks, including healthy snacks, protein snacks, chips, nuts, trail mixes, and meal-replacement products. As a result, packaging has become a critical component in ensuring product freshness, shelf-life extension, portability, convenience, and brand differentiation. Demand is increasing for resealable pouches, single-serve packs, lightweight flexible packaging, tamper-evident formats, and sustainable packaging solutions that enhance consumer convenience while maintaining product quality throughout distribution and retail channels.

The increasing popularity of convenience foods and ready-to-eat snack products is significantly accelerating growth in the global snack food packaging market. As consumers seek portable, shelf-stable, and easy-to-consume food options, manufacturers are investing in packaging solutions that enhance freshness, convenience, safety, and sustainability. Recent product launches, packaging innovations, and expanding snack portfolios across the food industry demonstrate how evolving consumption patterns are creating sustained demand for advanced snack food packaging formats worldwide.

Key Restraint/Challenge: Fluctuations in Raw Material Costs Impacting Production Economics

The snack food packaging market faces a significant restraint from fluctuations in raw material costs, which directly impact packaging production economics and profitability. Snack food packaging relies heavily on materials such as polyethylene (PE), polypropylene (PP), polyethylene terephthalate (PET), aluminum foil, paperboard, and recycled fiber, all of which are subject to volatility driven by crude oil prices, energy costs, geopolitical tensions, supply chain disruptions, trade policies, and changing demand-supply dynamics. Because packaging manufacturers often operate under long-term supply contracts with food companies, sudden increases in raw material prices can compress margins before cost increases can be passed on to customers. In addition, unpredictable material pricing makes procurement planning, inventory management, and investment decisions more challenging for packaging producers. For snack food manufacturers, higher packaging costs can increase overall product costs, reduce profitability, and potentially lead to price increases that affect consumer demand. As a result, ongoing volatility in resin, paper, and metal markets continues to create uncertainty across the snack food packaging value chain and acts as a restraint on market growth.

Fluctuating prices of resins, paperboard, aluminum, and other packaging substrates remain a major challenge for the global snack food packaging market. Volatility driven by inflation, energy prices, geopolitical tensions, trade policies, and supply-chain disruptions increases production costs, complicates procurement planning, and creates margin pressure for packaging manufacturers. As raw material uncertainty persists, both packaging suppliers and snack food producers must continuously adjust pricing, sourcing, and inventory strategies, making raw material cost fluctuations a significant restraint on the market’s long-term growth and profitability.

Key Market Opportunity: Advancements in Smart Packaging Technologies for Enhanced Consumer Interaction and Product Traceability

The growing adoption of smart packaging technologies is creating a significant opportunity for the snack food packaging market by transforming packaging from a passive protective medium into an interactive communication and traceability platform. Technologies such as QR codes, NFC (Near Field Communication), RFID tags, GS1 Digital Link-enabled 2D barcodes, augmented reality (AR), and cloud-connected packaging solutions allow snack manufacturers to engage consumers directly through smartphones while simultaneously improving supply chain visibility. Consumers increasingly seek transparency regarding ingredient sourcing, nutritional content, sustainability practices, and product authenticity. Smart packaging enables brands to provide this information instantly through digital interfaces, enhancing trust and brand loyalty. Furthermore, regulators and retailers are placing greater emphasis on product traceability and transparency, encouraging the adoption of connected packaging systems that can track products across the supply chain. For snack food companies, these technologies create opportunities for personalized marketing campaigns, loyalty programs, real-time consumer feedback, anti-counterfeiting measures, recall management, and sustainability communication. As digitalization becomes a core element of food packaging strategies, smart packaging is expected to emerge as a key differentiator that enhances consumer experience while delivering operational efficiencies and traceability benefits.

The convergence of consumer expectations, digital transformation initiatives, and evolving traceability requirements is expected to accelerate the deployment of smart packaging solutions across the snack food industry, supporting both brand value creation and operational efficiency.

North America Snack Food Packaging Market Scope

The North America snack food packaging market is segmented on the basis of packaging type, packaging material, closure type, barrier property, pack size, label type, packaging technology, application, and distribution channel.

- By Packaging Type

On the basis of packaging type, the North America snack food packaging market is segmented into flexible packaging, rigid packaging, secondary & multipack packaging, and semi-rigid packaging. The flexible packaging segment led the market with a 66.36% share in 2025, driven by its cost-effectiveness, lightweight nature, superior barrier properties, and ability to extend product shelf life. In North America, strong demand for convenient, on-the-go snack products and the widespread adoption of pouches, sachets, and wraps by leading snack manufacturers have significantly contributed to segment growth. Additionally, flexible packaging supports sustainability goals through reduced material consumption and lower transportation costs, further strengthening its market dominance.

Flexible packaging is the fastest-growing packaging type, projected to register a CAGR of 5.4% from 2026 to 2033. Growth is supported by increasing demand for resealable, portable, and portion-controlled packaging formats among consumers in the U.S., Canada, and Mexico. The growing emphasis on recyclable mono-material structures, e-commerce-ready packaging, and enhanced product convenience is expected to accelerate adoption across the regional snack food industry.

- By Packaging Material

On the basis of packaging material, the market is segmented into plastic, paper & paperboard, laminates & composites, bio-based/sustainable materials, metal, and glass. The plastic segment dominated the market with a 54.00% share in 2025, owing to its excellent barrier properties, lightweight nature, durability, and cost-effectiveness. Plastic packaging remains widely used across North America's snack food industry because it effectively protects products against moisture, oxygen, and contamination while supporting long shelf life and product freshness. Its compatibility with advanced manufacturing processes and high-quality printing capabilities also makes it an attractive choice for major snack brands.

The paper & paperboard segment is the fastest-growing packaging material category, with a CAGR of 5.9%, driven by increasing consumer preference for environmentally sustainable packaging and growing regulatory scrutiny of single-use plastics across North America. Major food companies are actively incorporating paper-based packaging into their sustainability strategies, while advancements in barrier coatings and recyclable packaging technologies continue to improve functionality and commercial viability.

- By Closure Type

On the basis of closure type, the market is segmented into heat seal, zipper/resealable, tamper-evident seals, pull-tab/tear-off, snap-on lids, and press-fit caps. The heat seal segment led the market with a 43.44% share in 2025, supported by its superior sealing strength, ability to maintain product freshness, and effectiveness in protecting snack products from moisture and oxygen exposure. Its widespread compatibility with flexible packaging formats and high-speed production lines has made it the preferred closure method among North American snack manufacturers.

The zipper/resealable segment is expected to experience the fastest growth at a CAGR of 5.8% from 2026 to 2033, driven by increasing consumer demand for convenience and freshness preservation. As households increasingly purchase larger snack packs and consume products over multiple occasions, resealable packaging is gaining popularity across categories such as chips, nuts, trail mixes, and popcorn. The trend toward premium packaging experiences is also supporting segment growth.

- By Barrier Property

On the basis of barrier property, the market is segmented into high barrier, medium barrier, active & modified atmosphere packaging, and low barrier. The high barrier segment dominated the market with a share of 49.01% in 2025 due to its ability to provide superior protection against moisture, oxygen, light, and external contaminants. High-barrier packaging is particularly important in North America, where extensive distribution networks and long transportation distances require packaging solutions that maintain freshness and product quality throughout the supply chain.

The low barrier segment is anticipated to witness the fastest CAGR of 5.8% from 2026 to 2033, driven by increasing demand for lightweight and sustainable packaging solutions. Manufacturers are adopting low-barrier structures for products with shorter shelf-life requirements to reduce material usage and improve recyclability. Growing interest in environmentally friendly packaging solutions is expected to further support segment expansion.

- By Pack Size

On the basis of pack size, the market is segmented into multi-serve packs, single-serve packs, family packs, and bulk/institutional packs. The multi-serve packs segment dominated the market with a share of 38.65% in 2025 due to strong demand from households seeking convenience and value. The popularity of club stores, supermarkets, and bulk purchasing trends across North America has significantly contributed to the growth of larger snack pack formats. Resealable packaging technologies have further enhanced the attractiveness of multi-serve packs by helping preserve freshness after opening.

The single-serve packs segment is expected to witness the fastest CAGR of 5.7% from 2026 to 2033, driven by growing demand for portion-controlled and on-the-go snack options. Busy lifestyles, increasing health awareness, and rising demand for convenient snack products among working professionals and younger consumers are supporting segment growth. Expansion of convenience stores and e-commerce channels is also increasing accessibility to single-serve snack products.

- By Label Type

On the basis of label type, the market is segmented into pressure-sensitive labels (PSL), shrink sleeve labels, wrap-around labels, digital printed labels, smart & interactive labels, and in-mold labels (IML). The pressure-sensitive labels (PSL) segment dominated the market with a 41.45% share in 2025 due to its versatility, cost-effectiveness, and suitability for a broad range of snack packaging applications. PSL technology allows efficient application on high-speed packaging lines while supporting premium branding and product differentiation.

The smart & interactive labels segment is expected to witness the fastest CAGR of 6.0% from 2026 to 2033. Growth is driven by increasing adoption of digital technologies across North America's food and beverage industry. QR codes, NFC-enabled labels, and connected packaging solutions are helping brands improve consumer engagement, provide transparency regarding ingredients and sustainability initiatives, and enhance supply chain traceability.

- By Packaging Technology

On the basis of packaging technology, the market is segmented into thermoforming/form-fill-seal (FFS), modified atmosphere packaging (MAP), blow molding/injection molding, vacuum packaging, and aseptic/retort processing. The modified atmosphere packaging (MAP) segment dominated the market with a share of 41.99% in 2025 due to its ability to significantly extend shelf life while preserving freshness, texture, and flavor. The technology is widely used across North America's snack food sector, where manufacturers prioritize product quality, reduced food waste, and longer distribution capabilities.

The MAP segment is also expected to witness the fastest CAGR of 5.8% from 2026 to 2033, driven by increasing demand for premium snack products, clean-label formulations, and preservative-free packaging solutions. Rising investments in advanced food packaging technologies and growing emphasis on food safety are expected to further support market growth.

- By Application

On the basis of application, the market is segmented into chips & crisps, nuts & seeds, confectionery snack products, extruded snacks, bakery snacks, pretzels & crackers, protein/energy bars, popcorn, functional/specialty snacks, baked snacks, dried fruits, and others. The chips & crisps segment dominated the market with a share of 24.60% in 2025 due to its extensive consumer base and high consumption frequency across North America. The segment generates substantial demand for advanced packaging solutions capable of maintaining crispness, flavor, and freshness throughout distribution and retail display.

The popcorn segment is expected to witness the fastest CAGR of 6.9% from 2026 to 2033, driven by increasing consumer preference for healthier snacking alternatives. Growth in premium, flavored, organic, and ready-to-eat popcorn products is encouraging manufacturers to invest in innovative packaging solutions that enhance product differentiation, sustainability, and shelf appeal.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct and indirect. The direct segment dominated the market with a share of 56.83% in 2025 due to strong partnerships between packaging manufacturers and major snack food producers throughout North America. Direct sales channels facilitate customized packaging development, long-term supply agreements, and efficient coordination on sustainability initiatives and packaging innovation projects.

The indirect segment is expected to witness the fastest CAGR of 5.6% from 2026 to 2033, driven by the expanding network of packaging distributors, converters, and third-party suppliers serving small and medium-sized snack manufacturers. The growth of regional food brands, contract manufacturing operations, and flexible sourcing strategies is expected to increase reliance on indirect sales channels across the North American market.

North America Snack Food Packaging Market Regional Analysis

U.S. dominated the North America snack food packaging market with the largest revenue share of 69.67% in 2025, due to its highly developed packaged food industry, strong presence of leading global snack manufacturers, and advanced packaging manufacturing infrastructure. The country benefits from high consumer demand for convenient, on-the-go snack products, driven by busy lifestyles and a well-established culture of snacking across all age groups.

In addition, the widespread availability of modern retail channels, including supermarkets, hypermarkets, and convenience stores, along with the rapid expansion of e-commerce grocery platforms, has significantly boosted demand for efficient and durable snack packaging solutions. The strong focus on innovation, sustainability initiatives, and adoption of advanced packaging technologies such as flexible packaging, smart labeling, and modified atmosphere packaging further reinforces the U.S. dominance in the regional market.

Mexico Snack Food Packaging Market Insight

The Mexico snack food packaging market is experiencing robust growth, driven by rising urbanization, expanding middle-class income levels, and increasing consumption of packaged and convenience snack products. The rapid expansion of modern retail formats such as supermarkets, hypermarkets, and convenience stores is further accelerating demand for efficient and attractive packaging solutions.

Additionally, the growing influence of Western-style snacking habits, particularly among younger consumers, is boosting demand for on-the-go and portion-controlled packaging formats. The increasing presence of multinational snack brands and investments in local food processing and packaging infrastructure are also strengthening market development.

North America Snack Food Packaging Market Share

The North America snack food packaging industry is primarily led by well-established companies, including:

- Smurfit Westrock plc (Ireland)

- Amcor plc (Switzerland)

- Mondi (U.K.)

- Graphic Packaging International, LLC (U.S.)

- Sonoco Products Company (U.S.)

- Sealed Air Corporation (U.S.)

- Jinan Huafeng Printing Co., Ltd (China)

- Huhtamäki Oyj (Finland)

- SIG Combibloc Group AG (Switzerland)

- Novolex Holdings, LLC (U.S.)

- Constantia Flexibles (Austria)

- ProAmpac LLC (U.S.)

- UFlex Packaging (India)

- Inteplast Group (U.S.)

- Winpak Ltd. (Canada)

- Printpack (U.S.)

- Coveris (Austria)

- Schur Flexibles Group (Austria)

- Gualapack S.p.A. (Italy)

- Nosco, Inc. (U.S.)

- ePac Holdings, LLC (U.S.)

- Glenroy, Inc. (U.S.)

- Dot Packtech (India)

Latest Developments in North America Snack Food Packaging Market

- In April, 2026 Sealed Air Corporation announced the completion of its previously announced acquisition by funds affiliated with CD&R. Sealed Air is now a privately held company, and its shares have ceased trading on the New York Stock Exchange.

- In April 2026, Mondi opened its new packaging production facility in Pittsburgh, Pennsylvania, further expanding its manufacturing capabilities in the U.S. to better support customers with reliable, high-quality paper-based packaging solutions across key end markets. The new state‑of‑the‑art plant produces a wide range of paper bags for customers in the eCommerce, food, feed, building materials, and chemicals sectors.

- In March 2026, Amcor offered an in-depth view of its expanded portfolio of rigid and flexible packaging solutions at Natural Products Expo West in Anaheim, California, at the Anaheim Convention Center from March 4-6, 2026.

- In January 2026, ePac Holdings, has launched Easy Open Barrier Films designed to enhance convenience and performance in premium packaging applications. The new films are engineered with a peelable, easy-open structure that eliminates the need for scissors or tear notches, while maintaining high-barrier protection for freshness and aroma. The solution is primarily targeted at coffee packaging and other high-barrier food applications, supporting better consumer usability and strong product protection in flexible packaging formats. This development will benefit ePac Holdings by strengthening its position in the premium sustainable packaging segment.

- In April 2025, Amcor plc completed the acquisition (combination) of Berry Global on April 30, 2025. The transaction was structured as an all-stock merger, with Berry shareholders receiving 7.25 Amcor shares for each Berry share. After closing, Berry became a wholly owned subsidiary of Amcor.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

North America Snack Food Packaging Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its North America Snack Food Packaging Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as North America Snack Food Packaging Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.